Lessons from Dan Loeb

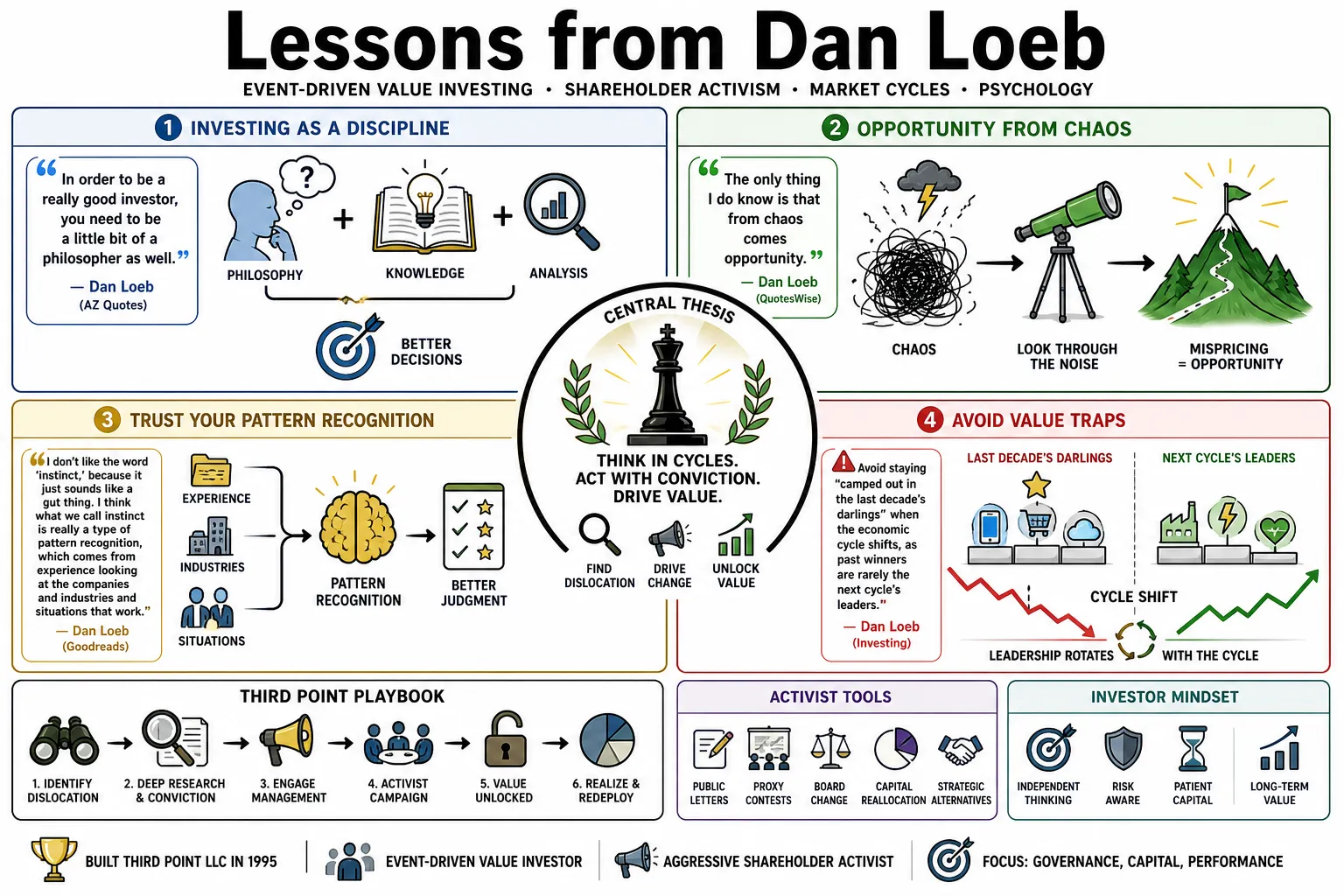

Daniel S. Loeb launched Third Point LLC in 1995, building a multi-billion dollar hedge fund on event-driven value investing and aggressive shareholder activism. He made his name writing scathing letters to corporate boards demanding management changes or capital reallocation. This profile gathers his public commentary on market cycles, corporate governance, and the psychology of institutional investing.

