Colin Camerer is an economist who helped establish the fields of behavioral game theory and neuroeconomics by studying how the human brain actually makes decisions. Rather than assuming people are perfectly rational calculating machines, his research uses tools like fMRI and behavioral experiments to map the cognitive limits, social preferences, and biological mechanisms that drive our choices. This profile collects his insights on why standard economic models fail and how real people navigate strategy, risk, and markets.

Part 1: The Limits of Rationality

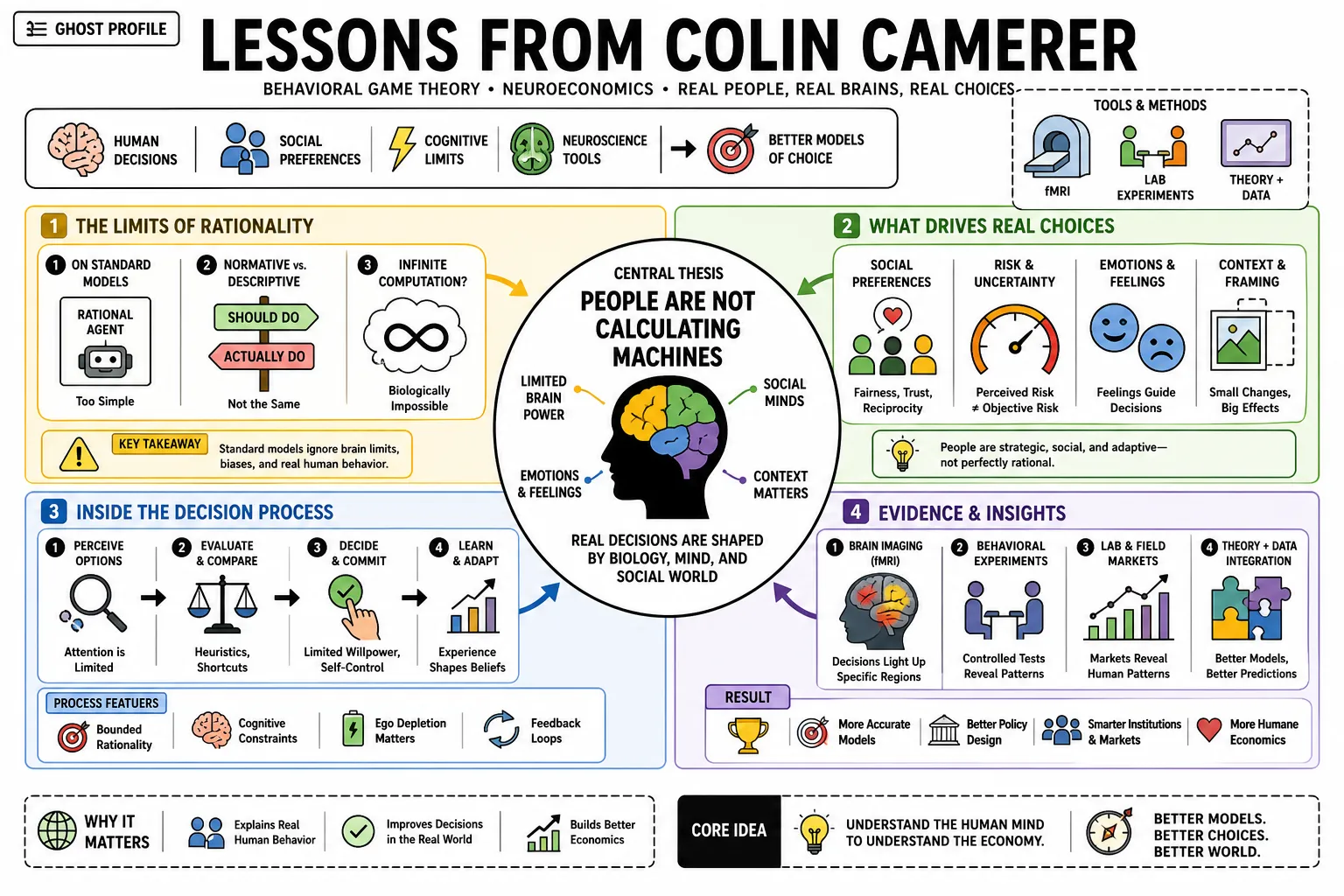

- On standard models: "Behavioral economics began with skepticism that rational choice theory would give you the best descriptive model of human behavior that one could hope for." — Source: Cambridge University Press

- On normative vs. descriptive theory: "The reason is that the normative theory won't be the best descriptive theory. What people should do is not always what they actually do." — Source: Advances in Behavioral Economics

