Lessons from Collette Chilton

Collette Chilton spent 17 years as the first Chief Investment Officer at Williams College, where she built the professional investment office and managed an endowment that fully funded all student financial aid. She approached the job with humility, focusing on diverse managers and tying investments directly to the school's mission. This profile breaks down her exact methods for allocating assets, mentoring staff, and building portfolios to last.

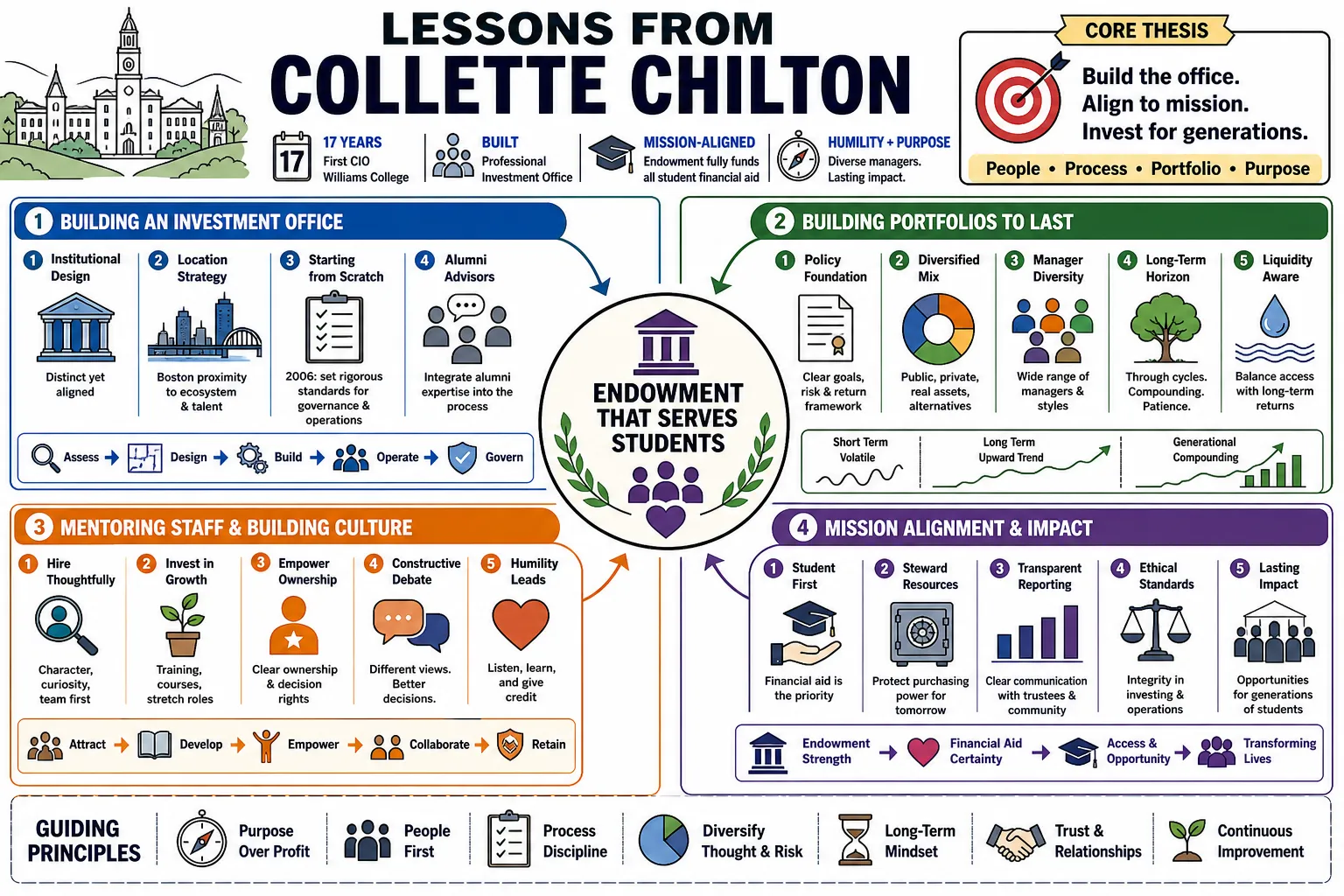

Part 1: Building an Investment Office

- On institutional design: "Establishing a professional investment office requires setting a physical and cultural foundation that is distinct from, yet fully aligned with, the parent institution." — Source: [Williams College Investment Report]

