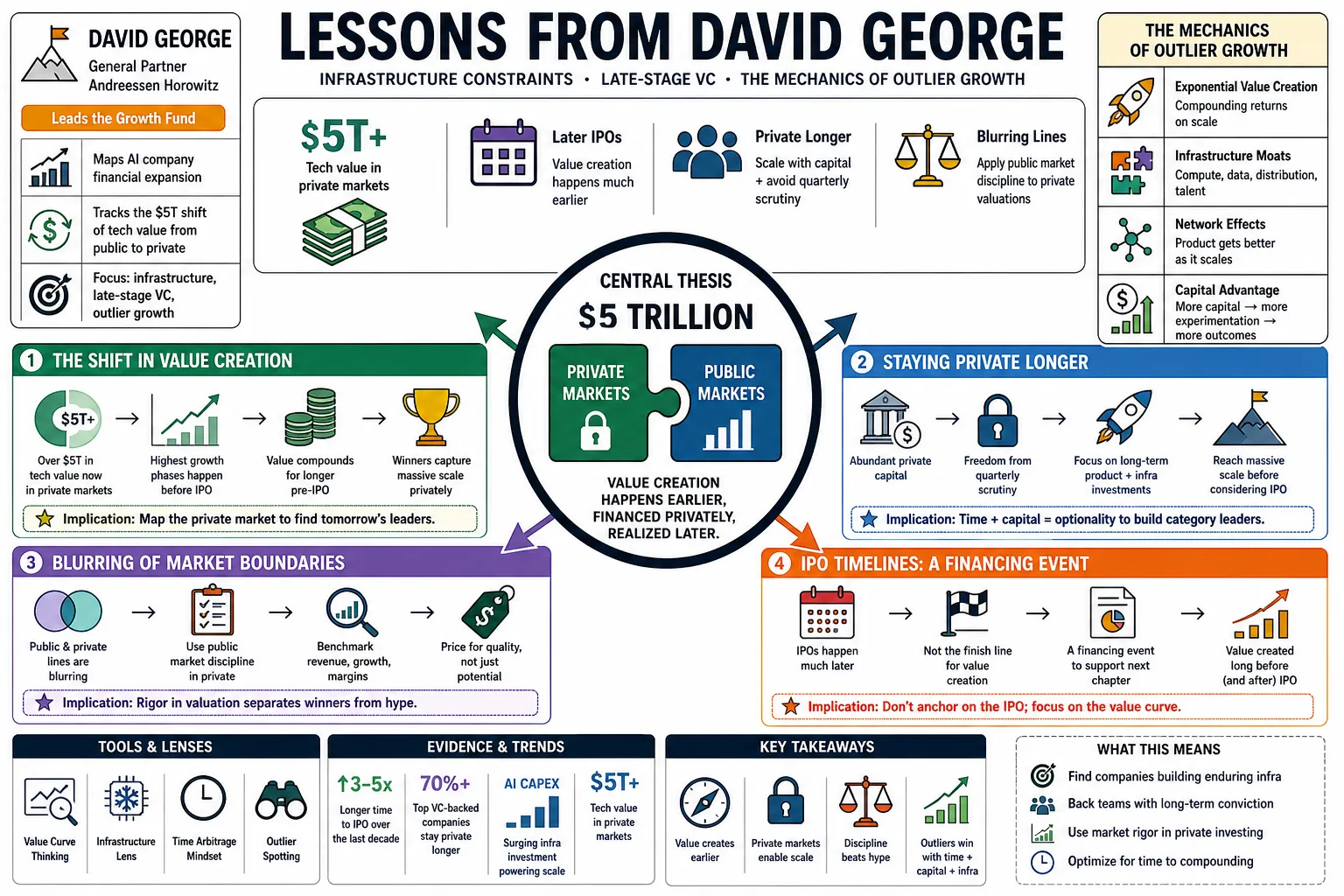

David George is a General Partner at Andreessen Horowitz (a16z), where he leads the firm’s Growth fund. He is known for mapping the rapid financial expansion of modern AI companies and tracking the five-trillion-dollar shift of technology value from public to private markets. This compilation organizes his perspectives on infrastructure constraints, late-stage venture capital, and the mechanics of outlier growth.

