Lessons from Gavin Baker

Gavin Baker is the founder and CIO of Atreides Management, having previously managed the Fidelity OTC Portfolio. He invests across both public and private markets, paying close attention to the physical constraints of technology infrastructure. This collection organizes his core frameworks for evaluating tech cycles, navigating market volatility, and managing portfolio risk.

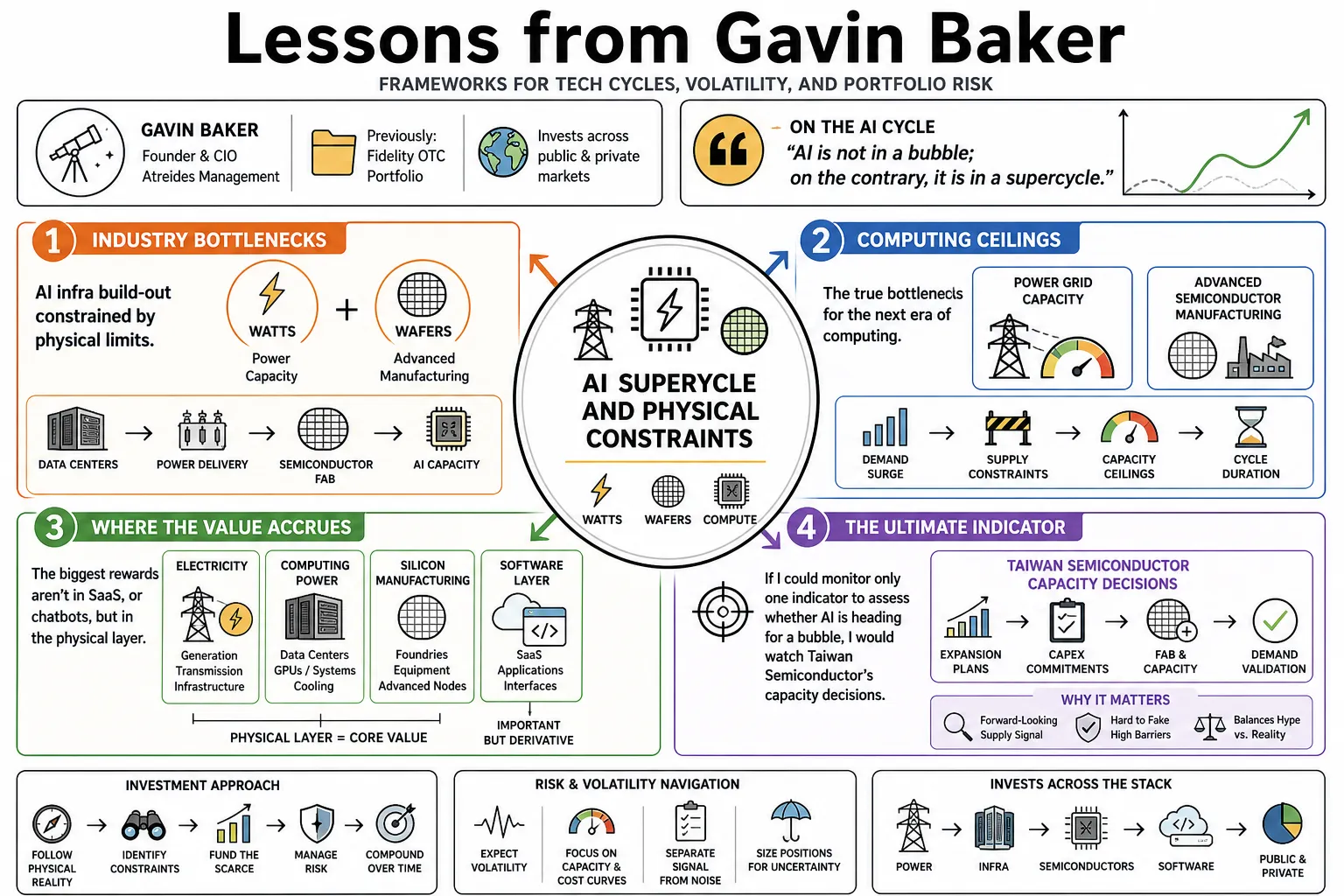

Part 1: The AI Supercycle and Physical Constraints

- On the AI Cycle: "AI is not in a bubble; on the contrary, it is in a supercycle." — Source: [Invest Like the Best]

