Lessons from David Rosenberg

Economist David Rosenberg, founder of Rosenberg Research and former Chief Economist for North America at Merrill Lynch, is known for his consistently cautious macroeconomic outlook. He frequently warns against market complacency and points to structural deflationary forces in the global economy. This profile breaks down his risk-management framework by examining his skepticism of consensus thinking, his read on central bank policy, and his case for defensive asset allocation.

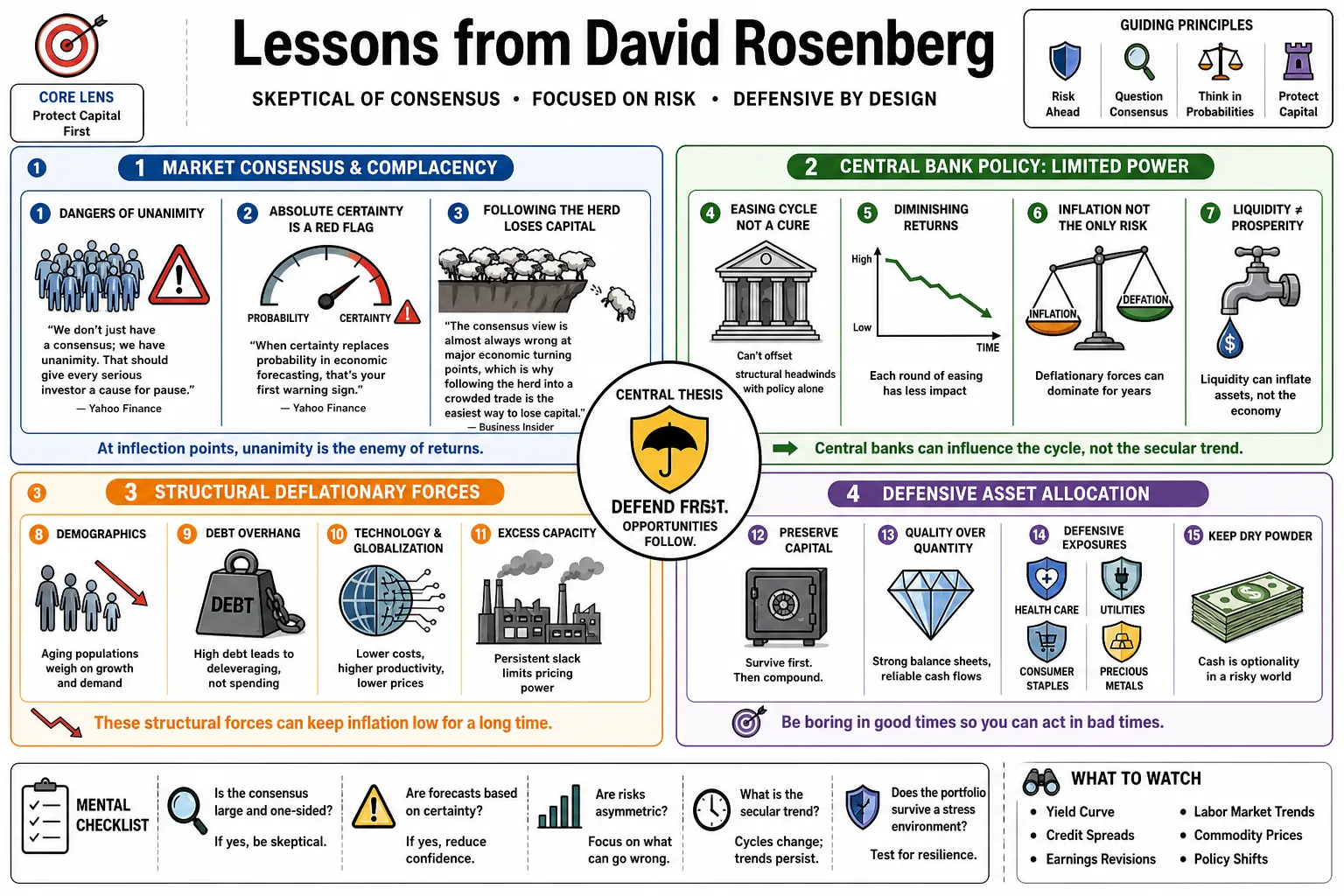

Part 1: Market Consensus & Complacency

- On the dangers of unanimity: "I know I keep harping on this one theme: that the consensus is rarely right at inflection points. And right now, we don't just have a consensus; we have unanimity. That should give every serious investor a cause for pause." — Source: Yahoo Finance

