Lessons from Deven Parekh

Deven Parekh has led over 140 software and internet investments as a Managing Director at Insight Partners since 2000. He made his name by taking early stakes in companies like Twitter and Alibaba and deploying in-house teams to scale mid-stage firms. These notes track his practical approach to evaluating software economics and managing investments through shifting market cycles.

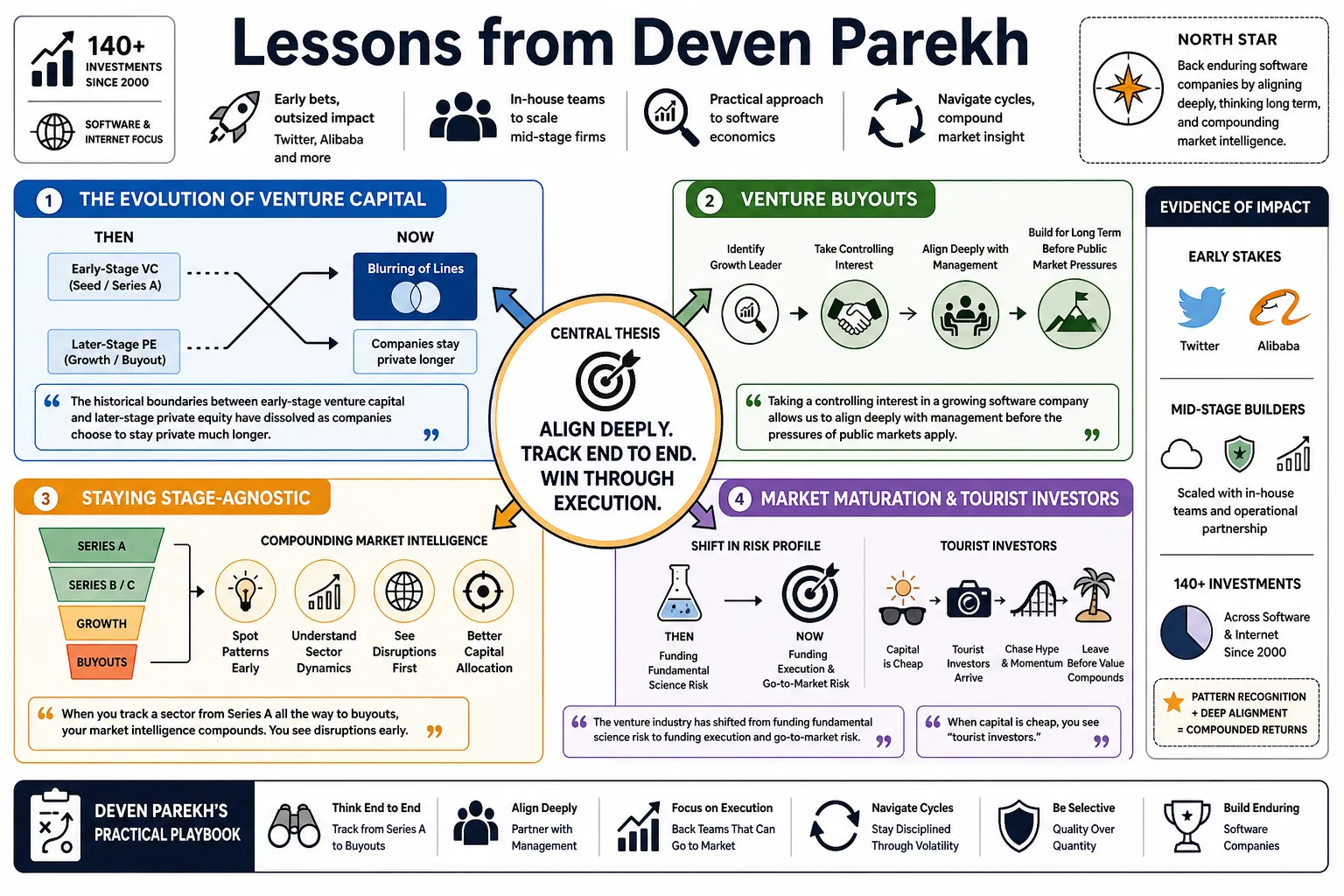

Part 1: The Evolution of Venture Capital

- On the Blurring of Lines: "The historical boundaries between early-stage venture capital and later-stage private equity have dissolved as companies choose to stay private much longer." — Source: [Masters in Business]

