Lessons from Ian Charles

Before co-founding Arctos Partners, Ian Charles worked in the private equity secondaries market. He helped turn sports franchise ownership into an institutional asset class and brought data science to alternative assets. This compilation details his approach to pricing illiquid assets and modeling the economics of live entertainment.

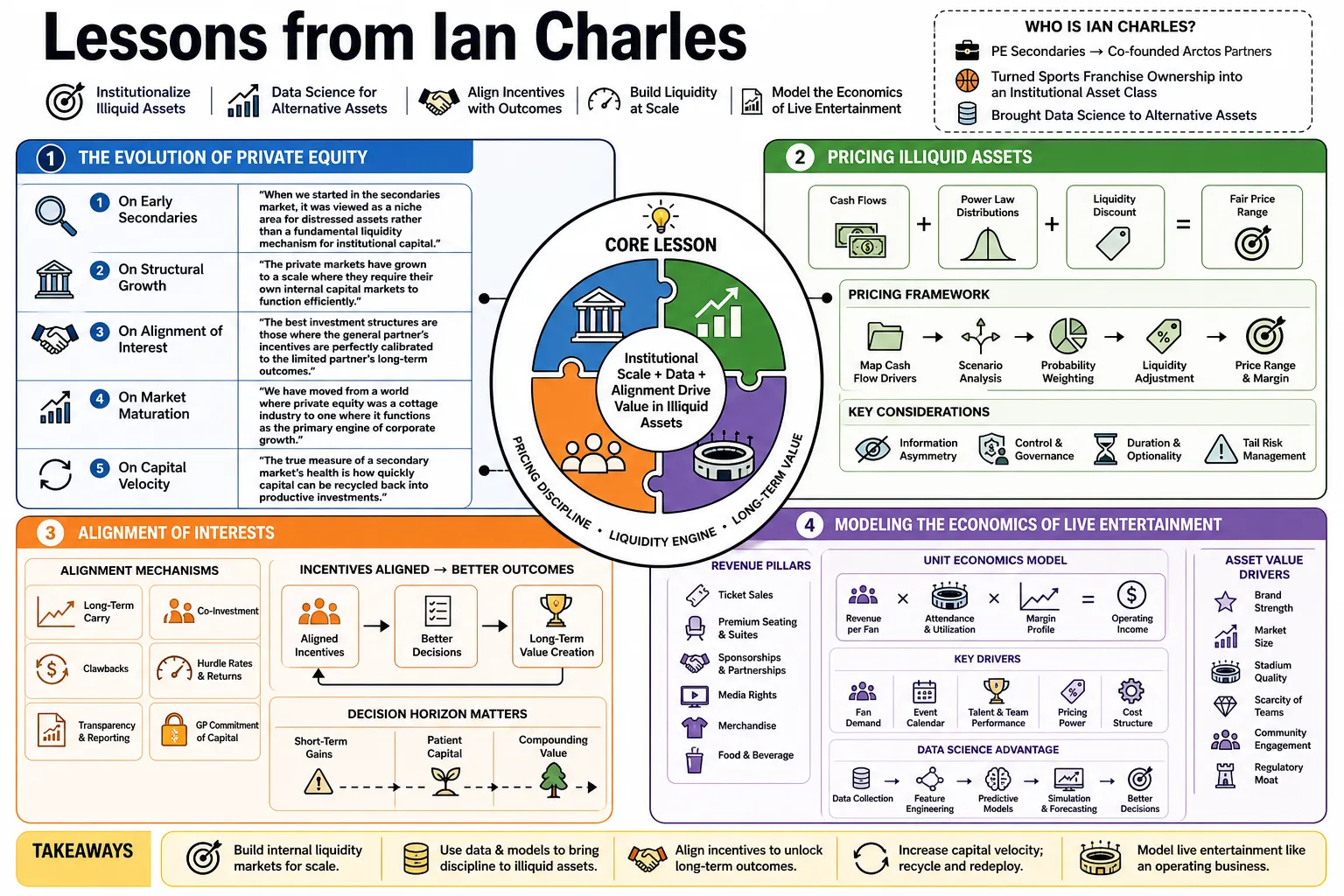

Part 1: The Evolution of Private Equity

- On early secondaries: "When we started in the secondaries market, it was viewed as a niche area for distressed assets rather than a fundamental liquidity mechanism for institutional capital." — Source: [PitchBook]