- On infinite computation: Economic models historically assumed humans possess unlimited computational power and willpower, which fundamentally ignores the biological limits of the brain. — Source: NBER

- On theoretical fables: "There is too much theory that is detached from likely observation. I prefer the prediction that comes with mathematics to be an actual prediction you would take seriously and want to test." — Source: The Art and Practice of Economics Research

- On the usefulness of math: Mathematical models in economics are incredibly useful for describing behavior, but they become a problem when theorists mistake the mathematical convenience for psychological reality. — Source: Masters in Business Podcast

- On human complexity: Understanding real decision-making requires accounting for natural limits on computation, willpower, and self-interest. — Source: American Economic Association

- On the resistance of traditional economics: "Historically, economics as a profession is timid about measuring and collecting new kinds of data. This is an unfortunate contrast to scientific innovation in most other fields." — Source: Neuroeconomics: How Neuroscience Can Inform Economics

- On borrowing from psychology: Economics spent decades trying to build models of human behavior while deliberately ignoring the empirical findings of psychology, a gap behavioral economics had to bridge. — Source: Behavioral Game Theory

- On bounded rationality: People are not irrational; they are boundedly rational. They use heuristics and shortcuts that work well in most situations but fail predictably in complex or novel environments. — Source: Caltech Directory

- On adapting models: Behavioral economics is not about throwing away classical economics; it is about keeping the mathematical rigor while replacing the psychological assumptions with ones that are empirically true. — Source: The Decision Lab

Part 2: Neuroeconomics and the Brain

- On the core premise: "Don't ask the person, ask the brain!" — Source: Marginal Revolution University

- On the recipe for neuroeconomics: "Neuroeconomics is about 90 percent neuroscience and 10 percent economics. We've taken mathematical models from economics to help describe what we see happening in the brain." — Source: Caltech News

- On levels of analysis: While most economic theory focuses on the algorithmic level of how a decision is made, neuroeconomics attempts to understand the physical and chemical implementation of that choice in the brain. — Source: Wharton Neuroscience Initiative

- On the long-term goal: The ultimate objective is to create a theory of economic choice and exchange that is neurally detailed, mathematically accurate, and behaviorally relevant. — Source: Neuroeconomics: How Neuroscience Can Inform Economics

- On subconscious processing: A vast majority of human brain activity occurs below the level of conscious awareness, making self-reported explanations of behavior inherently flawed. — Source: Apple Podcasts

- On opening the black box: For decades, economists treated the human mind as an unobservable black box. Brain imaging technologies like fMRI finally allow researchers to look inside and measure the mechanics of choice directly. — Source: MacArthur Foundation

- On tracking attention: Eye-tracking data reveals exactly what information a person considers before making a choice, proving that people routinely ignore data that rational models assume they process. — Source: PNAS

- On risk mapping: The brain processes the potential for financial loss in the exact same neural circuitry that it uses to process physical pain or disgust. — Source: Choiceology Podcast

- On biological measurement: We no longer have to guess if a subject is anxious or excited during a financial decision; we can measure their galvanic skin response and pupil dilation in real time. — Source: Masters in Business Podcast

- On the transition from physics: Moving from mathematics to neuroeconomics was driven by a desire to study systems that are messy and human, rather than clean and abstract. — Source: CASBS Video Series

Part 3: Behavioral Game Theory

- On closing the gap: "Game theory, the formalized study of strategy, began in the 1940s by asking how emotionless geniuses should play games, but ignored until recently how average people with emotions and limited foresight actually play games. This book marks the first substantial and authoritative effort to close this gap." — Source: Behavioral Game Theory

- On refining tools: Behavioral game theory is not about "disproving" game theory but rather about making it a more powerful tool for the analysis of strategic situations. — Source: USC Press

- On experimental rigor: "The way in which an experiment is conducted is unbelievably important." — Source: CERGE-EI

- On real incentives: People behave differently when there is real money on the line compared to when they are just answering a questionnaire, which is why experimental economics insists on incentivized choices. — Source: American Economic Association

- On strategy in practice: Real-world strategic interaction is less about computing mathematical equilibria and more about guessing what the other person is going to do based on their perceived nature. — Source: Advances in Behavioral Economics

- On Nash equilibrium: The mutual consistency assumed in Nash equilibrium—that players correctly anticipate what others will do—is implausible the first time players face a novel game. — Source: The Quarterly Journal of Economics

- On missing variables: Standard game theory often fails to predict outcomes in bargaining games because it omits variables like spite, fairness, and reputation. — Source: Behavioral Game Theory