- On Venture Buyouts: "Taking a controlling interest in a growing software company allows us to align deeply with management before the pressures of public markets apply." — Source: [Capital for Good Podcast]

- On Staying Stage-Agnostic: "When you track a sector from Series A all the way to buyouts, your market intelligence compounds. You see disruptions early." — Source: [Private Markets Insights]

- On Market Maturation: "The venture industry has shifted from funding fundamental science risk to funding execution and go-to-market risk." — Source: [Upfront Summit]

- On Tourist Investors: "When capital is cheap, you see 'tourist' capital enter venture, but sustainable returns require enduring operational support rather than passive check-writing." — Source: [This Week in Startups]

- On Capital as a Commodity: "Money alone no longer differentiates a firm. A modern venture partner must bring a playbook for scaling." — Source: [Dry Powder Podcast]

- On the IPO Window: "Going public is a funding event, not a finish line. The decision should hinge on internal readiness, never external market exuberance." — Source: [Masters in Business]

- On Patience: "The best returns often come from holding winners significantly longer than the traditional fund cycle dictates." — Source: [Insight Partners]

- On Structural Advantage: "Firms that build deep, specialized teams internally are the ones equipped to underwrite complex, multi-stage software companies." — Source: [Dry Powder Podcast]

- On Information Asymmetry: "In the early 2000s, investors held all the data. Today, founders are highly educated on metrics, meaning our value must come from post-investment execution." — Source: [Upfront Summit]

Part 2: Software and SaaS Dynamics

- On Software Eating the World: "We are still in the early innings of software penetrating traditional, non-tech industries." — Source: [Insight Partners]

- On SaaS Economics: "The beauty of a well-run SaaS business is the predictability of its revenue and the high margin of incremental growth." — Source: [CIBC Innovation Economy]

- On Growth Sustainability: "Valuation matters, but understanding a company's ability to sustain its compounding growth rate over five years is the ultimate determinant of a successful investment." — Source: [BetaKit]

- On Complexity: "We prefer to invest in software that solves deeply complex, unsexy enterprise problems rather than chasing superficial consumer trends." — Source: [Masters in Business]

- On Pricing Power: "A true leading software product demonstrates its necessity through its ability to maintain or raise prices without increasing churn." — Source: [Dry Powder Podcast]

- On Vertical SaaS: "Software built for specific industries often faces smaller total addressable markets, but makes up for it with significantly lower customer acquisition costs." — Source: [Insight Partners]

- On Hybrid Work: "The acceleration of remote and flexible work fundamentally expanded the baseline requirement for enterprise software." — Source: [SALT Talks]

- On Gross Retention: "Net retention gets the headlines, but high gross retention is the truest indicator that a customer actually needs your software to survive." — Source: [Capital for Good Podcast]

- On the Consumerization of IT: "Enterprise users now expect software that is as intuitive and cleanly designed as the apps they use in their personal lives." — Source: [Upfront Summit]

- On Platform Shifts: "Every major leap in enterprise value has been driven by an underlying platform shift, from on-premise to cloud, and now to applied intelligence." — Source: [Masters in Business]

Part 3: The Scale-Up Phase and Operational Support

- On Insight OnSite: "We realized early that if we were going to help companies navigate the perilous gap between product-market fit and an IPO, we needed dedicated operators inside the firm." — Source: [Dry Powder Podcast]

- On the Growth Chasm: "Getting from zero to $10 million in ARR requires product vision. Getting from $10 million to $100 million requires rigorous operational cadence." — Source: [Bain & Company]

- On Sales Efficiency: "Scaling a sales team is about codifying a repeatable go-to-market motion that works for an average performer." — Source: [Insight Partners]

- On Talent Acquisition: "At the scale-up stage, the most acute bottleneck is almost always executive talent capable of managing through hyper-growth." — Source: [Upfront Summit]

- On Pricing Optimization: "Many founders underprice their software in the early days. Systematic pricing reviews are one of the most immediate levers for value creation." — Source: [Dry Powder Podcast]

- On M&A as a Growth Lever: "Organic growth is essential, but teaching a mid-stage company how to successfully execute and integrate bolt-on acquisitions accelerates market leadership." — Source: [Capital for Good Podcast]

