Lessons from Chris Douvos

Chris Douvos, founder of Ahoy Capital, is a veteran limited partner who backed the micro-VC movement early on. He is known for arguing that "size is the enemy of performance" and pushing for transparency in venture allocation through the #OpenLP initiative. This collection covers his core principles on fund construction, the realities of emerging managers, and the mechanics of venture returns.

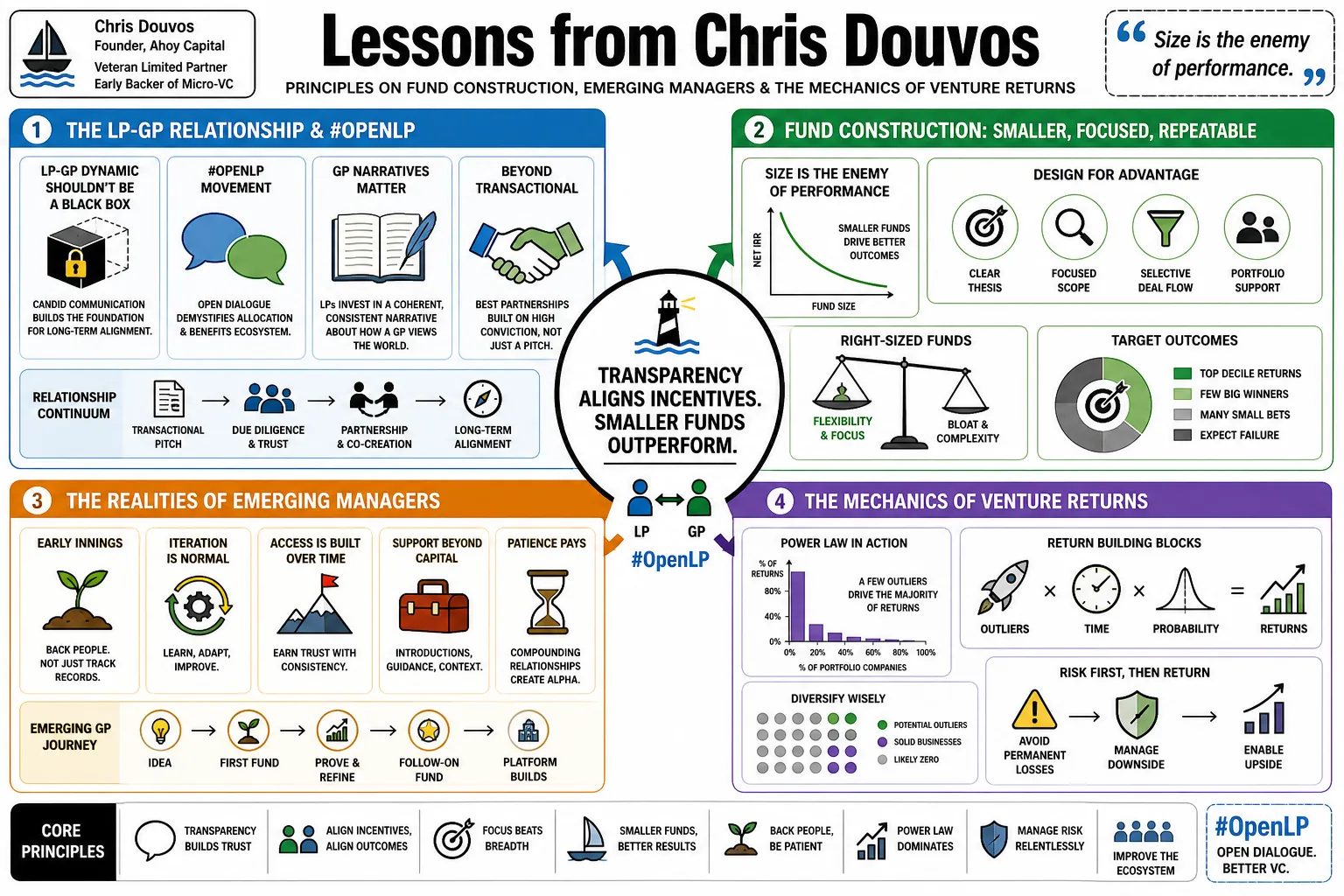

Part 1: The LP-GP Relationship & #OpenLP

- On Transparency: "The LP-GP dynamic shouldn't be a black box; candid communication builds the foundation for long-term alignment." — Source: Ahoy Capital