Part 1: The Fusion of Private and Public Markets

- On the shift in value creation: "Over five trillion dollars in technology value now resides in private markets, fundamentally altering where the highest growth phases of a company occur." — Source: [Odd Lots Podcast]

- On staying private longer: "Companies are choosing to remain private for extended periods because private capital allows them to reach massive scale without the quarterly pressures of public scrutiny." — Source: [The a16z Show]

- On the blurring of market boundaries: "The line between public and private investing has blurred; growth investors must now apply public market discipline to private market valuations." — Source: [20VC with Harry Stebbings]

- On IPO timelines: "An IPO is no longer the finish line for value creation; it is simply a financing event that happens much later in a company's lifecycle than it did a decade ago." — Source: [The State of Markets Report]

- On capital availability: "The depth of private markets means founders can raise hundreds of millions of dollars to fund capital-intensive projects without needing to ring the opening bell." — Source: [a16z Runtime]

- On public market expectations: "When companies finally go public today, they are expected to have a level of financial maturity and predictability that used to take years of public trading to develop." — Source: [Odd Lots Podcast]

- On illiquidity premiums: "Investors in private growth stages are trading liquidity for the opportunity to capture the steepest part of the growth curve." — Source: [The a16z Show]

- On market corrections: "Private markets eventually take their cues from public markets, but the lag time can create significant pricing dislocations during market transitions." — Source: [20VC with Harry Stebbings]

- On the role of growth funds: "Our job is to bridge the gap between early-stage venture capital and the public markets, providing the capital necessary to build category-defining businesses." — Source: [The State of Markets Report]

Part 2: The Arrival of "Model Busters"

- On defining outliers: "'Model busters' are companies that expand at rates and for durations that completely break traditional financial models and consensus expectations." — Source: [The a16z Show]

- On extreme growth rates: "We are seeing top-tier AI companies compound their revenue at rates as high as 693% year-over-year, which is unprecedented in traditional software." — Source: [a16z Runtime]

- On historical precedents: "The early years of the iPhone represent a classic model buster, where actual sales consistently outpaced even the most aggressive Wall Street estimates." — Source: [The State of Markets Report]

- On underestimating compounding: "Analysts often struggle to model these companies because the human brain is not wired to intuitively grasp hyper-compounding growth over multi-year periods." — Source: [20VC with Harry Stebbings]

- On total addressable market: "Model busters don't just capture existing markets; they expand the total addressable market by introducing entirely new capabilities and use cases." — Source: [The a16z Show]

- On sales and marketing efficiency: "The most striking feature of these companies is their ability to achieve extreme growth with surprisingly low sales and marketing spend, driven entirely by market pull." — Source: [Odd Lots Podcast]

- On sustaining high growth: "The challenge for model busters is not just achieving a high growth rate in year one, but sustaining a rate that defies gravity in years three, four, and five." — Source: [The State of Markets Report]

- On the AI supercharge: "Artificial intelligence is acting as a supercharger for model busters, accelerating product adoption faster than any technology shift we have seen." — Source: [a16z Runtime]

- On identifying them early: "Spotting a model buster requires looking past conservative financial projections and recognizing when a product has hit a profound nerve with consumers or enterprises." — Source: [20VC with Harry Stebbings]

- On traditional valuation metrics: "When a company is growing at several hundred percent organically, standard revenue multiples fail to capture the true present value of the business." — Source: [The a16z Show]

Part 3: AI Application Scaling and Economics

- On revenue per employee: "Modern AI companies are achieving record-breaking Annual Recurring Revenue per employee, frequently hitting between $500k and $1M." — Source: [The State of Markets Report]

- On software efficiency: "AI is enabling software companies to be fundamentally more efficient, producing more output and value with significantly leaner teams." — Source: [20VC with Harry Stebbings]

- On the speed of scaling: "The time it takes for a top-decile AI startup to reach $100 million in ARR has compressed dramatically compared to the standard SaaS era." — Source: [a16z Runtime]

- On organic adoption: "We are seeing enterprise AI applications adopted organically by end-users before top-down IT procurement even gets involved." — Source: [The a16z Show]

- On gross margins: "While AI compute costs can pressure gross margins initially, scale and model optimization consistently drive these margins back toward traditional software profiles." — Source: [Odd Lots Podcast]

- On the service-as-software shift: "AI is turning what used to be low-margin human service businesses into high-margin software businesses." — Source: [The State of Markets Report]

- On replacing incumbent software: "The most successful AI applications don't just add features; they entirely replace legacy software systems by automating the actual work." — Source: [20VC with Harry Stebbings]

- On pricing power: "Companies delivering clear, measurable productivity gains through AI possess immense pricing power, as the ROI is immediately obvious to the buyer." — Source: [The a16z Show]