Part 1: The Philosophy of Value Investing

- On investing as a discipline: "In order to be a really good investor, you need to be a little bit of a philosopher as well." — Source: AZ Quotes

- On the nature of opportunity: "The only thing I do know is that from chaos comes opportunity." — Source: QuotesWise

- On trusting your intuition: "I don't like the word 'instinct,' because it just sounds like a gut thing. I think what we call instinct is really a type of pattern recognition, which comes from experience looking at the companies and industries and situations that work." — Source: Goodreads

- On value traps: Avoid staying "camped out in the last decade's darlings" when the economic cycle shifts, as past winners are rarely the next cycle's leaders. — Source: Investing.com

- On strategy definition: "We've never defined ourselves as one kind of firm, and we've never really deviated from that kind of flexible approach." — Source: Third Point Limited

- On humility in markets: "The only thing we are 100% confident in is that we are fallible, we don't have all the answers, and we will make some mistakes." — Source: Medium

- On market timing: "Timing is everything in these markets." — Source: AZ Quotes

- On event-driven catalysts: True value is unlocked not just by buying cheap assets, but by identifying specific events—spinoffs, bankruptcies, or restructurings—that force the market to reprice them. — Source: TrendSpider

- On fundamental research: Conviction in any position, regardless of the asset class, must be backed by rigorous, bottom-up fundamental analysis rather than thematic speculation. — Source: Third Point Limited

- On technological evolution: Modern value investors must evolve into "technology investors" if they want to succeed in a market dominated by artificial intelligence and new infrastructure. — Source: Colossus

Part 2: Activism and Corporate Governance

- On the necessity of pressure: "Corporations without bankruptcy [are] like Catholicism without hell. I'd say the same thing about activism. Activism without the potential of a proxy contest doesn't work, so we keep that in our back pocket, our little trade secret." — Source: Hearts and Minds Investments

- On management quality: "Companies get the shareholders they deserve," a principle he applies when demanding that entrenched boards make room for growth-minded, long-term investors. — Source: Business Insider

- On financial commitments: "Brendan, it's time for you to put your money where your mouth is. If you are sincere in your statement that a premium bid for the company is not worthy of discussion, then we must insist that you demonstrate your conviction by acquiring shares." — Source: Hedge Fund Alpha

- On stepping down: "It is time for you to step down from your role as CEO and director so that you can do what you do best: retreat to your waterfront mansion in the Hamptons, where you can play tennis and hobnob with your fellow socialites." — Source: Hedge Fund Alpha

- On false confidence: "Do not confuse our $22 million stake as a vote of confidence in the Company's senior management or its Board of Directors. On the contrary, it is our view that your record in management, acquisitions and corporate governance is among the worst that we have witnessed in our investment career." — Source: Business Insider

- On "Chief Value Destroyers": He frequently labels underperforming, entrenched executives as "CVDs" (Chief Value Destroyers) who prioritize their own compensation over shareholder returns. — Source: Hearts and Minds Investments

- On the "Lucky Sperm Club": He criticizes nepotism and unearned corporate positions by referring to such executives as members of the "LSC" or "Lucky Sperm Club." — Source: Hearts and Minds Investments

- On board complicity: Activist letters are often designed to expose the fact that private communications with board members reveal they secretly agree with criticisms they publicly call "baseless." — Source: 10x EBITDA

- On private activism: Over time, he has transitioned toward engaging boards "behind the scenes," finding that a private, constructive approach is often more effective with modern boards of large-cap companies. — Source: Substack

- On signing off: He became notorious in financial circles for concluding his most blistering, critical shareholder letters with the deceptively formal sign-off: "Very truly yours, Daniel S. Loeb." — Source: Business Insider

Part 3: Managing Risk and Downside

- On process versus luck: "A manager that has become overconfident by using a bad process is like somebody who plays Russian roulette three times in a row without the gun going off, and thinks they're great at Russian roulette. The fourth time, they blow their brains out." — Source: Medium

- On position concentration: Early losses on single, overconcentrated positions taught him that rigid discipline in sizing and risk mitigation is the only way to survive market shocks. — Source: Verified Investing

- On probability weighting: When sizing positions, Third Point relies heavily on probability-weighted estimates of both upside potential and maximum downside risk. — Source: NJ.gov

- On institutional risk controls: Managing a multi-asset portfolio requires a dedicated, independent risk committee that meets weekly to stress-test exposures. — Source: NJ.gov

- On the FTX collapse: Failures like the FTX collapse serve as a brutal reminder that rigorous, skeptical due diligence must never be bypassed, especially in complex or novel markets. — Source: Dan Loeb interview

- On diversification: Expanding into private credit, venture capital, and structured credit is a necessary evolution to provide consistent income and hedge against public equity volatility. — Source: Grokipedia