- On charting a middle course: Behavioral game theory seeks a middle path between over-rational equilibrium models and under-rational, purely adaptive biological models. — Source: The Decision Lab

- On laboratory evidence: When laboratory results repeatedly and systematically violate a theoretical prediction, the theory must be adjusted to fit the data, not the other way around. — Source: NBER

- On the predictability of error: Human deviations from optimal game theory strategies are not random noise; they are systematic, predictable biases that can be modeled mathematically. — Source: Caltech Research

Part 4: Hypothetical Bias and Cheap Talk

- On cheap talk: "'Hypothetical bias' (AKA cheap talk) is the difference between what people SAY they'll do and what they ACTUALLY do." — Source: Marginal Revolution University

- On the voting gap: When pollsters ask people if they plan to vote, about 70 percent say yes, but only 45 percent actually show up. This 25 percent gap is a prime example of hypothetical bias. — Source: Masters in Business Podcast

- On consumer research: Asking consumers in a survey if they will buy a new product is a notoriously unreliable way to predict actual sales figures because words cost nothing. — Source: PNAS

- On physical tells: By tracking visual fixations during a hypothetical choice experiment, researchers can better predict what a consumer will actually buy when real money is introduced. — Source: Journal of Consumer Research

- On the cost of truth: The human brain is designed to conserve energy. Answering a hypothetical question accurately requires cognitive effort that subjects rarely expend unless they are financially incentivized. — Source: Choiceology Podcast

- On survey methodology: Camerer treats self-reports as unreliable unless the design gives people a reason to reveal real preferences: in the Masters in Business transcript, he says experimental economists usually pay participants based on their choices, then uses polling and new-product purchase intent as examples where stated intentions can overpredict actual behavior. — Reference: Masters in Business transcript on incentives, hypothetical bias, polling, and purchase-intent overstatement

- On biological lie detectors: Physiological measurements in neuroeconomics serve as a way to bypass the conscious filters and social desirability biases that corrupt survey data. — Source: Wharton Neuroscience Initiative

- On predicting behavior: If you want to know what someone will do, look at the neural activation in their striatum rather than asking them to fill out a questionnaire. — Source: Caltech News

- On the illusion of intent: People genuinely believe they will go to the gym tomorrow or save more money next month, meaning hypothetical bias is often an issue of self-deception rather than intentional lying. — Source: CASBS Video Series

Part 5: Social Preferences and Fairness

- On social utility: Players in economic games are almost never motivated solely by their own material payoffs; they evaluate outcomes through a lens of social utility. — Source: Advances in Behavioral Economics

- On the ultimatum game: The consistent rejection of low offers in the ultimatum game proves that humans have a strong, innate preference for fairness, even when enforcing it costs them money. — Source: Behavioral Game Theory

- On vengeance: Standard models assume emotionless calculation, but real human interaction is heavily influenced by moral obligation and vengeance. — Source: American Economic Association

- On the cost of spite: People will readily sacrifice their own financial gain to punish someone who has violated a social norm or treated them unfairly. — Source: The Decision Lab

- On trust as an economic engine: Trust cannot be fully explained by rational risk calculations; there is a biological and social component to trusting strangers that facilitates trade and market function. — Source: NBER

- On intention reading: We care not just about the final financial outcome of a transaction, but about the perceived intentions of the person we are transacting with. — Source: The Quarterly Journal of Economics

- On inequality aversion: Experimental data shows that many people experience a measurable drop in utility when rewards are distributed highly unequally, even if they are on the winning side. — Source: Caltech Research

- On cross-cultural fairness: While the exact definition of a "fair" split varies across different cultures and societies, the willingness to punish unfairness is a universal human trait. — Source: MacArthur Foundation

- On modeling emotion: Social preferences like altruism and reciprocity can and should be quantified and integrated into formal utility functions to make economic models accurate. — Source: Neuroeconomics: How Neuroscience Can Inform Economics

Part 6: Cognitive Hierarchy and Strategic Depth

- On limited thinking steps: The cognitive hierarchy model acknowledges a theory of how limits in the brain constrain the number of steps of "I think he thinks..." reasoning people naturally do. — Source: Behavioral Game Theory

- On defining the CH model: "In this model, each player assumes that his strategy is the most sophisticated." — Source: The Quarterly Journal of Economics

- On step-zero players: The model categorizes "step-zero" players as those who essentially randomize their choices without thinking deeply about their opponent's strategy. — Source: The Quarterly Journal of Economics

- On the average depth of thought: Empirical tests suggest that the average person only thinks about 1.5 steps ahead in a novel strategic interaction. — Source: Caltech Economics Working Papers

