Francisco García Paramés is a Spanish asset manager who built his reputation over twenty-five years at Bestinver, applying strict value principles to European equities, and later founded Cobas Asset Management. He is known for integrating the Austrian Business Cycle Theory with traditional Graham-and-Dodd stock picking to identify companies that can survive and thrive through economic shifts. Reading his insights provides a practical framework for identifying durable businesses, managing personal psychology during market panic, and using economic theory to avoid macro-driven traps.

Part 1: The Foundations of Value

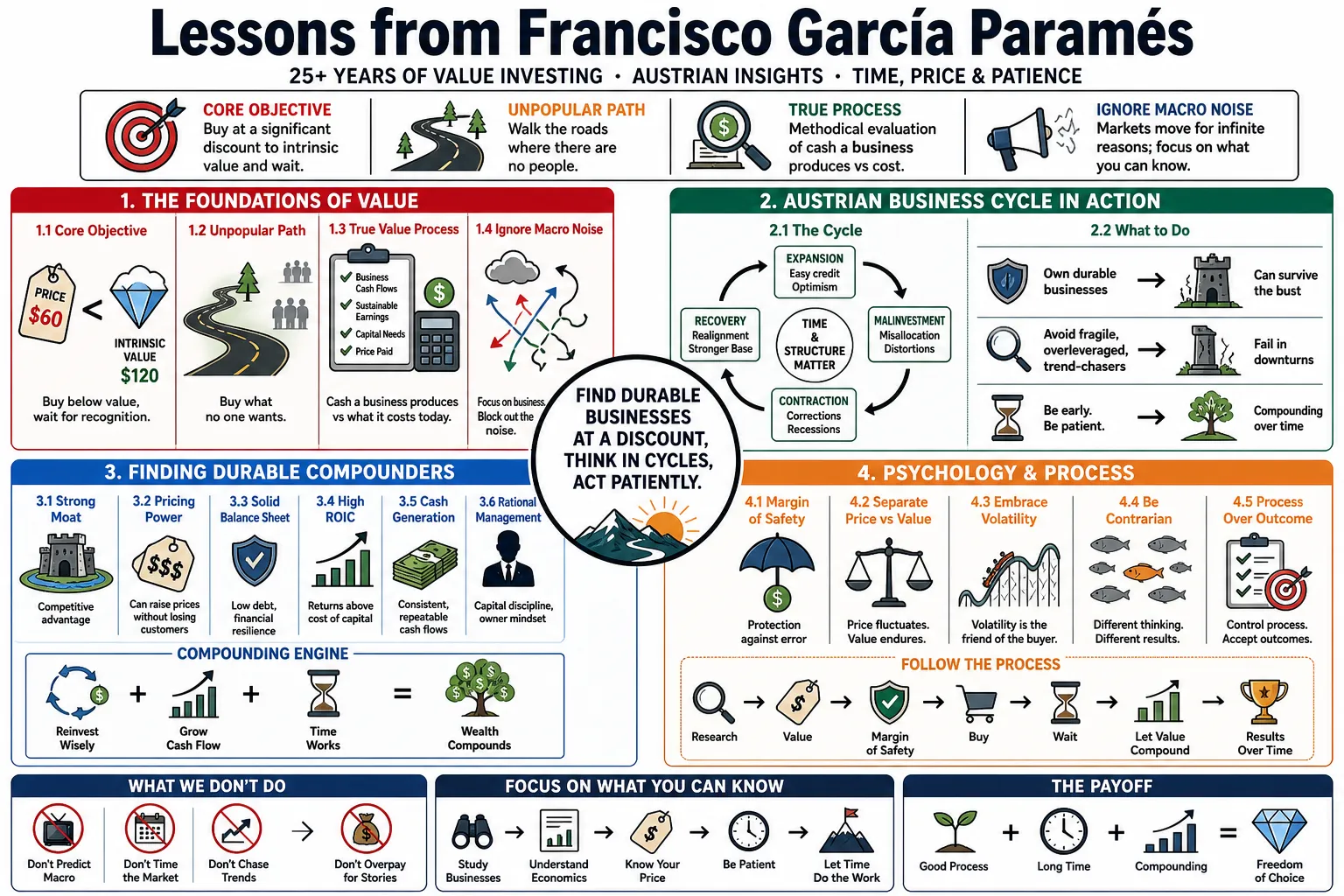

- On the core objective: "Our goal is simple: to buy something for significantly less than its intrinsic value and wait for the market to recognize that value." — Source: [Investing for the Long Term]

