Jan Hummel founded Paradigm Capital in 2001, building his career by applying strict value investing principles to small and mid-cap companies across Northern Europe. He is known for relying on deep fundamental research and low-leverage balance sheets rather than trying to time broader market trends. The insights collected here cover his approach to capital allocation, risk management, and the temperament required to invest effectively in public markets.

Part 1: The Foundations of Value

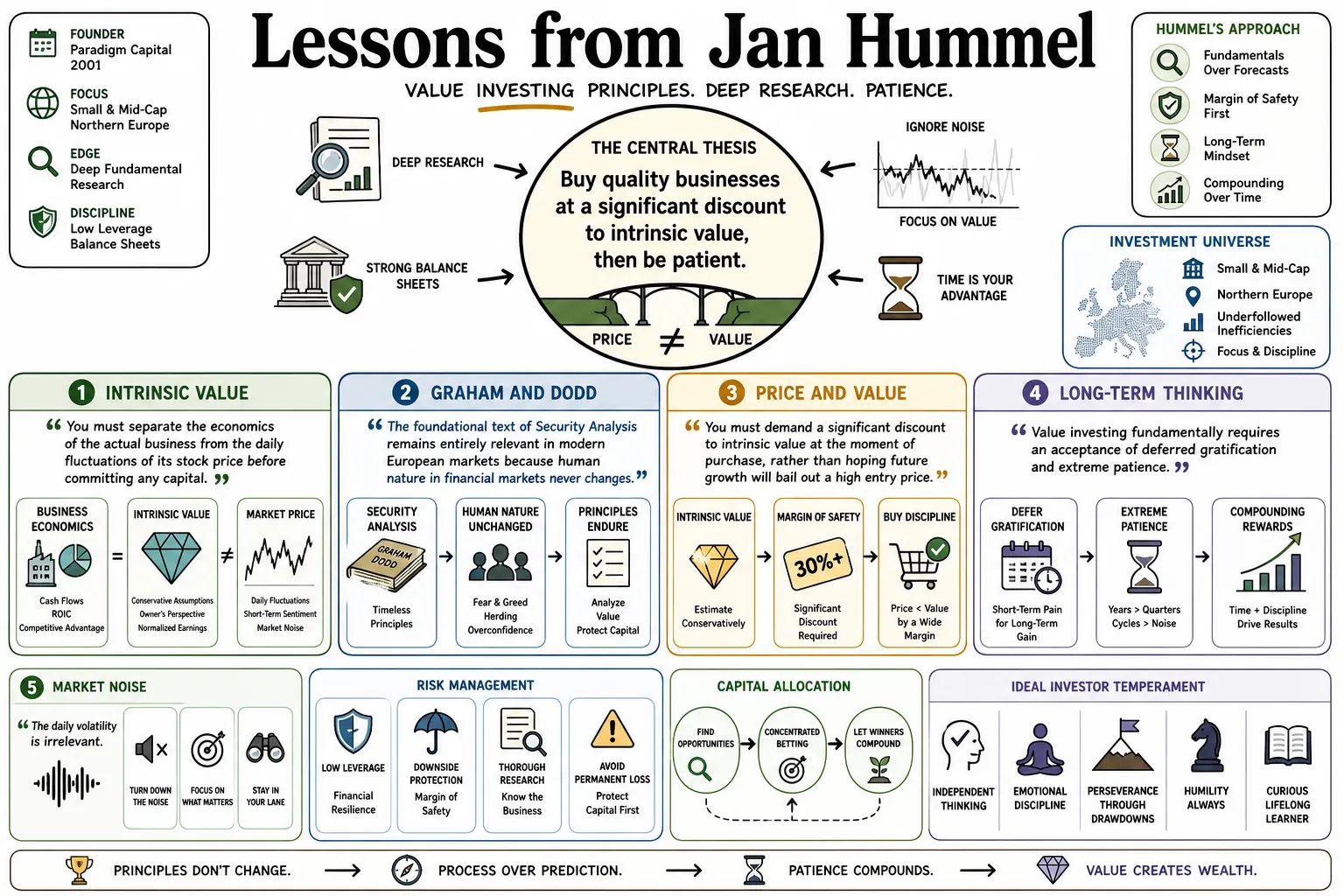

- On Intrinsic Value: "You must separate the economics of the actual business from the daily fluctuations of its stock price before committing any capital." — Source: [Santangel's Review]

