Lessons from David Swensen

David Swensen ran the Yale endowment from 1985 until 2021, pulling institutional money out of standard stocks and bonds to buy illiquid assets like private equity and real estate. The resulting Yale Model proved that funds with long time horizons could capture higher returns, permanently changing how universities invest. His writing outlines this approach to asset allocation while delivering a blunt critique of the retail financial industry.

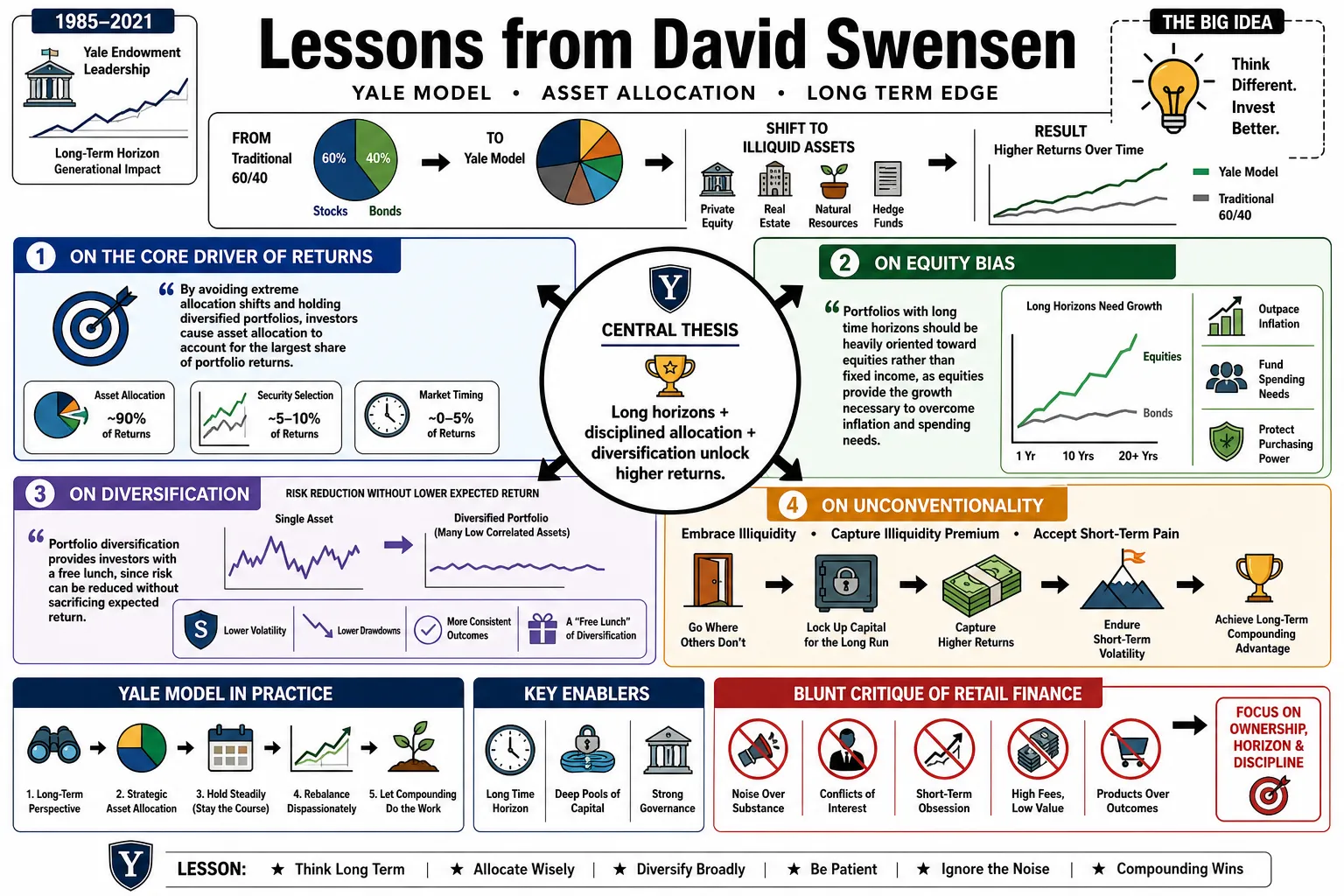

Part 1: The Yale Model and Asset Allocation

- On the core driver of returns: "By avoiding extreme allocation shifts and holding diversified portfolios, investors cause asset allocation to account for the largest share of portfolio returns." — Source: Unconventional Success

- On equity bias: "Portfolios with long time horizons should be heavily oriented toward equities rather than fixed income, as equities provide the growth necessary to overcome inflation and spending needs." — Source: Pioneering Portfolio Management