- On taking the unpopular path: "Walk the roads where there are no people. Buy what no one wants." — Source: [Economía y Finanzas]

- On true value investing: "Value investing is not a magic formula; it is a methodical process of evaluating what a business produces in cash versus what it costs to acquire it today." — Source: [Cobas Asset Management Letters]

- On ignoring the macro noise: "Financial markets move for infinite reasons... we cannot and should not seek to analyze them in depth, due to the difficulty of establishing appropriate relations between cause and effect." — Source: [Goodreads: Quotes]

- On real assets: "The only way to genuinely protect your savings against the erosion of inflation over decades is to hold stakes in real, productive assets—equities—rather than paper promises." — Source: [Investing for the Long Term]

- On margin of safety: "You do not need precise valuations to know a stock is cheap, much like you do not need to know a man's exact weight to know he is heavy. You just need a margin that absorbs your inevitable errors." — Source: [MOI Global]

- On the futility of market timing: "Attempting to predict the short-term movements of the market is a distraction. Your job is to value businesses, not to forecast the stock exchange." — Source: [Cobas Asset Management Letters]

- On price and value: "The market gives you prices every second, but it only reveals true value over years. The investor's job is to exploit the difference between the two." — Source: [Investing for the Long Term]

- On independent thinking: "You cannot achieve above-average returns if you agree with the consensus. You must have a view that differs from the crowd and, crucially, you must be right." — Source: [Invirtiendo a Largo Plazo Podcast]

Part 2: Navigating Volatility and Risk

- On befriending volatility: "Speculators and volatility are our friends; the more there are, the better results we will get in the long run." — Source: [Economía y Finanzas]

- On illiquidity: "The lack of liquidity is also our ally. Other investors pay too much for that liquidity." — Source: [Economía y Finanzas]

- On defining risk: "Risk is not the daily oscillation of a stock price. True risk is the probability of suffering a permanent loss of your purchasing power." — Source: [Cobas Asset Management Letters]

- On market panics: "Market crashes are the stress tests of a value investor’s conviction. If you know what you own, a 30% drop is an invitation, not a threat." — Source: [Investing for the Long Term]

- On fixed income dangers: "Bonds and cash often provide the illusion of safety while slowly destroying your wealth through monetary debasement." — Source: [MOI Global]

- On dealing with drawdowns: "Temporary underperformance is the admission price to the long-term compounding club. You cannot enjoy the latter without enduring the former." — Source: [Cobas Annual Conference]

- On managing emotions: "An automatic, disciplined investment process is the only reliable shield against the emotional extremes generated by market volatility." — Source: [Investing for the Long Term]

- On business resilience: "A company with net cash and a dominant market position is naturally insulated against the worst macroeconomic shocks." — Source: [Cobas Asset Management Letters]

- On buying cyclical stocks: "Cyclicals offer value when purchased at the bottom of the cycle. The risk is reduced if the company leads its sector and carries minimal debt." — Source: [GuruFocus]

- On surviving the noise: "Turn off the screens. The more closely you monitor the daily price action, the more tempted you will be to interrupt the compounding process." — Source: [Invirtiendo a Largo Plazo Podcast]

Part 3: The Psychology of Markets

- On media attention: "The more a company appears in the press, the further you should keep away from it." — Source: [MoneyWeek]

- On herd behavior: "Humans are biologically wired to find comfort in the crowd. In investing, the crowd is almost always wrong at the most critical turning points." — Source: [Investing for the Long Term]

- On extrapolation: "Investors consistently make the mistake of extrapolating the recent past into the distant future, ignoring the cyclical nature of almost all human enterprises." — Source: [MOI Global]

- On overconfidence: "Beware of precise models predicting distant outcomes. We must accept our limitations in forecasting and demand a wider margin of safety instead." — Source: [Cobas Asset Management Letters]

- On contrarianism: "Being a contrarian just for the sake of it is foolish. You must be contrarian and have the fundamentals firmly on your side." — Source: [Investing for the Long Term]

- On boredom: "Good investing should resemble watching paint dry. If you are seeking entertainment in your portfolio, you will likely pay a steep price for it." — Source: [Invirtiendo a Largo Plazo Podcast]

