Lessons from George Selgin

George Selgin, a monetary economist and senior fellow at the Cato Institute, argues that private banks can issue money more stably than central banks. This profile surveys his case against government currency monopolies, his historical research into competitive banking, and his definition of the "productivity norm"—the idea that prices should naturally fall as economic efficiency improves.

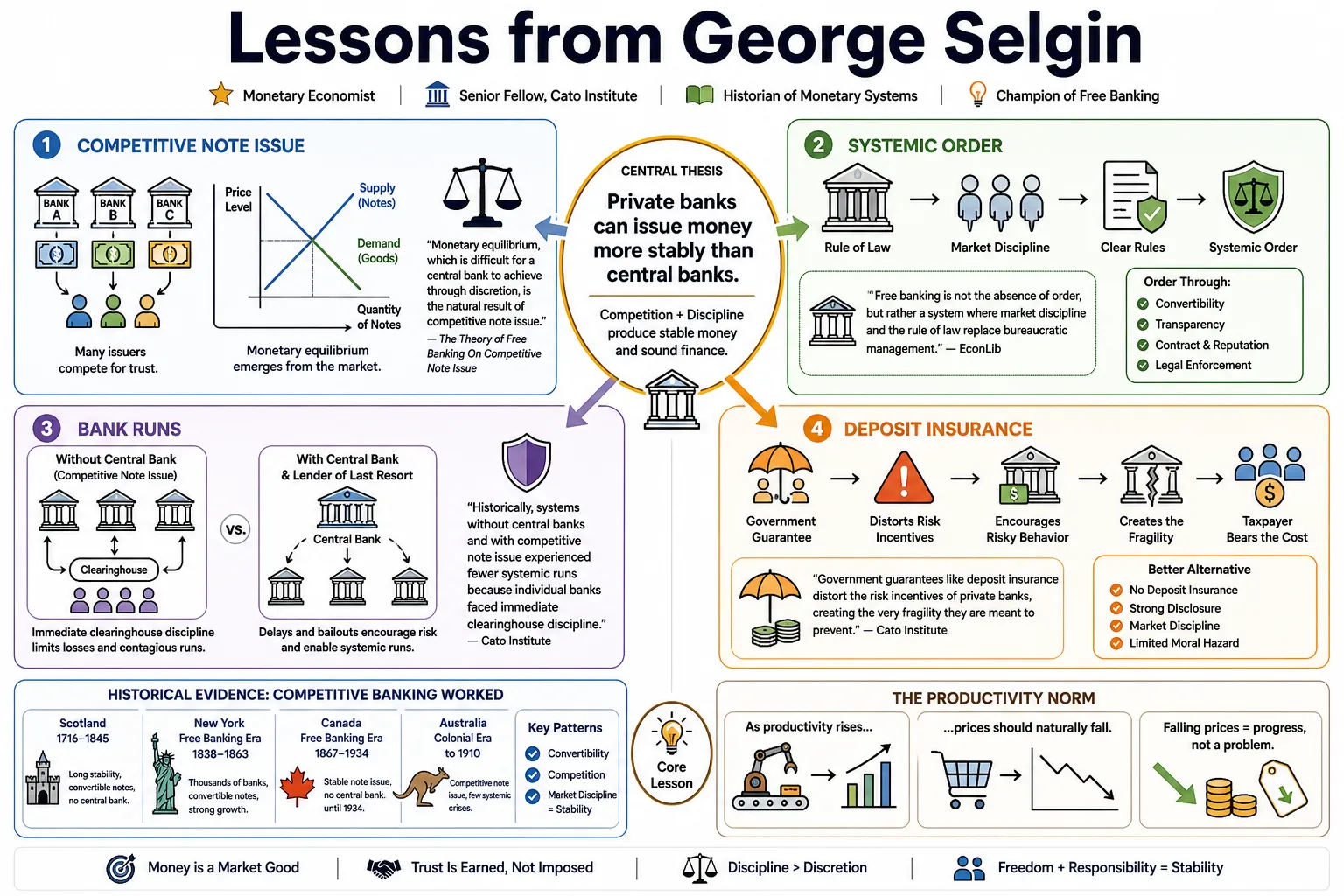

Part 1: The Theory of Free Banking

- On Competitive Note Issue: "Monetary equilibrium, which is difficult for a central bank to achieve through discretion, is the natural result of competitive note issue." — Source: The Theory of Free Banking

