Lessons from Django Davidson

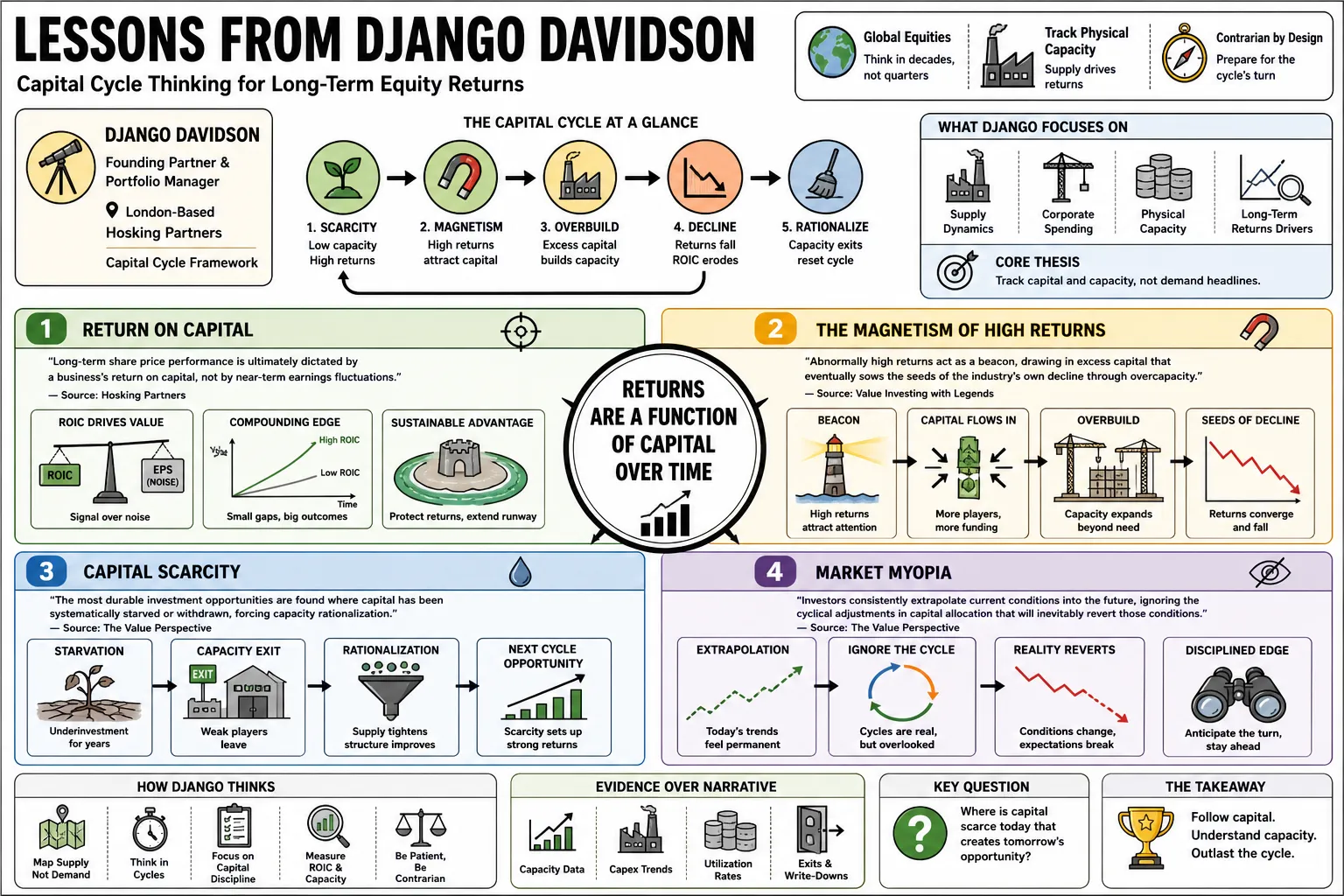

Django Davidson is a founding partner and portfolio manager at London-based Hosking Partners. He applies the capital cycle framework to global equities, focusing on how supply dynamics and corporate spending dictate long-term returns. This collection organizes his contrarian approach to tracking physical capacity instead of chasing demand.

