Jeremy Siegel is a finance professor at the Wharton School who demonstrated that stocks reliably outperform bonds and gold over extended time horizons. He is best known for his 1994 book Stocks for the Long Run, which used two centuries of market data to show how dividends and compounding drive wealth creation. This profile organizes his historical research, views on the "growth trap," and critiques of Federal Reserve policy into a straightforward reference guide.

Part 1: The Long Run Thesis & Historical Returns

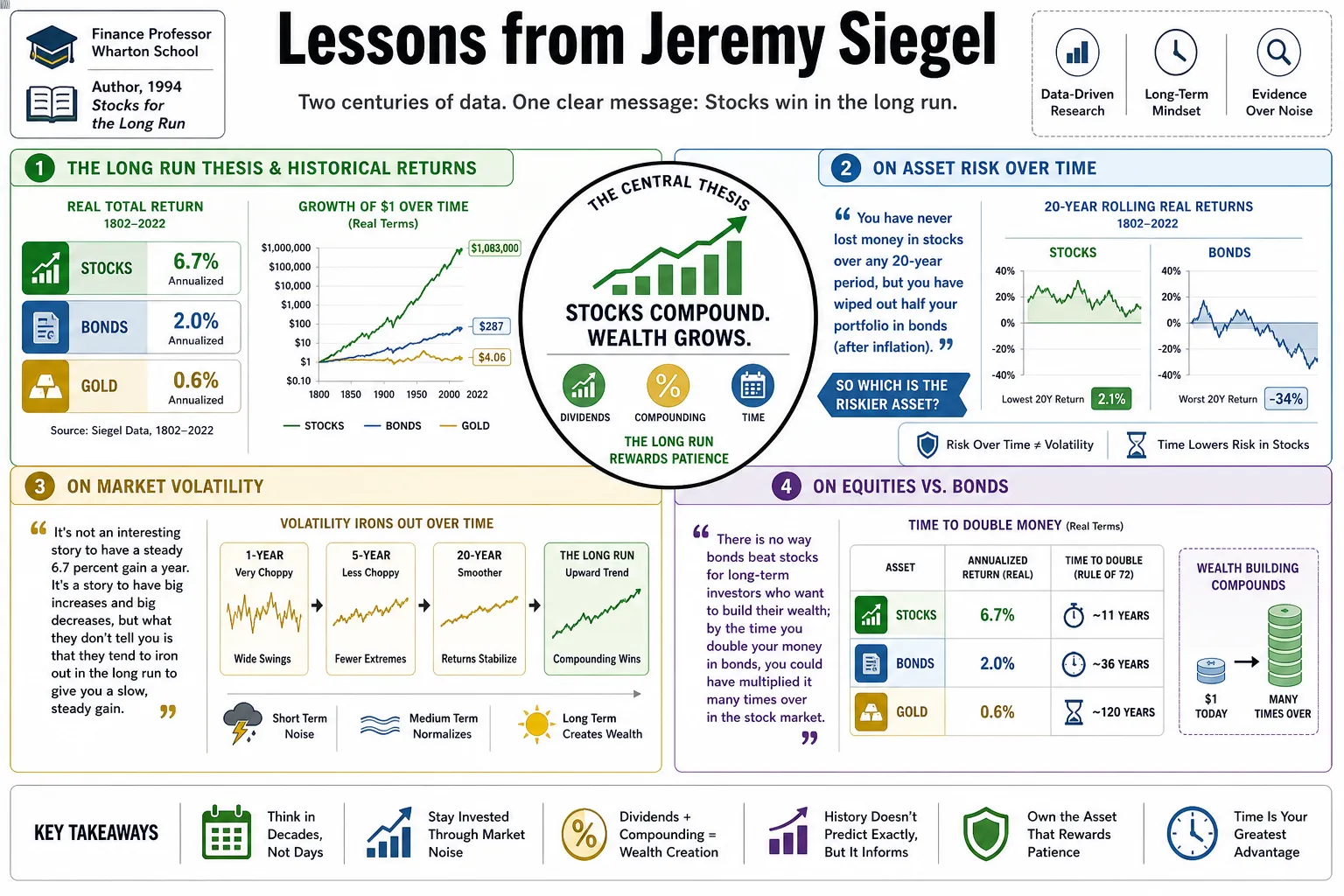

- On Asset Risk over Time: "You have never lost money in stocks over any 20-year period, but you have wiped out half your portfolio in bonds (after inflation). So which is the riskier asset?" — Source: [AZQuotes]

- On Market Volatility: "It's not an interesting story to have a steady 6.7 percent gain a year. It's a story to have big increases and big decreases, but what they don't tell you is that they tend to iron out in the long run to give you a slow, steady gain." — Source: [Penn Today]

- On Equities vs. Bonds: "There is no way bonds beat stocks for long-term investors who want to build their wealth; by the time you double your money in bonds, you could have multiplied it many times over in the stock market." — Source: [Business Insider]