- On Systemic Order: "Free banking is not the absence of order, but rather a system where market discipline and the rule of law replace bureaucratic management." — Source: EconLib

- On Bank Runs: "Historically, systems without central banks and with competitive note issue experienced fewer systemic runs because individual banks faced immediate clearinghouse discipline." — Source: Cato Institute

- On Deposit Insurance: "Government guarantees like deposit insurance distort the risk incentives of private banks, creating the very fragility they are supposed to cure." — Source: Alt-M

- On Laissez-Faire Finance: "A true free banking system requires banking to operate without special government regulations, restrictions, or privileges." — Source: Cato at Liberty

- On Central Planning: "It is fundamentally futile to try to maintain monetary equilibrium through central direction." — Source: Review of Austrian Economics

- On Market Feedback: "In a competitive system, clearinghouse mechanisms provide real-time feedback, forcing banks to contract their note issue when they over-expand." — Source: The Theory of Free Banking

- On Money Creation: "Banks do not simply create money out of thin air; they act as intermediaries whose note issuance is strictly constrained by public demand." — Source: Alt-M

- On Historical Evidence: "The Scottish free banking era demonstrates that a financial system can operate efficiently and stably for over a century without a central bank." — Source: Cato Institute

- On Fractional Reserves: "A fractional-reserve free banking system is perfectly capable of matching the supply of bank money to the demand to hold it." — Source: Mises Institute

Part 2: The Productivity Norm and Deflation

- On Benign Deflation: "A fall in prices in response to reduced per-unit costs is essential to the maintenance of equilibrium." — Source: Cato at Liberty

- On the Zero Inflation Target: "Forcing the price level to remain flat at zero percent inflation when productivity is rising requires central banks to inject excess money, which creates economic distortions." — Source: Less Than Zero

- On Money Illusion: "The public often suffers from money illusion, failing to realize that falling prices in a growing economy represent rising real wages." — Source: Less Than Zero

- On Malign Deflation: "Not all deflation is equal; malign deflation caused by a contraction in the money supply harms the economy, whereas benign deflation reflects abundance." — Source: Cato Institute

- On Monetary Policy Goals: "What is needed is a policy that prevents price changes due to changes in the demand for money relative to income without preventing price changes due to changes in productive efficiency." — Source: Alt-M

- On Historical Precedent: "The late 19th century experienced significant economic growth alongside mild deflation, proving that falling prices do not inherently cause depressions." — Source: Macro Musings

- On Central Bank Errors: "By resisting benign deflation, central banks often inadvertently inflate asset bubbles." — Source: Cato Institute

- On Nominal Income: "Allowing prices to fall in response to productivity gains keeps the dollar flow of spending stable, which improves macroeconomic stability." — Source: EconLib

- On the Fear of Falling Prices: "The universal fear of deflation among modern economists is a misapplied lesson from the 1930s Great Depression." — Source: Macro Musings

- On Wage Rigidity: "When prices fall due to cheaper production, nominal wages do not need to be cut for workers to experience an increase in purchasing power." — Source: Less Than Zero

Part 3: Critiques of the Federal Reserve

- On Destabilizing Influence: "Central banks are fundamentally destabilizing. While framed as stabilizers, they often create the artificial booms that lead to severe busts." — Source: Independent Institute

- On the Fed's Record: "The Federal Reserve's history has been marked by significant macroeconomic instability, and its performance has not clearly surpassed that of the preceding National Banking era." — Source: A Century of Failure

- On Lender of Last Resort: "The Fed’s lender of last resort function creates moral hazard, leading to the mispricing of risk and encouraging excessive speculation." — Source: EconLib

- On Interest on Reserves: "Paying interest on excess reserves transformed the Fed from an institution that manages the money supply into one that actively directs credit allocation." — Source: Cato Institute

- On Central Bank Origins: "Central banks gained their dominance through legislation and currency-issuing privileges, not through organic market competition." — Source: FEE

- On Political Pressures: "The structure of the financial system is largely the product of political deal-making rather than economic efficiency." — Source: Cato at Liberty

- On the Pre-Fed Era: "The financial panics of the late 19th century were not failures of free markets, but failures caused by regulations that prevented banks from issuing notes against general assets." — Source: Alt-M