- On structural growth: "The private markets have grown to a scale where they require their own internal capital markets to function efficiently." — Source: [Bloomberg Markets]

- On alignment of interest: "The best investment structures are those where the general partner's incentives are perfectly calibrated to the limited partner's long-term outcomes." — Source: [The Money Maze Podcast]

- On market maturation: "We have moved from a world where private equity was a cottage industry to one where it functions as the primary engine of corporate growth." — Source: [PEI Events]

- On capital velocity: "The true measure of a secondary market's health is how quickly and accurately it can price complex, illiquid assets." — Source: [Cogent Partners Archives]

- On institutional specialization: "Firms can no longer be generalists in everything; the future belongs to deep sector specialists who bring operational distinctiveness." — Source: [Arctos Partners Insights]

- On liquidity solutions: "Providing liquidity to founders and early investors without forcing a premature sale unlocks long-term value creation." — Source: [The Holy Grail of Investing]

- On alternative asset classes: "An asset class only becomes institutional when you have enough historical data to underwrite the downside risk." — Source: [Wharton Alumni Network]

- On the role of data in PE: "Historically, private equity relied on relationship networks. Today, if you omit data science from your sourcing and underwriting, you fall behind." — Source: [Crain Currency]

Part 2: Sports Franchises as an Asset Class

- On scarcity: "There is a mathematically hard cap on the number of premium sports franchises in the world, creating a permanent supply-demand imbalance." — Source: [The Holy Grail of Investing]

- On media rights: "Live sports are the last remaining form of appointment viewing, which makes their media rights uniquely valuable in a fragmented ecosystem." — Source: [Bloomberg Markets]

- On correlation to broad markets: "Sports franchises offer a rare combination of high historical returns and low correlation to traditional equities." — Source: [The Money Maze Podcast]

- On franchise valuation: "You are buying a localized monopoly with deep, multi-generational consumer loyalty." — Source: [Arctos Partners Insights]

- On institutional capital entering sports: "Leagues opening up to private equity is fundamentally about bringing institutional capital to team operations, rather than simply providing an exit for founders." — Source: [Sports Business Journal]

- On downside protection: "The structural rules of major leagues, like salary caps and revenue sharing, are designed specifically to protect the viability of the franchises." — Source: [PitchBook]

- On minority stakes: "Taking a passive, minority stake allows us to partner with great owners without disrupting the culture they have built." — Source: [The Holy Grail of Investing]

- On intellectual property: "A sports team is fundamentally an intellectual property business wrapped in a live entertainment product." — Source: [Crain Currency]

- On international expansion: "The next frontier for major leagues is fully monetizing their global fanbases, which are currently under-indexed compared to domestic fans." — Source: [Bloomberg Markets]

- On fan engagement: "The connection a fan has with their team is more resilient than brand loyalty in almost any other consumer sector." — Source: [The Money Maze Podcast]

Part 3: The Dynamics of the Secondaries Market

- On pricing illiquidity: "The secondary market exists because the timeline of an investment fund rarely matches the timeline of its underlying investors." — Source: [Landmark Partners Archives]

- On portfolio management: "Active management of private market portfolios requires the ability to sell just as efficiently as you buy." — Source: [PEI Events]

- On market cycles: "Secondary volumes are highly pro-cyclical, but the best secondary returns often come during periods of capital dislocation." — Source: [PitchBook]

- On GP-led secondaries: "General Partner-led transactions have transformed the market from a tool for distressed investors into a strategic option for extending hold periods on winning assets." — Source: [The Holy Grail of Investing]

- On information asymmetry: "In the early days of secondaries, returns were driven by information asymmetry. Today, they are driven by analytical execution." — Source: [Cogent Partners Archives]