- On absorbing bad news: "When a sector is universally hated, the negative news is already priced in. That is the exact moment you must start looking for survivors to buy." — Source: [Cobas Annual Conference]

- On managing expectations: "We do not promise high returns every year; we promise a disciplined application of a strategy that has historically rewarded the patient over the long run." — Source: [Cobas Asset Management Letters]

- On narrative fallacies: "Do not fall in love with the story a management team tells. Look strictly at how the business generates cash." — Source: [Investing for the Long Term]

Part 4: The Austrian School and Economic Cycles

- On theoretical frameworks: "The Austrian School of Economics gave me the framework to understand human action and the origins of market cycles, which mathematical models fail to capture." — Source: [MOI Global]

- On central banking: "Investors should steer clear of economies whose growth is based on credit creation under the auspices of low interest rates established by central banks." — Source: [WordPress: Value Quotes]

- On malinvestment: "Artificially low interest rates lead to malinvestment. Capital flows into projects that are not fundamentally viable, creating bubbles that inevitably burst." — Source: [Investing for the Long Term]

- On the role of the entrepreneur: "Austrian economics correctly places the creative entrepreneur at the center of wealth creation, rather than viewing the economy as a static machine to be managed." — Source: [MOI Global]

- On discovering Hayek: "Reading Friedrich Hayek’s 'The Road to Serfdom' was the catalyst that changed how I analyzed the financial world." — Source: [Investing for the Long Term]

- On avoiding bubbles: "By understanding the Austrian theory of credit cycles, we managed to largely sidestep the technology bubble of 2000 and the real estate collapse of 2008." — Source: [Fundación Rafael del Pino]

- On debt: "Excessive leverage is the enemy of survival. A company without debt is the master of its own destiny during an economic contraction." — Source: [Cobas Asset Management Letters]

- On human action: "Economics is not physics. It is the study of human action, which is subjective, dynamic, and resistant to precise mathematical modeling." — Source: [Investing for the Long Term]

- On capital destruction: "When the market finally forces a correction of central bank distortions, the destruction of poorly allocated capital is swift and brutal." — Source: [Invirtiendo a Largo Plazo Podcast]

Part 5: Evaluating Quality and Management

- On corporate longevity: "The older a company is, the more possibilities it has of surviving." — Source: [MoneyWeek]

- On business visibility: "Avoid businesses where you cannot reasonably estimate what the industry landscape will look like in ten years." — Source: [The Corner]

- On return on capital: "Over a decade, a stock's return will inevitably mirror the underlying business's return on invested capital." — Source: [Investing for the Long Term]

- On evolving from 'cigar butts': "Buying mediocre businesses simply because they are cheap is a trap. The passage of time is the enemy of a bad business and the friend of a good one." — Source: [MoneyWeek]

- On competitive moats: "We look for businesses that have built structural advantages—whether through scale, brand, or switching costs—that competitors cannot easily replicate." — Source: [Cobas Asset Management Letters]

- On management integrity: "You cannot make a good deal with a bad person. If management shows a history of enriching themselves at the expense of shareholders, move on." — Source: [Invirtiendo a Largo Plazo Podcast]

- On capital allocation: "A CEO's most critical job is capital allocation. Look at their track record of share repurchases, dividends, and acquisitions to understand if they are creating or destroying value." — Source: [Investing for the Long Term]

- On simplicity: "Complexity in a business model often hides fundamental weaknesses. We prefer simple businesses that we can thoroughly understand." — Source: [MOI Global]

- On structural growth: "While we do not pay premium prices for growth, we recognize that a business capable of reinvesting its cash flow at high rates is intrinsically far more valuable." — Source: [Cobas Annual Conference]

- On tangible assets: "While intangibles matter, buying businesses backed by strong, tangible real assets provides a foundational layer of protection for our capital." — Source: [Investing for the Long Term]

Part 6: Family Ownership and Governance

- On aligned interests: "We heavily favor investing in companies controlled by families, because their wealth and legacy are tied directly to the long-term success of the business." — Source: [MoneyWeek]

- On long-term thinking: "A family owner does not manage the business to beat next quarter's earnings estimates; they manage it to ensure it thrives for the next generation." — Source: [Fundación Rafael del Pino]

- On skin in the game: "Since I cannot sit on the boards of all my investments, I must delegate oversight to owners who have their own substantial capital at risk." — Source: [Investing for the Long Term]