- On location strategy: "Basing the investment office in Boston rather than on the Williams campus in Williamstown provided necessary proximity to the financial ecosystem and prospective talent." — Source: [Institutional Investor]

- On starting from scratch: "Transitioning from a decentralized or externally advised model to a dedicated internal team in 2006 required setting rigorous new standards for governance and daily operations." — Source: [The Williams Record]

- On alumni advisors: "Integrating alumni expertise into the advisory committee provides a built-in layer of loyalty and institutional memory that external consultants cannot replicate." — Source: [Capital Allocators Podcast]

- On team structure: "A successful investment office relies on a flat organizational structure where analysts are encouraged to debate ideas openly with senior leadership." — Source: [The Williams Record]

- On institutional alignment: "The investment team must thoroughly understand the college's operating budget cycle to ensure liquidity matches seasonal funding needs." — Source: [Williams College Investment Report]

- On setting benchmarks: "Early on, the office established customized benchmarks that accurately reflected the college's specific risk tolerance rather than relying on generic market indices." — Source: [Capital Allocators Podcast]

- On transitioning models: "Moving an institution toward professionalized endowment management means deliberately shifting the board's role from selecting individual stocks to focusing on broad policy." — Source: [Institutional Investor]

- On succession planning: "A hallmark of a well-built office is the ability to seamlessly transition leadership to a deputy who helped build the underlying processes." — Source: [The Williams Record]

Part 2: Humility and Loyalty

- On quiet confidence: "I've seen things you people wouldn't believe; the key is carrying those experiences forward with a quiet confidence rather than ego." — Source: [UCLA Economics Newsletter]

- On avoiding the limelight: "The objective is to deliver exceptional returns for the institution, not to win the popularity contests that dominate the allocator community." — Source: [Institutional Investor]

- On institutional loyalty: "Loyalty in an investment office means recognizing that the portfolio exists to serve the students and faculty, not to serve as a personal trading track record." — Source: [Capital Allocators Podcast]

- On admitting mistakes: "Humility is recognizing when an investment thesis is broken and having the discipline to exit the position rather than defending a bad decision." — Source: [Capital Allocators Podcast]

- On peer comparisons: "Measuring success by how you stack up against other elite endowments is a distraction; success is meeting your own institution's long-term spending rate." — Source: [Institutional Investor]

- On retaining staff: "Creating a culture of loyalty requires giving team members meaningful responsibility early on and sharing the credit when investments succeed." — Source: [The Williams Record]

- On managing expectations: "Humility in communication means preparing the board for the inevitability of down years rather than promising uninterrupted growth." — Source: [Williams College Investment Report]

- On competitive environments: "Steering clear of the ultra-competitive allocator mentality allows a team to focus on quiet, consistent compounding." — Source: [Institutional Investor]

- On long-term stewardship: "We are temporary stewards of capital that is meant to last in perpetuity; that reality demands a deferential approach to risk." — Source: [Capital Allocators Podcast]

Part 3: Asset Allocation and Philosophy

- On market behavior: "The market can stay irrational longer than you can remain solvent." — Source: [Capital Allocators Podcast]

- On hedge fund allocations: "Hedge funds, when selected carefully, provide necessary downside protection that plain-vanilla equity portfolios lack during severe market corrections." — Source: [Institutional Investor]

- On venture capital pacing: "Maintaining a strict, consistent pacing model in venture capital is better than trying to time cycles of innovation." — Source: [Capital Allocators Podcast]

- On absolute returns: "Over a ten-year period, generating an annualized return of 10.3 percent requires a willingness to hold illiquid assets that others abandon during panics." — Source: [The Williams Record]

- On contrarianism: "Finding alpha often means deliberately looking away from the crowded, popular trades that everyone else is trying to access." — Source: [Capital Allocators Podcast]

- On private equity: "The premium for locking up capital in private markets must be substantial enough to justify the loss of flexibility." — Source: [Institutional Investor]