- On Gold as an Investment: "Gold is a very expensive insurance policy that produces nothing and pays no income, leading to negligible real returns compared to equities." — Source: [WisdomTree]

- On Purchasing Power: "Stocks are the safest long-term investment for the preservation of purchasing power against the erosive effects of inflation." — Source: [Efficient Frontier]

- On Long-term Holding: "While stocks are volatile in the short run, their risk relative to bonds actually diminishes over long holding periods." — Source: [CFA Institute]

- On the 1802 Chart: "A single dollar invested in gold in 1802 would have grown to only a few dollars in real purchasing power over two centuries, whereas a similar investment in stocks would have grown into millions." — Source: [Marotta on Money]

- On Bear Market Recoveries: "Historically, even the most severe bear markets, such as those during the Great Depression, appear as mere blips in the long-term upward trajectory of equity values." — Source: [Knowledge at Wharton]

- On the Equity Premium: "The equity risk premium should always be measured consistently as the difference between the real riskless return, positive or negative, and the return on risky equity." — Source: [CFA Institute]

- On Historical Context: "Early stock returns did not exceed fixed-income returns by the same magnitude seen in more recent, high-performing decades, suggesting the post-WWII premium was exceptionally high." — Source: [EconDSE]

Part 2: The Growth Trap & Valuation

- On the Growth Trap: "The growth trap is the tendency for investors to simply buy the fastest-growing firm in terms of earnings, or the fastest-growing sector. My research confirms that this is most often a poor strategy." — Source: [Financial Wisdom Forum]

- On Seductive Technologies: "The Growth Trap seduces investors into overpaying for the very firms and industries that drive innovation and spearhead economic expansion." — Source: [WisdomTree]

- On Growth Expectations: "The return on stocks depends not on earnings growth but solely on whether this earnings growth exceeds what investors expected, and those growth expectations are embodied in the price-to-earnings, or P/E ratio." — Source: [Knowledge at Wharton]

- On Paying Too Much: "In their enthusiasm to embrace the new, investors invariably pay too high a price for a piece of the action and are doomed to suffer poor returns." — Source: [Cambridge University Press]

- On the Tried and True: "Avoiding the growth trap and sticking with the tried and true has served investors very well in the past." — Source: [Knowledge at Wharton]

- On Buying at Valuations: "Although those who wait long enough will eventually recoup losses on a diversified portfolio of stocks, buying stocks at or below their historical valuation is the best way to guarantee superior returns." — Source: [Goodreads]

- On IBM vs. Standard Oil: "Despite IBM's superior growth in sales and earnings, Standard Oil provided better long-term returns to investors because it was purchased at a much more reasonable price." — Source: [Oblivious Investor]

- On Price Importance: "Price is a very important variable in buying stocks. Not how fast the earnings are growing, but how fast they are growing relative to the P/E ratio." — Source: [Financial Wisdom Forum]

- On IPOs: "There is no question that the losing IPOs far outnumber the winners." — Source: [Goodreads]

Part 3: Dividend Yields & Reinvestment

- On Reinvesting Dividends: "97% of the total after-inflation accumulation from stocks comes from reinvesting dividends. Only 3% comes from capital gains." — Source: [The Motley Fool]

- On Underpriced Firms: "Profitable firms that do not catch investors' eyes are often underpriced. If investors reinvest the dividends of such firms, they are buying undervalued shares that will add significantly to their return." — Source: [Goodreads]

- On Bear Market Protectors: "Dividends act as a bear-market protector by providing a cushion in down markets, easing the psychological pain of holding equities." — Source: [Heartland Advisors]

- On Return Accelerators: "Reinvesting dividends during market downturns allows investors to purchase more shares at lower prices, acting as a return accelerator when the market recovers." — Source: [The Motley Fool]

- On Objective Measures: "Dividends offer a more objective and unambiguous measure of a company’s health and profitability than stock prices, which can be easily skewed by market sentiment." — Source: [WisdomTree]

- On Fundamental Indexing: "Market-capitalization weighting forces investors to hold stocks that have become overpriced due to speculation, making fundamental indexing based on dividends a superior approach." — Source: [Advisor Perspectives]

- On Valuation Anomalies: "Over time, portfolios of stocks with higher dividend yields and lower P-E ratios have outperformed the market more than would be predicted by the efficient markets hypothesis or the capital asset pricing model." — Source: [Simply Investing]

- On Dividend Value: "Tilt your portfolio toward value by buying passive indexed portfolios of value stocks or fundamentally weighted index funds." — Source: [Goodreads]

- On the Reinvestment Engine: "Dividends are the primary engine for long-term wealth accumulation, providing a consistent mechanism for compounding capital over time." — Source: [Business Insider]

Part 4: Inflation & Real Assets

- On Stocks as Real Assets: "The good thing about the dividend-paying stocks is, first of all you have stocks, which are real assets if we have some inflation." — Source: [AZQuotes]

