Lessons from Ivar Kreuger

Ivar Kreuger built an early 20th-century empire by lending money to cash-strapped European governments in exchange for national match monopolies. When his operation collapsed during the Great Depression, the wreckage revealed massive accounting fraud and forged bonds that wiped out investors globally. The fallout from his deception directly prompted the creation of modern securities laws, forcing public companies to report honest financials.

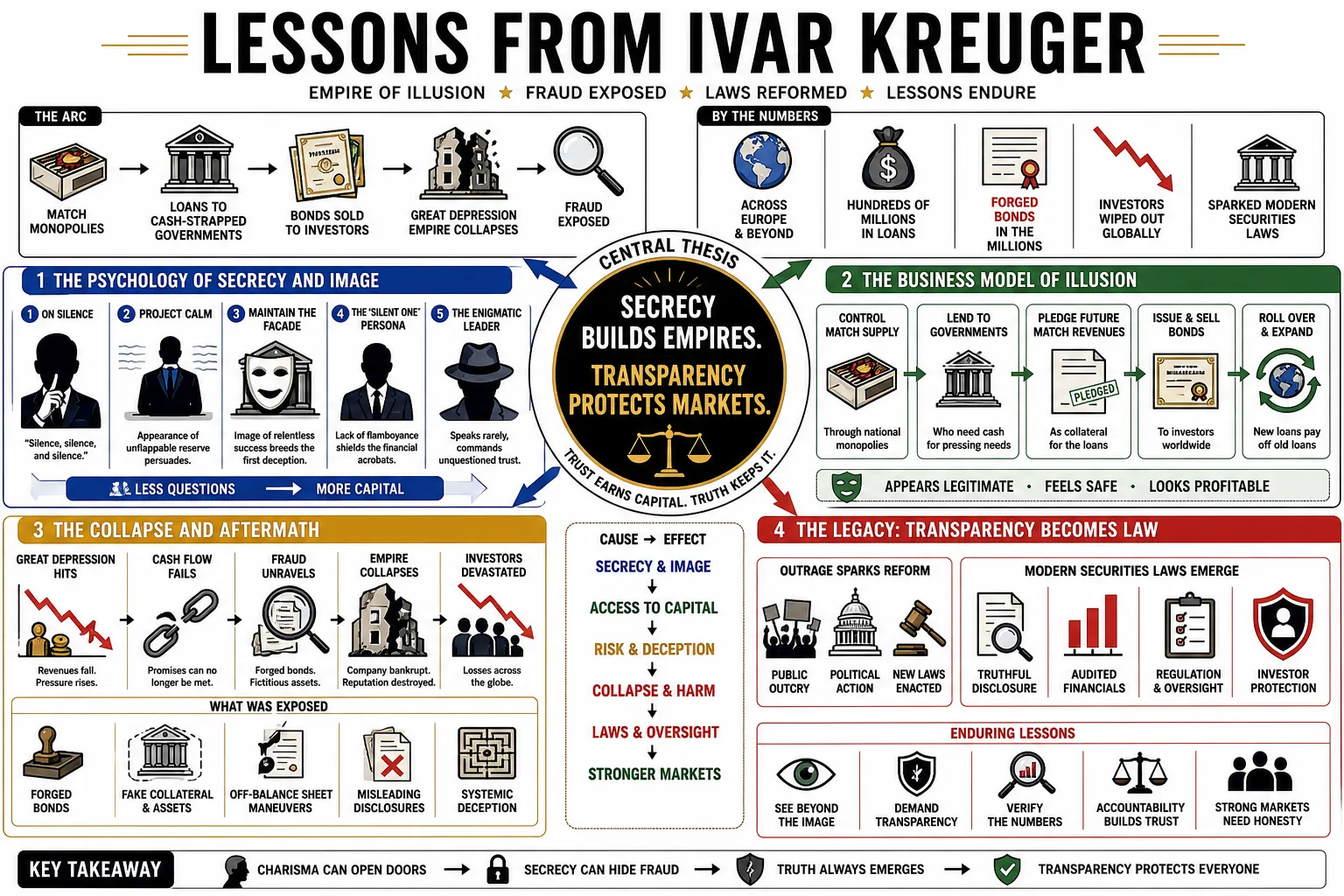

Part 1: The Psychology of Secrecy and Image

- On silence: "Silence, silence, and silence." — Source: [Wikiquote: Ivar Kreuger]

