Lessons from Dan Sundheim

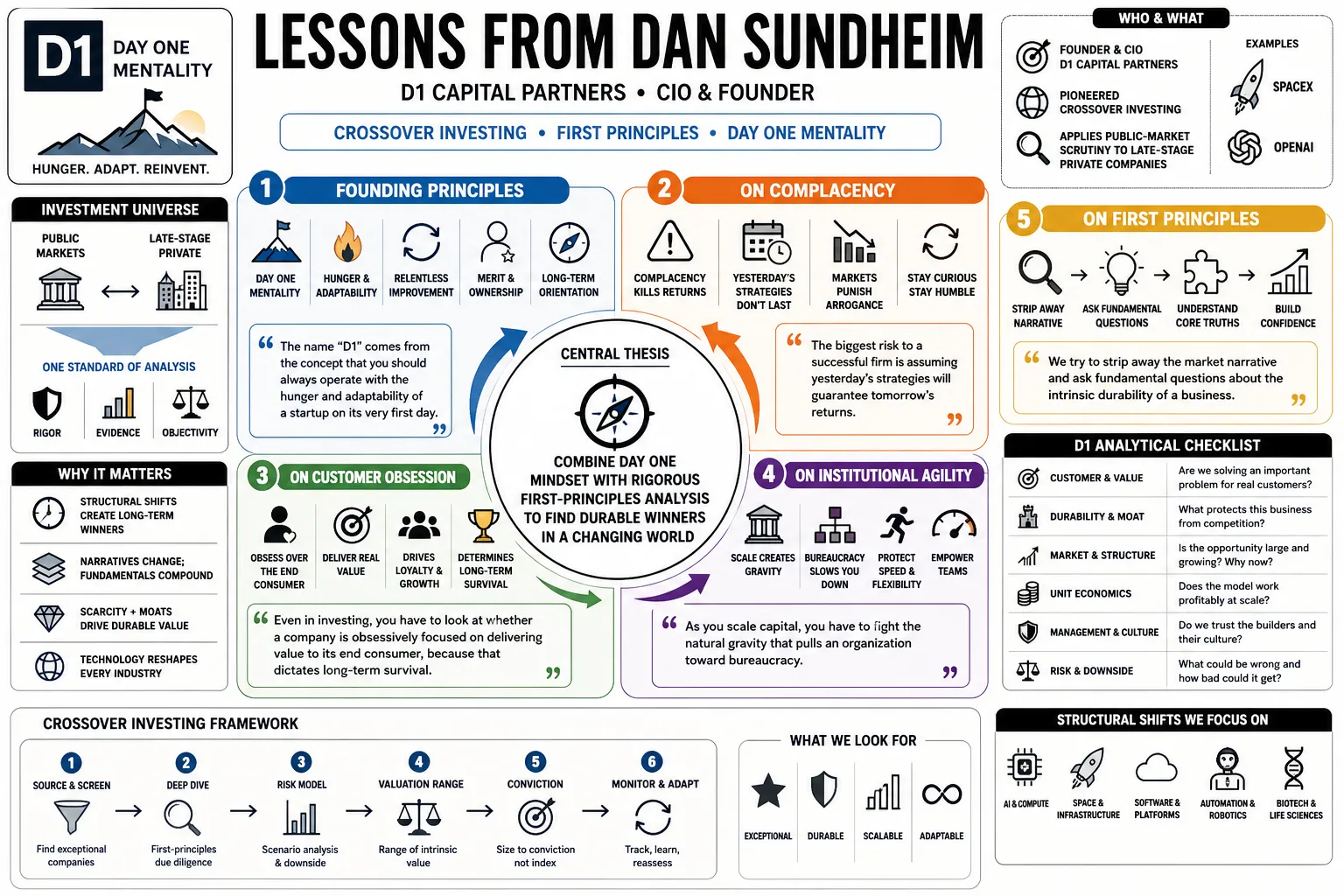

Dan Sundheim is the founder and chief investment officer of D1 Capital Partners. He helped popularize crossover investing by analyzing late-stage private companies like SpaceX and OpenAI with the strict scrutiny usually reserved for public markets. This collection breaks down his approach to valuation and risk, along with his views on structural shifts in technology.