Part 1: The Core of Capital Cycle Theory

- On Return on Capital: "Long-term share price performance is ultimately dictated by a business's return on capital, not by near-term earnings fluctuations." — Source: Hosking Partners

- On the Magnetism of High Returns: "Abnormally high returns act as a beacon, drawing in excess capital that eventually sows the seeds of the industry's own decline through overcapacity." — Source: Value Investing with Legends

- On Capital Scarcity: "The most durable investment opportunities are found where capital has been systematically starved or withdrawn, forcing capacity rationalization." — Source: The Value Perspective

- On Market Myopia: "Investors consistently extrapolate current conditions into the future, ignoring the cyclical adjustments in capital allocation that will inevitably revert those conditions to the mean." — Source: Hosking Partners

- On the Life Cycle of Margins: "Peak margins are often a warning sign of peak competition. When profitability looks its best, new entrants are already funded and building." — Source: Capital Cyclists

- On Consolidation: "The end of a downcycle is marked by consolidation. When the weakest players exit or are absorbed, the survivors inherit pricing power." — Source: Money of Mine

- On the Role of Management: In the PIWORLD summary of his Mavericks conversation, Davidson presents capital-cycle investing as an exercise in judgment about where capital is flowing and where it is being withheld, which makes portfolio management less about forecasting bravado and more about disciplined capital allocation across an industry. — Reference: PIWORLD on capital-cycle investing as disciplined judgment about capital flows

- On Cyclicality: "There is no such thing as a permanently impaired industry, only prices that do not reflect the current reality of the capital cycle." — Source: Hosking Partners

- On Measuring the Cycle: "To understand where an industry sits in the cycle, track the aggregate capital expenditure of all participants, not just the leading company." — Source: The Value Perspective

- On Creative Destruction: "The destruction of capital during a downturn is a necessary precursor for the next bull phase, as it clears out excess capacity and restores discipline." — Source: Value Investing with Legends

Part 2: Supply Over Demand

- On the Certainty of Supply: "Supply is measurable and grounded in physical reality. Demand is often a product of storytelling and hope." — Source: Capital Cyclists

- On Forecasting Errors: "Wall Street spends an inordinate amount of time trying to model demand, an exercise fraught with error. We prefer to count the number of new factories being built." — Source: Value Investing with Legends

- On Asymmetric Information: "The market often prices in demand shocks instantly but is remarkably slow to recognize the long-term impact of supply constraints." — Source: Hosking Partners

- On Capacity Addition: "It takes years to build a new copper mine or semiconductor fab, making future supply highly predictable based on today's capital expenditure budgets." — Source: Money of Mine

- On Demand Mirages: "Strong demand often masks underlying oversupply. If the supply base is growing faster than demand, prices will eventually collapse regardless of how popular the product is." — Source: The Value Perspective

- On Identifying Inflection Points: "The best time to buy is when demand is stagnant but supply is actively shrinking. The turnaround comes when the remaining capacity tightens." — Source: Hosking Partners

- On the Cost of Capital: "A rising cost of capital naturally acts as a constraint on new supply, which paradoxically improves the returns for incumbent businesses." — Source: Value Investing with Legends

- On Lead Times: "Long lead times in capacity expansion create the most pronounced cycles, as price signals take years to translate into actual production." — Source: Capital Cyclists

- On Ignoring the Macro: "By focusing strictly on industry-level supply dynamics, you can largely tune out the noise of macroeconomic predictions." — Source: The Value Perspective

- On Pricing Power: "Pricing power is rarely a permanent structural advantage; it is usually a temporary outcome of tight supply relative to steady demand." — Source: Hosking Partners

Part 3: The Illusion of Forecasting

- On Analyst Estimates: "Consensus earnings estimates are generally just a linear extrapolation of recent history, making them useless for identifying turning points in the capital cycle." — Source: Value Investing with Legends

- On Narrative Fallacies: "We are hardwired to prefer a compelling narrative about the future over a boring analysis of current capacity constraints, which leads to chronic mispricing." — Source: The Value Perspective

- On Terminal Value: "Most of the value in a DCF model resides in the terminal year, a number highly sensitive to inputs that are impossible to predict with any accuracy." — Source: Hosking Partners

- On the Danger of Consensus: "When an entire industry agrees on a long-term demand forecast, the inevitable result is synchronized capital spending and subsequent oversupply." — Source: Capital Cyclists

- On Recognizing Ignorance: In "Where's a copper when you need one," Davidson argues that long-range demand forecasts are loaded with imponderables, so the sounder starting point is to admit what cannot be known and focus on the supply side that can actually be measured. — Reference: Hosking Partners on demand uncertainty and the measurable supply side

- On Historical Blindness: "Investors repeatedly assume that 'this time is different' because a new technology or market paradigm obscures the timeless mechanics of capital flow." — Source: Hosking Partners

- On False Precision: "A complex model projecting cash flows to three decimal places provides a false sense of security while missing the broader structural shifts in the industry." — Source: Value Investing with Legends

- On Extrapolation: "The market's tendency to extrapolate both peak profitability and trough distress is the engine that drives value investing opportunities." — Source: The Value Perspective

- On Adaptability: "Rather than trying to predict the future, structure a portfolio to be resilient across a range of outcomes by focusing on the underlying capital dynamics." — Source: Capital Cyclists