- On the #OpenLP Movement: "Fostering an open dialogue between Limited Partners and General Partners demystifies the allocation process and benefits the entire ecosystem." — Source: Capital Allocators

- On GP Narratives: "LPs don't just invest in numbers; they invest in a coherent, consistent narrative about how a GP views the world." — Source: Cup of Zhou

- On Transactional Relationships: Douvos frames the best LP-GP relationships as long-game partnerships: the AdvancingVC episode emphasizes enduring firms, long-term alignment, and support for breakthrough managers over transactional fundraising moments. — Reference: AdvancingVC episode summary on enduring firms, LP-GP relationships, and high-conviction venture craftsmanship

- On the Principal-Agent Problem: "You have to constantly guard against the principal-agent problem in finance; alignment of incentives is everything." — Source: Swimming with Allocators

- On Bad News: "GPs should share bad news early. LPs hate surprises far more than they hate setbacks." — Source: Superclusters

- On LP Empathy: "Understanding what keeps your LP awake at night is as important as understanding the startups you back." — Source: 10X Capital Podcast

- On Fund Reporting: "A glossy quarterly report can't replace the trust built through authentic, unvarnished conversations." — Source: Capital Allocators

- On Reference Calls: "The most telling reference calls aren't the ones you orchestrate, but the back-channel conversations that reveal how you act when things go wrong." — Source: Cup of Zhou

Part 2: Fund Sizing & "Diworseification"

- On Performance: "Size is the enemy of performance in venture capital." — Source: Ahoy Capital

- On Right-Sizing: "Funds should be intentionally right-sized to pursue investment excellence, not fee maximization." — Source: Venture Capital Journal

- On Over-Capitalization: Douvos argues that concentration matters for LPs and that too much diversification can become "diworseification"; the Alt Goes Mainstream episode also ties smaller fund sizes to potential outperformance. — Reference: Alt Goes Mainstream episode summary on concentration, diworseification, and smaller fund sizes

- On Micro-VC: "The micro-VC movement emerged because smaller, focused funds have a structural advantage in generating outsized multiples." — Source: PodScripts

- On Strategy Drift: "As AUM grows, there's a gravity that pulls GPs away from their original, sharp-elbowed strategy toward index-like mediocrity." — Source: Capital Allocators

- On Capacity Constraints: "Early-stage venture is a capacity-constrained asset class; you can't just deploy twice as much capital and expect the same returns." — Source: Ahoy Capital

- On Fee Concentration: "A model driven by management fees changes the GP's behavior, shifting focus from carrying interest and true alpha to asset gathering." — Source: Swimming with Allocators

- On Discipline: "The hardest discipline for a successful GP is turning down money to maintain a fund size that actually serves the strategy." — Source: Superclusters

- On The Solo GP: "The Solo GP phenomenon is a direct reaction to the bloat of traditional partnerships, allowing for concentrated, high-conviction bets." — Source: 10X Capital Podcast

- On Deployment Pace: "Raising larger funds often creates an artificial pressure to deploy capital faster, overriding natural market rhythms." — Source: Ahoy Capital

Part 3: Value vs. Perception in Venture

- On The Formula for Opportunity: "Opportunity equals value minus perception." — Source: Innovation Footprints

- On Market Hype: "The venture industry is excellent at inflating perception, but true intrinsic value is much harder to find." — Source: Swimming with Allocators

- On Contrarianism: "To generate alpha, you must be willing to be occasionally wrong and alone in pursuit of being right and alone." — Source: Investing in Startups

- On Price Sensitivity: "As pricing increases across the market, it compresses returns not just for the median companies, but for the big winners too." — Source: Innovation Footprints

- On Heat-Seeking Missiles: "There are so many investors who are just caught up in these tides. They're heat-seeking missiles, looking for the new, new thing." — Source: Cup of Zhou