- On portfolio construction: "A resilient portfolio is built not by chasing the highest possible returns, but by optimizing for survival across multiple distinct economic environments." — Source: [Williams College Investment Report]

- On active vs. passive: "Active management earns its fees primarily in inefficient markets; in highly efficient sectors, passive exposure is often the more rational choice." — Source: [Capital Allocators Podcast]

- On return targets: "The mathematics of endowment management are unforgiving: you must clear inflation plus the annual payout rate just to maintain purchasing power." — Source: [Williams College Investment Report]

Part 4: Endowment Management and Mission

- On the greatest accomplishment: "We've provided billions of dollars to Williams to be able to do everything that goes on at the College." — Source: [The Williams Record]

- On funding financial aid: "By outperforming the market, the investment office generated enough money to more than pay for all of the financial aid provided to students during the time the office existed." — Source: [The Williams Record]

- On the burden of operations: "Knowing that the endowment funds a significant portion of the college's annual operating budget adds a layer of gravity to every allocation decision." — Source: [Williams College Investment Report]

- On communicating with students: "Demystifying the endowment for the student body is an important part of the job, which is why participating in Winter Study programs matters." — Source: [The Williams Record]

- On spending rules: "A disciplined spending policy protects the institution from eating into its principal during extended bear markets." — Source: [Williams College Investment Report]

- On the purpose of capital: "Endowment growth is not an abstract scoreboard; it translates directly into smaller class sizes, better facilities, and broader access." — Source: [The Williams Record]

- On institutional priorities: "Investment decisions must never operate in a vacuum; they have to remain tightly tethered to the strategic goals set by the college president and trustees." — Source: [Capital Allocators Podcast]

- On long-term horizons: "A university endowment is one of the few pools of capital that can genuinely afford to look past the next decade." — Source: [Institutional Investor]

- On stakeholder trust: "Maintaining the trust of alumni donors requires absolute transparency about how their gifts are being invested and protected." — Source: [Williams College Investment Report]

Part 5: Risk Management and the 2008 Crisis

- On crisis management: "The 2008 financial crisis tested every assumption we had about liquidity and correlations across different asset classes." — Source: [The Williams Record]

- On liquidity crunches: "You only find out how illiquid your portfolio truly is when everyone else in the market is trying to sell at exactly the same time." — Source: [Capital Allocators Podcast]

- On holding firm: "During extreme volatility, the hardest but most necessary action is often to do nothing and trust the asset allocation plan you built during peacetime." — Source: [Williams College Investment Report]

- On board communication in a downturn: "Frequent, unvarnished communication with the investment committee is essential when portfolio values are dropping rapidly." — Source: [Capital Allocators Podcast]

- On the cost of panic: "Selling risk assets at the bottom of a drawdown permanently impairs the endowment's ability to recover when the market inevitably turns." — Source: [Institutional Investor]

- On stress testing: "Historical stress tests are useful, but they never fully capture the psychological pressure of a real-world liquidity crisis." — Source: [Capital Allocators Podcast]

- On defensive positioning: "Downside protection is expensive when markets are roaring, but it pays for itself entirely during severe market dislocations." — Source: [Institutional Investor]

- On adapting to new realities: "Post-2008, the definition of a safe asset fundamentally changed, requiring us to rethink how we construct the fixed-income portion of the portfolio." — Source: [Williams College Investment Report]

- On institutional memory: "Documenting the decisions made during a crisis ensures that future teams don't repeat the same mistakes when the next panic hits." — Source: [The Williams Record]

Part 6: Diversity and Mentorship

- On closing the gender gap: "Increasing the number of women in portfolio management requires deliberate interventions at the undergraduate level, before career paths are fully set." — Source: [Girls Who Invest]

- On early career regrets: "One of my regrets is not focusing on student program diversity and inclusion efforts earlier in my career." — Source: [The Williams Record]

- On lack of mentors: "Navigating institutional finance early on was difficult precisely because there were so few female mentors in executive leadership roles." — Source: [The Williams Record]

- On building inclusive teams: "A homogenous investment team is a risk factor; diverse perspectives are required to spot blind spots in an investment thesis." — Source: [Capital Allocators Podcast]

- On board service: "Joining the board of Girls Who Invest is about creating a structural pipeline for women to enter and stay in the asset management industry." — Source: [Girls Who Invest]