Part 4: Contrarianism and Crowded Trades

- On True Contrarianism: "Being a contrarian isn't just about buying what's out of favor; it's about providing capital when it is scarce and withholding it when it is abundant." — Source: Hosking Partners

- On Hype Cycles: "Whenever capital is effectively free and enthusiasm is unchecked, you are likely looking at the early stages of capital destruction." — Source: Value Investing with Legends

- On Un-crowded Spaces: "The most lucrative investments often reside in boring, stagnant sectors that have been entirely abandoned by growth-chasing capital." — Source: The Value Perspective

- On the Pain of Being Early: "Investing at the bottom of the capital cycle requires enduring a period where the fundamentals look dire and the market tells you you are wrong." — Source: Capital Cyclists

- On Passive Flows: "The rise of index funds exacerbates capital cycles by blindly channeling money into the largest companies, regardless of their return profiles or capital discipline." — Source: Hosking Partners

- On Growth Traps: In "The AI Paradox: Capital Questions," Davidson warns that explosive adoption and a powerful technology theme do not guarantee good equity outcomes when costs, losses, and competitive capital raising are all accelerating at the same time. — Reference: Hosking Partners on AI adoption not guaranteeing attractive investor returns

- On Value Traps: "A true value trap is a cheap company in an industry where capital is still flowing in, preventing any rationalization of supply." — Source: Value Investing with Legends

- On Market Sentiment: In his Mavericks discussion, Davidson argues that capital is over-indexed toward the "Digital Masters of the Universe" while physical supply chains are being starved, creating valuation discrepancies that can favor the assets the market currently finds least exciting. — Reference: PIWORLD on valuation gaps created by neglect of physical supply chains

- On Institutional Imperatives: "Career risk prevents many institutional investors from buying assets at the bottom of the cycle, leaving the opportunity to those willing to appear foolish in the short term." — Source: Hosking Partners

Part 5: The Geography of Capital

- On Geographic Arbitrage: "Capital cycles do not occur uniformly across the globe. Analyzing regional disparities in capital availability can uncover distinct mispricings." — Source: Hosking Partners

- On Emerging Markets: "Emerging economies often experience violent capital cycles due to sudden influxes of foreign investment followed by rapid withdrawals during crises." — Source: The Value Perspective

- On Japan's Corporate Reforms: "The recent shifts in Japanese corporate governance are less about sudden growth and more about the rational deployment and return of long-trapped capital." — Source: Value Investing with Legends

- On State-Directed Capital: "When governments mandate capital expenditure toward specific sectors, it inevitably distorts the cycle, often leading to massive overcapacity." — Source: Capital Cyclists

- On Currency Impacts: "Currency fluctuations can act as a hidden catalyst in the capital cycle, altering the relative competitiveness and investment incentives of local producers." — Source: Hosking Partners

- On De-globalization: "The shift toward localized supply chains is a capital-intensive process that structurally lowers global returns on capital while creating regional bottlenecks." — Source: The Value Perspective

- On Regulatory Moats: In his copper analysis, Davidson notes that supply is heavily shaped by politics, permitting hostility, and state-backed strategic investment, so regulatory regimes can tighten capacity in one geography while encouraging concentration and distortion in another. — Reference: Hosking Partners on permitting, politics, and strategic policy shaping supply

- On U.S. Tech Dominance: "The concentration of global capital in a handful of U.S. technology firms is a symptom of a late-stage cycle, historically a precursor to mean reversion." — Source: Hosking Partners

- On Frontier Markets: "Frontier markets offer a pure expression of capital scarcity, though they come with non-cyclical risks related to property rights and governance." — Source: Capital Cyclists

- On Reshoring: "Bringing manufacturing back to developed markets requires massive capital outlays that will pressure corporate margins for years before yielding efficiencies." — Source: Value Investing with Legends

Part 6: ESG and the Green Energy Transition

- On the Cost of Green Infrastructure: "The energy transition requires an unprecedented deployment of physical capital, a reality that models built on infinite software margins fail to grasp." — Source: Money of Mine

- On ESG Capital Distortions: "By systematically starving traditional energy sectors of capital, ESG mandates have inadvertently created a floor under fossil fuel prices and improved the returns for incumbents." — Source: Hosking Partners

- On the Metals Supercycle: "You cannot electrify the global economy without copper, yet the capital expenditure required to find and extract it has been structurally neglected." — Source: Capital Cyclists

- On Policy-Driven Bubbles: "When subsidies drive investment rather than economic returns, the resulting overcapacity in sectors like solar or wind inevitably crushes equity holders." — Source: The Value Perspective