- On Industry Bottlenecks: The AI infrastructure build-out is constrained primarily by physical limits, specifically "watts and wafers." — Source: [Atreides Management]

- On Computing Ceilings: The true bottlenecks for the next era of computing are power grid capacity and advanced semiconductor manufacturing. — Source: [Invest Like the Best]

- On Where the Value Accrues: "The biggest rewards aren't in SaaS, or chatbots like OpenAI or Anthropic, but in electricity, computing power, and silicon manufacturing." — Source: [Sohn Conference]

- On the Ultimate Indicator: "If I could monitor only one indicator to assess whether AI is heading for a bubble, I would watch Taiwan Semiconductor’s capacity decisions." — Source: [Invest Like the Best]

- On Capital Quality: "This is not an internet bubble because the buyers are mainly the world's smartest and cash-rich companies, and they are not buying computing power with debt leverage." — Source: [Capital Allocators]

- On Infrastructure vs. Applications: The most durable alpha lies in the picks and shovels of the AI economy rather than the application layer. — Source: [Invest Like the Best]

- On Orbital Infrastructure: Looking ahead, orbital data centers may solve terrestrial power and cooling constraints because "in every way, data centers in space… are superior to data centers on Earth." — Source: [Exit Liquidity Podcast]

- On Space and Thermodynamics: Space offers near-perfect conditions for compute density: "You just put a radiator on the dark side of the satellite… it's as close to absolute zero as you can get." — Source: [Exit Liquidity Podcast]

- On Supply-Side Focus: The AI supercycle demands focusing on supply-side constraints rather than demand-side speculation. — Source: [Invest Like the Best]

Part 2: Investing as Truth-Seeking

- On the Core Pursuit: Investing is fundamentally a search for truth that requires intellectual honesty above all else. — Source: [Capital Allocators]

- On People vs. Process: "Any investment organization, no matter how big, there's somewhere between two and 10 people, and if you took those people out and the organization had the exact same process, the results would be very different." — Source: [Capital Allocators]

- On What Drives Performance: Long-term performance is driven more by people, culture, and execution than by rigid adherence to an institutional process. — Source: [Capital Allocators]

- On Organizational Culture: A successful investment culture must actively reward constructive disagreement and debate. — Source: [Capital Allocators]

- On Process Arbitrage: In highly competitive markets, purely process-driven alpha is quickly arbitraged away by competitors. — Source: [Capital Allocators]

- On Updating Priors: The willingness to be wrong and rapidly update your baseline assumptions is essential for sustained success. — Source: [Gavin Baker Medium]

- On Practical Utility: Real insight often comes from recognizing that "context beats IQ" in evaluating new technologies. — Source: [Invest Like the Best]

- On the Danger of Process: Relying heavily on repeatable processes often creates a false sense of security while investment edge requires continuous adaptation. — Source: [Capital Allocators]

- On Team Dynamics: Cultivating a team that challenges consensus is a structural advantage over firms optimizing for harmony. — Source: [Capital Allocators]

Part 3: Psychology and Emotional Discipline

- On Self-Awareness: Successful investing is deeply tied to understanding your own psychological makeup and behavioral biases. — Source: [Gavin Baker Medium]

- On Taking Losses: "Being willing to take a loss is critical to being a great investor." — Source: [Gavin Baker Medium]

- On Handling Drawdowns: When a position is losing significantly, doing nothing is the worst possible course of action; you must either buy more or cut it. — Source: [Gavin Baker Medium]

- On Winning Positions: Drawing from The Art of Execution, the defining trait of the best investors is that they "let their winners run." — Source: [Gavin Baker Medium]

- On Strategy Compatibility: You must find an investment strategy that is compatible with your temperament, otherwise you will abandon it during periods of stress. — Source: [Capital Allocators]

- On Emotional Control: Maintaining emotional discipline when positions move against you is what separates professionals from amateurs. — Source: [Gavin Baker Medium]