- On Graham and Dodd: "The foundational text of Security Analysis remains entirely relevant in modern European markets because human nature in financial markets never changes." — Source: [Value Investing with Legends]

- On Price and Value: "You must demand a significant discount to intrinsic value at the moment of purchase, rather than hoping future growth will bail out a high entry price." — Source: [Ben Graham Centre]

- On Long-Term Thinking: "Value investing fundamentally requires an acceptance of deferred gratification and extreme patience." — Source: [Paradigm Capital]

- On Market Noise: "The daily volatility of the stock market serves as a distraction for anyone trying to assess the long-term cash generation of a real company." — Source: [Value Investing with Legends]

- On Business Fundamentals: "A share of stock is simply a fractional interest in a business, and it must be analyzed exactly through that lens." — Source: [Santangel's Review]

- On Simple Businesses: "Complexity in a business model often hides fragility. We prefer companies where the mechanics of cash generation are transparent." — Source: [Ben Graham Centre]

- On Consistency: "Our edge comes not from successfully predicting the future, but from consistently buying quality assets when the broader market prices them for distress." — Source: [Value Investing with Legends]

- On Economic Moats: "A business without strong barriers to entry is a melting ice cube, regardless of how cheap the valuation multiples look today." — Source: [Santangel's Review]

- On Historical Context: "Having lived through previous cycles gives you the perspective required to recognize when market participants are acting irrationally." — Source: [Value Investing with Legends]

Part 2: Deep Diligence

- On Research Intensity: "Our strategy relies on doing more fundamental research than our competitors, rather than trying to forecast macroeconomic shifts." — Source: [Santangel's Review]

- On Real-World Experience: "Decades spent in private equity and restructurings teach you to look at a public company's balance sheet the way a creditor would." — Source: [Value Investing with Legends]

- On Reading the Footnotes: "The most critical disclosures regarding a company's financial health are almost never found on the first page of the annual report." — Source: [Ben Graham Centre]

- On Field Work: "You cannot fully understand a mid-cap manufacturing business without physically visiting the facilities and talking to the people on the factory floor." — Source: [Paradigm Capital]

- On Earnings Quality: "We heavily scrutinize proven historical earnings power rather than relying on a management team's adjusted, forward-looking projections." — Source: [Value Investing with Legends]

- On Restructurings: "Understanding a turnaround situation requires diagnosing whether the core problem is a temporary operational hiccup or a permanent structural decline in the industry." — Source: [Santangel's Review]

- On Competitor Analysis: "To understand the true durability of a company's profit margins, you must spend equal time analyzing the unit economics of their direct competitors." — Source: [Value Investing with Legends]

- On Cash Flows: "Reported profits can be heavily manipulated by accounting assumptions, but cash flow generated from actual operations is much harder to fake." — Source: [Ben Graham Centre]

- On Valuation Models: "A financial model is only as useful as the conservatism of its inputs; precision in a spreadsheet should never be confused with accuracy." — Source: [Santangel's Review]

- On Information Overload: "Effective diligence is not about gathering the most data, but filtering out the noise to identify the two or three variables that truly drive the business." — Source: [Paradigm Capital]

Part 3: Margin of Safety and Risk Management

- On the Margin of Safety: "The margin of safety is a non-negotiable requirement at the time of purchase; it is the only thing that protects you from your own inevitable analytical mistakes." — Source: [Ben Graham Centre]

- On Diluting Discipline: "The protection of a margin of safety is entirely diluted the moment an investor compromises on their underwriting discipline to chase a trend." — Source: [Value Investing with Legends]

- On Permanent Loss: "Our primary objective is always the absolute avoidance of permanent capital impairment, not the maximization of short-term quarterly returns." — Source: [Santangel's Review]

- On Macro Risks: "We rely on rigorous bottom-up analysis to understand exactly how a specific business is exposed to economic boom and bust cycles." — Source: [Ben Graham Centre]

- On Valuation as Protection: "Overpaying for a great business removes your margin of safety just as surely as buying a deteriorating business at a steep discount." — Source: [Value Investing with Legends]

- On Hedging: "While our core focus is equity ownership, we are willing to use hedging and non-equity instruments to protect the portfolio from severe downside scenarios." — Source: [Paradigm Capital]