- On diversification: "Portfolio diversification provides investors with a free lunch, since risk can be reduced without sacrificing expected return." — Source: Pioneering Portfolio Management

- On unconventionality: "Establishing and maintaining an unconventional investment profile requires acceptance of uncomfortably idiosyncratic portfolios, which frequently appear downright imprudent in the eyes of conventional wisdom." — Source: Pioneering Portfolio Management

- On the futility of market timing: Asset allocation decisions should be strategic and long-term, because market timing and security selection are net negatives for most investors due to fees and taxes. — Source: Unconventional Success

- On human capital: "If an individual owns a small business, the equity-oriented nature of the private holding argues for a lower equity position in the investor's financial holdings." — Source: Unconventional Success

- On liabilities: "From a portfolio perspective, liabilities act like negative assets. In other words, borrowing by an individual offsets lending by that individual." — Source: Unconventional Success

- On defining the goal: Institutions must clearly define their purpose and time horizon before selecting assets, ensuring the portfolio directly serves the underlying operational mission. — Source: Pioneering Portfolio Management

- On enduring principles: "Diversification makes sense and equity-oriented portfolios produce higher returns. Those principles do not go in and out of favor." — Source: ProPublica

- On taking the broad view: "Investors benefit from taking the broadest view of their financial circumstances, integrating personal assets, future earning power, and financial portfolios." — Source: Unconventional Success

Part 2: The Mutual Fund Industry and Wall Street

- On the negative-sum game: "The harsh reality of the negative-sum game dictates that, in aggregate, active managers lose to the market by the amount it costs to play in the form of management fees, trading commissions, and dealer spread." — Source: Unconventional Success

- On industry failure: "The mutual-fund industry consistently fails to meet the basic active management goal of providing market-beating returns." — Source: Unconventional Success

- On financial complexity: "As a general rule of thumb, the more complexity that exists in a Wall Street creation, the faster and farther investors should run." — Source: Pioneering Portfolio Management

- On performance drag: "Wall Street's share of the pie defines the amount of performance drag experienced by the would-be market beaters." — Source: Pioneering Portfolio Management

- On fund of funds: "Fund of funds are a cancer on the institutional-investor world. They facilitate the flow of ignorant capital." — Source: Wall Street Journal

- On mutual fund taxation: "The management of taxable mutual-fund assets without considering the tax consequences of trading activity represents a highly visible, yet little considered scandal." — Source: Unconventional Success

- On the motive of fund companies: The core conflict of the mutual fund industry is that it gathers assets to maximize fee revenue, which directly contradicts the investor’s goal of maximizing net returns. — Source: Unconventional Success

- On high turnover: Excessive trading by mutual fund managers generates high transaction costs and tax liabilities that quietly destroy investor wealth year after year. — Source: Unconventional Success

- On marketing vs. performance: Wall Street spends massive amounts on marketing to convince individuals they can beat the market, obscuring the mathematical reality that most will underperform. — Source: Unconventional Success

- On non-profit alternatives: Investors are far better served by utilizing member-owned or not-for-profit financial institutions, like Vanguard, which eliminate the inherent conflict between corporate shareholders and fund investors. — Source: Unconventional Success

Part 3: Active vs. Passive Management

- On the great divide: "The most important distinction in the investment world does not separate individuals and institutions; the most important distinction divides those investors with the ability to make high quality active management decisions from those investors without active management expertise." — Source: Pioneering Portfolio Management

- On passive dominance: "When you look at the results on an after-fee, after-tax basis, over reasonably long periods of time, there's almost no chance that you end up beating the index fund." — Source: Unconventional Success

- On efficient markets: "Passive management strategies suit highly efficient markets, such as U.S. Treasury bonds, where market returns drive results and active management adds little or nothing." — Source: Pioneering Portfolio Management

- On inefficient markets: "Active management strategies fit inefficient markets, such as private equity, where market returns contribute very little to ultimate results and investment selection provides the fundamental source of return." — Source: Pioneering Portfolio Management

- On the odds of active success: "Fully 95 percent of active investors lose to the passive alternative... Equity mutual-fund returns in recent decades provide a textbook example of the negative-sum game of active management." — Source: Unconventional Success

- On the spectrum of activity: "The right solution is not in the middle. The right solution is at one extreme or the other. One end of the spectrum is being intensively active. The other is being completely passive." — Source: ProPublica

- On the cost of active management: The hurdles for active managers are enormous because they must overcome management fees, trading costs, and cash drag just to match the index. — Source: Unconventional Success

