David Samra is the founding partner of the Artisan Partners International Value Team and the lead portfolio manager of the Artisan International Value Fund since its inception in 2002. He is known for the practice of "quality arbitrage"—buying excellent global businesses only when they trade at a steep discount to their intrinsic value. This profile is worth reading to understand how a disciplined focus on balance sheets, management quality, and a strict 30% margin of safety can consistently compound capital in international markets.

Part 1: The Core Philosophy of Value

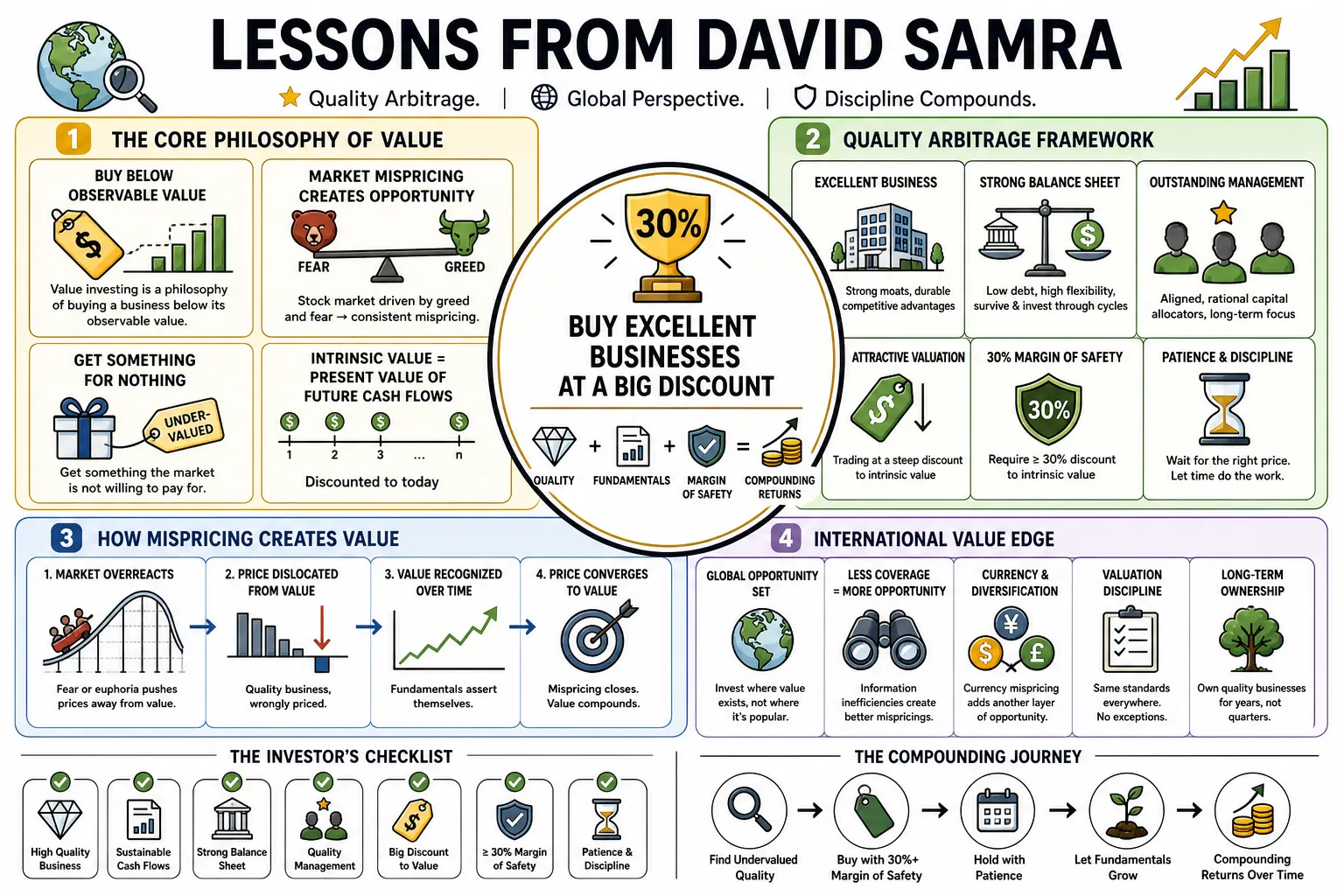

- On the essence of value investing: "Value investing is a philosophy of buying a business below its observable value. By definition, it cannot be a misguided principle." — Source: [Forbes]