- On overestimating others: A key insight of the cognitive hierarchy model is that a "step-k" thinker assumes the rest of the population is distributed across steps 0 through k-1, completely ignoring the possibility that someone is out-thinking them. — Source: The Quarterly Journal of Economics

- On predictive precision: "If the mean number of thinking steps is specified in advance (1.5 is a reasonable estimate), this theory has zero free parameters, is just as precise as Nash equilibrium, and always fits experimental data better." — Source: The Quarterly Journal of Economics

- On beauty contests: In games like the "Guess 2/3 of the Average" game, winning requires you to accurately predict the cognitive limits of the crowd, not just find the mathematical equilibrium. — Source: Behavioral Game Theory

- On working memory: The number of strategic steps a person can simulate in their head is heavily constrained by biological limits on working memory. — Source: Wharton Neuroscience Initiative

- On bounded sophistication: Camerer, Ho, and Chong model strategic sophistication as bounded: step-k thinkers best-respond to less sophisticated players, and an average of about 1.5 thinking steps fits data from many games better than assuming everyone reasons to equilibrium. — Reference: IDEAS/RePEc abstract for Camerer, Ho, and Chong on cognitive hierarchy and bounded steps of thinking

Part 7: Markets, Bubbles, and Financial Decisions

- On simulating markets: "It's like simulating earthquakes: we can over and over study a bubble, crash, bubble, crash. Then we can see mathematically if there's some regular pattern and what's going on in people's brains." — Source: Caltech News

- On bubble formation: Asset bubbles form precisely because traders fail to accurately estimate the cognitive hierarchy and beliefs of the other participants in the market. — Source: Masters in Business Podcast

- On risk and loss: People are generally risk-averse when dealing with gains but become highly risk-seeking when trying to avoid a guaranteed loss. — Source: Choiceology Podcast

- On market corrections: Traditional finance assumes arbitrageurs will quickly correct mispricing, but behavioral finance shows that arbitrage is risky and often constrained by the limits of human capital. — Source: Advances in Behavioral Economics

- On recognizing momentum: Brain imaging shows that during the formation of a financial bubble, traders experience increased activity in areas associated with theory of mind, as they try to guess when the crowd will turn. — Source: PNAS

- On overconfidence: Corporate executives and retail traders alike suffer from systematic overconfidence in their own predictions, leading to excessive trading and market volatility. — Source: NBER

- On ignoring base rates: Investors frequently overreact to new, salient information (like a news headline) while ignoring historical base rates that are far more predictive of future outcomes. — Source: The Decision Lab

- On the disposition effect: The human tendency to hold onto losing investments too long and sell winning investments too early is driven by the brain's strong biological aversion to realizing a loss. — Source: Masters in Business Podcast

- On evaluating risk: Real financial choices are driven more by emotional responses to uncertainty than by the cold calculation of expected value. — Source: Neuroeconomics: How Neuroscience Can Inform Economics

Part 8: Learning, Habits, and Experience

- On experience-weighted attraction: People learn which strategies work over time through a process called Experience-Weighted Attraction (EWA), adapting their behavior based on the specific feedback they receive from previous interactions. — Source: Behavioral Game Theory

- On habit formation: Much of daily economic behavior is governed not by active decision-making, but by neural autopilot, where the brain minimizes effort by repeating past actions. — Source: Behind Your Behavior Podcast

- On learning from failure: In economic games, individuals adjust their strategies much more dramatically after a painful loss than after a success. — Source: American Economic Association

- On shifting strategies: Over repeated rounds of a game, humans slowly migrate from intuitive, heuristic-based play toward behaviors that more closely resemble classical equilibrium predictions. — Source: Advances in Behavioral Economics

- On the speed of adaptation: How quickly a person learns a new optimal strategy depends entirely on the clarity and immediacy of the reward signal they receive from the environment. — Source: Caltech Research

- On unlearning bad habits: Breaking a financial habit requires overriding deeply entrenched neural pathways, which is why financial education programs often fail to change long-term behavior. — Source: CASBS Video Series

- On fictitious play: When deciding how to act in the future, people not only evaluate the rewards of what they did, but they simulate the hypothetical rewards they would have received if they had chosen differently. — Source: The Quarterly Journal of Economics

- On memory constraints: Learning in economic markets is imperfect because human memory is selective; we remember our brilliant trades vividly and conveniently forget our irrational mistakes. — Source: Choiceology Podcast

- On the evolution of trust: Trust is not a static trait; it is a learned behavior that is constantly updated in the brain based on the reliability of the counterparties we interact with over time. — Source: MacArthur Foundation