Lessons from Corey Hoffstein

Corey Hoffstein is the co-founder and CIO of Newfound Research, where he turns quantitative research into investable portfolios. He built his reputation on the "Return Stacking" framework and his work detailing the market risks of "Liquidity Cascades." This profile breaks down his approach to capital efficiency, quantitative modeling, and designing portfolios investors can actually stick with during drawdowns.

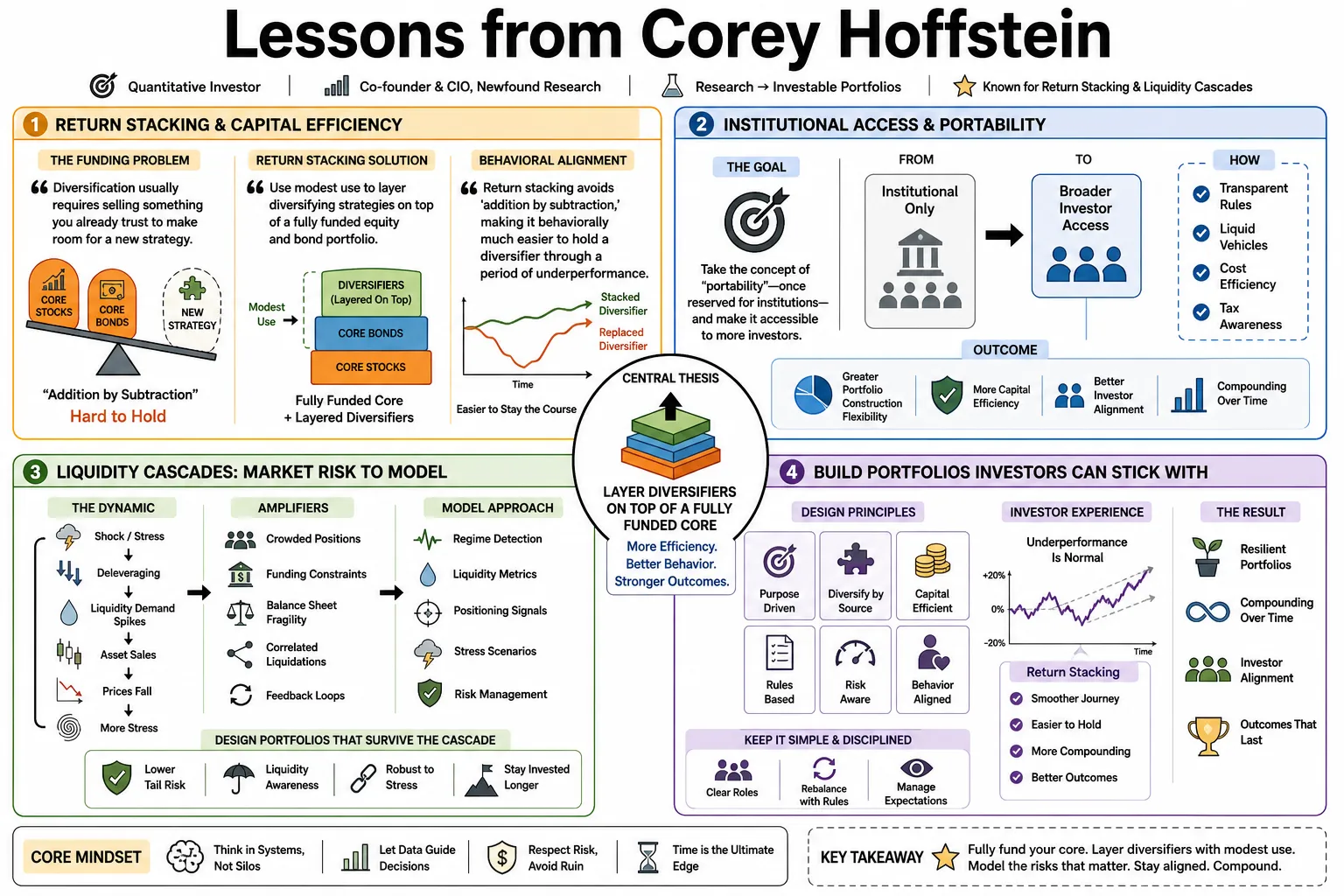

Part 1: Return Stacking & Capital Efficiency

- On the funding problem: "The fundamental issue with diversification is that it usually requires selling something you already trust, like core stocks or bonds, to make room for a new strategy." — Source: Masters in Business

- On return stacking: "Instead of replacing your core holdings, you can use modest use to layer diversifying strategies on top of a fully funded equity and bond portfolio." — Source: Return Stacked® ETFs