- On complexity premiums: "The harder a portfolio is to value, the greater the opportunity for a buyer with the right analytical tools." — Source: [Wharton Alumni Network]

- On capital velocity: "Many institutions hold onto underperforming funds because they fear realizing a loss, but capital velocity is usually more important than preserving a paper mark." — Source: [Crain Currency]

- On structural innovation: "We invent new transaction structures to accommodate the unique tax and regulatory needs of global sellers." — Source: [The Money Maze Podcast]

- On market scale: "What was once a fraction of a percent of private market activity is now a fundamental pillar of alternative asset liquidity." — Source: [Bloomberg Markets]

- On underwriting standards: "You cannot rely on the original manager's underwriting; a secondary buyer must re-underwrite the asset from today's entry point." — Source: [Arctos Partners Insights]

Part 4: Data Science and Institutionalizing Ownership

- On quantitative analysis: "You cannot bring institutional capital to a new asset class without first building the data infrastructure to model its behavior." — Source: [The Money Maze Podcast]

- On evaluating front offices: "We look at sports franchises the way we look at corporate management teams: we evaluate their capital allocation and operational efficiency." — Source: [Sports Business Journal]

- On predictive modeling: "Using historical revenue curves allows us to isolate the impact of on-field performance from underlying macro trends." — Source: [The Holy Grail of Investing]

- On bespoke data sets: "The advantage of being early to a market is that you have to build your own datasets, which then becomes a formidable barrier to entry." — Source: [Arctos Partners Insights]

- On defining beta: "In sports investing, the beta is the overall growth of the league and media rights, while the alpha is the specific operational improvements of the team." — Source: [Bloomberg Markets]

- On real estate integration: "Sophisticated owners use their sports venue as an anchor tenant for a broader, year-round real estate ecosystem." — Source: [PitchBook]

- On consumer analytics: "Teams have decades of ticketing and merchandise data, but very few have optimized how to monetize that fan graph." — Source: [Crain Currency]

- On risk quantification: "Institutional investors require a clear understanding of what happens to cash flows in the worst-case scenarios, like a labor strike or a pandemic." — Source: [The Money Maze Podcast]

- On operational alpha: "Capital is only one part of the equation; the actual advantage comes from providing analytics to help owners optimize pricing and sponsorships." — Source: [Arctos Partners Insights]

- On tech integration: "The integration of technology into the fan experience is shifting teams from being event businesses to media platforms." — Source: [The Holy Grail of Investing]

Part 5: Navigating Structural Inefficiencies

- On finding edges: "Alpha is usually found in the structural gaps between traditional investment silos." — Source: [Wharton Alumni Network]

- On capital constraints: "When an asset class has high barriers to entry and limited capital providers, the terms of investment tilt heavily toward the provider." — Source: [PitchBook]

- On regulatory moats: "League rules regarding ownership limits act as a structural moat, preventing speculative capital from inflating valuations." — Source: [Sports Business Journal]

- On liquidity discounts: "Investors consistently over-penalize illiquidity, which creates a permanent pricing advantage for long-term capital." — Source: [The Money Maze Podcast]

- On market friction: "Every time an asset class requires specialized legal and tax structuring, it reduces competition and increases potential returns." — Source: [Bloomberg Markets]

- On owner demographics: "We are seeing a generational wealth transfer in sports ownership, which necessitates new forms of structured capital." — Source: [The Holy Grail of Investing]

- On syndicated capital: "The traditional model of passing a hat to dozens of wealthy individuals to buy a team is breaking down due to the sheer cost of these assets." — Source: [Crain Currency]

- On valuation lag: "Private markets do not price in real-time, meaning those with the best forward-looking data can consistently acquire assets below intrinsic value." — Source: [Arctos Partners Insights]

- On structural subordination: "Understanding where you sit in the capital stack is more important than understanding the terminal value of the asset." — Source: [PEI Events]

Part 6: Risk Management and Market Fundamentals

- On asymmetric risk: "We construct portfolios where the downside is strictly capped by hard assets while the upside captures broad cultural trends." — Source: [The Money Maze Podcast]