Part 1: The "Day One" Philosophy

- On Founding Principles: "The name 'D1' comes from the concept that you should always operate with the hunger and adaptability of a startup on its very first day." — Source: [Bloomberg Wealth]

- On Complacency: "The biggest risk to a successful firm is assuming yesterday's strategies will guarantee tomorrow's returns." — Source: [Invest Like the Best]

- On Customer Obsession: "Even in investing, you have to look at whether a company is obsessively focused on delivering value to its end consumer, because that dictates long-term survival." — Source: [Hedge Fund Alpha]

- On Institutional Agility: "As you scale capital, you have to fight the natural gravity that pulls an organization toward bureaucracy." — Source: [Cheeky Pint Podcast]

- On First Principles: "We try to strip away the market narrative and ask fundamental questions about the intrinsic durability of a business model." — Source: [Bloomberg Wealth]

- On Long-Term Thinking: "Day one isn't just about speed; it's about making decisions today that compound over decades." — Source: [Invest Like the Best]

- On Stagnation: "Once a management team believes they have arrived, the decline has already begun." — Source: [D1 Capital Investor Letter]

- On Intellectual Curiosity: "The market is constantly evolving, so your primary competitive advantage has to be an endless appetite to learn." — Source: [Value Investors Club]

- On Adapting to Scale: "It is much harder to maintain a startup mentality when you manage billions, but that is exactly when it is most critical." — Source: [Cheeky Pint Podcast]

- On Daily Execution: "Success is less about grand structural shifts and more about stringing together thousands of high-quality daily decisions." — Source: [Invest Like the Best]

Part 2: Crossover Investing

- On Public vs. Private Markets: "The underlying business doesn't know if its stock is publicly traded or privately held. The analysis should be identical." — Source: [Invest Like the Best]

- On Arbitraging Information: "Being active in the private markets gives you an early read on structural shifts that will eventually disrupt public incumbents." — Source: [Hedge Fund Alpha]

- On Capital Structure: "You want to find the best companies in the world and own them, regardless of whether you have to buy them through an IPO or a Series E." — Source: [Cheeky Pint Podcast]

- On Structural Advantages: "Crossover funds have an edge because they can promise a private founder that they will anchor their public offering down the line." — Source: [Financial Times]

- On Valuation Discipline: "Just because a company is private doesn't mean you can suspend the laws of financial gravity when pricing it." — Source: [Institutional Investor]

- On Remaining Private: "Many of the best companies today are choosing to stay private longer simply because they don't want the distraction of quarterly earnings cycles." — Source: [Invest Like the Best]

- On Cross-Pollination: "Our analysts cover a sector holistically, from early-stage disruptors to legacy public mega-caps." — Source: [D1 Capital Investor Letter]

- On Liquidity: "The premium you pay for public liquidity isn't always justified if you are truly investing for a five-year horizon." — Source: [Bloomberg Wealth]

- On Late-Stage Growth: "The sweet spot is finding a private company that has already derisked its product but still has a massive runway for scaling." — Source: [Cheeky Pint Podcast]

Part 3: Fundamental Research and Valuation

- On Bottom-Up Analysis: "You cannot outsource the hard work of reading the filings, talking to suppliers, and understanding the unit economics." — Source: [Value Investors Club]

- On the Lowest-Cost Producer: "In any commoditized or highly competitive industry, the lowest-cost producer is the only one in control of its destiny." — Source: [Invest Like the Best]

- On Durable Cash Flows: "Growth is an input to value, but ultimately you are buying the present value of future free cash flows." — Source: [Bloomberg Wealth]

- On Pattern Recognition: "After looking at thousands of companies, you start to recognize the specific traits that lead to compounding success." — Source: [Cheeky Pint Podcast]

- On Management Quality: "A brilliant business model can be ruined by poor capital allocation, so the team at the top matters immensely." — Source: [Hedge Fund Alpha]

- On Margin of Safety: "You have to build in a margin of safety, not just in the multiple you pay, but in the durability of the revenue stream." — Source: [Institutional Investor]

