Lessons from David Zorub

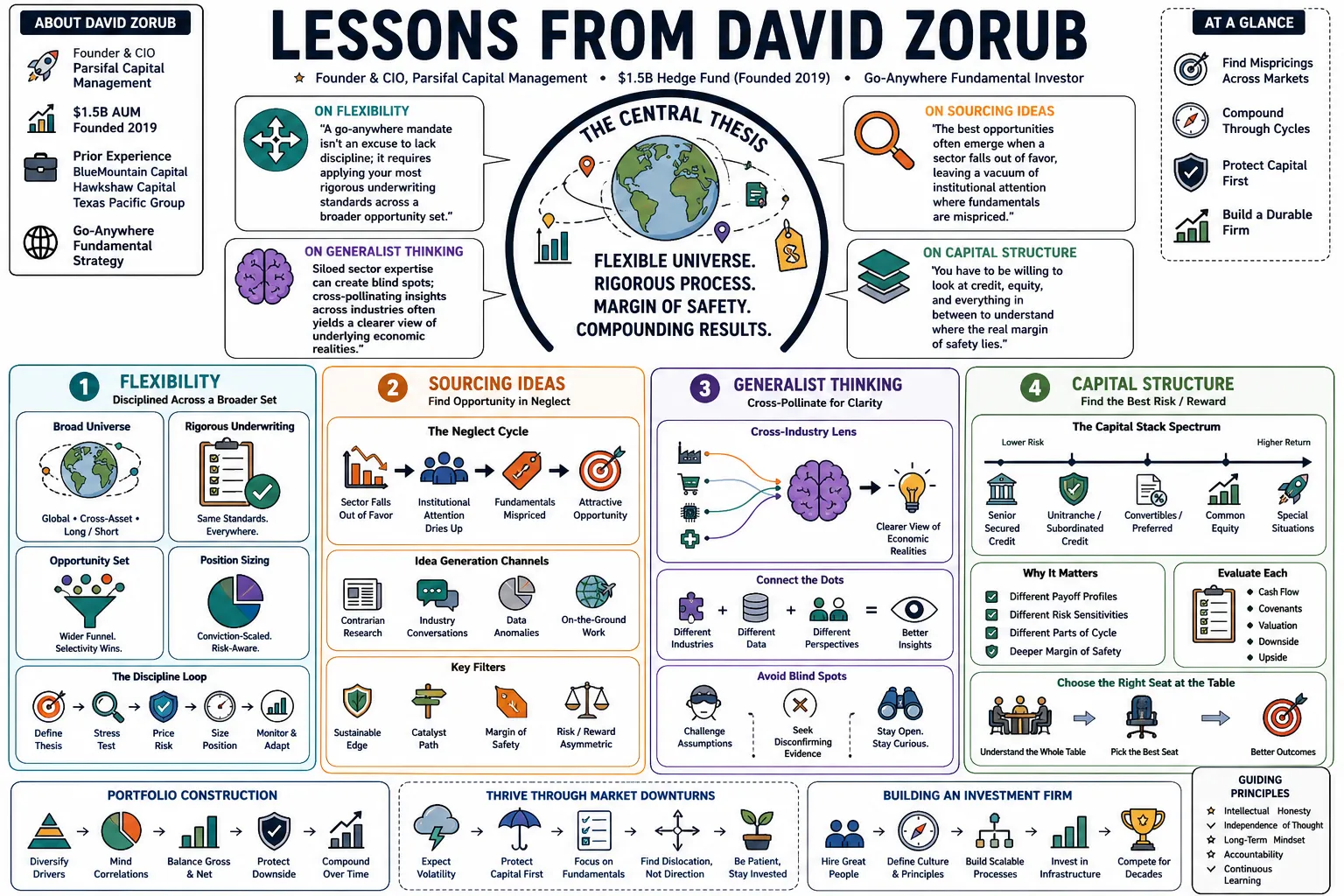

David Zorub is the founder and CIO of Parsifal Capital Management, a $1.5 billion hedge fund launched in 2019. Known for a "go-anywhere" fundamental investment strategy, he previously worked at BlueMountain Capital Management, Hawkshaw Capital, and Texas Pacific Group. This collection covers his approach to portfolio construction, handling market downturns, and the practical work of building an investment firm.