- On diversification: "Owning a single team carries operational risk; owning a basket of minority stakes across leagues transforms that into systemic league growth." — Source: [The Holy Grail of Investing]

- On debt versus equity: "In highly predictable revenue models, carefully structured equity can offer downside protection similar to debt, but with uncapped upside." — Source: [Arctos Partners Insights]

- On macro insulation: "Consumer spending on live sports and entertainment has historically been deeply insulated from typical recessionary pressures." — Source: [Bloomberg Markets]

- On labor relations: "A sports league is fundamentally a partnership between capital and labor. Understanding collective bargaining is essential to underwriting the asset." — Source: [PitchBook]

- On governance: "Being a minority investor requires ironclad governance rights to protect capital without interfering in the daily pursuit of winning." — Source: [Sports Business Journal]

- On underwriting assumptions: "If your model requires the team to win championships to hit its return hurdle, it is a flawed investment." — Source: [Crain Currency]

- On cash flow visibility: "The long-term nature of media and sponsorship contracts gives sports franchises a revenue visibility that most software companies would envy." — Source: [The Holy Grail of Investing]

- On aligning incentives: "The best partnerships are formed when the financial goals of the investor and the competitive goals of the operator are mutually reinforcing." — Source: [Wharton Alumni Network]

Part 7: Building and Scaling Investment Firms

- On institutional culture: "A firm's culture is defined by how it handles the investments that fail to meet their initial projections." — Source: [Arctos Partners Insights]

- On pioneering markets: "When you build a new category, half your time is spent educating the market and the other half is spent executing the strategy." — Source: [The Money Maze Podcast]

- On team construction: "You need a mix of traditional financial engineers and people who deeply understand the operational nuances of the specific asset." — Source: [PitchBook]

- On specialized expertise: "Generalist platforms struggle to compete with specialists who focus entirely on a single vertical." — Source: [Bloomberg Markets]

- On LP relationships: "Institutional investors look for partners who offer co-investment and specific knowledge transfer, rather than a generic fund vehicle." — Source: [PEI Events]

- On adaptability: "The initial thesis rarely survives contact with the market entirely intact; success comes from the speed at which you iterate." — Source: [The Holy Grail of Investing]

- On process engineering: "Investing at scale requires turning bespoke deal-making into a repeatable, institutional process." — Source: [Cogent Partners Archives]

- On brand equity in finance: "In private markets, your reputation as a fair and constructive partner is your ultimate proprietary sourcing channel." — Source: [Crain Currency]

- On long-term vision: "We are building infrastructure for the next fifty years of alternative capital, rather than optimizing for a single fund cycle." — Source: [Arctos Partners Insights]

Part 8: The Future of Media and Live Entertainment

- On content scarcity: "As the broader media market fractures into specialized niches, unified, live, unscripted drama becomes highly valuable content." — Source: [The Holy Grail of Investing]

- On streaming economics: "Tech platforms view sports rights primarily as customer acquisition engines for their broader ecosystems." — Source: [Bloomberg Markets]

- On global convergence: "The barriers between domestic and international leagues are eroding, creating a truly global marketplace for fan attention." — Source: [Sports Business Journal]

- On venue optimization: "The stadium of the future operates as a continuously engaged hub for a surrounding community, rather than a place you visit for three hours." — Source: [The Money Maze Podcast]

- On interactive consumption: "Future fan bases will expect to interact with broadcasts through data overlays and real-time social features." — Source: [Arctos Partners Insights]

- On direct-to-consumer models: "The transition from bundled cable to direct-to-consumer requires teams to know exactly who their fans are and what they are willing to pay." — Source: [PitchBook]

- On women's sports: "We are in the early stages of a secular growth cycle in the valuation and commercialization of women's leagues." — Source: [Crain Currency]

- On adjacent revenue streams: "The core game is simply the engine; the actual margin expansion comes from adjacent businesses like real estate and digital media." — Source: [The Holy Grail of Investing]

- On enduring relevance: "Trends in media change rapidly, but the tribal affiliation of sports has survived essentially unchanged for centuries." — Source: [Wharton Alumni Network]