- On the projection of calm: "The appearance of unflappable reserve is a tool of persuasion; investors rarely question an executive who never seems panicked." — Source: [The Match King by Frank Partnoy]

- On maintaining the facade: "Once a business relies on a curated image of relentless success to secure funding, the pressure to maintain that image often breeds the first acts of deception." — Source: [Wikipedia: Ivar Kreuger]

- On the 'Silent One' persona: "A deliberate lack of personal flamboyance can act as a shield, making financial acrobatics seem like the predictable work of a serious engineer." — Source: [The Economist: The Match King]

- On the power of the enigmatic leader: "When a founder speaks rarely and only in measured tones, markets tend to project their own assumptions of competence onto the silence." — Source: [Harvard Business School: Ivar Kreuger Case]

- On cultivating mystique: "True financial power often lies in being perceived as possessing knowledge or systems too intricate for the layman to grasp." — Source: [The Match King by Frank Partnoy]

- On isolation: "Concentrating all strategic knowledge and accounting truths in the hands of one individual guarantees an information bottleneck that hides systemic risk." — Source: [Investopedia: Ivar Kreuger]

- On the illusion of modesty: "Modest personal habits—working late, speaking softly—are highly effective cover for aggressive, debt-fueled corporate expansion." — Source: [The Life and Death of Ivar Kreuger]

- On managing the press: "By remaining aloof from daily media scrums, a corporate leader can ensure that when they do speak, their words are treated as market-moving gospel." — Source: [The Economist: The Match King]

- On the danger of unquestioned authority: "When a founder's reputation ascends to a level where questioning their methods is considered a breach of etiquette, fraud becomes structurally protected." — Source: [The Match King by Frank Partnoy]

Part 2: Monopoly and Market Dominance

- On the appeal of monopolies: "True pricing power does not come from out-competing rivals on the open market, but from legally eliminating them through exclusive government contracts." — Source: [Investopedia: Ivar Kreuger]

- On matches as a commodity: "The ideal monopoly is built on a high-margin, high-volume, low-cost necessity that is immune to technological disruption." — Source: [Wikipedia: Ivar Kreuger]

- On tying debt to market access: "Loaning money to desperate governments in exchange for exclusive national production rights turns sovereign debt into a vehicle for corporate conquest." — Source: [The Economist: The Match King]

- On scaling horizontally: "Controlling the means of production is only half the battle; capturing the entire supply chain, from timber to retail distribution, ensures no competitor can undercut prices." — Source: [Harvard Business School: Ivar Kreuger Case]

- On the illusion of stability: "A portfolio of national monopolies appears mathematically invincible to investors, masking the underlying fragility of the debt used to acquire them." — Source: [The Match King by Frank Partnoy]

- On leveraging the gold standard: "By operating across multiple currencies during a period of monetary instability, a multinational monopoly can arbitrage exchange rates to inflate reported profits." — Source: [The Life and Death of Ivar Kreuger]

- On the elasticity of demand: "The Swedish match has not felt any effect from the current crisis... Often unemployment causes an increase in match consumption because when people do not work, they smoke more cigarettes." — Source: [1931 Letter via TopWar]

- On the limits of geographic expansion: "A strategy reliant on continuously acquiring new national monopolies eventually exhausts the map, forcing the business to invent new ways to show growth." — Source: [The Economist: The Match King]