- On behavioral alignment: "Return stacking avoids 'addition by subtraction,' making it behaviorally much easier for an investor to hold a diversifier through a period of underperformance." — Source: The Meb Faber Show

- On institutional access: "The goal was to take the concept of 'portable alpha'—which large institutions have used for decades—and wrap it in an accessible, retail-friendly ETF." — Source: ReSolve Asset Management

- On capital efficiency: "Capital efficiency isn't about maximizing risk; it's about maximizing the utility of every dollar in your portfolio so it can work in multiple ways simultaneously." — Source: Flirting with Models

- On use: "use is just a tool. When applied to a concentrated position, it increases risk. When applied to expand diversification into uncorrelated assets, it can actually improve risk-adjusted returns." — Source: Think Newfound

- On the 60/40 portfolio: "The 60/40 portfolio isn't dead, but it can be highly capital inefficient. Stacking allows you to keep the 60/40 while solving for the macro environments where it traditionally fails." — Source: Masters in Business

- On cash collateral: "If you are holding a bond portfolio, that same capital can often be posted as collateral to support a managed futures overlay, essentially earning two distinct return streams on one asset." — Source: RCM Alternatives

- On expected returns: "In a world where expected returns for traditional assets may be lower than historical averages, stacking diversifiers is one of the few mathematical ways to maintain target return levels without taking outsized equity risk." — Source: Return Stacked

- On tracking error: "By maintaining your core beta exposure, you minimize the tracking error to the benchmark that typically gets investors fired or causes them to abandon a strategy at the wrong time." — Source: AdvisorAnalyst

Part 2: Liquidity Cascades & Market Structure

- On coordinated risk: "Modern financial markets are increasingly driven by the coordinated risk of uncoordinated market participants acting on similar incentives." — Source: Delphi Digital

- On pro-cyclical forces: "The growth of passive investing, target-date funds, and volatility-targeting strategies creates pro-cyclical forces that reinforce sharp market moves." — Source: Think Newfound

- On melt-ups and crashes: "Liquidity cascades don't just cause market crashes; the exact same mechanics drive rapid, aggressive melt-ups when technical buying pressure feeds upon itself." — Source: Simplify ETFs

- On market microstructure: "Microstructure matters. The shift toward passive indexing fundamentally changes the liquidity profile of the underlying stocks, making them more susceptible to structural flow shocks." — Source: Investment Magazine

- On reflexivity: "Markets have always been somewhat reflexive, but the automation of risk management has hardcoded that reflexivity into the system." — Source: Flirting with Models

- On unseen convergence: "The danger lies in unforeseen destructive convergences—when multiple independent strategies all receive the signal to deleverage at the exact same moment." — Source: AdvisorAnalyst

- On central bank influence: "A decade of central bank intervention didn't just suppress volatility; it incentivized the creation of yield-seeking strategies that implicitly rely on that suppressed volatility continuing." — Source: WisdomTree

- On volatility as an asset class: "Because of these structural changes, volatility itself has transformed from a statistical measurement into an actively traded asset class that wags the dog of the equity market." — Source: ReSolve Asset Management

- On passive investing's impact: "Passive investing is essentially a momentum strategy that buys more of a stock simply because its market cap increased, entirely agnostic to valuation." — Source: Think Newfound

- On surviving cascades: "To survive liquidity cascades, you need strategies in your portfolio that are either completely immune to these specific technical flows or designed to explicitly exploit them." — Source: Delphi Digital

Part 3: Diversification & Portfolio Construction

- On false diversification: "Holding five different equity mutual funds isn't diversification; it's just an expensive way to own the S&P 500. True diversification requires fundamentally different economic drivers." — Source: The Meb Faber Show

- On managed futures: "Managed futures are one of the few strategies that have historically demonstrated the ability to provide crisis alpha exactly when equities and bonds are correlating downward." — Source: RCM Alternatives

- On long/short framing: "You can measure the distance between any two portfolios as a long/short strategy. Framing the problem this way clarifies exactly what active bets you are implicitly making." — Source: Think Newfound

- On the pain of being different: "The optimal portfolio on paper is useless if it looks so weird compared to your peers that you abandon it during the inevitable three-year drawdown." — Source: WisdomTree

- On ensemble methods: "Rather than trying to find the single best parameter for a strategy, we prefer ensemble methods that blend multiple parameters to create a more strong, generalized signal." — Source: Flirting with Models

- On asset allocation: "Asset allocation is ultimately an exercise in humility. You are admitting that you don't know what the future holds, so you must prepare for multiple distinct macroeconomic regimes." — Source: Top Traders Unplugged

