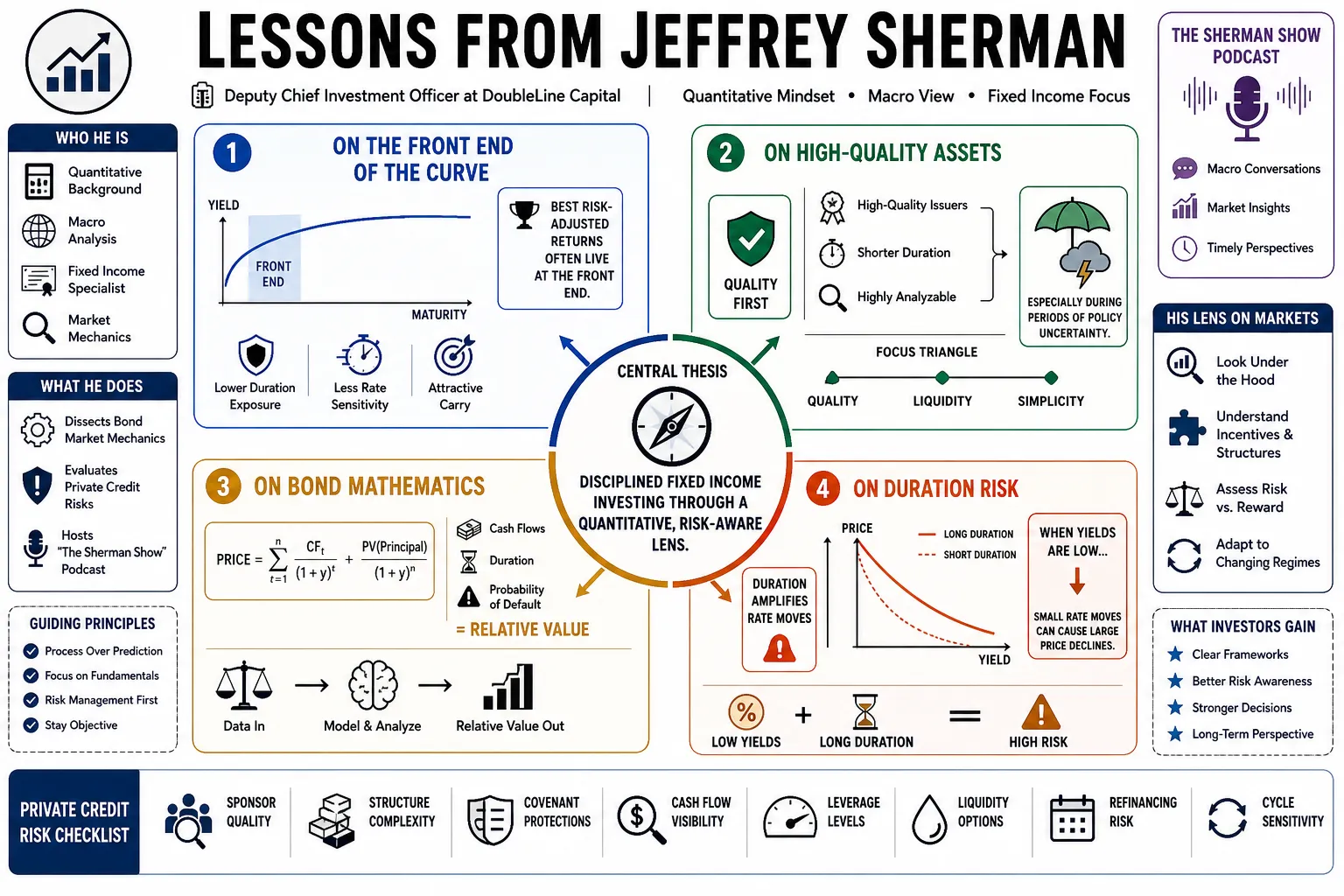

Jeffrey Sherman serves as the Deputy Chief Investment Officer at DoubleLine Capital, where he applies a quantitative background to macroeconomic analysis and fixed income. He is known for dissecting bond market mechanics, evaluating the hidden risks of private credit, and hosting "The Sherman Show" podcast. This compilation catalogs his perspectives on market fundamentals and asset allocation, offering practical guidelines for navigating complex economic environments.