- On Active Trading in Panics: Navigating extreme volatility can feel like "being in a knife fight when you're blindfolded and covered in grease." — Source: [Invest Like the Best]

- On True Conviction: The market routinely tests your thesis and true conviction is holding strong when the price action is working aggressively against you. — Source: [Capital Allocators]

- On Managing Fear: Fear and panic are natural responses, but they must be managed systematically rather than reactively. — Source: [Gavin Baker Medium]

- On Secular Growth: "Fear is the mind-killer: secular growth stocks are becoming increasingly attractive" when the market overreacts to short-term macroeconomic noise. — Source: [Gavin Baker Medium]

Part 4: Crossover Investing and Market Dynamics

- On the Crossover Advantage: Investing across public and private markets provides an informational advantage by offering a full-lens view of competitive dynamics. — Source: [Capital Allocators]

- On Ecosystem Tracking: To fully understand the technology ecosystem, you must track how private disruptors are pushing public incumbents. — Source: [Capital Allocators]

- On Direct Competition: Public and private companies increasingly compete directly at every layer of the modern technology stack. — Source: [Atreides Management]

- On Artificial Divisions: The division between public and private equity is artificial because the underlying business reality is continuous. — Source: [Capital Allocators]

- On Forward-Looking Capital: Private market valuations often reveal where the most aggressive capital believes the future of an industry is headed. — Source: [Invest Like the Best]

- On Valuation Discipline: Public market discipline helps inform private market sizing and prevents the over-exuberance common in late-stage venture capital. — Source: [Capital Allocators]

- On Identifying Constraints: Tracking private venture rounds helps map future supply chain constraints before they impact the public markets. — Source: [Atreides Management]

- On Capital Migration: A crossover structure allows capital to migrate to whichever market offers the most asymmetrical risk and reward at any given time. — Source: [Capital Allocators]

- On Information Silos: Information silos between public and private investing teams put both at a structural disadvantage in fast-evolving tech sectors. — Source: [Capital Allocators]

Part 5: Navigating Volatility and Bear Markets

- On Crisis Timing: During severe market panics, it often pays to panic early or double down late. — Source: [Gavin Baker Medium]

- On the Ultimate Metric: "The most important metric today... is the days of solvency at zero revenue." — Source: [Gavin Baker Medium]

- On Zero Revenue Scenarios: "If you have zero revenue forever, then the answer is none, for even if you have a hundred billion dollars in cash and no debt... you will eventually run out of cash." — Source: [Gavin Baker Medium]

- On Cutting Expenses: Management teams that cut expenses early are consistently better positioned for recovery than those that delay the inevitable. — Source: [Gavin Baker Medium]

- On Delayed Cost Cuts: Companies that wait too long to reduce burn rates are eventually forced to cut so deeply that they permanently impair their growth trajectory. — Source: [Gavin Baker Medium]

- On Capital Market Dependency: Bear markets ruthlessly expose companies that rely on continuous capital market access to fund their day-to-day operations. — Source: [Gavin Baker Medium]

- On Changing Metrics: In a severe downturn, the focus shifts entirely from total addressable market entirely to unit economics and sheer survival. — Source: [Gavin Baker Medium]

- On Volatility as Opportunity: High volatility should be treated as a feature of the market that creates opportunity rather than merely a risk to be avoided. — Source: [Invest Like the Best]

- On Market Share: Down cycles clear out marginal competitors and dramatically improve the market share prospects for well-capitalized survivors. — Source: [Gavin Baker Medium]

- On Entry Points: The most attractive entry points in secular growth stories usually occur when macroeconomic fear temporarily obscures fundamental business momentum. — Source: [Gavin Baker Medium]

Part 6: Risk Management and Portfolio Construction

- On Turnover Triggers: Portfolio turnover should correlate closely with market volatility rather than with arbitrary calendar periods or time horizons. — Source: [Capital Allocators]

- On Position Sizing: Position sizing should be driven by conviction-adjusted risk and reward analysis rather than standardized allocation buckets. — Source: [Capital Allocators]