- On Metrics Discipline: "Operating blindly is fatal. A scale-up must transition from looking at lagging financial indicators to managing by leading operational metrics." — Source: [CIBC Innovation Economy]

- On Product Debt: "As you scale, you have to continually pay down the technical and product debt accumulated during the rush to find initial market fit." — Source: [Masters in Business]

- On Board Governance: "The role of the board shifts from product brainstorming in the early days to capital allocation and executive accountability in the scale-up phase." — Source: [This Week in Startups]

- On Culture Scaling: "Maintaining a founder's original culture is impossible; the goal is to intentionally evolve the culture so it supports a much larger, more complex organization." — Source: [Upfront Summit]

Part 4: Market Cycles and Resilience

- On Booms and Busts: "This too shall pass. The euphoria of peak markets is always temporary, but so is the despair of the corrections." — Source: [Private Markets Insights]

- On Navigating Downturns: "Great companies are often forged in constrained environments. Scarcity of capital forces clarity of business model." — Source: [Masters in Business]

- On Over-Capitalization: "Raising too much money at too high a valuation can actually be toxic for a startup, creating misaligned expectations and limiting future exit options." — Source: [This Week in Startups]

- On the Dot-Com Crash: "Surviving the early 2000s taught us to underwrite the actual unit economics of a business, not the narrative of the market." — Source: [Upfront Summit]

- On Valuation Discipline: "We are willing to pay premium prices for premium assets, but we refuse to abandon the fundamental math of how a company will generate cash in the long run." — Source: [Dry Powder Podcast]

- On Cash Management: "In a volatile market, extending runway buys you the optionality to play offense when competitors falter." — Source: [SALT Talks]

- On Cleaning Cap Tables: "Down cycles provide an opportunity to restructure capitalization tables, aligning the incentives of current management with future growth." — Source: [This Week in Startups]

- On Constant Adaptability: "The investment playbooks that worked perfectly five years ago must be constantly rewritten to account for changing interest rates and macro environments." — Source: [Capital for Good Podcast]

- On Market Timing: "We consistently deploy capital across cycles, relying on the secular growth of software to drive long-term returns." — Source: [Bain & Company]

Part 5: The AI Paradigm Shift

- On Ubiquity: "Every company to some degree is an AI company. It doesn't mean that they're .AI in their name, but every board meeting that we go to at Insight, we're talking about AI." — Source: [Private Markets Insights]

- On Business Model Impact: "Even if you're not investing, quote unquote in an AI company, you better be thinking about how AI is gonna affect your business model or how can it improve your business model?" — Source: [Masters in Business]

- On Valuing AI Startups: "If you're paying a high multiple then your conviction needs to be high on the growth rate... we just have to be right enough." — Source: [Insight Partners]

- On Incumbents vs. Upstarts: "We are closely watching whether AI will primarily serve as a sustaining innovation that strengthens existing enterprise software giants, or a disruptive one that creates a new class of leaders." — Source: [ScaleUp:AI 2025]

- On Workflow Automation: "The real enterprise value in AI will come from seamlessly automating complex, multi-step back-office workflows." — Source: [Capital for Good Podcast]

- On Data Defensibility: "In an era of commoditized foundational models, a startup's distinct advantage lies in its proprietary data access and deep workflow integration." — Source: [ScaleUp:AI 2025]

- On AI Hardware: "The infrastructure layer requires massive capital expenditure, which dictates a completely different risk profile compared to investing in the application layer." — Source: [Sidebar Summit]

- On Coding Efficiency: "AI-assisted development tools are accelerating the pace at which software is built, meaning product roadmaps must become drastically more ambitious." — Source: [Masters in Business]

- On AI Governance: "As AI becomes embedded in critical enterprise functions, investors must diligence a company's approach to data privacy, security, and algorithmic bias." — Source: [Council on Foreign Relations]

Part 6: Deal Evaluation and Human Judgment

- On the Human Element: "At the end of the day, for now at least, venture capital is still a human decision business. Determining a good deal still requires human judgement." — Source: [Business Insider]

- On Founder Assessment: "We look for founders who possess a rare combination of unwavering long-term vision and brutal short-term intellectual honesty." — Source: [Upfront Summit]

- On Pattern Recognition: "Decades of reviewing software companies allows you to quickly identify structural flaws in a business model that a spreadsheet might hide." — Source: [Masters in Business]