- On Timing: "The reality is that by the time the new, new thing is new to them, it's already a little bit longer in the tooth in the ecosystem—all the great deals have been done." — Source: Cup of Zhou

- On Fundamentals: "Hype can fund a company for a few rounds, but eventually, the market demands real unit economics and intrinsic value." — Source: Capital Allocators

- On Valuation Discipline: "Valuation discipline isn't about being cheap; it's about protecting the asymmetric upside that venture requires." — Source: Swimming with Allocators

- On Echo Chambers: "The Valley operates as a massive echo chamber where perception often outruns reality for years before correcting." — Source: Ahoy Capital

Part 4: The Realities of Being an Emerging Manager

- On The Hustle: "Being an emerging manager requires a relentless hustle that goes far beyond just picking good companies." — Source: 10X Capital Podcast

- On Specialization: "Generalist emerging managers face a steep uphill battle; you need a sharp wedge or specialized focus to stand out to LPs." — Source: Superclusters

- On Track Records: "An attributed track record from a prior firm is helpful, but LPs are really underwriting your ability to build a firm from scratch." — Source: Capital Allocators

- On Sourcing: "As a new GP, your proprietary sourcing network is your lifeblood; if you're seeing deals when everyone else is, you've already lost." — Source: PodScripts

- On LP Rejection: "Emerging managers must build a high tolerance for rejection; LPs say no for a hundred reasons that have nothing to do with your talent." — Source: Cup of Zhou

- On First Funds: "Fund I is about proving you can access the right deals; Fund II is about proving Fund I wasn't a fluke." — Source: Ahoy Capital

- On Back-Office Operations: "GPs often underestimate the operational burden of running a firm. LPs look closely at your back-office maturity." — Source: Superclusters

- On Co-investments: "Offering co-investment rights can be a powerful tool for emerging managers to attract institutional LPs." — Source: Ahoy Capital

- On Authenticity: "Don't try to mimic established mega-funds. Lean into the agility and hunger that makes emerging managers uniquely dangerous." — Source: 10X Capital Podcast

- On Longevity: Douvos treats firm durability as a central test: the AdvancingVC episode highlights architecture, culture, long-term alignment, and how LPs think about generational transition. — Reference: AdvancingVC episode summary on enduring venture firms, architecture, culture, and generational transition

Part 5: The Power Law & Venture Math

- On Returns: "Venture is fundamentally a power-law business where a tiny fraction of hits drives the vast majority of returns." — Source: Innovation Footprints

- On Portfolio Construction: "You have to construct your portfolio knowing that any single company could go to zero, but you only need one to return the fund multiple times over." — Source: Capital Allocators

- On Entry Prices: "Entry valuations dictate your ultimate multiple. Overpaying for a winner might still yield a return, but it destroys the power-law math." — Source: Ahoy Capital

- On Secondary Sales: "Managing liquidity through secondary sales is an increasingly critical skill for GPs navigating long paths to IPOs." — Source: Superclusters

- On Ownership: "Target ownership percentages aren't just vanity metrics; they are mathematical prerequisites for generating venture-scale returns." — Source: 10X Capital Podcast

- On Pro-rata Rights: "Defending your pro-rata in breakout companies is where funds separate the good from the great." — Source: PodScripts

- On Loss Ratios: "If your loss ratio is zero, you aren't taking enough risk. The math of early-stage venture demands a healthy failure rate." — Source: Capital Allocators

- On Capital Recycling: "Strategic capital recycling can turn a good fund into a top-quartile fund without calling additional capital from LPs." — Source: Cup of Zhou

- On Multiples vs. IRR: "IRR can be gamed with timing, but cash-on-cash multiples are the ultimate truth-teller in venture performance." — Source: Ahoy Capital

Part 6: Firm Building & Culture

- On Principles: "The man who grasps principles can successfully select his own methods. The man who tries methods, ignoring principles, is sure to have trouble." — Source: Innovation Footprints

- On Team Dynamics: "A venture partnership is a fragile ecosystem. Misaligned incentives or egos can destroy a firm faster than bad investments." — Source: Capital Allocators