- On correlation breakdowns: "Correlations are not static. The assumption that bonds will always hedge stocks is a recency bias born from a specific multi-decade disinflationary environment." — Source: Return Stacked

- On structural alpha: "The most durable alpha often comes from structural risk premia—providing liquidity or taking on risks that other market participants are institutionally constrained from holding." — Source: Masters in Business

- On the permanence of loss: "Volatility is a temporary phenomenon; the permanent loss of capital is what portfolio construction is ultimately trying to prevent." — Source: Think Newfound

- On alternative assets: "Adding alternatives isn't about boosting returns; it's about reshaping the geometry of your portfolio's compounding path over time." — Source: AdvisorAnalyst

Part 4: Factor Investing & Momentum

- On factor commoditization: "As traditional factors like value and momentum become increasingly commoditized, the edge shifts from the model itself to the speed and quality of the underlying data." — Source: Bloomberg News

- On momentum's durability: "Momentum is a persistent behavioral anomaly because it is driven by the slow dissemination of information and the anchoring bias of human investors." — Source: Flirting with Models

- On value investing: "Traditional price-to-book value investing struggled for a decade not because value is dead, but because the accounting metrics failed to capture the rise of intangible assets." — Source: Moon Tower Meta

- On factor timing: "Factor timing is notoriously difficult. Instead of trying to time when value or momentum will work, it is usually better to maintain persistent, diversified exposure to both." — Source: Think Newfound

- On trend following: "Trend following is simply a systematic way to cut losses short and let winners ride, effectively transforming the return distribution of a portfolio to have positive skew." — Source: Top Traders Unplugged

- On intangible value: "When you adjust value models to include R&D and brand equity as capitalized assets, much of the recent underperformance of traditional value strategies disappears." — Source: Flirting with Models

- On multi-factor models: "A multi-factor portfolio requires careful construction to ensure the factors don't just cancel each other out, leaving you with an expensive index fund." — Source: WisdomTree

- On momentum crashes: "The biggest risk to a momentum strategy isn't a slow grind down, but a sharp, sudden market inflection point where the strategy is caught offsides and forced to rapidly deleverage." — Source: ReSolve Asset Management

- On strategy decay: "All quantitative strategies experience decay over time as they are discovered. The only way to survive is through continuous research and incremental refinement." — Source: Quant Galore

Part 5: Risk Management & Tail Risk

- On defining risk: "Risk is not standard deviation. Risk is the probability that you fail to meet your financial liabilities at the exact moment they come due." — Source: Flirting with Models

- On tail risk hedging: "Buying out-of-the-money puts is like buying fire insurance. It's an explicit cost that drags on your portfolio for years, but it guarantees liquidity during a fire." — Source: Think Newfound

- On crisis alpha: "You can't buy crisis alpha on the cheap during a crisis. You have to be willing to bleed a little bit during the good times to have the capital when the bad times hit." — Source: The Meb Faber Show

- On sequence of returns: "Sequence of return risk is the silent killer of retirement plans. Experiencing a severe drawdown right as you begin distributing capital mathematically destroys the portfolio's longevity." — Source: AdvisorAnalyst

- On absolute return: "Absolute return strategies aim to provide positive performance regardless of the macro environment, but they often require tolerating significant tracking error to equity markets." — Source: Masters in Business

- On managing drawdowns: "It is mathematically much harder to recover from a 50% drawdown than a 20% drawdown. Limiting the depth of the valley is essential for long-term compounding." — Source: Top Traders Unplugged

- On implied volatility: "When you use options to hedge, you are implicitly taking a view on the cost of volatility. Sometimes the market prices that insurance so high that it guarantees a negative expected outcome." — Source: ReSolve Asset Management

- On rebalancing: "Rebalancing is fundamentally a contrarian action. It forces you to sell the asset that has been making you rich and buy the asset that has been causing you pain." — Source: Think Newfound

- On hidden use: "Many investors carry hidden use in their portfolios through implicit short volatility positions in high-yield credit or structured products." — Source: Simplify ETFs

Part 6: Quantitative Research & Data Quality

- On data cleaning: "Ninety percent of quantitative research is just cleaning data. If your data parsing, linking, and standardization are flawed, your sophisticated model is worthless." — Source: Flirting with Models

- On overfitting: "Given enough parameters, you can fit a model to predict anything in the past. The true test of a quant is resisting the urge to over-optimize away historical noise." — Source: Think Newfound