- On active mentorship: "Mentorship cannot be passive. It requires putting junior team members in rooms with senior managers and letting them ask the hard questions." — Source: [The Williams Record]

- On educational initiatives: "Supporting programs like Winter Study allows students who never considered finance to see it as a viable, intellectually rigorous path." — Source: [The Williams Record]

- On evaluating talent: "When hiring, we look for intellectual curiosity and a capacity to learn, rather than just a specific pedigree in finance." — Source: [Capital Allocators Podcast]

- On industry change: "The asset management industry is slowly changing, but it requires continuous pressure from asset owners to demand diversity from their external managers." — Source: [Girls Who Invest]

- On retaining women in finance: "Getting women into entry-level roles is only half the battle; the industry must create environments where they can realistically ascend to the CIO seat." — Source: [Girls Who Invest]

Part 7: Manager Selection and Relationships

- On judging character: "The manager selection process is ultimately an exercise in evaluating human character and integrity under pressure." — Source: [Capital Allocators Podcast]

- On popular managers: "Navigating around the most famous, oversubscribed managers is often necessary to find emerging talent that still has the hunger to generate alpha." — Source: [Institutional Investor]

- On alignment of interests: "We refuse to invest with any firm where the general partners do not have a significant portion of their own net worth invested alongside ours." — Source: [Williams College Investment Report]

- On patience with underperformance: "If the underlying thesis hasn't changed, you must have the patience to stick with a high-conviction manager through a period of short-term underperformance." — Source: [Capital Allocators Podcast]

- On due diligence: "Thorough due diligence means checking references that the manager did not provide and visiting them when they are not expecting a pitch." — Source: [The Williams Record]

- On sizing positions: "A great idea doesn't matter if it isn't sized appropriately in the portfolio to actually impact the bottom line." — Source: [Institutional Investor]

- On manager transparency: "The moment a manager becomes evasive about a bad month or a broken trade, the trust is broken and the relationship is effectively over." — Source: [Capital Allocators Podcast]

- On capacity constraints: "The best returns often come from managers who are willing to hard-close their funds to protect performance rather than simply gathering assets for fees." — Source: [Institutional Investor]

- On long-term partnerships: "We look for managers who view us as partners in their business, not just as another source of sticky capital." — Source: [Williams College Investment Report]

- On separating luck from skill: "The hardest part of manager evaluation is determining whether a multi-year track record was the result of repeatable skill or simply catching a macro tailwind." — Source: [Capital Allocators Podcast]

Part 8: Career Lessons and Leadership

- On public vs. private pensions: "Managing a public pension like MassPRIM involves navigating intense political constraints that simply do not exist in the corporate or endowment worlds." — Source: [Capital Allocators Podcast]

- On corporate environments: "At Lucent, I learned how to manage assets in an environment where the health of the pension was directly tied to the operating health of a single, volatile corporation." — Source: [Capital Allocators Podcast]

- On the endowment advantage: "The freedom of a college endowment is the absence of daily liquidity constraints, allowing you to harvest the illiquidity premium properly." — Source: [Institutional Investor]

- On board dynamics: "A CIO's effectiveness is completely dependent on having an investment committee chair who acts as a mentor and runs interference with the broader board." — Source: [Institutional Investor]

- On career longevity: "Surviving decades in this industry requires developing a thick skin and learning not to take market fluctuations personally." — Source: [Capital Allocators Podcast]

- On lifetime achievement: "Receiving a lifetime achievement award is less about individual brilliance and more a recognition of building processes that outlast any single market cycle." — Source: [Institutional Investor]

- On leaving a legacy: "The true test of a CIO's legacy is how well the portfolio and the team perform in the five years after they retire." — Source: [The Williams Record]

- On continuous learning: "The markets evolve constantly; the moment you rely entirely on what worked ten years ago is the moment your returns begin to decay." — Source: [Capital Allocators Podcast]

- On making decisions: "In investments, you never have 100 percent of the information you want; leadership is making a firm decision with 70 percent of the data." — Source: [The Williams Record]

- On the role of a CIO: "The CIO is ultimately a translator, turning the complex mechanics of global finance into reliable funding for a college's core mission." — Source: [Williams College Investment Report]