- On market consolidation: "Aggressive acquisition of smaller rivals, often at inflated prices, is a necessary cost of maintaining the narrative that your company is the only viable player in the industry." — Source: [Wikipedia: Ivar Kreuger]

Part 3: Financial Engineering and Complexity

- On extreme complexity: "When a corporate structure becomes a labyrinth of cross-holdings and shell companies, the complexity itself is often the product, designed to obscure the absence of real cash flow." — Source: [The Match King by Frank Partnoy]

- On off-balance-sheet vehicles: "Shifting debt to unlisted subsidiary companies allows the parent corporation to project an image of pristine financial health to public markets." — Source: [Investopedia: Ivar Kreuger]

- On dividend policies: "Paying unnaturally high, consistent dividends out of capital rather than operating profit is a desperate tactic to keep share prices elevated and attract new capital." — Source: [Wikipedia: Ivar Kreuger]

- On the role of auditing: "In an era before standardized international accounting, a company that audits itself across dozens of jurisdictions can essentially dictate its own financial reality." — Source: [Harvard Business School: Ivar Kreuger Case]

- On the utility of foreign exchange: "Booking profits in strong currencies while hiding liabilities in weak or collapsing currencies creates an optical illusion of massive asset growth." — Source: [The Economist: The Match King]

- On the issuance of new securities: "Constantly creating novel financial instruments, such as participating debentures, allows a company to raise capital without diluting the voting control of the founder." — Source: [The Match King by Frank Partnoy]

- On the nature of a Ponzi scheme within a corporation: "When the cash required to service existing debt can only be found by issuing new debt, the enterprise has shifted from a business to a systemic fraud." — Source: [Investopedia: Ivar Kreuger]

- On overvaluing assets: "Assigning arbitrary, inflated values to intangible assets like 'monopoly concessions' allows a balance sheet to balance, regardless of actual cash reserves." — Source: [Wikipedia: Ivar Kreuger]

- On the speed of financial innovation: "Financial regulation almost always lags a decade behind the invention of the instruments designed to exploit its loopholes." — Source: [The Match King by Frank Partnoy]

- On the appeal of black box investments: "Investors will readily fund a mechanism they do not understand, provided it consistently delivers above-market returns." — Source: [The Economist: The Match King]

Part 4: Government Relations and Sovereign Debt

- On acting as a central bank: "When private enterprise assumes the role of a sovereign lender of last resort, the boundaries between state policy and corporate strategy dangerously blur." — Source: [The Match King by Frank Partnoy]

- On exploiting political desperation: "Governments struggling to rebuild after major conflicts will readily trade long-term national assets for short-term liquidity." — Source: [Wikipedia: Ivar Kreuger]

- On the diplomatic immunity of capital: "A financier holding the debt of multiple sovereign nations acquires a level of political influence that traditional diplomats can only envy." — Source: [Harvard Business School: Ivar Kreuger Case]

- On the risk of sovereign default: "Building a corporate empire on the assumption that nation-states will always honor their debts is a gamble that ignores the realities of revolution and regime change." — Source: [The Economist: The Match King]

- On the privatization of public revenue: "Securing monopolies in exchange for loans effectively turns a nation's tax-collection apparatus into a debt-servicing machine for foreign shareholders." — Source: [Investopedia: Ivar Kreuger]

- On negotiating from a position of strength: "The entity with immediate access to hard currency dictates the terms of engagement to any government facing a bond crisis." — Source: [The Life and Death of Ivar Kreuger]

- On the illusion of government backing: "Investors often wrongly assume that because a corporation deals directly with heads of state, its operations are implicitly guaranteed by those states." — Source: [The Match King by Frank Partnoy]

- On the geopolitical risks of expansion: "A global monopoly inherently exposes itself to the domestic political turmoil of every country in which it operates." — Source: [Wikipedia: Ivar Kreuger]