- On continuous improvement: "Unlike static software, AI products benefit from continuous feedback loops, meaning the product materially improves every time a customer uses it." — Source: [a16z Runtime]

Part 4: Infrastructure and the AI Buildout

- On physical constraints: "The bottlenecks for AI scaling are moving from silicon availability to physical world constraints like energy generation and power grid capacity." — Source: [Odd Lots Podcast]

- On the capital intensity of AI: "Building the infrastructure layer for the next decade of AI requires a capital intensity that rivals the early days of telecommunications or railroads." — Source: [The State of Markets Report]

- On energy demand: "Securing clean, reliable power at a massive scale—often requiring dedicated gas turbines or nuclear sources—is becoming a primary competitive advantage for data centers." — Source: [a16z Runtime]

- On the supply chain: "The physical supply chain for AI infrastructure extends far beyond GPUs; it includes cooling systems, transformers, and highly specialized construction labor." — Source: [The a16z Show]

- On infrastructure utilization: "Despite the massive capital expenditure, the utilization rates of AI infrastructure remain incredibly high due to insatiable developer demand." — Source: [20VC with Harry Stebbings]

- On the duration of the buildout: "The infrastructure phase of this technological cycle is not a two-year trend; it is a decade-long project that will require continuous private and public investment." — Source: [Odd Lots Podcast]

- On hyperscaler dominance: "The major cloud providers are acting as the primary financiers of the AI revolution, converting their balance sheets into computing power." — Source: [The State of Markets Report]

- On edge computing: "As model capabilities grow, the infrastructure will eventually need to decentralize, pushing inference closer to the edge to manage latency and bandwidth." — Source: [The a16z Show]

- On systemic fragility: "The concentration of critical components in specific geographic regions introduces a fragility to the AI buildout that the industry must aggressively diversify." — Source: [a16z Runtime]

Part 5: Growth Investing Mechanics

- On focusing on inputs: "In growth investing, it is critical to focus on the fundamental business inputs—product usage, retention, customer love—rather than obsessing over the temporary output of market valuation." — Source: [20VC with Harry Stebbings]

- On dealing with consensus: "If you only invest when the consensus agrees with you, you will never generate outlier returns; you have to be right about something the market misunderstands." — Source: [The a16z Show]

- On the danger of average: "Venture capital punishes average businesses. A company that is merely 'good' will consume capital and time without ever generating the necessary exit velocity." — Source: [The State of Markets Report]

- On price discipline: "While you must be willing to pay up for true outliers, maintaining price discipline across the rest of the portfolio is what protects the fund during downturns." — Source: [Odd Lots Podcast]

- On assessing market size: "The most common mistake in growth investing is underestimating how much a highly compelling product can expand the boundaries of its market." — Source: [a16z Runtime]

- On unit economics: "High growth covers a multitude of sins, but if the underlying unit economics are fundamentally broken at scale, the business will eventually collapse under its own weight." — Source: [20VC with Harry Stebbings]

- On winning the deal: "Identifying the best company is only half the battle; the other half is convincing the founder that your partnership offers value beyond just the capital." — Source: [The a16z Show]

- On holding periods: "Growth investing requires the patience to hold through volatility. If the fundamental thesis remains intact, short-term market fluctuations should be ignored." — Source: [The State of Markets Report]

- On the role of capital: "In winner-take-most markets, capital can be used as an offensive weapon to accelerate product development and lock in market share before competitors react." — Source: [Odd Lots Podcast]

- On learning from failure: "Post-mortems on investments that failed to scale often reveal that the team compromised on the quality of the product in a rush to meet arbitrary revenue targets." — Source: [a16z Runtime]

Part 6: Evaluating Founders and Teams

- On the strength of strengths: "Our core rule for evaluating leadership is to invest in the founder’s 'strength of strengths.' You back someone for their extraordinary superpower, not their lack of weakness." — Source: [The a16z Show]

- On founder evolution: "The CEO who took the company from zero to ten million in revenue often has to reinvent their management style completely to take it to a hundred million." — Source: [20VC with Harry Stebbings]

- On complementary teams: "A visionary founder must be paired with an exceptional operational team. The superpower needs a highly functional infrastructure to deliver results." — Source: [The State of Markets Report]

- On clarity of vision: "The best founders can explain a complex, decade-long technical roadmap in terms that a non-technical customer immediately understands and values." — Source: [a16z Runtime]