Part 1: The Foundation of a Go-Anywhere Strategy

- On Flexibility: "A go-anywhere mandate isn't an excuse to lack discipline; it requires applying your most rigorous underwriting standards across a broader opportunity set." — Source: [Capital Allocators, Episode 96]

- On Sourcing Ideas: "The best opportunities often emerge when a sector falls out of favor, leaving a vacuum of institutional attention where fundamentals are mispriced." — Source: [Capital Allocators, Episode 434]

- On Generalist Thinking: "Siloed sector expertise can create blind spots; cross-pollinating insights across industries often yields a clearer view of underlying economic realities." — Source: [Capital Allocators, Episode 96]

- On Capital Structure: "You have to be willing to look at credit, equity, and everything in between to understand where the real margin of safety lies." — Source: [Santangels Review]

- On Adaptability: "Markets regime-shift faster than they used to. A static playbook will eventually get you run over if you can't pivot your focus." — Source: [Capital Allocators, Episode 434]

- On Avoiding Crowded Trades: "Consensus is comfortable but expensive. The premium returns are found in the overlooked and misunderstood pockets of the market." — Source: [Capital Allocators, Episode 96]

- On the Value of Patience: "Sometimes the highest returning action is doing nothing while you wait for a pitch that falls perfectly into your strike zone." — Source: [Capital Allocators, Episode 434]

- On Defining the Mandate: "You have to define your universe broadly enough to capture dislocation, but narrowly enough that you actually understand the businesses you own." — Source: [Capital Allocators, Episode 96]

- On Cross-Asset Analysis: "Understanding the credit narrative of a business frequently gives you an information advantage when trading its equity." — Source: [Santangels Review]

- On Geographic Flexibility: "Regional biases can limit performance; a truly global view allows you to arbitrate valuations across different regulatory and economic environments." — Source: [Capital Allocators, Episode 434]

Part 2: Building and Structuring a Hedge Fund

- On Launching Parsifal: "Building a firm requires as much thought on the operational architecture as it does on the investment engine." — Source: [Capital Allocators, Episode 96]

- On Day One Priorities: "The goal on day one isn't to put all your capital to work immediately; it is to establish a culture of rigorous debate and process integrity." — Source: [Capital Allocators, Episode 96]

- On Institutional Alignment: "Your structure must align your duration of capital with the duration of your investment thesis. Mismatches there are fatal." — Source: [Capital Allocators, Episode 434]

- On Scaling AUM: "Growth in assets should be a byproduct of compounding and performance, rather than the primary objective of the business." — Source: [Capital Allocators, Episode 434]

- On Selecting Partners: "You want limited partners who understand that fundamental investing is lumpy and requires a multi-year horizon to execute properly." — Source: [Capital Allocators, Episode 96]

- On Early Mistakes: "Every new manager underestimates the sheer volume of non-investment decisions required to keep the lights on and the firm compliant." — Source: [Capital Allocators, Episode 96]

- On Operational Soundness: "An operationally sound back-office prevents errors and frees the investment team to focus entirely on generating returns." — Source: [Santangels Review]

- On Brand Building: "Your reputation is built on the numbers you put up, paired with the transparency and consistency of your communication when things go wrong." — Source: [Capital Allocators, Episode 434]

- On Fee Structures: "Fees have to be structured in a way that rewards long-term outperformance rather than just asset gathering." — Source: [Capital Allocators, Episode 96]

Part 3: Navigating Market Headwinds

- On Macro Volatility: "You cannot predict the macro, but you can build a portfolio durable enough to survive various macroeconomic states without suffering permanent impairment." — Source: [Capital Allocators, Episode 434]

- On Rate Environments: "A transition from zero interest rates forces the market to once again care about the cost of capital and actual free cash flow generation." — Source: [Capital Allocators, Episode 434]

- On Inflation: "Inflation exposes businesses that lack true pricing power. It separates the companies with moats from those that merely rode a wave of cheap money." — Source: [Santangels Review]

- On Short Selling in Bull Markets: "Shorting in a liquidity-driven rally is a painful exercise; you have to size positions assuming the market can remain irrational longer than you expect." — Source: [Capital Allocators, Episode 434]

- On Liquidity Crunches: "When liquidity dries up, correlations go to one. Your only defense is having a deep understanding of what you own and the capital to take advantage of the panic." — Source: [Capital Allocators, Episode 434]

- On Staying Rational: "The hardest part of a drawdown is trusting the underwriting you did when the environment was calm. If the facts haven't changed, you hold." — Source: [Capital Allocators, Episode 96]

- On Identifying Value Traps: "A low multiple isn't enough. In a headwind, cheap companies can always get cheaper if their terminal value is permanently impaired." — Source: [Capital Allocators, Episode 434]

- On Sector Rotations: "We do not try to time sector rotations; instead, we look for idiosyncratic opportunities that will work regardless of which sector is currently in favor." — Source: [Santangels Review]