- On Evaluating Downside: "Before we ever ask how much money we can make on an investment, we rigorously attempt to figure out exactly how much we can lose." — Source: [Santangel's Review]

- On Cyclicality: "Investors routinely mistake peak cyclical earnings for permanent structural growth, which destroys their margin of safety when the cycle inevitably turns." — Source: [Value Investing with Legends]

- On Portfolio Construction: "Real risk management is achieved by thoroughly understanding the ten businesses you own, rather than holding a hundred names you understand poorly." — Source: [Ben Graham Centre]

Part 4: Capital Allocation and Leverage

- On Financial Leverage: "We deliberately target companies with limited financial leverage; debt removes operational flexibility and introduces existential risk during a downturn." — Source: [Santangel's Review]

- On Management's Role: "A CEO's most critical responsibility is capital allocation, yet very few operators come into the role with any formal training in it." — Source: [Value Investing with Legends]

- On Returns on Capital: "Over a long enough timeline, a stock's return will roughly mirror the company's internal return on invested capital." — Source: [Paradigm Capital]

- On Acquisitions: "We remain highly skeptical of growth through acquisition unless the management team has a proven history of integrating businesses at sensible multiples." — Source: [Santangel's Review]

- On Share Repurchases: "Buybacks only create value for continuing shareholders when they are executed at a meaningful discount to the company's intrinsic value." — Source: [Value Investing with Legends]

- On Reinvestment: "The ideal business generates significant free cash flow and has a long internal runway to reinvest that cash at high rates of return." — Source: [Ben Graham Centre]

- On Dividends: "If a company lacks high-return internal projects, we expect management to return capital to shareholders rather than attempt to build an empire." — Source: [Paradigm Capital]

- On Debt at the Portfolio Level: "We strictly avoid using leverage at the portfolio level, as margin debt forces your hand during the exact moments you should be buying aggressively." — Source: [Ben Graham Centre]

- On Hidden Liabilities: "Off-balance sheet obligations, pension liabilities, and aggressive accounting are forms of hidden leverage that we refuse to underwrite." — Source: [Santangel's Review]

Part 5: Identifying High-Quality Management

- On Assessing Operators: "We want management teams that operate the company as if they own the entire business, not hired hands managing for the next quarter." — Source: [Santangel's Review]

- On Alignment of Interests: "The absolute best protection for a minority public shareholder is a management team that has a substantial portion of their own net worth invested in the common stock." — Source: [Value Investing with Legends]

- On Track Records: "You evaluate management not by the forward-looking promises in the annual report, but by studying their past capital allocation decisions." — Source: [Ben Graham Centre]

- On Corporate Culture: "A distinct culture of frugality and operational efficiency usually originates at the very top and permeates the entire organization." — Source: [Paradigm Capital]

- On Turnaround Leaders: "In a severe restructuring, the incumbent management team who caused the problem is almost never the team equipped to fix it." — Source: [Santangel's Review]

- On Candor: "We prefer executives who speak bluntly about the challenges the business faces over those who present uninterrupted, polished optimism." — Source: [Value Investing with Legends]

- On Compensation: "Executive incentive structures must be strictly aligned with long-term per-share value creation, not merely top-line revenue growth or short-term stock performance." — Source: [Ben Graham Centre]

- On Founder-Led Companies: "Founder-operated businesses often retain a long-term strategic view that traditional, bureaucratic corporate structures struggle to maintain." — Source: [Paradigm Capital]

- On Board Governance: "An active and independent board is necessary to ensure that management's capital allocation serves all shareholders, rather than just enriching corporate insiders." — Source: [Santangel's Review]

Part 6: Understanding European Markets

- On the Nordic Region: "The Nordic markets consistently produce high-quality, export-driven industrial companies with deeply ingrained engineering cultures." — Source: [Santangel's Review]

- On Structural Inefficiencies: "Small- and mid-cap European companies are frequently ignored by large global institutions, creating structural pricing inefficiencies we can exploit." — Source: [Value Investing with Legends]

- On the DACH Region: "In the German-speaking regions, you find 'Mittelstand' companies that dominate highly specific, niche global markets with immense pricing power." — Source: [Paradigm Capital]