- On Federal Reserve Independence: "True central bank independence is a myth; the Fed is always subject to fiscal pressures and political realities." — Source: Macro Musings

- On Monetary Medicine: "Those who look upon monetary expansion as a way to eradicate almost all unemployment fail to appreciate that persistent unemployment is a non-monetary condition." — Source: Less Than Zero

- On the Floor System: "Operating a floor system where the central bank pays banks not to lend effectively severs the link between the monetary base and broad money creation." — Source: The Menace of Fiscal QE

Part 4: The Menace of Fiscal QE and Monetary Interventions

- On Fiscal QE: "Quantitative easing often blurs the line between monetary and fiscal policy, allowing the central bank to fund government debt indirectly." — Source: The Menace of Fiscal QE

- On Credit Allocation: "When the central bank buys mortgage-backed securities, it ceases to be a neutral manager of money and becomes a political allocator of capital." — Source: Cato Institute

- On Balance Sheet Size: "A permanently large central bank balance sheet reduces interbank lending and increases the banking sector's reliance on government interventions." — Source: Alt-M

- On Market Distortion: "Vast asset purchase programs suppress natural interest rates and penalize savers while rewarding leveraged speculation." — Source: Macro Musings

- On Unconventional Tools: "Tools designed as emergency measures frequently become permanent features of the monetary framework, expanding state power." — Source: Cato at Liberty

- On Central Bank Footprints: "A heavier central bank footprint in financial markets crowds out private liquidity provision." — Source: The Menace of Fiscal QE

- On Treasury Dominance: "During crises, monetary authorities routinely capitulate to the financing needs of the Treasury." — Source: Alt-M

- On Financial Repression: "Keeping interest rates artificially low over long periods acts as a hidden tax that liquidates real government debt burdens." — Source: Cato Institute

- On Normalization: "Once a central bank expands its balance sheet and takes on fiscal roles, returning to a lean, traditional operational framework proves nearly impossible politically." — Source: Macro Musings

Part 5: Private Coinage and "Good Money"

- On State Failure: "During the British Industrial Revolution, the Royal Mint entirely failed to provide sufficient small-denomination coinage to meet the needs of a growing economy." — Source: Good Money

- On Private Solutions: "To solve the severe shortage of small change, private manufacturers stepped in to produce custom-made tradesman’s tokens that became widely accepted." — Source: Good Money

- On Quality Control: "The privately minted copper tokens were often of higher quality and harder to counterfeit than the official royal coinage." — Source: IEA

- On Market Trust: "Because they needed to maintain public trust to circulate, private minters voluntarily backed their tokens and ensured reliable redemption." — Source: Mises Institute

- On State Monopoly: "The history of British private coinage challenges the unquestioned assumption that currency production must inherently be a state monopoly." — Source: Cato Institute

- On Technological Innovation: "Entrepreneurs like Matthew Boulton applied steam power to minting, drastically lowering costs and improving the security of physical money." — Source: Good Money

- On Government Suppression: "The private coinage industry flourished until the British Crown forcibly reasserted its monopoly and outlawed private tokens to protect its own seigniorage." — Source: Alt-M

- On Historical Blindspots: "Mainstream economic history often ignores how effectively the private sector provided stable money before governments legislated them out of existence." — Source: EconLib

- On Modern Parallels: "The success of private tokens in the 18th century offers direct historical precedent for modern alternatives like digital currencies and electronic payments." — Source: IEA

Part 6: The New Deal and Economic Recovery

- On the 1933 Baseline: "Before Roosevelt's inauguration, the US economy resembled a body slowly bleeding out, its organs failing one by one." — Source: False Dawn

- On Measuring Success: "If one wants to properly gauge the progress of economic recovery, one must ask how close the economy is to making full use of its available resources, including its labor force." — Source: False Dawn

- On the Lack of Strategy: "The New Deal was not a plan, not even an agreement, and it was certainly not a plot, as was later charged." — Source: Law & Liberty

- On Regime Uncertainty: "Constant shifts in tax, labor, and monetary policies created a paralyzing uncertainty that prevented businesses from making long-term investments." — Source: False Dawn

- On Capital Investment: "Because of unpredictable regulations, managers were unwilling to embark upon plans for major improvements, confining purchases mainly to basic replacements." — Source: Claremont Review of Books