- On absolute certainty: "When certainty replaces probability in economic forecasting, that's your first warning sign." — Source: Yahoo Finance

- On contrarianism: "The consensus view is almost always wrong at major economic turning points, which is why following the herd into a crowded trade is the easiest way to lose capital." — Source: Business Insider

- On ignoring the warning signs: "Markets often dismiss critical underlying weakness by focusing entirely on headline resilience until the breaking point becomes undeniable." — Source: Rosenberg Research

- On groupthink: "When every economist on Wall Street shares the exact same outlook for a soft landing, it is the highest form of systemic risk." — Source: Business Insider

- On market tops: "Euphoria in financial markets is rarely a sign of health; it is usually the psychological peak right before a fundamental breakdown." — Source: Kitco News

- On the illusion of stability: "The appearance of a stable economy is often merely a reflection of a rising stock market, masking deep structural vulnerabilities underneath." — Source: Kitco News

- On risk assessment: "Investors currently treat economic outcomes as a guaranteed positive, completely pricing out the historical probability of a standard business cycle downturn." — Source: Yahoo Finance

- On consensus blindness: "The majority of market participants fail to see recessions coming because they linearly extrapolate current conditions into the future indefinitely." — Source: Business Insider

- On permanent plateaus: "Believing that markets have reached a permanently high plateau is the classic error made by consensus thinkers just before a cyclical correction." — Source: Business Insider

Part 2: The Federal Reserve & Monetary Policy

- On Powell's pivot: "He went from Bambi to Godzilla." — Source: Business Insider

- On late policy shifts: "The Fed's job is to take the punch bowl away as the party gets started, but this version of the Fed took the punch bowl away at 4 a.m., when everybody was pissed drunk." — Source: Business Insider

- On data dependency: "The Fed seems to be focusing not just on flawed data, but on headlines only. I don't sense any analysis of the data by the various FOMC officials as much as reporting of the data." — Source: Business Insider

- On Fed credibility: "This is the weakest Fed ever in my forty-year career, driven entirely by reactive impulses rather than proactive modeling." — Source: Wealthion

- On the interest rate shock: "We've had the biggest interest rate shock since 1981, if I'm not mistaken. 1981 was followed by 1982, which was not a mild recession by the way." — Source: Business Insider

- On being behind the curve: "Central banks consistently wait too long to ease policy, mistakenly relying on lagging economic indicators until a contraction is already underway." — Source: Hidden Forces

- On policy errors: "Over-tightening into a fundamentally weak economy is a classic central bank mistake that turns mild slowdowns into severe recessions." — Source: Macro Voices

- On ignoring structural shifts: "The Fed often fights the last war, fixating on cyclical price pressures while missing the massive secular forces reshaping the economy." — Source: Financial Post

- On rate cuts: "The Federal Reserve will likely be slow to cut interest rates, trapped by their own rhetoric even as the underlying economic data continues to sputter." — Source: BNN Bloomberg

- On the neutral rate: "At 2.75 per cent, that neutral rate is supposed to coincide with an economy in balance, an economy that does not have a disinflationary excess supply backdrop. That's where they have to get to at a minimum." — Source: BNN Bloomberg

Part 3: Inflation, Deflation & Japanification

- On deflationary shocks: "We are now staring down the barrel of a deflationary shock, and it amazes me how all the bond bears, inflation-phobes, and Fed policy hawks are missing this secular shift as they continue to play by the old rules." — Source: Business Insider

- On the aftermath of bubbles: "Deflation not inflation will be the topic when housing, equity bubbles pop." — Source: Financial Post

- On long-term inflation trends: "Inflation is going to be a lot lower. I'm talking about Japanification. I think inflation in the next three, five, 10 years is going to be a lot lower than 2% to 2.5%." — Source: Business Insider

- On the inflation narrative: "The same people calling for inflation now were calling for inflation back then. They're the ones that have to answer as to why it is that inflation in the final analysis... we never did get the big inflation." — Source: Mauldin Economics

- On secular vs. cyclical forces: "I'm not going to try and obscure what is secular and what is cyclical. To me that's a complete waste of time. We had secular deflationary forces in play in the last cycle." — Source: Macro Voices

- On excess capacity: "The global economy is characterized by excess supply and overcapacity, which inherently puts immense downward pressure on prices over the long term." — Source: Rosenberg Research