- On Technical Diligence: "You cannot invest heavily in software without going under the hood. We assess the quality of the codebase just as rigorously as the financial audit." — Source: [CIBC Innovation Economy]

- On Market Size: "A common mistake is statically evaluating a total addressable market. The best founders actively expand their TAM as their product evolves." — Source: [Dry Powder Podcast]

- On Competitive Moats: "Software moats are rarely static. They are built continuously through a high velocity of product iteration and deepening customer entanglement." — Source: [Insight Partners]

- On Reference Checks: "The most valuable insights often come from back-channel conversations with a company's lost customers, rather than the happy ones they provide on a reference list." — Source: [Capital for Good Podcast]

- On Conviction: "If you rely entirely on consensus in a partnership meeting, you will only make safe, average investments. Outsized returns require individual conviction." — Source: [Upfront Summit]

- On Overpaying for Quality: "It is generally a better strategy to slightly overpay for an exceptional business than to get a bargain on a mediocre one." — Source: [BetaKit]

Part 7: The Double Down Investment Strategy

- On Staging Capital: "Our strategy is often to make smaller initial investments to see what is working internally, followed by aggressively doubling down on the clear winners." — Source: [Insight Partners]

- On Asymmetric Upside: "The mechanics of venture require you to maximize your exposure to your portfolio's outliers. You can't be passive when a company starts to break out." — Source: [Masters in Business]

- On Insider Dynamics: "Having a board seat gives you the visibility to preemptively offer growth capital before a company even realizes they need to run a broad fundraising process." — Source: [Dry Powder Podcast]

- On Risk Mitigation: "A double-down strategy actually reduces risk. You are concentrating capital into assets where you have perfect information regarding execution." — Source: [Capital for Good Podcast]

- On Cap Table Influence: "By continually leading subsequent rounds in our best companies, we secure the governance necessary to help steer them toward a successful exit." — Source: [This Week in Startups]

- On the Cost of Missing Out: "The biggest mistakes in our industry aren't the companies that fail; they are the generational companies you invest in early but fail to follow-on with sufficient capital." — Source: [Upfront Summit]

- On Flexible Mandates: "To effectively double down, your fund structure must be flexible enough to write a $10 million check on day one, and a $100 million check three years later." — Source: [Private Markets Insights]

- On Founder Trust: "Founders prefer to take growth capital from insiders they already trust, allowing them to skip the distraction of roadshows." — Source: [CIBC Innovation Economy]

- On Portfolio Concentration: "While we index broadly at the early stage, the vast majority of our deployed capital is highly concentrated in our most successful scale-ups." — Source: [Masters in Business]

Part 8: Global Markets and Civic Engagement

- On Global Ambition: "Software is inherently borderless. A company built in Europe or Asia can scale globally just as effectively as one built in Silicon Valley." — Source: [FII PRIORITY Summit]

- On International Expansion: "We often help our North American portfolio companies navigate the operational complexities of establishing their first European or Asian footprint." — Source: [Insight Partners]

- On Cross-Border M&A: "Identifying global market leaders often involves merging strong regional players to create a singular, unified platform with worldwide reach." — Source: [Dry Powder Podcast]

- On Geopolitical Context: "Investors today cannot operate in a vacuum. Understanding the macroeconomic and geopolitical landscape is critical to predicting regulatory shifts and market access." — Source: [Council on Foreign Relations]

- On Public Service: "Business leaders have a responsibility to lend their operational expertise to civic institutions and government agencies facing modernization challenges." — Source: [Capital for Good Podcast]

- On Inclusive Opportunity: "The technology sector must actively work to widen the funnel of opportunity, ensuring that capital and mentorship reach a broader demographic of founders." — Source: [Robert F. Kennedy Human Rights]

- On U.S. Development Finance: "Strategic capital deployment on a global scale can be a powerful tool for advancing both economic stability and national security interests." — Source: [DFC Board Remarks]

- On Educational Endowment: "Investing in healthcare and educational institutions is vital, as they form the foundational infrastructure that produces the next generation of innovators." — Source: [NYU Langone Health]

- On Long-Term Legacy: "Ultimately, the measure of a career in finance isn't just the aggregate return profile; it's the lasting impact of the companies you helped build and the communities you served." — Source: [Upfront Summit]