- On Leaving Gold: "The sudden departure from the gold standard was not a deeply considered strategy by the administration's financial experts, but a unilateral decision by the President." — Source: Cambridge University Press

- On Persistent Stagnation: "Even by 1940, despite years of federal intervention, the prosperity which had vanished in 1929 seemed as unattainable as a rainbow." — Source: Cato Institute

- On Prolonging the Depression: "Many New Deal interventions, particularly those designed to artificially raise prices and wages, actively hindered the natural recovery process." — Source: Alt-M

- On True Recovery: "The Depression finally ended when the government was no longer at war with business, rather than simply because of wartime spending." — Source: Financial Post

Part 7: Central Bank Digital Currencies (CBDCs)

- On Digital Bank Runs: "Allowing the public to hold accounts directly with the central bank could make financial crises more severe by facilitating instant digital bank runs." — Source: Cato Institute

- On Retail CBDCs: "Central bank provision of retail digital money threatens to completely disintermediate the private banking sector." — Source: Alt-M

- On Federal Reserve Accounts: "If anyone can place deposits in a Fed Master Account, the central bank’s footprint on credit allocation will expand dramatically." — Source: Cato at Liberty

- On Intermediated Models: "Whereas the synthetic CBDC plan allows for numerous retail digital currencies, the Fed's intermediated CBDC plan provides for a single digital currency only." — Source: The Daily Economy

- On Privacy Risks: "A retail CBDC would grant the central bank unprecedented visibility into and control over individual financial transactions." — Source: Cato Institute

- On Narrow Stablecoins: "Instead of having the Fed enter the retail CBDC business, it would be better to offer wholesale accounts and services to a broad set of retail digital currency or stablecoin providers." — Source: Cato Institute

- On Fostering Innovation: "Congress should prevent the Federal Reserve from issuing a retail CBDC to ensure that innovation remains driven by the competitive private sector." — Source: Alt-M

- On Historical Instability: "Central bank monopolization of paper money has been an important historical cause of financial instability; monopolizing digital money will repeat this error." — Source: Cato Institute

- On Regulatory Double Standards: "Governments often advocate for CBDCs while simultaneously pushing hostile regulations against private stablecoins that provide the same utility." — Source: Macro Musings

Part 8: Bitcoin and Cryptocurrency

- On Synthetic Commodity Money: "Bitcoin represents a fascinating realization of synthetic commodity money, existing independently of any central monetary authority." — Source: Castle Island Ventures

- On Medium of Exchange: "Despite its innovations, Bitcoin is poorly suited to function as a nation's primary medium of exchange due to its inelastic supply." — Source: Traders Union

- On the Digital Gold Fallacy: "The narrative that Bitcoin serves as a superior digital gold or strategic reserve asset fundamentally misunderstands how reserve assets function within a fiat system." — Source: Policy Commons

- On Elasticity of Supply: In Bitcoin: Problems and Prospects, Selgin argues that Bitcoin’s predetermined supply makes no allowance for changes in real demand. As issuance approaches its 21 million limit while transactions demand keeps growing, a Bitcoin standard would tend toward deflation, with sharper bouts when money demand rises cyclically; a better cybercurrency would need supply elasticity tied to transactions volume. — Reference: Selgin paper, Bitcoin: Problems and Prospects, on Bitcoin supply inelasticity and elastic cybercurrency design

- On Strategic Reserves: "The notion of establishing a strategic Bitcoin reserve for the U.S. government is economically incoherent and ignores the mechanics of modern sovereign debt." — Source: Cato Institute

- On El Salvador’s Mandate: "While Bitcoin legislation in El Salvador promoted financial choice, government mandates forcing merchants to accept it contradict the principles of monetary freedom." — Source: Alt-M

- On the Definition of Money: "Money is better understood as a spectrum of liquidity rather than a strict binary concept, which complicates Bitcoin's classification as pure money." — Source: Castle Island Ventures

- On Free Market Potential: "Cryptocurrencies demonstrate that the private sector is fully capable of engineering sophisticated payment and settlement networks without state direction." — Source: Medium

- On Long-term Viability: "For a cryptocurrency to succeed as a widespread currency, it must solve the problem of macroeconomic stability, which requires elasticity rather than absolute scarcity." — Source: Macro Musings