- On simplicity: "Complex models often break in complex ways. In financial markets, a strong, simple heuristic usually outperforms a fragile, highly optimized algorithm out-of-sample." — Source: EQ Derivatives

- On parameter stability: "We look for strategies that exhibit parameter stability—if changing the lookback period from 200 days to 195 days destroys the return, it's not a real signal." — Source: Flirting with Models

- On trading costs: "A strategy with incredible gross returns on paper can easily become a negative-yielding strategy in reality once you factor in slippage, spread, and market impact." — Source: Quant Galore

- On alternative data: "Alternative data is only valuable if you have the domain expertise to map it correctly to financial outcomes. A satellite image of a parking lot is meaningless without context." — Source: Flirting with Models

- On academic anomalies: "Many anomalies published in academic finance journals only exist in micro-cap stocks and completely disappear the moment you apply realistic liquidity constraints." — Source: Think Newfound

- On systematic vs discretionary: "Systematic investing isn't about removing human judgment; it's about shifting the human judgment from the moment of execution to the moment of research and design." — Source: Top Traders Unplugged

- On regime shifts: "Models trained entirely on data from the post-2008 era are implicitly betting that the structural disinflation and monetary easing of that period will last forever." — Source: ReSolve Asset Management

Part 7: Behavioral Finance & Investor Psychology

- On sticking with the plan: "The optimal portfolio is not the one with the highest Sharpe ratio; it is the one you can stick with when it inevitably underperforms your neighbor's portfolio." — Source: Masters in Business

- On line-item risk: "Investors suffer from line-item veto. They will hyper-focus on the one diversifier in their portfolio that is down 10%, ignoring that it functioned exactly as intended while the rest of the portfolio was up." — Source: The Meb Faber Show

- On tracking error regret: "Tracking error is the emotional tax you pay for being different from the benchmark. If you can't afford the tax, you shouldn't hold the active strategy." — Source: Think Newfound

- On recent performance: "Investors are hardwired to buy what they wish they had owned three years ago and sell what they will wish they own three years from now." — Source: AdvisorAnalyst

- On the illusion of control: "Discretionary overrides of systematic models usually destroy value. The human mind steps in to 'fix' the model at the exact moment of maximum psychological pain, which is usually the worst time to intervene." — Source: Flirting with Models

- On communicating complexity: "You can build the most mathematically elegant strategy in the world, but if you can't explain it to an advisor in three minutes, they will never allocate client capital to it." — Source: Other People's Money (OPM)

- On framing: "How you frame a strategy matters just as much as its mechanics. Calling a strategy 'insurance' changes an investor's expectation from 'profit center' to 'cost center'." — Source: Flirting with Models

- On boredom: "Good investing is inherently boring. If your portfolio is providing you with entertainment or adrenaline, you are likely doing it wrong." — Source: Top Traders Unplugged

- On market timing: "The penalty for getting market timing wrong is so severe that it almost always outweighs the theoretical benefit of getting it right." — Source: Think Newfound

Part 8: The Business of Asset Management & Content

- On building a brand: "In a crowded asset management space, your content—whether it's a white paper, a podcast, or a blog—is your most effective distribution channel." — Source: Other People's Money (OPM)

- On podcasting: "Hosting a podcast like Flirting with Models is more than about marketing; it's a forced mechanism for continuous learning and networking with the smartest people in the industry." — Source: Flirting with Models

- On education as sales: "You don't sell a complex quantitative product by pitching returns; you sell it by educating the advisor on exactly how and why it fits into their clients' broader puzzle." — Source: Think Newfound

- On the ETF wrapper: "The democratization of finance is more than about lower fees; it's about taking institutional-grade strategies like return stacking and putting them into a tax-efficient, easily accessible ETF wrapper." — Source: Return Stacked® ETFs

- On transparency: "The days of the 'black box' quant are ending. Advisors demand transparency; they need to know more than what the model bought, but the exact intuition behind the trade." — Source: Masters in Business

- On collaboration: "The asset management industry is shifting from walled gardens to open ecosystems. Partnering with other firms allows us to combine distinct edges and bring better solutions to market." — Source: ReSolve Asset Management

- On firm culture: "A successful quantitative research firm must cultivate a culture of radical skepticism, where challenging the underlying assumptions of a model is rewarded, not penalized." — Source: Flirting with Models

- On survival: "The most important rule in the business of asset management is simply staying in the game long enough for your particular investment style to come back into favor." — Source: Top Traders Unplugged

- On defining success: "Beating the market is no longer enough. Success for a modern asset manager means solving a specific structural or behavioral problem for the end investor." — Source: Other People's Money (OPM)