- On treating nations as clients: "When entire countries are reduced to line items on a corporate balance sheet, the scale of potential failure becomes systemic rather than localized." — Source: [The Economist: The Match King]

Part 5: Investor Psychology and Trust

- On the suspension of disbelief: "The market's desire for a guaranteed, high-yield return is so powerful that it will willfully ignore glaring inconsistencies in how that return is generated." — Source: [The Match King by Frank Partnoy]

- On the halo effect: "Once a leader is successfully branded as a visionary, investors will actively defend their questionable practices to protect their own psychological investment in the narrative." — Source: [Harvard Business School: Ivar Kreuger Case]

- On the fear of missing out: "Institutional investors often abandon their due diligence when they see their peers profiting from a vehicle they do not yet understand." — Source: [Investopedia: Ivar Kreuger]

- On the perception of size as safety: "The sheer scale of a global enterprise is often falsely equated with its stability, leading investors to believe it is simply too large to fail." — Source: [Wikipedia: Ivar Kreuger]

- On the complicity of the financial establishment: "Major banks and underwriting firms will overlook red flags as long as the fees for issuing new securities remain lucrative." — Source: [The Economist: The Match King]

- On the illusion of elite access: "Offering exclusive investment opportunities to prominent political and social figures creates a vanguard of powerful defenders who will vouch for the company's legitimacy." — Source: [The Life and Death of Ivar Kreuger]

- On the breakdown of critical analysis: "When financial statements are consistently presented with extreme confidence, analysts often substitute the presenter's conviction for actual mathematical proof." — Source: [The Match King by Frank Partnoy]

- On the psychology of the dividend: "For many investors, the regular arrival of a dividend check is the only proof of viability they require, making them blind to the erosion of the underlying capital." — Source: [Wikipedia: Ivar Kreuger]

- On the fragility of reputation: "A corporate empire built entirely on the personal credibility of its founder has a single point of failure that cannot be hedged." — Source: [Investopedia: Ivar Kreuger]

Part 6: Corporate Structure and Obfuscation

- On the utility of holding companies: "A multi-layered holding company structure is the most efficient way to maintain absolute control over a vast empire with a minority of actual equity." — Source: [The Match King by Frank Partnoy]

- On jurisdictional arbitrage: "Registering subsidiaries in countries with weak or non-existent corporate disclosure laws is a deliberate strategy to shield the core operations from scrutiny." — Source: [Wikipedia: Ivar Kreuger]

- On internal transactions: "Moving cash rapidly back and forth between hundreds of controlled entities creates a false velocity of money that looks like legitimate commercial revenue." — Source: [The Economist: The Match King]

- On the suppression of internal dissent: "A corporate culture that prizes loyalty to the founder above all else ensures that employees who discover accounting irregularities remain silent." — Source: [Harvard Business School: Ivar Kreuger Case]

- On the absence of independent boards: "A board of directors composed entirely of the founder's friends, employees, and dependents is a rubber stamp, not a mechanism of oversight." — Source: [Investopedia: Ivar Kreuger]

- On the weaponization of geography: "Keeping the corporate headquarters in one country, the financial operations in another, and the physical assets in a third makes a holistic audit nearly impossible." — Source: [The Life and Death of Ivar Kreuger]

- On the creation of phantom assets: "By forging bonds or overstating the value of distant real estate, a company can continuously satisfy lenders' demands for collateral without deploying real capital." — Source: [The Match King by Frank Partnoy]

- On the opacity of joint ventures: "Using joint ventures with foreign governments allows a company to book the profits immediately while hiding the liabilities behind state secrecy laws." — Source: [Wikipedia: Ivar Kreuger]

- On the manipulation of communication: "Controlling the flow of information between global offices allows a central authority to dictate different financial realities to different regional auditors." — Source: [The Economist: The Match King]

- On the architecture of a shell game: "The survival of a fraudulent enterprise depends on moving the liabilities just out of sight immediately before the auditors arrive." — Source: [The Match King by Frank Partnoy]