Part 1: Fixed Income Strategy

- On the Front End of the Curve: "The dirty secret in the bond market is that some of the best risk-adjusted returns are often found at the front end of the yield curve." — Source: [DoubleLine Webcasts]

- On High-Quality Assets: "We advocate for holding high-quality, shorter-duration, and highly analyzable assets, especially during periods of policy uncertainty." — Source: [The Sherman Show]

- On Bond Mathematics: "Fixed income is ultimately a math problem; you are looking at cash flows, duration, and the probability of default to determine relative value." — Source: [Bloomberg Masters in Business]

- On Duration Risk: "Investors often underestimate duration risk when yields are low, forgetting that small interest rate moves can cause significant price declines." — Source: [CNBC Media Appearances]

- On Core Fixed Income: "A core bond portfolio should act as a reliable anchor, rather than a source of speculative return that correlates highly with equities." — Source: [DoubleLine Capital]

- On Credit Selection: "In corporate credit, you have to do the fundamental homework to ensure you are being adequately compensated for the default risk you assume." — Source: [Yahoo Finance]

- On High Yield Bonds: "High yield can offer equity-like returns with less volatility, but only if you avoid the land mines at the bottom of the credit spectrum." — Source: [The Sherman Show]

- On Liquidity in Bonds: "Public fixed income markets offer a level of daily liquidity and price discovery that investors often take for granted until they step into private markets." — Source: [DoubleLine Webcasts]

- On Mortgage-Backed Securities: "Agency MBS provides an attractive spread over Treasuries with implicit government backing, making it a central component of high-quality fixed income allocations." — Source: [Bloomberg TV]

- On Active Management: "Passive bond indices are structurally flawed because they reward the most indebted issuers with the highest weightings; active management is required to avoid this trap." — Source: [DoubleLine Capital]

Part 2: Macroeconomics and Growth

- On Economic Fundamentals: "Tune out the headline ping-pong and focus on underlying fundamentals, such as fiscal deficits and labor market shifts." — Source: [The Sherman Show]

- On Labor Shortages: "The long-term underinvestment in skilled trades creates a meaningful, underappreciated headwind to future economic growth." — Source: [Bloomberg Masters in Business]

- On Fiscal Deficits: "Massive structural fiscal deficits are fundamentally altering the supply dynamics of the Treasury market and crowding out private investment." — Source: [CNBC Media Appearances]

- On Immigration Policy: "Labor force growth is a primary driver of GDP, making immigration policy a central, yet often overlooked, macroeconomic variable." — Source: [The Sherman Show]

- On Geopolitical Shifts: "In an environment characterized by war and structural economic shifts, the historical models of globalization are being rewritten." — Source: [DoubleLine Webcasts]

- On Productivity: "Technological advancements must translate into measurable productivity gains to offset the demographic drag of an aging population." — Source: [Yahoo Finance]

- On Consumer Strength: "The resilience of the US consumer is heavily tied to the labor market and excess savings, both of which are finite resources." — Source: [Bloomberg TV]

- On Supply Chains: "Reshoring and supply chain redundancies enhance economic security but inherently drive up the baseline cost of production." — Source: [DoubleLine Capital]

- On Energy Costs: "Energy serves as the baseline input for the entire global economy; structural underinvestment in energy infrastructure constrains broad economic growth." — Source: [The Sherman Show]

- On Structural Headwinds: "We are transitioning from an era of abundant labor and cheap capital to one of constrained resources and structurally higher financing costs." — Source: [CNBC Media Appearances]

Part 3: The Yield Curve and Recession Indicators

- On Yield Curve Inversion: "You need that persistence. It can't just be inverted one day and that means recession's coming. It needs to be persistent for a period of time." — Source: [Business Insider]

- On Interpreting Signals: "There is no exact science to timing a recession based on the yield curve; it is as much art as it is mathematics." — Source: [The Sherman Show]

- On the Steepening Curve: "The real danger often materializes not when the curve inverts, but when it rapidly steepens as the Federal Reserve begins to cut rates in a panic." — Source: [Bloomberg Masters in Business]

- On Term Premium: "Investors are increasingly demanding a higher term premium to hold longer-dated debt given the uncertainty around inflation and fiscal supply." — Source: [DoubleLine Webcasts]

- On Leading Indicators: "We look at an aggregate of leading economic indicators, rather than relying on a single data point, to form our macroeconomic baseline." — Source: [CNBC Media Appearances]

- On False Positives: "While the yield curve has an excellent track record, post-pandemic market distortions require us to question traditional recessionary timelines." — Source: [Yahoo Finance]