- On taking advantage of market behavior: "The stock market is driven by greed and fear, leading to a consistent process of mispricing. Value investing aims to take advantage of mispricing." — Source: [Forbes]

- On the core objective: "When I approach an equity, I'm trying to get something for nothing — something that the market is not willing to pay for." — Source: [Business Insider]

- On intrinsic value: "The value of a business is the present value of its future cash flows." — Source: [Business Insider]

- On quality arbitrage: The strategy relies on finding high-quality businesses that the market has temporarily mispriced due to short-term fears or complexities. — Source: [Artisan Partners]

- On continuous application: The core tenets of identifying undervalued, high-quality businesses remain the most effective path to long-term performance, regardless of technological changes. — Source: [The Meb Faber Show]

- On the fundamental factors: Every potential investment must possess four primary traits: it must be a good company, trading at a steep discount, with a strong balance sheet and excellent management. — Source: [Behind the Balance Sheet]

- On the origins of his framework: His disciplined philosophy was heavily shaped by his studies at Columbia Business School and his early career training under Mario Gabelli. — Source: [Graham & Doddsville]

- On the relationship between price and value: Value is not determined by the ticker moving up or down on a screen, but by the tangible cash flows the business can generate over decades. — Source: [Morningstar]

- On long-term wealth generation: True compounding happens when you identify structural mispricings and allow the underlying business economics to resolve the valuation gap over time. — Source: [Value Investor Insight]

Part 2: Defining Quality in a Business

- On defining a good company: A good company is fundamentally characterized by its ability to generate sustainable, high returns on invested capital over long periods. — Source: [Behind the Balance Sheet]

- On rejecting mediocrity: Refusing to sacrifice business quality for a low price is the primary distinction between traditional deep-value investing and quality arbitrage. — Source: [Business Insider]

- On business durability: The underlying economics of the business must be strong enough to survive economic downturns and industry disruptions. — Source: [Morningstar]

- On competitive moats: A business worth buying must have a demonstrable advantage that prevents competitors from eroding its profit margins over time. — Source: [Artisan Partners]

- On evaluating growth: Growth is only valuable if it is accompanied by high returns on capital; stagnant growth with poor returns destroys shareholder value regardless of how cheap the stock looks. — Source: [Barron's]

- On sustainable cash flows: Earnings can be manipulated by accounting, but the ability to generate consistent, free cash flow is the true marker of business health. — Source: [Value Investor Insight]

- On consumer brands: Well-established consumer brands often provide the pricing power necessary to protect margins during inflationary environments. — Source: [Barron's]

- On fixing temporary problems: The best opportunities often arise in high-quality companies facing operational issues that the broader market treats as permanent impairments. — Source: [Hedge Fund Alpha]

- On capital intensity: Businesses that require massive amounts of capital just to maintain their current competitive position are generally poor candidates for long-term compounding. — Source: [Graham & Doddsville]

- On industry structures: It is vastly easier to invest in a business operating within a rational, consolidated industry than one fighting for survival in a fragmented, highly competitive market. — Source: [Behind the Balance Sheet]

Part 3: The Importance of the Balance Sheet

- On financial strength as a shield: A robust balance sheet is essential for companies to weather unexpected economic shocks without permanently impairing equity. — Source: [Behind the Balance Sheet]

- On the dangers of leverage: High leverage combined with a cheap valuation is a classic recipe for a value trap, as debt eliminates the margin of safety. — Source: [Business Insider]

- On optionality: Companies with strong financial health have the flexibility to play offense during downturns, buying back stock or acquiring distressed competitors. — Source: [Value Investor Insight]

- On evaluating debt: Debt must always be measured against the stability of the cash flows servicing it; cyclical businesses require far more conservative balance sheets than stable consumer staples. — Source: [Artisan Partners]

- On avoiding zeroes: Protecting the downside is the first rule of compounding, and the most common cause of permanent capital loss is excessive debt. — Source: [Morningstar]

- On hidden liabilities: A thorough balance sheet analysis must go beyond stated debt to account for underfunded pensions, off-balance-sheet leases, and looming legal liabilities. — Source: [Graham & Doddsville]