- On the LLCC Framework: The LLCC model dictates that investors must closely monitor Liquidity, Leverage, Concentration, and Crowding. — Source: [Atreides Management]

- On Crowded Trades: Crowded trades become structurally fragile because the fundamental news doesn't need to be bad to cause a selloff, it just needs to be less good than expected. — Source: [Atreides Management]

- On Liquidity: Liquidity constraints are frequently ignored by investors until the exact moment they become the only thing that matters. — Source: [Atreides Management]

- On Leverage: Leverage acts as an accelerant to both returns and mistakes, but its cost during severe drawdowns is often fatal. — Source: [Atreides Management]

- On Concentration Risks: Concentration builds wealth, but it must be paired with extreme intellectual flexibility to avoid catastrophic portfolio losses. — Source: [Capital Allocators]

- On Diversification: Over-diversification is often used by investors as a substitute for deep fundamental understanding of their holdings. — Source: [Capital Allocators]

- On Scenario Planning: A portfolio should be constructed to survive a wide range of outcomes instead of just the single scenario you believe is most likely to occur. — Source: [Capital Allocators]

Part 7: Assessing Valuations and Inefficiencies

- On Pricing Discrepancies: Markets can become cross-sectionally inefficient, where valuation multiples for related companies in the same sector do not logically align. — Source: [Invest Like the Best]

- On Foundational Assets: Core infrastructure assets often appear cheap compared to higher-multiple stocks in derivative areas like power, cooling, or optics. — Source: [Invest Like the Best]

- On Supply Chain Edge: Identifying valuation discrepancies across a complex supply chain is a key driver of consistent outperformance in technology investing. — Source: [Atreides Management]

- On Derivative Mispricing: The broader market often correctly identifies the macroeconomic trend but drastically misprices the derivative beneficiaries. — Source: [Invest Like the Best]

- On AI Utility: For AI technologies, utility will ultimately dictate valuation because the technology needs to become demonstrably useful rather than just technically impressive. — Source: [Invest Like the Best]

- On Premium Multiples: High valuations can be justified if the company is actively solving a fundamental physical bottleneck that is gating an entire industry's growth. — Source: [Atreides Management]

- On Grounded Frameworks: Valuing hardware companies based on metrics like performance per watt provides a more grounded framework than abstract revenue growth multiples. — Source: [Invest Like the Best]

- On Scarcity to Abundance: The transition from scarcity to abundance in any critical technology component will rapidly compress its valuation multiple. — Source: [Invest Like the Best]

- On Maturing Infrastructure: As the AI build-out matures, investment focus must shift toward identifying companies with durable competitive advantages that can survive supply normalization. — Source: [Invest Like the Best]

Part 8: Technology, History, and the Future

- On Applied History: History and science fiction are practical analytical tools for predicting long-term technological shifts. — Source: [Gavin Baker Medium]

- On Infrastructure Cycles: Understanding the history of previous infrastructure booms provides a reliable template for navigating the current AI build-out. — Source: [Invest Like the Best]

- On Science Fiction: Science fiction often accurately predicts the utility and purpose of future technology even if it completely misses the exact developmental timeline. — Source: [Gavin Baker Medium]

- On Changing Paradigms: The transition from software-defined constraints to physics-defined constraints changes the entire analytical paradigm of technology investing. — Source: [Invest Like the Best]

- On Energy Demands: Humanity’s exponentially increasing demand for compute will eventually force a systemic reckoning with the physical limitations of Earth’s energy grid. — Source: [Exit Liquidity Podcast]

- On Physical Reality: Evaluating the next decade of technological progress requires mapping the physical reality of supply chains rather than just software architecture. — Source: [Invest Like the Best]

- On Thermodynamics: We are rapidly entering an era where the fundamental laws of thermodynamics will dictate the pace and direction of software innovation. — Source: [Exit Liquidity Podcast]

- On Bits and Atoms: The most important and lucrative innovations of the next decade will likely occur at the exact intersection of digital bits and physical atoms. — Source: [Invest Like the Best]

- On Economic Value: Studying past technological revolutions reveals that the most profound economic value is usually captured by the companies that lay the tracks rather than those that run the first trains. — Source: [Invest Like the Best]