- On the 2-Year Treasury: "The 2-year Treasury yield is often a more accurate reflection of where Fed policy is heading than the Fed's own dot plot." — Source: [Bloomberg TV]

- On Curve Normalization: "A normalized, upward-sloping yield curve is necessary for the healthy functioning of the financial system and traditional banking models." — Source: [The Sherman Show]

- On Economic Lags: "Monetary policy operates with long and variable lags; the effects of rate hikes often surface long after the market assumes the danger has passed." — Source: [DoubleLine Capital]

Part 4: Inflation and Fed Policy

- On Inflation Shocks: "Policymakers should avoid overreacting to oil-driven inflation shocks, as these surges often act as a form of monetary policy tightening themselves." — Source: [DoubleLine Webcasts]

- On Sticky Inflation: "Service sector inflation and wage growth are inherently stickier than goods inflation, requiring sustained restrictive policy to cool down." — Source: [Bloomberg Masters in Business]

- On the Fed's Mandate: "The Federal Reserve is constantly balancing its dual mandate, but when inflation flares, price stability must become the singular focus." — Source: [The Sherman Show]

- On Forward Guidance: "The market has become too reliant on Fed forward guidance, which often traps policymakers into predetermined paths regardless of new data." — Source: [CNBC Media Appearances]

- On Quantitative Tightening: "Quantitative tightening removes systemic liquidity in ways that are difficult to model, increasing the probability of sudden market accidents." — Source: [Yahoo Finance]

- On Real Rates: "Positive real interest rates are essential for curbing speculative excess and properly allocating capital across the economy." — Source: [Bloomberg TV]

- On Inflation Expectations: "If consumers and businesses embed higher inflation expectations into their behavior, the Fed's job becomes exponentially more difficult." — Source: [DoubleLine Capital]

- On Policy Errors: "The classic central banking error is cutting rates prematurely before inflation is fully extinguished, leading to a secondary, more damaging inflationary wave." — Source: [The Sherman Show]

- On the Neutral Rate: "The neutral rate of interest is likely structurally higher today due to deglobalization, decarbonization, and demographic shifts." — Source: [DoubleLine Webcasts]

Part 5: Portfolio Construction and Risk Management

- On Surviving Land Mines: "A durable portfolio must be constructed to weather the land mine so that the firm remains in business to capitalize on future opportunities." — Source: [The Sherman Show]

- On Asset Allocation: "Asset allocation is about balancing risks, rather than solely chasing returns; you must understand how different assets behave under various macroeconomic stress tests." — Source: [DoubleLine Capital]

- On the 60/40 Portfolio: "The traditional 60/40 portfolio requires structural adjustments when stock-bond correlations flip from negative to positive during inflationary periods." — Source: [Bloomberg Masters in Business]

- On Finding Quality: "What really one needs to focus on right now is just finding quality still in the marketplace, prioritizing balance sheet strength." — Source: [CNBC Media Appearances]

- On Diversification: "True diversification means holding assets that will actively perform well when your primary growth engines fail, rather than assets that fall slightly less." — Source: [Yahoo Finance]

- On Drawdowns: "Avoiding severe drawdowns is mathematically more important to long-term wealth compounding than capturing every percentage point of upside." — Source: [Bloomberg TV]

- On Quantitative Modeling: "Quantitative models are invaluable for framing risk, but they must be paired with human judgment to account for regime changes that the models have never seen." — Source: [The Sherman Show]

- On Volatility as Opportunity: "Volatility is not strictly a risk to be avoided; for the prepared investor with liquidity, it is the mechanism that creates attractive entry points." — Source: [DoubleLine Webcasts]

- On Correlation Shifts: "Investors must constantly re-evaluate their correlation assumptions, as assets that hedge each other in a deflationary scare may move in tandem during an inflation shock." — Source: [DoubleLine Capital]

- On Liquidity Management: "Maintaining adequate portfolio liquidity is the ultimate form of risk management, allowing you to play offense when others are forced to play defense." — Source: [The Sherman Show]

Part 6: Emerging Markets and Global Trade

- On EM Yields: "Emerging market local currency bonds can offer attractive yields while providing a natural hedge against a potentially weaker U.S. dollar." — Source: [DoubleLine Webcasts]

- On EM Fundamentals: "Many emerging economies have vastly improved their balance sheets and orthodox monetary policies compared to previous decades." — Source: [Bloomberg TV]