- On downside limits: Maintaining strict internal guidelines to limit downside risk at the individual position level prevents a single thesis failure from damaging the broader fund. — Source: NJ.gov

- On adapting risk profiles: A successful fund must be willing to shift its risk profile entirely, moving away from pure event-driven equities into reinsurance and credit when the risk-reward ratio dictates it. — Source: Institutional Investor

- On quantitative oversight: Integrating a proprietary risk management system, like Third Point's "RiskPoint," is essential to continuously monitor real-time exposures across diverse asset classes. — Source: NJ.gov

Part 4: Market Psychology and Cycles

- On emotional discipline: In highly complex and polarized macroeconomic environments, maintaining an "unemotional response, independent of one's political views," is critical for sound investing. — Source: Institutional Investor

- On market retail participation: "Fundamental analysis is increasingly taking a back seat to monitoring daily option expiries and Reddit message boards." — Source: Reddit

- On continuous learning: The market constantly changes its rules, requiring investors to cultivate a mindset geared strictly toward continuous, lifelong improvement. — Source: Dan Loeb interview

- On the "revenge of the nerds": When speculative excess recedes, the market inevitably returns to rewarding disciplined, fundamental value investors—the "value nerds." — Source: Investing.com

- On free market capitalism: "Perhaps our leaders will awaken to the fact that free market capitalism is the best system to allocate resources and create innovation, growth and jobs." — Source: Hedge Fund Alpha

- On short selling: Short selling remains a vital but increasingly difficult art form, requiring intense discipline as markets become more heavily influenced by passive flows and retail momentum. — Source: Dan Loeb podcast search

- On narrative battles: Modern market cycles are often defined by a "battle of two narratives: Rates and inflation on one hand versus GDP growth, margins and ultimately earnings on the other." — Source: Investing.com

- On second-order thinking: Success in markets rarely comes from reacting to the obvious news; it comes from applying "second-order thinking" to understand the cascading effects of policy decisions. — Source: Institutional Investor

- On optimism: Even amid tightening financial conditions and fiscal uncertainty, investors must avoid becoming "overly negative," as perfectly timing recessions is virtually impossible. — Source: Macro Ops

Part 5: Assessing Management and Leadership

- On corporate complacency: Boards that remain "tenured and complacent" while operational performance lags are the primary targets for necessary shareholder intervention. — Source: Forbes

- On resource allocation: He intensely scrutinizes corporate expense reports, famously weaponizing details like "hundreds of thousands" spent on "luxury lunches" to demonstrate a management team's disconnect from shareholders. — Source: Forbes

- On hiring criteria: When evaluating a board's decisions, he looks for specific industry expertise, frequently criticizing the hiring of executives with "abysmal performance" records and no relevant sector experience. — Source: Business Insider

- On the "brain drain": A company's inability to retain top engineering and technical talent is a massive red flag that points directly to leadership failures and future manufacturing deficiencies. — Source: CRN

- On strategic bungling: Boards that repeatedly fail to monetize non-core assets or liberate the value of minority stakes are guilty of "strategic bungling" and must be replaced. — Source: Business Insider

- On accountability for bad acquisitions: Management teams must be held accountable not just for their current operations, but for refusing to divest from their "failed acquisitions." — Source: CRN

- On deceptive resumes: He will aggressively investigate executive backgrounds, as seen when his pressure exposed a CEO who had misstated his academic record, leading to immediate resignation. — Source: Business Insider

- On ignoring core businesses: "We find it perplexing that Mr. Hirai does not worry about a division that has just released 2013's version of Waterworld and Ishtar back-to-back." — Source: Forbes

- On building partnership: While known for hostility, he is willing to initially tone down his rhetoric to build a "spirit of partnership" if he believes management is acting in good faith. — Source: 10x EBITDA

Part 6: Navigating Macroeconomics and Data

- On the new market drivers: Global markets are now dictated "almost exclusively by the twin forces of energy and the rapid evolution of artificial intelligence," overshadowing standard government reports. — Source: Dan Loeb interview

- On traditional indicators: Traditional macroeconomic indicators like standard unemployment or inflation prints have largely lost their predictive edge in the modern, technology-driven economy. — Source: Dan Loeb interview

- On the "old playbook": The "old investing playbook no longer works," requiring investors to study how technological regimes are actively reshaping economic activity. — Source: Benzinga

- On bottoms-up focus: Rather than relying on sweeping macro predictions, a fund should remain "bottoms-up," focusing strictly on specific company performance and individual cash flows. — Source: Investing.com