- On index fund selection: "With all assets, I recommend that people invest in index funds because they're transparent, understandable, and low-cost." — Source: Yale Alumni Magazine

- On the illusion of skill: Many active managers mistake bull market luck for skill, a reality that only becomes apparent when market cycles shift and structural flaws are exposed. — Source: Pioneering Portfolio Management

- On evaluating active managers: True active management requires a qualitative assessment of the manager's character, intelligence, and alignment with the investor, not a mere review of past performance metrics. — Source: Pioneering Portfolio Management

Part 4: The Illiquidity Premium

- On embracing illiquidity: "Market participants willing to accept illiquidity achieve a significant edge in seeking high risk-adjusted returns." — Source: Pioneering Portfolio Management

- On the cost of liquidity: "Because market players routinely overpay for liquidity, serious investors benefit by avoiding overpriced liquid securities and by embracing less liquid alternatives." — Source: Pioneering Portfolio Management

- On value orientation: "Intelligent acceptance of illiquidity and a value orientation constitute a sensible, conservative approach to portfolio management." — Source: Pioneering Portfolio Management

- On private equity as a model: "Private equity... where you buy the company, you make the company better and then you sell the company is a superior form of capitalism." — Source: CFR Interview (2017)

- On time horizon advantages: Institutions with perpetual time horizons waste a massive competitive advantage if they limit themselves to daily liquid securities. — Source: Pioneering Portfolio Management

- On alternative asset classes: True portfolio defense comes from uncorrelated illiquid assets, such as timber and private real estate, which behave fundamentally differently than public equities. — Source: Pioneering Portfolio Management

- On market inefficiencies: Illiquid markets lack the constant pricing and analyst coverage of public markets, creating wider spreads between price and intrinsic value for skilled managers to exploit. — Source: Pioneering Portfolio Management

- On locking up capital: Investors must be structurally prepared to lock up their capital for years, ensuring that unexpected cash flow needs do not force the sale of illiquid assets at distressed prices. — Source: Pioneering Portfolio Management

- On sizing alternative bets: An allocation to alternative assets must be large enough to meaningfully impact the total portfolio; token allocations introduce complexity without moving the needle. — Source: Pioneering Portfolio Management

Part 5: Fiduciary Duty and Alignment of Interests

- On defining success: A good external manager defines winning by producing great investment returns for the client, rather than generating huge flows of fees for themselves. — Source: Pioneering Portfolio Management

- On managing taxable assets: "A serious fiduciary with responsibility for taxable assets recognizes that only extraordinary circumstances justify deviation from a simple strategy of selling losers and holding winners." — Source: Unconventional Success

- On mission-driven work: "People think working for something other than the most money you could get is an odd concept, but it seems a perfectly natural concept to me." — Source: Yale Alumni Magazine

- On structure and behavior: Fiduciaries must ensure the legal and fee structures of their investments align the manager’s incentives explicitly with the long-term compounding of the client's capital. — Source: Pioneering Portfolio Management

- On institutional responsibility: Endowment managers are stewards of intergenerational equity; their duty is to preserve purchasing power so future students receive the same financial support as current ones. — Source: Pioneering Portfolio Management

- On evaluating character: When interviewing fund managers, the assessment of their integrity and ethical compass is as critical as analyzing their financial models. — Source: Pioneering Portfolio Management

- On independent thinking: A fiduciary cannot simply outsource their judgment to consultants; they must take personal responsibility for understanding and defending every asset in the portfolio. — Source: Pioneering Portfolio Management

- On the failure of diversification in a crisis: True fiduciaries know that in extreme panics, correlations move to one; therefore, survival depends on fundamentally safe assets like U.S. Treasuries, not just a mix of risky ones. — Source: Consuelo Mack Wealthtrack

- On tax efficiency as a duty: For the individual investor, tax avoidance through strategic placement of assets in retirement accounts is a primary fiduciary duty to oneself. — Source: Unconventional Success

Part 6: Rebalancing and Contrarian Discipline

- On contrarian action: "Supremely rational investors take the further step of acting against consensus, rebalancing to long-term portfolio targets by buying the out-of-favor and selling the in-vogue." — Source: Pioneering Portfolio Management

- On maintaining targets: "Unless investors engage in systematic rebalancing of portfolios, the risk and return profile of the actual portfolio invariably differs from the risk and return profile of the desired portfolio." — Source: Pioneering Portfolio Management

- On mechanical execution: "To maintain desired allocations, investors sell assets that appreciate in relative terms and buy assets that depreciate in relative terms." — Source: Unconventional Success