- On Market Psychology: "Fear is a much stronger emotion than greed, and it creates the most rapid and dramatic mispricings in the market." — Source: [Capital Allocators, Episode 434]

- On Adaptation: "The strategies that worked brilliantly in the 2010s are not the same strategies that will generate outsized returns in a capital-constrained environment." — Source: [Capital Allocators, Episode 434]

Part 4: Risk Management and Portfolio Construction

- On Sizing Positions: "Position sizing should be entirely a function of your conviction level and the asymmetric nature of the risk-reward, rather than matching an index weight." — Source: [Capital Allocators, Episode 96]

- On Concentration: "A concentrated portfolio requires you to be right more often, but it is the only reliable way to generate meaningful absolute returns." — Source: [Capital Allocators, Episode 96]

- On Gross vs. Net Exposure: "Managing your net exposure dynamically allows you to play defense when the opportunity set is poor, without having to liquidate your best ideas." — Source: [Capital Allocators, Episode 434]

- On Downside Protection: "The first question we ask is never 'how much can we make?' It is always 'how do we lose money on this investment, and how much can we lose?'" — Source: [Santangels Review]

- On Factor Risks: "You have to be acutely aware of the unintended factor bets in your portfolio; otherwise, you might think you are generating excess returns when you are just riding momentum." — Source: [Capital Allocators, Episode 434]

- On Hedging: "A good hedge goes beyond an inverse ETF; it requires a carefully underwritten short position that is expected to generate returns independently of market direction." — Source: [Capital Allocators, Episode 96]

- On Portfolio Balance: "You want a mix of structural compounders and idiosyncratic catalysts so that the portfolio has different engines driving return at different times." — Source: [Capital Allocators, Episode 434]

- On Cutting Losses: "The hardest discipline to enforce is knowing when the thesis is broken and taking the loss before it becomes a permanent impairment of capital." — Source: [Capital Allocators, Episode 96]

- On Margin of Safety: "Margin of safety is not a mathematical formula; it is a qualitative judgment about the durability of the business franchise in stress scenarios." — Source: [Santangels Review]

Part 5: Fundamental Analysis and Value Creation

- On Cash Flow: "Earnings can be manipulated by accounting assumptions, but cash flow is the undeniable truth of a business's health." — Source: [Capital Allocators, Episode 434]

- On Management Quality: "We spend an enormous amount of time evaluating capital allocation decisions. Management teams that allocate capital poorly will eventually destroy a great business." — Source: [Capital Allocators, Episode 96]

- On Competitive Moats: "A true moat is visible in pricing power. If a company cannot raise prices without losing volume, the moat is an illusion." — Source: [Capital Allocators, Episode 434]

- On Reading the Footnotes: "The most valuable insights are rarely in the press release; they are buried in the footnotes of the 10-K where the risks are quietly disclosed." — Source: [Santangels Review]

- On Intrinsic Value: "Intrinsic value is a range, not a point estimate. If your thesis relies on hitting a precise terminal multiple, your margin for error is too thin." — Source: [Capital Allocators, Episode 96]

- On Catalysts: "Value is subjective, but catalysts are objective. A cheap stock needs a tangible event to force the market to close the valuation gap." — Source: [Capital Allocators, Episode 434]

- On the Sum of the Parts: "Complex businesses are frequently mispriced because the market applies a conglomerate discount. Understanding each segment independently is where the edge lies." — Source: [Capital Allocators, Episode 96]

- On Capital Cycles: "Following the flow of capital into and out of industries gives you a roadmap for where returns on invested capital will expand or contract." — Source: [Capital Allocators, Episode 434]

- On Turnarounds: "Turnarounds are historically difficult to execute. We prefer to bet on great businesses facing temporary, solvable issues rather than bad businesses trying to reinvent themselves." — Source: [Santangels Review]

- On Primary Research: "You cannot rely entirely on sell-side research. You have to talk to suppliers, competitors, and former employees to get the unvarnished truth about a company." — Source: [Capital Allocators, Episode 96]

Part 6: Team Dynamics and Leadership

- On Hiring Analysts: "I look for intellectual curiosity and the ability to hold a contrarian view without being arrogant. The best analysts know what they don't know." — Source: [Capital Allocators, Episode 96]

- On Intellectual Honesty: "A healthy investment culture is one where a junior analyst feels completely comfortable telling the CIO that their thesis is fundamentally flawed." — Source: [Capital Allocators, Episode 434]

- On Decision Making: "Consensus kills performance. If everyone on the team agrees on a name, we are probably too late to the trade." — Source: [Capital Allocators, Episode 96]