- On Competitive Moats: "A moat isn't static. It is either widening or shrinking every single day based on execution." — Source: [Invest Like the Best]

- On Forecasting: "We don't try to predict the macro economy; we try to predict how a specific business will perform regardless of the macro environment." — Source: [Bloomberg Wealth]

- On Turnarounds: "Corporate turnarounds are notoriously difficult, but when a new management team can successfully reset the cost base, the equity upside is massive." — Source: [D1 Capital Investor Letter]

Part 4: Risk, Resilience, and The GameStop Squeeze

- On Market Extremes: "The GameStop short squeeze was the worst two weeks of my career. It was a harrowing reminder of market mechanics." — Source: [Bloomberg Wealth]

- On Technical vs. Fundamental Risk: "You can be 100% right on the fundamentals of a short position and still get completely wiped out by technical market dynamics." — Source: [Invest Like the Best]

- On Adjusting Strategy: "After taking extreme pain, the rational response is not to double down, but to reinvent your risk framework." — Source: [Institutional Investor]

- On Emotional Asymmetry: "The pain of losing money always feels sharper than the joy of making it, and you have to train yourself to not let that asymmetry dictate your decisions." — Source: [Cheeky Pint Podcast]

- On Short Selling: "Shorting individual stocks has become structurally more dangerous; we've shifted toward using basket indices for hedging." — Source: [Business Insider]

- On Survival: "In this business, job one is survival. If you get taken out of the game during an anomaly, your long-term thesis doesn't matter." — Source: [Hedge Fund Alpha]

- On Accepting Mistakes: "The faster you can admit you are on the wrong side of a trade, the faster you can protect your capital." — Source: [Invest Like the Best]

- On Volatility: "To capture outlier returns over a decade, you must possess the stomach to endure severe drawdowns." — Source: [Bloomberg Wealth]

- On Systemic Shifts: "Retail coordination fundamentally altered the liquidity profile of heavily shorted equities." — Source: [Financial Times]

- On Moving Forward: "You take the lesson, you adjust the portfolio constraints, and you wake up the next day ready to find new opportunities." — Source: [Cheeky Pint Podcast]

Part 5: Artificial Intelligence and Tech Investing

- On AI Scaling Laws: "The historical predictability of AI scaling laws gives us confidence that injecting more compute and data will yield structurally more capable models." — Source: [Invest Like the Best]

- On Transformational Capital: "Companies like SpaceX and OpenAI aren't just software startups; they require capital expenditure on a scale previously reserved for nation-states." — Source: [D1 Capital Investor Letter]

- On LLM Business Models: "We are still in the early innings of understanding how value will accrue between the foundation models, the cloud providers, and the application layer." — Source: [Cheeky Pint Podcast]

- On Anthropic: "We look past the 'winner-take-all' narrative; there will be multiple massive winners in the frontier model space." — Source: [Financial Times]

- On Legacy Software: "AI is going to be incredibly disruptive to traditional SaaS companies that simply act as workflow wrappers around databases." — Source: [Invest Like the Best]

- On SpaceX: "SpaceX represents a transformational leap in launch economics, which fundamentally changes what is possible in low Earth orbit." — Source: [D1 Capital Investor Letter]

- On Hardware Moats: "The physical constraints of building out data centers and securing energy have become the primary bottlenecks for AI progress." — Source: [Bloomberg Wealth]

- On Strategic Feedback: "As an investor, you want to be close enough to founders to offer strategic insights, like exploring alternative monetization models for AI products." — Source: [Hedge Fund Alpha]

- On Tech Valuations: "You have to separate the hype cycle from the actual revenue trajectory; we are willing to pay up for growth, but not for illusions." — Source: [Invest Like the Best]

- On Foundational Technologies: "Every few decades a technology emerges that lowers the cost of a fundamental input, and AI is doing that for cognitive labor." — Source: [Cheeky Pint Podcast]

Part 6: Private Markets and Venture Strategy

- On Dedicated Funds: "Moving from side pockets to a dedicated private equity structure allows for better alignment of duration between the capital and the investment." — Source: [Institutional Investor]