- On technology's impact: "Rapid technological advancement and automation are massive structural deflationary forces that easily overwhelm temporary cyclical inflation." — Source: ValueTrend

- On demographic headwinds: "Aging populations across the developed world create a Japan-style economic environment that structurally suppresses both aggregate demand and sustained inflation." — Source: Business Insider

- On misreading price spikes: "Temporary supply chain disruptions are often mistakenly extrapolated by the market as permanent inflation, ignoring the eventual demand destruction." — Source: Wealthion

- On the ultimate risk: "The true danger to the global economy is not runaway inflation, but a debt-deflation spiral triggered by the popping of historic asset bubbles." — Source: Financial Post

Part 4: The Consumer & The Wealth Effect

- On consumer fragility: "The modern consumer is hanging on by a string, increasingly relying on credit cards and buy-now-pay-later schemes to offset falling real incomes." — Source: Memo From The Chief Economist

- On stock market dependence: "The only reason why everything looks okay is because of the stock market. It all comes down to the stock market." — Source: Kitco News

- On exhausted savings: "Consumers are effectively at the end of the rope, having entirely depleted their excess pandemic-era savings while facing higher borrowing costs." — Source: Business Insider

- On the wealth effect illusion: "Consumer spending is currently being propped up not by wage growth, but by an artificial equity wealth effect concentrated almost entirely among high-income households." — Source: Kitco News

- On credit erosion: "We just replaced credit cards with what happened with subprime mortgages 15 years ago. This is how a recession starts, it starts with a significant erosion in credit." — Source: Business Insider

- On capital versus labor: "The relative share of profits to the size of the economy has never been this extreme at a peak, meaning income from capital risks replacing income from labor." — Source: Memo From The Chief Economist

- On spending sustainability: "Consumption driven by asset price appreciation rather than organic income generation is historically unsustainable and highly vulnerable to market corrections." — Source: Rosenberg Research

- On real wages: "Shrinking take-home pay and underlying job losses severely contradict the mainstream narrative of a solid economy." — Source: Benzinga

- On borrowing capacity: "With interest rates significantly elevated, the consumer's ability to borrow their way out of an income shortfall has been fundamentally impaired." — Source: Business Insider

Part 5: The Labor Market & "No-Hire, No-Fire"

- On hiring freezes: "We are operating in a no-hire, no-fire economy, where corporate hiring rates have quietly fallen well below pre-pandemic levels." — Source: Kitco News

- On vulnerability to layoffs: "At these low levels of hiring, even a modicum of layoffs will lead to successive monthly declines in nonfarm payrolls." — Source: Kitco News

- On lagging indicators: "Wages, like the labor market, tend to be a coincident, a lagging indicator." — Source: Wealthion

- On the household survey: "Analysts place too much faith in headline nonfarm payrolls while ignoring the persistent weakness and job losses frequently revealed in the underlying Household survey." — Source: Benzinga

- On underlying job losses: "The reality of hidden job losses completely undermines the Federal Reserve's assumption of an overheated labor market." — Source: Benzinga

- On silent contractions: "The labor market is experiencing a silent contraction, characterized by reduced hours worked and a shift toward part-time employment rather than outright mass firings." — Source: Traders Union

- On corporate margins: "Companies will inevitably resort to cutting headcount when their pricing power evaporates and profit margins begin to compress under the weight of higher rates." — Source: Macro Voices

- On structural weakness: "The headline unemployment rate often masks deep structural weaknesses, such as declining labor force participation among prime-age workers." — Source: Rosenberg Research

- On job market sentiment: "Workers are increasingly hesitant to quit their jobs voluntarily, signaling a profound internal shift in labor market confidence that official data has yet to capture." — Source: Business Insider

Part 6: Recession Probabilities & Indicators

- On predicting downturns: "Recessions don't announce themselves with a megaphone. They arrive precisely when they're least expected, when the consensus has declared them impossible." — Source: Yahoo Finance

- On probability distributions: Rosenberg frames macro calls as probability distributions rather than fixed certainties: investors need a base case, a stated conviction level, and Plan B/C/D/E scenarios for where the base case could be wrong. — Reference: Excess Returns transcript where Rosenberg discusses conviction levels, base cases, and Plan B/C/D/E scenario thinking

- On the catalyst: "If the artificial support provided by the stock market fades, then there's no doubt in my mind that we're going to have a recession next year." — Source: Kitco News