- On the U.S. Dollar: "The trajectory of the U.S. dollar is the single most important variable for emerging market asset performance and global capital flows." — Source: [The Sherman Show]

- On Commodity Exporters: "Emerging markets that export base commodities are uniquely positioned to benefit from the global transition toward renewable energy infrastructure." — Source: [CNBC Media Appearances]

- On Trade Tariffs: "Tariffs act as a regressive tax on consumers and disrupt the optimized global supply chains that kept inflation low for the past twenty years." — Source: [Yahoo Finance]

- On China's Economy: "China's transition from an export-driven manufacturing hub to a domestic consumption model presents deep deflationary and inflationary ripple effects globally." — Source: [Bloomberg Masters in Business]

- On Sovereign Risk: "Evaluating emerging market sovereign debt requires a deep understanding of local politics, institutional stability, and reliance on external financing." — Source: [DoubleLine Capital]

- On Deglobalization: "The fracturing of global trade into regional blocs reduces aggregate economic efficiency and structural growth rates worldwide." — Source: [The Sherman Show]

- On Currency Hedging: "When investing internationally, the decision to hedge currency risk is often as consequential as the underlying asset selection itself." — Source: [DoubleLine Webcasts]

Part 7: Private Credit and Systemic Risks

- On the Margin Vortex: "Semi-liquid private credit vehicles carry a hidden contagion risk, creating a 'margin vortex' when investors attempt to redeem and cannot." — Source: [The Sherman Show]

- On Forced Selling: "When private fund redemptions are gated, investors are forced to sell their liquid public assets to raise cash, dragging down broader public valuations." — Source: [Bloomberg TV]

- On Illiquidity Premiums: "Investors must critically assess whether the yield premium they earn in private credit adequately compensates them for the total loss of liquidity." — Source: [CNBC Media Appearances]

- On Valuation Lags: "Private market valuations often operate on a delay, creating a false sense of stability compared to the daily mark-to-market pricing of public markets." — Source: [Yahoo Finance]

- On Default Cycles: "The true test of the private credit boom will only occur during a sustained economic downturn when corporate cash flows are severely impaired." — Source: [DoubleLine Webcasts]

- On Leverage in the System: "Systemic risk usually hides in the shadows of lightly regulated, highly indebted vehicles that promise steady returns with limited volatility." — Source: [Bloomberg Masters in Business]

- On Covenant-Lite Loans: "The proliferation of covenant-lite loans limits the ability of lenders to intervene early when a borrower's financial health begins to deteriorate." — Source: [DoubleLine Capital]

- On Retail Access: "Democratizing access to illiquid private investments for retail investors introduces significant behavioral risks during periods of market stress." — Source: [The Sherman Show]

- On Capital Misallocation: "When capital flows too freely into private vehicles chasing yield, it invariably leads to relaxed underwriting standards and misallocated resources." — Source: [CNBC Media Appearances]

Part 8: Market Psychology and Valuation

- On Equity Valuations: "When equities trade at 25x forward earnings while short-term Treasuries offer competitive yields, the risk-reward tradeoff becomes difficult to justify." — Source: [DoubleLine Webcasts]

- On the Buy-the-Dip Mentality: "The traditional 'buy-the-dip' strategy may be more dangerous now than in previous years due to shifting geopolitical and macroeconomic realities." — Source: [The Sherman Show]

- On Complacency: "Prolonged periods of central bank intervention have bred market complacency, teaching investors to ignore fundamental risks." — Source: [Bloomberg TV]

- On Market Narratives: "Investors must separate compelling narratives from mathematical realities; a great technological story does not automatically equal a great investment at any price." — Source: [Yahoo Finance]

- On Behavioral Biases: "Recency bias causes investors to assume the macroeconomic conditions of the past decade will persist indefinitely into the future." — Source: [DoubleLine Capital]

- On Yield Chasing: "Reaching for yield in late-cycle environments is a classic behavioral error that typically ends in severe principal impairment." — Source: [CNBC Media Appearances]

- On Contrarian Investing: "True contrarianism requires the mathematical conviction to stand by your analysis when the broader market is consumed by euphoria or panic." — Source: [Bloomberg Masters in Business]

- On Patience: "Sometimes the best investment decision is to sit in cash or short-term paper and wait for valuations to normalize." — Source: [The Sherman Show]

- On Market Hubris: "The market has a humbling way of reminding investors that risk cannot be permanently destroyed, only transferred or hidden." — Source: [DoubleLine Webcasts]