- On avoiding agency problems: "Professional managers often optimize for their own bonuses. Family owners act like true owners, minimizing unnecessary risks." — Source: [Invirtiendo a Largo Plazo Podcast]

- On capital preservation: "Families tend to operate with stronger balance sheets and less debt, naturally protecting the business against severe economic downturns." — Source: [Cobas Asset Management Letters]

- On structural stability: "The stability provided by family ownership allows management to execute strategies that take five to ten years to bear fruit." — Source: [MOI Global]

- On BMW as a model: "Companies like BMW, anchored by families with deep industry knowledge, exemplify the type of steadfast governance we seek to partner with." — Source: [MoneyWeek]

- On identifying stewardship: "Look at how a family owner handled the last recession. If they diluted shareholders or took on massive debt, the family label is meaningless. If they bought back shares, they are stewards." — Source: [Investing for the Long Term]

- On his own background: "Spending 25 years at Bestinver under the Acciona family structure taught me firsthand the massive advantage of operating with patient, aligned capital." — Source: [Hedgeweek]

Part 7: Portfolio Strategy and Concentration

- On concentration: "If you have done the deep research required, it makes no sense to dilute your best ideas by investing in your twentieth or thirtieth choice." — Source: [Cobas Asset Management Letters]

- On sizing positions: "Position sizing should be dictated exclusively by the combination of business quality and the width of the margin of safety, not by index weights." — Source: [Investing for the Long Term]

- On knowing what you hold: "A portfolio of twenty deeply understood businesses carries far less risk than a portfolio of two hundred businesses you know nothing about." — Source: [MOI Global]

- On idle cash: "Invest in shares all your savings not necessary for the near future." — Source: [Economía y Finanzas]

- On sector limits: "We do not enforce arbitrary sector limits, but we naturally gravitate toward areas where human needs are permanent and slow to change." — Source: [Invirtiendo a Largo Plazo Podcast]

- On tracking error: "If your goal is to beat the market, you must guarantee that your portfolio looks nothing like the market. Tracking error is a feature, not a bug." — Source: [Cobas Annual Conference]

- On international diversification: "Good businesses exist everywhere. By expanding our search globally, we simply increase the probability of finding severe mispricings." — Source: [Cobas Asset Management Letters]

- On averaging down: "If the original thesis remains completely intact, a dropping share price is an absolute mandate to buy more, not a reason to panic." — Source: [Investing for the Long Term]

- On when to sell: "We sell when the price reaches our estimate of intrinsic value, when we realize we made a mistake in our analysis, or when we find a significantly better opportunity." — Source: [GuruFocus]

Part 8: Patience and Lifelong Learning

- On the ultimate asset: "Patience is an investor's biggest asset, not intelligence." — Source: [Squarespace: Value Studies]

- On the necessity of waiting: "Investment is a long-term business where patience determines profitability." — Source: [Economía y Finanzas]

- On formal education: "The importance attached to prestigious universities, and even university teaching itself, may be overstated. What you learn at 20 years of age is not as important as lifelong education – preferably when it is self-taught." — Source: [Goodreads: Quotes]

- On finding your path: "Three or four years of being put on the right path by good professors may be useful, but the key thing is to have a spark of interest awoken in us at a particular point in time, which opens up an appealing and limitless path." — Source: [Goodreads: Quotes]

- On reading habits: "The best investors spend the vast majority of their day reading and thinking. Action should be rare." — Source: [Investing for the Long Term]

- On learning from mistakes: "Errors are the tuition you pay to the market. The objective is to keep the tuition costs low and learn the lesson permanently." — Source: [Cobas Annual Conference]

- On intellectual honesty: "If the facts change and your initial analysis proves wrong, you must admit it immediately. Pride destroys capital." — Source: [Invirtiendo a Largo Plazo Podcast]

- On compounding knowledge: "Knowledge in investing compounds exactly like capital. The books you read in your twenties pay dividends in your sixties." — Source: [Investing for the Long Term]

- On client alignment: "We structure our fees to reward investors who stay with us over the long run, because a patient investor base is required to execute a patient strategy." — Source: [Cobas Asset Management Letters]

- On the final test: "The market will eventually reward true value, but it operates on its own schedule. Your only defense against that timeline is unyielding patience." — Source: [MOI Global]