- On macro uncertainty: When macro factors are contradictory, the best defense is a portfolio built on idiosyncratic, company-specific catalysts that can generate returns independent of GDP growth. — Source: Third Point Limited

- On credit dislocations: Periods of macroeconomic stress and rising rates create the most lucrative opportunities in corporate and structured credit markets. — Source: Third Point Limited

- On geopolitical shifts: Changes in global supply chains and nearshoring trends are not just political talking points; they are tangible macroeconomic forces requiring immediate portfolio reallocation. — Source: Third Point Limited

- On technological infrastructure: The massive capital expenditures required to build AI data centers represent a macro-level shift in resource allocation comparable to the industrial revolution. — Source: Colossus

- On inflation protection: In highly inflationary environments, pricing power is the single most important metric for evaluating the durability of a long equity position. — Source: Third Point Limited

Part 7: Specific Campaigns and Deals

- On Sotheby's board: He demanded a "Shareholder Slate" of directors at Sotheby's, arguing the existing board was completely "dysfunctional" and detached from modern market realities. — Source: 10x EBITDA

- On Yahoo's Asian assets: During the Yahoo campaign, he relentlessly pushed the board to "liberate the value" of its highly lucrative Asian assets, specifically its stake in Alibaba. — Source: Newsweek

- On Sony's structure: He campaigned heavily for Sony to spin off its entertainment division, arguing that its lack of profitability was dragging down the valuation of its core electronics business. — Source: Standard

- On Intel's manufacturing: He targeted Intel by arguing they had ceded their manufacturing leadership to rivals like TSMC and Samsung, demanding they explore immediate strategic alternatives. — Source: CRN

- On Intel's turnaround: Following his pressure campaign, he publicly supported the return of Pat Gelsinger as CEO, acknowledging it as the necessary first step to fix Intel's broken culture. — Source: GuruFocus

- On Sotheby's CEO: He explicitly pushed for the resignation of CEO William Ruprecht, citing his "lackluster operating performance" despite operating in a booming art market. — Source: Forbes

- On Yahoo's CEO hire: He publicly ridiculed the hiring of Carol Bartz at Yahoo, viewing her appointment as proof that the board fundamentally misunderstood the internet space. — Source: GuruFocus

- On Elon Musk's debt: He has actively participated in purchasing bonds issued by Elon Musk's companies, viewing the debt structures of entities like X and xAI as uniquely mispriced opportunities. — Source: FutuNN

- On Japanese equities: Recognizing shifts in corporate governance culture, he has increasingly allocated capital to Japanese equities, viewing their balance sheet reforms as a massive structural catalyst. — Source: FutuNN

Part 8: Life, Mindset, and Surfing

- On the nature of surfing: The ocean is unpredictable, requiring a surfer to "sense when it’s happening and then have the drive to act at the right time"—a mindset he applies directly to trading. — Source: Mercenary Trader

- On naming his fund: He famously named his multi-billion dollar hedge fund, Third Point, after a specific, highly unpredictable surf break at Malibu Beach. — Source: Financial Times

- On travel and priorities: He considers his surf trips to remote locations like the Maldives and Indonesia to be "the highlights of my life," second only to time spent with his family. — Source: Wave Ki

- On physical training: He actively promotes the discipline of out-of-water surf training programs, viewing physical and mental preparation as critical to high performance in high-stress environments. — Source: Wave Ki

- On the necessity of detachment: Stepping away from the screens to be in the ocean provides the mental clarity required to survive the daily volatility of the financial markets. — Source: Financial Times

- On taking aggressive drops: Whether dropping into a steep wave or taking a massive activist position in a hostile boardroom, success requires fully committing once the decision is made. — Source: Mercenary Trader

- On respecting the environment: A surfer must respect the power of the ocean, just as an investor must respect the underlying mechanics of a macro market cycle, as fighting either will end in disaster. — Source: Mercenary Trader

- On the balance of chaos: Surfing Third Point at Malibu requires navigating a crowded, chaotic lineup to find the perfect wave, mirroring his approach to finding alpha in crowded financial markets. — Source: Financial Times

- On aging in the industry: Longevity in both surfing and investing requires pivoting strategies over time; relying solely on the aggressive energy of youth eventually gives way to the necessity of refined technique. — Source: Wave Ki

- On ultimate fulfillment: Beyond the proxy fights and billions managed, true fulfillment is found in the simplicity of the natural world and the disciplined pursuit of a personal craft. — Source: Wave Ki