- On interest rate sensitivity: Businesses reliant on continuous refinancing at low interest rates are structurally fragile and typically fail the quality test. — Source: [The Meb Faber Show]

- On cash generation: A balance sheet is only as strong as the cash flowing into it; an asset-heavy balance sheet with poor liquidity offers little protection in a crisis. — Source: [Behind the Balance Sheet]

- On shareholder structure: Understanding who owns the debt and how the capital structure is organized is vital when investing in complex international markets. — Source: [Columbia Business School]

Part 4: Assessing and Engaging with Management

- On the role of executives: Management teams are primarily responsible for two things: running the underlying operations efficiently and allocating the cash those operations generate. — Source: [Behind the Balance Sheet]

- On capital allocation: The ability of a management team to make disciplined capital-allocation decisions is often the primary driver of long-term shareholder returns. — Source: [Value Investor Insight]

- On aligning interests: Management must be economically aligned with common shareholders, either through significant direct ownership or properly structured incentive programs. — Source: [Morningstar]

- On assessing track records: You evaluate a CEO by looking at their past actions during industry downturns, not by the promises they make in their current slide decks. — Source: [Artisan Partners]

- On share repurchases: Buybacks are only evidence of good management if they are executed when the stock is trading below intrinsic value, not when it is expensive. — Source: [Barron's]

- On corporate governance: Independent, active boards of directors are essential to prevent management teams from engaging in empire-building at the expense of shareholders. — Source: [Graham & Doddsville]

- On in-person evaluations: Sitting down with management teams and observing their corporate culture firsthand is a crucial part of the qualitative due diligence process. — Source: [Behind the Balance Sheet]

- On handling mistakes: Excellent management teams admit when they have made an operational error and pivot quickly, rather than throwing good money after bad. — Source: [The Meb Faber Show]

- On constructive engagement: As large shareholders, it is sometimes necessary to actively engage with management to encourage the divestment of non-core assets or improvements in capital structure. — Source: [Business Insider]

Part 5: Navigating International Markets

- On global complexity: Investing internationally requires a deep, nuanced understanding of different legal, cultural, and macroeconomic frameworks across jurisdictions. — Source: [Columbia Business School]

- On the generalist model: Using a team of generalists rather than strict regional specialists prevents analytical silos and allows capital to flow to the absolute best global ideas. — Source: [Mutual Fund Observer]

- On state-owned enterprises: Companies with heavy government involvement often prioritize political objectives over shareholder returns, making them difficult to value reliably. — Source: [Artisan Partners]

- On macro versus micro: While macroeconomic conditions dictate the environment, investment decisions should ultimately be driven by bottom-up, company-specific fundamentals. — Source: [Barron's]

- On emerging markets: The higher growth rates in emerging markets must be heavily discounted by the elevated risks in corporate governance, currency volatility, and rule of law. — Source: [Value Investor Insight]

- On European equities: Structurally lower growth in Europe can still yield excellent investments if the business is globally diversified and management is focused on margin improvement. — Source: [Bloomberg]

- On currency risks: Currency fluctuations are an unavoidable aspect of international investing, but buying companies with strong global cash flows provides a natural operational hedge. — Source: [Behind the Balance Sheet]

- On accounting standards: You must adjust reported earnings across different countries to a standardized baseline to accurately compare the free cash flow yields of global peers. — Source: [Morningstar]

- On home-country bias: Investors who restrict themselves to domestic equities arbitrarily cut themselves off from high-quality, undervalued businesses operating in other developed markets. — Source: [The Meb Faber Show]

Part 6: Understanding and Avoiding Value Traps

- On defining a trap: A value trap is a company that appears mathematically cheap but suffers from structurally deteriorating economics that will slowly destroy the business. — Source: [Business Insider]

- On the illusion of low multiples: A low price-to-earnings ratio is meaningless if the earnings power is about to be permanently cut in half by technological obsolescence. — Source: [Forbes]

- On secular decline: You cannot rely on a reversion to the mean in an industry that is experiencing a permanent, secular contraction in demand. — Source: [Artisan Partners]

- On bad management as a trap: Even a great asset will act as a value trap if the management team continually misallocates the cash flows generated by that asset. — Source: [Graham & Doddsville]