- On Unintended Consequences: "Divestment campaigns alter the ownership structure of carbon-intensive assets but do nothing to reduce aggregate demand, effectively transferring high returns to private actors." — Source: Value Investing with Legends

- On Transition Bottlenecks: In "Where's a copper when you need one," Davidson argues that the energy transition is constrained by the physical buildout of mines, grids, and materials supply, not just by the appeal of the end-state narrative. — Reference: Hosking Partners on the energy transition being constrained by physical supply buildout

- On Brown-to-Green Valuations: "The market currently misprices the cash generation of legacy 'brown' assets, ignoring their vital role in funding the bridge to a renewable future." — Source: Hosking Partners

- On Capital Misallocation: "We are witnessing a historical misallocation where capital flows freely into speculative climate tech while basic materials necessary for the transition face a funding drought." — Source: Money of Mine

- On the Reality of Physics: "Energy density and material constraints are physical limits that capital cycles must eventually respect, regardless of the prevailing political narrative." — Source: Capital Cyclists

Part 7: AI and Technological Bubbles

- On the AI Arms Race: "The current rush to build AI infrastructure mirrors classic telecom and railway booms: massive, indiscriminate capital expenditure based on unproven, long-term demand." — Source: Value Investing with Legends

- On Semiconductor Cycles: "Despite the narrative of structural growth, the semiconductor industry remains bound by the capital cycle; the massive fab buildouts today guarantee oversupply tomorrow." — Source: Hosking Partners

- On the Beneficiaries of Hype: "During a tech infrastructure boom, the companies selling the 'picks and shovels' capture the initial value, but even they eventually succumb to the resulting overcapacity." — Source: The Value Perspective

- On Software Margins: "The assumption that software businesses are immune to capital cycles ignores the reality that intense venture funding eventually commoditizes niche applications." — Source: Capital Cyclists

- On Disruption Narratives: In "The AI Paradox: Capital Questions," Davidson treats grand technological narratives with skepticism when they are paired with massive fund-raising, heavy capex, and unresolved economics, because story alone does not repeal competition or mean reversion. — Reference: Hosking Partners on skepticism toward AI hype amid capex and weak economics

- On Capital Burn: "When capital is cheap, tech companies prioritize user acquisition over unit economics; when capital tightens, the focus rapidly shifts to cash preservation." — Source: Hosking Partners

- On Data Center Constraints: "The AI expansion will ultimately be bottlenecked by physical constraints—primarily power generation and grid capacity—rather than computing innovation." — Source: Value Investing with Legends

- On the Illusion of Monopoly: In "The AI Paradox: Capital Questions," Davidson says the big open question is whether AI becomes winner-take-most or more like commodity infrastructure, and he notes that easy switching and intense rivalry would push returns down toward marginal cost. — Reference: Hosking Partners on AI monopoly assumptions versus commoditization risk

- On Normalization: "Every technological revolution eventually transitions from an era of speculative capital formation to a mundane period of utility and mean-reverting returns." — Source: Hosking Partners

Part 8: Patience and Long-Term Value

- On Time Arbitrage: "The market's increasing obsession with short-term data points provides a structural advantage to investors willing to underwrite a three-to-five-year capital cycle." — Source: The Value Perspective

- On Enduring Volatility: "You cannot harvest the outsized returns of a cycle turn without the psychological fortitude to look wrong during the final stages of the previous trend." — Source: Value Investing with Legends

- On Activity Bias: "In investing, doing nothing is often the hardest and most profitable decision. The capital cycle takes years to unfold, and constant trading only detracts from returns." — Source: Hosking Partners

- On Evaluating Management: "A management team's true mettle is tested not during a boom, but by their willingness to shrink the capital base and buy back stock during a severe downturn." — Source: Capital Cyclists

- On the Definition of Risk: In his Clockwork CIO conversation, Davidson ties the investment problem back to return on capital and contrarian positioning, implying that real risk comes from committing capital where competition and crowding are already set up to erode future returns. — Reference: Hosking Partners on return on capital, contrarian positioning, and crowding risk

- On Compounding: "The mechanics of compounding require a business to maintain high returns on incremental capital, a feat that becomes mathematically harder as the asset base grows." — Source: Hosking Partners

- On Staying Power: "The structure of your investment vehicle—having stable, aligned clients—is a prerequisite for successfully executing a capital cycle strategy through market drawdowns." — Source: The Value Perspective

- On Recognizing Mistakes: "When the facts of supply change, you must change your mind. Stubbornly holding onto a thesis when new capacity is clearly entering the market is fatal." — Source: Value Investing with Legends

- On the Ultimate Lesson: "The stock market is a mechanism for transferring wealth from those who extrapolate the present to those who understand the cyclical nature of capital." — Source: Hosking Partners