Part 7: Crisis, Collapse, and the Unraveling

- On the catalyst of economic shock: "A carefully constructed financial illusion can survive normal market fluctuations, but it will shatter instantly under the pressure of a global liquidity crisis." — Source: [Wikipedia: Ivar Kreuger]

- On the sudden evaporation of credit: "When the broader market panics, the ability to roll over short-term debt vanishes, exposing the insolvency of an enterprise that relies on constant refinancing." — Source: [Investopedia: Ivar Kreuger]

- On the speed of contagion: "The collapse of a central holding company instantly destroys the value of all its subsidiaries, revealing how interconnected the seemingly isolated assets truly were." — Source: [Harvard Business School: Ivar Kreuger Case]

- On the final desperate acts: "Forging sovereign bonds to use as collateral is the terminal stage of a financial fraud, signaling that all legitimate avenues of capital have been exhausted." — Source: [The Match King by Frank Partnoy]

- On the failure of implicit guarantees: "Even the most politically connected enterprises will be abandoned by governments when the scale of the fraud threatens the stability of the national banking system." — Source: [The Economist: The Match King]

- On the psychological toll of deception: "The mental burden of maintaining a multi-billion dollar lie inevitably erodes the judgment of the architect, leading to erratic and fatal decisions." — Source: [The Life and Death of Ivar Kreuger]

- On the nature of the end: "I have made such a mess of things that I believe this to be the most satisfactory solution for everybody concerned." — Source: [Wikipedia: Ivar Kreuger - Suicide]

- On the immediate aftermath: "The death of a charismatic founder instantly transforms a company from a going concern into a crime scene, as the suspension of disbelief evaporates." — Source: [The Match King by Frank Partnoy]

- On the discovery of the truth: "The true scale of a complex financial fraud is never understood until the architect is removed and independent accountants are finally given the keys to the vault." — Source: [Investopedia: Ivar Kreuger]

Part 8: Legacy and Regulatory Impact

- On the birth of modern regulation: "The sheer magnitude of a generational fraud is often the necessary catalyst for the creation of standardized, legally mandated financial disclosures." — Source: [The Match King by Frank Partnoy]

- On the legacy of the Securities Act: "The requirement that companies selling public securities must provide audited, truthful financial statements is a direct response to the abuses of unchecked corporate power." — Source: [Harvard Business School: Ivar Kreuger Case]

- On the separation of banking and commerce: "The realization that commercial banks were deeply compromised by their investments in fraudulent holding companies led directly to calls for structural firewalls in the financial industry." — Source: [Wikipedia: Ivar Kreuger]

- On the evolution of accounting standards: "The necessity of independent, third-party audits with rigorous standards for verifying assets became universally accepted only after the realization of how easily internal numbers could be manipulated." — Source: [The Economist: The Match King]

- On the enduring nature of financial scams: "While the specific instruments change, the underlying mechanics of exploiting investor greed, utilizing complexity, and centralizing control remain constant across eras." — Source: [Investopedia: Ivar Kreuger]

- On the cautionary tale of the visionary: "History remembers those who build real value, but it ruthlessly dissects those whose primary innovation was merely the manipulation of perception." — Source: [The Life and Death of Ivar Kreuger]

- On the cost of blind trust: "The destruction of wealth that follows a systemic fraud is a permanent reminder that in finance, trust must always be verified by math." — Source: [The Match King by Frank Partnoy]

- On the resilience of markets: "Despite the catastrophic failure of a dominant player, the underlying demand for the physical product remains, eventually allowing legitimate competitors to rebuild the industry." — Source: [Wikipedia: Ivar Kreuger]

- On the ultimate lesson of the Match King: "A business model built entirely on debt, obfuscation, and the personal mythology of its founder is not a company; it is a ticking time bomb." — Source: [The Match King by Frank Partnoy]