- On the turnaround fallacy: Turnarounds rarely turn, and it is far more profitable to buy good businesses facing temporary headwinds than bad businesses trying to reinvent themselves. — Source: [Value Investor Insight]

- On rigid cost structures: Companies with high fixed costs and shrinking revenues will see their margins compress violently, turning a cheap stock into an expensive one overnight. — Source: [Behind the Balance Sheet]

- On evaluating catalysts: If a stock is cheap but lacks any plausible mechanism or management action to unlock that value, it is likely dead money. — Source: [Barron's]

- On the danger of book value: Buying based strictly on a discount to book value is dangerous if the assets on the balance sheet do not actually generate an economic return. — Source: [The Meb Faber Show]

- On knowing when to sell: If the original investment thesis regarding the quality of the business is proven wrong, you must sell immediately, regardless of the current price. — Source: [Morningstar]

- On avoiding the easiest mistakes: The simplest way to avoid value traps is to implement a strict, unyielding requirement for strong balance sheets and high returns on capital. — Source: [Hedge Fund Alpha]

Part 7: Portfolio Management and Capital Allocation

- On the 30% rule: An investment is typically only initiated when the stock can be purchased at a discount of at least 30% to a conservative estimate of intrinsic value. — Source: [Behind the Balance Sheet]

- On the function of the margin: A steep discount to intrinsic value serves two purposes: it protects against analytical errors and provides the mechanism for outsized returns. — Source: [Business Insider]

- On position sizing: Capital should be concentrated in the highest-conviction ideas where the combination of business quality and margin of safety is the most extreme. — Source: [Morningstar]

- On holding cash: If the market does not provide opportunities that meet the strict criteria for quality and price, building cash is preferable to deploying capital into mediocre ideas. — Source: [Value Investor Insight]

- On portfolio turnover: A process focused on buying businesses at a steep discount and waiting for the gap to close naturally results in low portfolio turnover and tax efficiency. — Source: [Artisan Partners]

- On managing risk: Risk is not measured by the historical volatility of a stock price, but by the probability of suffering a permanent loss of capital. — Source: [Forbes]

- On selling winners: A disciplined process requires trimming or selling positions when the market price eventually reaches or exceeds the calculated intrinsic value. — Source: [Barron's]

- On avoiding benchmark hugging: To meaningfully outperform an index over the long term, a portfolio must look significantly different from that index in its sector and country allocations. — Source: [The Meb Faber Show]

- On absolute returns: The goal is to generate absolute compounding of wealth over a business cycle, not just to lose slightly less money than the benchmark during a bear market. — Source: [Graham & Doddsville]

Part 8: Patience, Discipline, and the Investor's Mindset

- On the timeline of value: The investment philosophy is deeply long-term in nature; investors must be willing to wait years for a thesis to fully materialize. — Source: [The Meb Faber Show]

- On ignoring noise: The daily fluctuations of the stock market are driven by human emotion and algorithmic trading, neither of which has any bearing on the true value of a business. — Source: [Forbes]

- On the difficulty of discipline: The intellectual concepts of value investing are simple, but the behavioral execution—buying when others are panicking and selling when they are euphoric—is incredibly difficult. — Source: [Behind the Balance Sheet]

- On independent thinking: To find mispriced assets, you must conduct your own primary research and be comfortable holding a view that directly contradicts the current Wall Street consensus. — Source: [Columbia Business School]

- On the nature of volatility: Market volatility should not be viewed as a risk to be minimized, but as the primary mechanism that creates the pricing inefficiencies value investors rely on. — Source: [Artisan Partners]

- On historical perspective: Studying past market cycles provides the emotional grounding necessary to act rationally during periods of extreme financial distress. — Source: [Graham & Doddsville]

- On intellectual honesty: A successful investor must constantly re-evaluate their own assumptions and be willing to admit when the facts have changed. — Source: [Morningstar]

- On institutional imperatives: The pressure to generate short-term quarterly performance forces most market participants into crowded, expensive trades, leaving the long-term horizon completely uncrowded. — Source: [Value Investor Insight]

- On the ultimate edge: In a market where everyone has access to the same financial data, the only sustainable competitive advantage is having a longer time horizon and superior emotional control. — Source: [Business Insider]