- On Language and Culture: "Understanding local business culture and speaking the language remains a critical advantage when assessing management teams in regional European markets." — Source: [Ben Graham Centre]

- On Accounting Differences: "While international standards have unified much of European accounting, local nuances in how depreciation and provisions are handled still offer an edge to careful analysts." — Source: [Santangel's Review]

- On Market Myopia: "European equity markets often overreact to macroeconomic slowdowns, allowing us to buy durable industrial businesses at distressed prices." — Source: [Value Investing with Legends]

- On Corporate Structures: "Cross-shareholdings and dual-class share structures in Europe require careful underwriting to ensure minority investors are not systematically disadvantaged." — Source: [Paradigm Capital]

- On Private Equity Dynamics: "Having a background in European private equity allows us to view public market investments through the strict lens of a control buyer." — Source: [Santangel's Review]

- On Regional Resilience: "Despite consistently negative macro headlines, the underlying operational resilience of Northern European industrials is frequently underestimated by foreign investors." — Source: [Value Investing with Legends]

Part 7: Variant Perception and Contrarianism

- On Having an Edge: "You must develop a 'variant perception'—a view that is distinctly different from the consensus and backed by rigorous, verifiable analysis." — Source: [Value Investing with Legends]

- On Concentration: "We stay as far away from the index as possible; portfolio concentration is a form of contrarianism that forces you to only capitalize on your highest-conviction ideas." — Source: [Ben Graham Centre]

- On Being Uncomfortable: "The absolute best investments often make you feel slightly uncomfortable when you initially make them, because the consensus view is usually fiercely negative." — Source: [Santangel's Review]

- On Market Reactions: "When the market aggressively sells off a solid business due to a temporary, highly solvable issue, that is exactly where we deploy capital." — Source: [Paradigm Capital]

- On Independent Thinking: "You cannot generate outsized returns by reading the same sell-side reports and arriving at the same safe conclusions as everyone else." — Source: [Value Investing with Legends]

- On Institutional Imperatives: "Large funds are often forced to liquidate illiquid small-caps during times of stress; we act as liquidity providers in those exact moments." — Source: [Santangel's Review]

- On Patience as an Advantage: "In an environment driven by quarterly earnings estimates, simply having a three-to-five year time horizon is a massive structural advantage." — Source: [Value Investing with Legends]

- On Groupthink: "If you find yourself agreeing with the majority of the financial press on a given stock, it is time to ruthlessly re-evaluate your thesis." — Source: [Ben Graham Centre]

- On Boring Businesses: "The most reliable returns often come from dull, overlooked industries that attract zero attention from growth-focused momentum funds." — Source: [Paradigm Capital]

- On Pricing Anomalies: "Market panics do not destroy intrinsic value; they simply serve as a mechanism to transfer wealth from the impatient to the patient." — Source: [Santangel's Review]

Part 8: The Temperament of an Investor

- On Emotional Discipline: "The mechanics of valuation are straightforward; it is the temperament to act rationally during chaos that separates great investors from average ones." — Source: [Value Investing with Legends]

- On Conviction: "When you have done the deep diligence yourself, you have the conviction to hold through severe volatility rather than being shaken out of a position." — Source: [Santangel's Review]

- On Intellectual Honesty: "An investor must be willing to admit when the facts change and quickly exit a position if the original thesis proves definitively incorrect." — Source: [Value Investing with Legends]

- On Humility: "The market is a continuous, expensive lesson in humility; the moment you believe you have figured it out, you are vulnerable to significant losses." — Source: [Ben Graham Centre]

- On Staying in the Game: "Longevity in this business requires setting up your portfolio to ensure that no single mistake can ever take you entirely out of the game." — Source: [Paradigm Capital]

- On Focus: "You must ruthlessly protect your time and attention from the noise of the market and focus only on what is both knowable and important." — Source: [Santangel's Review]

- On Tenacity: "Value investing requires a certain tenacity—the willingness to dig deeper into the footnotes than the next person is willing to go." — Source: [Value Investing with Legends]

- On Continuous Learning: "Every investment mistake is a tuition payment; the goal is to make sure you never pay tuition for the exact same lesson twice." — Source: [Ben Graham Centre]

- On Defining Success: "True success in investing is not about beating a benchmark in any given quarter, but safely compounding capital over decades." — Source: [Paradigm Capital]