- On Deal Sourcing: "The best private deals come from having a reputation as a long-term partner who understands the public markets where these companies will eventually live." — Source: [Bloomberg Wealth]

- On Founder Relationships: "Founders don't just want capital; they want investors who can guide them through the transition from a private growth story to a public compounder." — Source: [Invest Like the Best]

- On Venture Returns: "A concentrated bet on a generational company in the private markets can drive the performance of an entire fund." — Source: [Financial Times]

- On Due Diligence: "We apply the exact same rigorous modeling to a late-stage private company as we do to a Fortune 500 public equity." — Source: [Cheeky Pint Podcast]

- On Capital Requirements: "The most ambitious hardware and deep-tech companies require patient, heavy capital that traditional venture wasn't historically built to provide." — Source: [Hedge Fund Alpha]

- On Market Corrections: "When public multiples compress, private markets eventually follow, creating exceptional entry points for disciplined capital." — Source: [D1 Capital Investor Letter]

- On Portfolio Concentration: "Venture is a power-law game. You have to be willing to hold and even size up your winners." — Source: [Invest Like the Best]

- On Exit Environments: "We underwrite our private investments assuming a difficult exit environment, ensuring the company can self-fund if the IPO window shuts." — Source: [Bloomberg Wealth]

Part 7: Lessons from Value Investors Club and Viking Global

- On Early Hustle: "Writing deep-dive short theses under an alias online was my master class in fundamental analysis." — Source: [Business Insider]

- On Forensic Accounting: "Finding a fraud like Orthodontic Centers of America taught me that the numbers tell a story the management team often tries to hide." — Source: [Value Investors Club]

- On Idea Generation: "You have to be a voracious consumer of ideas, reading cases from other investors to understand different frameworks of thinking." — Source: [Cheeky Pint Podcast]

- On Mentorship: "My years at Viking Global instilled a rigorous, repeatable process for tearing down a company’s financials." — Source: [Bloomberg Wealth]

- On Building a Team: "The talent model I learned early on is that you need analysts who are deeply specialized but capable of seeing the broader market context." — Source: [Invest Like the Best]

- On Pitching Ideas: "A great investment pitch must be concise; if you can't explain the thesis in a few sentences, it is probably too complex." — Source: [Value Investors Club]

- On Selling Too Early: "One of my biggest lessons was selling Netflix too soon. When a company is continuously expanding its total addressable market, historical multiples lose relevance." — Source: [Hedge Fund Alpha]

- On Scaling Responsibility: "Managing a small sleeve of capital is very different from overseeing half the firm's assets; the margin for error shrinks dramatically." — Source: [Bloomberg Wealth]

- On Intellectual Honesty: "The best investors I've worked with are the ones who are ruthlessly objective about their own mistakes." — Source: [Invest Like the Best]

Part 8: The Psychology of Markets

- On Routine: "Waking up at 3:00 AM to trade European markets isn't just about edge; it is about establishing an absolute discipline." — Source: [Cheeky Pint Podcast]

- On Stress: "The market has a way of finding your exact breaking point and lingering there." — Source: [Invest Like the Best]

- On Contrarianism: "It is easy to call yourself a contrarian, but it is excruciatingly difficult to hold a position when the entire market is betting against you." — Source: [Bloomberg Wealth]

- On Confidence vs. Arrogance: "You need immense conviction to take a concentrated position, but enough humility to change your mind when the facts change." — Source: [Hedge Fund Alpha]

- On Noise: "In an era of endless information, the ability to filter out the noise and focus on unit economics is a superpower." — Source: [Cheeky Pint Podcast]

- On Talent Location: "You have to go where the talent is, which is why we maintain a dual-headquarters structure to attract younger analysts." — Source: [Bloomberg Wealth]

- On Losing: "A bad trade doesn't make you a bad investor unless you refuse to extract the lesson from it." — Source: [Value Investors Club]

- On Patience: "Sometimes the hardest action to take in public markets is simply doing nothing at all." — Source: [Invest Like the Best]

- On The Long Game: "True compounding, both in capital and in knowledge, only happens when you commit to staying in the arena for decades." — Source: [D1 Capital Investor Letter]