- On dealing with adversity: "Growth is rarely linear. We look for founders who exhibit resilience and intellectual honesty when they inevitably miss a quarter or face a product setback." — Source: [Odd Lots Podcast]

- On hiring standards: "A trailing indicator of a company's future success is the quality of the executives the founder is able to recruit away from safe, established companies." — Source: [The a16z Show]

- On obsessive focus: "Outlier founders are deeply, almost uncomfortably obsessed with the details of their product and the specific friction points of their user experience." — Source: [20VC with Harry Stebbings]

- On capital allocation skills: "As a company reaches the growth stage, the founder's primary job shifts from building the product to effectively allocating capital across multiple bets." — Source: [The State of Markets Report]

- On self-awareness: "Founders who understand their own limitations and proactively hire executives to fill those gaps scale much faster than those who try to manage every function." — Source: [a16z Runtime]

Part 7: Power Laws and Venture Capital Realities

- On the nature of venture returns: "Venture capital is fundamentally a power-law business; the vast majority of a fund's returns will inevitably come from a very small number of massive winners." — Source: [The State of Markets Report]

- On portfolio construction: "Because of the power law, portfolio construction is less about minimizing risk and entirely about maximizing exposure to the absolute best companies in a category." — Source: [20VC with Harry Stebbings]

- On category dominance: "In software and AI, the number one company in a category often captures seventy percent of the market value, leaving the rest to fight over the scraps." — Source: [The a16z Show]

- On the cost of missing out: "The biggest risk in growth investing is not losing your capital on a bad bet; it is passing on the one company that defines the decade." — Source: [Odd Lots Podcast]

- On ownership targets: "To make the power law work mathematically, an investor must not only identify the winner but secure and maintain a meaningful ownership percentage as the company grows." — Source: [a16z Runtime]

- On doubling down: "When a company in the portfolio begins to exhibit the traits of an outlier, the correct strategy is to aggressively double down and deploy more capital." — Source: [The State of Markets Report]

- On the irrelevance of median performance: "Tracking the median performance of venture investments is useless; the asset class only makes sense when viewed through the lens of extreme outliers." — Source: [20VC with Harry Stebbings]

- On recognizing the winner early: "The market often reveals the winner early through undeniable metrics in usage and retention; the job is to recognize those signals before the valuation reflects them." — Source: [The a16z Show]

- On structural advantages: "Firms that can provide deep operational support and networks have a structural advantage in winning the allocations necessary to capitalize on power-law outcomes." — Source: [Odd Lots Podcast]

- On patience and realization: "Power law outcomes take time to mature. A fund must have the structural patience to let a company compound for a decade to realize its full value." — Source: [a16z Runtime]

Part 8: Technological Cycles and Macro Trends

- On the AI product cycle: "Artificial intelligence is not a short-term trend or a bubble; it is a fundamental 10- to 15-year product cycle that will reshape every sector of the economy." — Source: [The a16z Show]

- On the lump-of-labor fallacy: "Fears of an 'AI Job Apocalypse' are rooted in the lump-of-labor fallacy; history shows that technological productivity gains consistently create new industries and net-new jobs." — Source: [The State of Markets Report]

- On historical parallels: "The transition to AI computing is comparable to the shift from on-premise servers to cloud computing, but it is happening at a significantly accelerated pace." — Source: [Odd Lots Podcast]

- On economic deflation: "Software has always been a deflationary force, but AI takes this further by dramatically lowering the marginal cost of intelligence and specialized labor." — Source: [20VC with Harry Stebbings]

- On the speed of adoption: "The speed at which consumers and enterprises are adopting generative AI tools has outpaced the adoption curves of the personal computer, the internet, and the smartphone." — Source: [a16z Runtime]

- On navigating cycles: "The most successful technology investors do not try to time the macroeconomic cycle; they focus on finding companies building fundamental utilities that endure through downturns." — Source: [The a16z Show]

- On the next platform shift: "We are moving from a world where software is a tool you use to a world where software is an agent that acts on your behalf." — Source: [The State of Markets Report]

- On global competitiveness: "The rapid deployment of AI infrastructure is not just a commercial race; it is becoming a critical component of national economic competitiveness." — Source: [Odd Lots Podcast]

- On the long-term outlook: "Despite short-term market volatility, the long-term trajectory of technology remains relentlessly upward, driven by compound innovation and structural shifts in human productivity." — Source: [20VC with Harry Stebbings]