- On reputational risk: "Unless institutions maintain contrarian positions through difficult times, the resulting damage of buying high and selling low imposes severe financial and reputational costs on the institution." — Source: Pioneering Portfolio Management

- On the pain of discipline: Rebalancing forces investors to allocate capital to the asset classes that have caused them the most recent pain, a mathematically sound practice that feels emotionally unnatural. — Source: Unconventional Success

- On systematic moves: Rebalancing should be an automatic, policy-driven action rather than a discretionary choice, removing human emotion from periods of market stress. — Source: Pioneering Portfolio Management

- On the danger of momentum: Letting winners run without trimming them exposes the portfolio to concentration risk and leaves the investor vulnerable to the inevitable mean reversion of markets. — Source: Unconventional Success

- On the courage to act: Having a contrarian strategy is useless without the institutional fortitude to execute it when colleagues and committee members are panicking. — Source: Pioneering Portfolio Management

- On continuous assessment: Rebalancing is not a one-time event but a continuous process of assessing market prices relative to long-term portfolio targets and adjusting accordingly. — Source: Pioneering Portfolio Management

Part 7: Individual vs. Institutional Investing

- On retail access to alternatives: Individuals should generally avoid hedge funds and private equity, as the high-quality managers are closed to new capital, leaving retail investors with overpriced, second-tier options. — Source: Unconventional Success

- On the Core Six: A sensible portfolio for an individual consists of U.S. Stocks, Foreign Developed Stocks, Emerging Markets, Real Estate (REITs), U.S. Treasury Bonds, and TIPS. — Source: Yale Alumni Magazine

- On Real Estate: For individuals lacking access to private real estate deals, inexpensive Real Estate Investment Trust (REIT) index funds provide necessary exposure to real assets and inflation protection. — Source: Unconventional Success

- On U.S. Treasuries: "U.S. Treasury bonds provide protection against financial crises and deflationary shocks, serving as the ultimate safe haven in a well-diversified individual portfolio." — Source: Yale Alumni Magazine

- On TIPS: Treasury Inflation-Protected Securities (TIPS) are an essential tool for the individual investor to explicitly hedge against unexpected spikes in inflation. — Source: Unconventional Success

- On corporate bonds: Individuals should avoid corporate bonds; they fail to provide the safety of Treasuries during equity market crashes while capping upside potential. — Source: Unconventional Success

- On simplicity: While institutions require dedicated staffs to manage complex alternative portfolios, individuals must embrace simplicity to prevent high costs from destroying their returns. — Source: Unconventional Success

- On the opportunity for success: "In spite of the massive failure of the mutual-fund industry, investors willing to take an unconventional approach to portfolio management enjoy the opportunity to achieve financial success." — Source: Unconventional Success

- On self-awareness: The single biggest advantage an individual has is the ability to know their own limitations and choose a passive strategy that requires zero active forecasting. — Source: Unconventional Success

Part 8: Markets, Crises, and Human Behavior

- On market complacency: "When you compare the fundamental risks that we see all around the globe with the lack of volatility in our securities markets, it's profoundly troubling." — Source: CFR Interview (2017)

- On historical memory: Investors routinely forget past crises, acting with shock during downturns despite the historical inevitability of events like 1987, 1998, and 2008. — Source: CFR Interview (2017)

- On behavior during a panic: During market collapses, the analysis shifts abruptly from bottom-up fundamental security selection to top-down macroeconomic survival. — Source: Consuelo Mack Wealthtrack

- On the failure of conventional wisdom: Following the herd feels safe in the short term but guarantees mediocre returns and exposes the portfolio to the same catastrophic downside as the broad market. — Source: Pioneering Portfolio Management

- On emotional investing: The market mechanism is designed to exploit human emotion, systematically transferring wealth from those who panic to those who adhere to a disciplined framework. — Source: Unconventional Success

- On the limits of models: Financial models and historical correlations are useful guides, but they break down during severe crises when human panic overrides mathematical expectations. — Source: Pioneering Portfolio Management

- On recognizing mistakes: Even the best investors make poor active management decisions; the key to survival is recognizing the error quickly and refusing to let ego justify holding a losing position. — Source: Pioneering Portfolio Management

- On short-termism: Wall Street’s obsession with quarterly earnings creates a structural misalignment with long-term capital aggregators, forcing companies into decisions that destroy long-term value. — Source: Pioneering Portfolio Management

- On the nature of capitalism: Despite its flaws, bubbles, and periods of irrationality, the capital market remains the most effective mechanism for allocating resources and generating long-term wealth. — Source: CFR Interview (2017)