- On the yield curve: "The inversion of the yield curve remains the most reliable leading indicator of a recession, reflecting the bond market's certainty of future economic weakness." — Source: Business Insider

- On leading indicators: "While coincident data looks fine, the persistent decline in the index of leading economic indicators is loudly signaling an inevitable business cycle downturn." — Source: Macro Voices

- On credit tightening: "Recessions invariably begin when bank lending standards tighten and credit conditions erode, choking off the lifeblood of business expansion." — Source: Yahoo Finance

- On ignoring history: "Economists who currently claim we have achieved a permanent soft landing are willfully ignoring the historical track record of every major rate-hiking cycle." — Source: Business Insider

- On hidden weaknesses: "Broad economic aggregates often mask severe recessions already occurring in specific, rate-sensitive sectors like housing and manufacturing." — Source: Traders Union

- On the point of no return: "Once employment momentum decisively breaks downward, the negative feedback loop between lost income and reduced spending makes a recession unavoidable." — Source: Rosenberg Research

Part 7: Historical Parallels & Bubbles

- On the 1929 parallel: "Almost like the Irving Fisher refrain in 1929: 'Stock prices have reached what looks like a permanently high plateau.'" — Source: Business Insider

- On the dot-com era: "Maybe a bit like Abby Joseph Cohen ahead of the tech wreck: 'We expect 2001 to be yet another year of profit expansion, albeit at a slower pace.'" — Source: Business Insider

- On the 2008 financial crisis: "Or how about Chuck Prince's doozy in July 2007 that 'as long as the music is playing, you've got to get up and dance.'" — Source: Business Insider

- On being labeled a perma-bear: "If that [experiencing Black Monday on his first day] happened to you, then you'd be Eeyore the donkey for the rest of your professional life as well. They call me the permabear. It's almost genetic in some way." — Source: Business Insider

- On extreme valuations: "The current market exhibits all the classic symptoms of a mega bubble, mirroring the euphoric, unhinged valuations seen at major historical peaks." — Source: Macro Voices

- On cyclical amnesia: "Market participants suffer from a profound historical amnesia, forgetting that every era of unchecked speculation eventually ends in a brutal mean reversion." — Source: Rosenberg Research

- On AI speculation: "The massive speculative frenzy surrounding artificial intelligence bears a striking resemblance to previous thematic bubbles that ultimately collapsed under their own weight." — Source: Benzinga

- On navigating extremes: "Studying financial history is the only way to recognize when asset prices have completely detached from underlying economic reality." — Source: Wealthion

- On the illusion of new paradigms: "Every generation convinces itself that the old rules of finance no longer apply, only to learn the hard way that the business cycle has not been repealed." — Source: Financial Post

Part 8: Asset Allocation: Bonds, Gold, & Defensive Investing

- On the purpose of gold: "I know it's a tradition among gold investors to think of gold as an insurance policy against catastrophe... but gold is also a thing you need to increase prosperity." — Source: Sprott

- On central bank gold buying: "The Chinese central bank is so ridiculously under-golded compared to all its peers. That alone will keep gold trudging to new highs." — Source: Sprott

- On Treasury bonds: "Treasuries are still likely to be a very good risk manager for stocks. That is, they go up when stocks get hit hard." — Source: Cut The Crap Investing

- On bond bubbles: "It is ludicrous to talk about a bubble in a security in which the capital is fully secure and pays a return." — Source: Business Insider

- On portfolio resilience: "My advice is to ignore market and macro pundits and ensure that your portfolio, like mine, captures at least a chunk of the upside while not participating in the downside." — Source: Financial Post

- On diversification: "All markets move in cycles, but not simultaneously, which is why diversification (as I like to say) is not some dirty 15-letter word." — Source: Financial Post

- On the perma-bear label: "I must say it gets a little tiring to always be labelled a ‘perma bear.’ There is no room for ‘perma anything’ in this business because nothing is permanent. Change is constant." — Source: Financial Post

- On risk management: Rosenberg says his investing philosophy starts with two rules: never put all your eggs in one basket, and never treat anything as a sure thing; the discipline is to respect the probabilities of all outcomes and focus on risk-adjusted returns. — Reference: Financial Post column where Rosenberg states his two investing philosophies and risk-adjusted-return focus

- On defensive positioning: "In an environment characterized by extreme valuations and macroeconomic fragility, prioritizing capital preservation through high-quality bonds and precious metals is the only rational strategy." — Source: Rosenberg Research