- On Retaining Talent: "You keep great people by giving them genuine autonomy and tying their compensation directly to the performance they generate, rather than firm-wide AUM." — Source: [Santangels Review]

- On Handling Mistakes: "We conduct post-mortems on every losing trade, not to assign blame, but to figure out if our process failed or if we just encountered bad luck." — Source: [Capital Allocators, Episode 434]

- On Mentorship: "My job as a manager is to take a smart person and teach them how to filter noise, frame a thesis, and understand when to swing hard." — Source: [Capital Allocators, Episode 96]

- On Diversity of Thought: "If your entire investment team went to the same three schools and worked at the same three banks, your groupthink will eventually destroy capital." — Source: [Capital Allocators, Episode 434]

- On Managing Ego: "The market is a ruthless humbler. The moment you believe you have it all figured out is the exact moment you are about to take a massive hit." — Source: [Capital Allocators, Episode 96]

- On Firm Culture: "Culture is defined by the behaviors you tolerate when times are tough, not by what is written on a plaque in the lobby." — Source: [Santangels Review]

Part 7: The Evolution of the Hedge Fund Industry

- On Passive vs. Active: "The relentless rise of passive investing has created massive inefficiencies in small and mid-cap spaces where price discovery is broken." — Source: [Capital Allocators, Episode 434]

- On Algorithmic Trading: "Machines are incredible at processing data, but they are terrible at parsing context. Our edge remains in qualitative judgment." — Source: [Capital Allocators, Episode 96]

- On Information Parity: "The edge today lies less in getting the data first and more in synthesizing it better and maintaining a longer time horizon than your peers." — Source: [Capital Allocators, Episode 434]

- On the Multi-Manager Model: "Platform funds have forced single-manager firms to be clearer about their value proposition; we cannot compete on day-to-day trading, we compete on deep, multi-year underwriting." — Source: [Capital Allocators, Episode 434]

- On Alignment of Interests: "The industry has slowly moved toward better alignment, but LPs still need to be rigorous about demanding hurdle rates and appropriate lock-ups." — Source: [Santangels Review]

- On Special Purpose Vehicles (SPVs): "Co-investments and SPVs are powerful tools, but they can distract a manager from their core mandate if they become the primary focus." — Source: [Capital Allocators, Episode 96]

- On ESG Integration: "Governance has always been a core tenet of fundamental investing; the broader environmental and social metrics require careful scrutiny to separate reality from marketing." — Source: [Capital Allocators, Episode 434]

- On Retail Participation: "Retail flow creates extreme dislocations. It provides liquidity to exit positions, but it also creates traps where valuations detach entirely from reality." — Source: [Capital Allocators, Episode 434]

- On the Future of Alpha: "Alpha generation will increasingly rely on the willingness to look silly in the short term to be proven right in the long term." — Source: [Capital Allocators, Episode 96]

Part 8: Lessons from the Institutional Path

- On Private Equity Roots: "Working in private equity teaches you to view a business as an owner, focusing on operations and cash flow rather than quarterly earnings beats." — Source: [Capital Allocators, Episode 96]

- On Lessons from BlueMountain: "My time at BlueMountain ingrained the importance of institutional-grade infrastructure and the necessity of managing credit and equity risk symmetrically." — Source: [Santangels Review]

- On Banking: "Investment banking provides an incredible foundation in financial modeling, but it takes years to unlearn the habit of trying to build a spreadsheet to justify a transaction." — Source: [Capital Allocators, Episode 96]

- On Career Transitions: "Moving from a massive platform to starting your own firm is the most jarring transition; suddenly, you are responsible for the thermostat as well as the portfolio." — Source: [Capital Allocators, Episode 96]

- On Network Building: "Your network in this industry is your most vital sourcing tool. The best ideas often come from quiet conversations with former colleagues, rather than from sell-side blasts." — Source: [Capital Allocators, Episode 434]

- On Resilience: "The institutional path teaches you that careers are long. A bad quarter is inevitable; how you communicate and recover from it defines your longevity." — Source: [Santangels Review]

- On Continuous Learning: "The day you stop reading and adapting is the day your returns start to decay. The market is a constantly evolving puzzle." — Source: [Capital Allocators, Episode 434]

- On Managing Stress: "You have to decouple your personal identity from your daily performance, otherwise the emotional volatility will burn you out before you reach your peak." — Source: [Capital Allocators, Episode 96]

- On the End Goal: "Ultimately, we are stewards of capital. Our job is to protect purchasing power and compound wealth so our partners can meet their obligations." — Source: [Capital Allocators, Episode 434]