- On Decision Making: Douvos describes great venture decision-making as high-conviction craftsmanship: AdvancingVC summarizes his focus on moving beyond spray-and-pray investing, knowing how to say no, and building decision cultures around nuance, depth, and originality. — Reference: AdvancingVC episode summary on decision-making, high-conviction craftsmanship, and saying no in venture

- On Mentorship: "Institutional knowledge in venture is passed down through apprenticeship; losing that thread weakens the next generation." — Source: Ahoy Capital

- On GP Commitment: "LPs want to see GPs meaningfully invested in their own funds. Shared pain and shared upside ensure deep alignment." — Source: Swimming with Allocators

- On Differentiation: "If your firm's value proposition is 'we add value,' you don't have a value proposition. It needs to be specific and actionable." — Source: Cup of Zhou

- On Brand Building: "Your brand isn't what you say on your website; it's what founders say about you when you're not in the room." — Source: 10X Capital Podcast

- On Evolving Strategies: "A firm must evolve its strategy as markets shift, but it must do so without abandoning the core principles that made it successful." — Source: Capital Allocators

- On Partnership Equality: "Equal economics in a partnership can foster collaboration, but it requires extreme intellectual honesty about contribution." — Source: Superclusters

Part 7: Avoiding Hype & The Crowd

- On Contrarian Thinking: "True contrarianism looks like a bad idea to most reasonable people until the moment it suddenly becomes obvious." — Source: Investing in Startups

- On Tourist Investors: "When tourist capital floods the market, discipline is the first casualty." — Source: Swimming with Allocators

- On Fear of Missing Out (FOMO): "FOMO is the most destructive force in venture capital. It leads to skipped diligence and compressed timelines." — Source: Ahoy Capital

- On Market Cycles: "Every cycle brings a new wave of investors who believe the old rules no longer apply. They are usually wrong." — Source: Capital Allocators

- On Entrepreneurship: "Entrepreneurship is like a gas. It's hottest when it's compressed." — Source: Cup of Zhou

- On Capital as a Commodity: "When capital becomes commoditized, a GP's only true moat is their network and their judgment." — Source: 10X Capital Podcast

- On Sector Rotation: "Chasing the current hot sector is a surefire way to buy at the top. The best returns come from funding what will be hot in five years." — Source: PodScripts

- On Diligence: "Speed to term sheet is a competitive advantage, but not when it comes at the expense of fundamental underwriting." — Source: Ahoy Capital

- On Staying Grounded: "It's vital to step outside the Silicon Valley echo chamber to maintain an objective view of global technology trends." — Source: Capital Allocators

- On Media Narratives: "The companies that grace magazine covers are rarely the ones driving the best fund returns; they are often priced for perfection." — Source: Swimming with Allocators

Part 8: The "Heartbreak Business" & LP Psychology

- On The Nature of VC: "Venture capital is fundamentally a heartbreak business." — Source: Swimming with Allocators

- On Emotional Resilience: "You will spend most of your time dealing with things that are broken, failing, or struggling. It requires a specific emotional resilience." — Source: Cup of Zhou

- On Founder Empathy: "Recognizing the profound psychological toll on founders makes you a better board member and a better investor." — Source: 10X Capital Podcast

- On LP Patience: "The J-curve is not just a financial concept; it is an emotional valley of death that LPs must be prepared to endure." — Source: Capital Allocators

- On Celebrating Wins: "In a business defined by failure, you have to celebrate the intermediate wins, even if they don't immediately translate to DPI." — Source: Ahoy Capital

- On the Burden of Capital: "Accepting millions of dollars from pensions and endowments is a heavy fiduciary burden that should keep GPs grounded." — Source: PodScripts

- On Intellectual Honesty: "The hardest part of the job is maintaining intellectual honesty when a thesis you loved is clearly not working out." — Source: Swimming with Allocators

- On Enduring Relationships: "The venture business is tiny and memories are long. How you handle the heartbreaks defines your reputation." — Source: Superclusters

- On The Long Game: "True success in this asset class isn't measured in a single fund cycle, but over decades of navigating chaos." — Source: Ahoy Capital