- On Pricing Power: "Corporations do well with moderate inflation. It gives them pricing power. Their assets move up with prices. I'm not fearful of that inflation." — Source: [AZQuotes]

- On the Inflation Sweet Spot: "An inflation rate of 2% to 4% is a sweet spot for stocks because companies can easily adjust their prices to pass costs onto consumers." — Source: [AZQuotes]

- On Bond Vulnerability: "Bonds are deeply vulnerable to the erosive effects of inflation, making them a poor choice for protecting purchasing power over long horizons." — Source: [Efficient Frontier]

- On Real vs. Nominal Yields: "Investors commonly make a valuation error by comparing equity earnings yields directly to nominal Treasury bond yields instead of looking at real returns via TIPS." — Source: [WisdomTree]

- On Post-Pandemic Inflation: "The massive increase in money supply following the COVID-19 pandemic made subsequent high inflation virtually inevitable, despite central bank claims that it was transitory." — Source: [CNBC]

- On Supply Shocks: "Upward pressure on inflation due to geopolitical conflicts and oil price spikes should ideally be looked through by the Federal Reserve rather than reacting with immediate rate hikes." — Source: [Business Insider]

- On Gold's Hedging Limitations: "While gold may serve as a hedge during specific inflationary periods, its long-term real return fails to keep pace with the wealth generation of equities." — Source: [WisdomTree]

- On Protecting Wealth: "Investors worried about inflation should avoid shifting heavily into bonds, as equities ultimately provide the most robust defense against a depreciating currency." — Source: [CNBC]

Part 5: Market Timing & Active Management

- On Playing Hunches: "Hindsight plays tricks on our minds... often distorts the past and encourages us to play hunches and outguess other investors, who in turn are playing the same game." — Source: [AZQuotes]

- On Beating the Market: "For most of us, trying to beat the market leads to disastrous results... our actions lead to much lower returns than can be achieved by just staying in the market." — Source: [AZQuotes]

- On Indexing Superiority: "It is interesting that an investor who has some knowledge of the principles of equity valuations often performs worse than someone with no knowledge who decides to index his portfolio." — Source: [Goodreads]

- On Portfolio Diversification: "It can be shown that maximum diversification is achieved by holding each stock in proportion to its value to the entire market." — Source: [AZQuotes]

- On Staying Invested: "Attempting to jump in and out of the market based on macroeconomic news usually results in missing the market's best performing days, severely crippling long-term returns." — Source: [Knowledge at Wharton]

- On Global Exposure: "Investors should allocate their stock portfolios according to a country's share of world equity values, utilizing low-cost indexed funds to own a wide assortment of international stocks." — Source: [Knowledge at Wharton]

- On Active Management Costs: "The fees associated with active management compound negatively over time, creating a significant hurdle that most fund managers fail to overcome compared to simple index funds." — Source: [Livemint]

- On Sector Rotation: "Sector rotation out of high-flying megacaps into cyclical and value-oriented stocks is a sign of a healthier, broadening bull market rather than a warning of collapse." — Source: [WisdomTree]

- On Following the Herd: "Investors who fail to control their emotions and instead chase trends or flee during downturns often significantly underperform the broader market." — Source: [Thornburg Investment Management]

- On Core Strategy: "Low-cost index funds should serve as the foundational core for the vast majority of investors' portfolios, avoiding the temptation to trade actively." — Source: [Knowledge at Wharton]

Part 6: Demographics, Technology, & Innovation

- On the Aging Population: "The aging of the global population is the most critical long-term economic issue facing the developed world, necessitating a reliance on emerging markets to absorb assets." — Source: [Knowledge at Wharton]

- On the Role of the Developing World: "In a future of shrinking developed workforces, the global economy will increasingly rely on a younger world to produce goods, provide labor, and fund retirement needs." — Source: [Library of Economics and Liberty]

- On Technology and Productivity: "Technology, while a significant factor in productivity, must be managed carefully. Excessive investment can hinder profit growth and destroy shareholder value." — Source: [Bookey]

- On Navigating Labor Shortages: "Firms are increasingly leaning into technological innovation and process efficiency as a necessary countermeasure to persistent global labor shortages." — Source: [Stocktwits]

- On Macro Forces: "There's technology, there's globalization, and there's demographics. All of those point to... lower real-rates and some lower inflation." — Source: [Meb Faber Research]

- On Artificial Intelligence: "The biggest risk on AI investing is that it can be done much more cheaply, suggesting that the cost of technology deployment could disrupt current high-margin expectations." — Source: [CNBC]

- On Technological Bubbles: "Investors should be careful not to label every new technological advancement a bubble; true bubbles lack the earnings-backed growth seen in many modern tech leaders." — Source: [Advisor Perspectives]

- On Innovation and Returns: "While innovation drives the economy forward, the most innovative companies are often priced too perfectly, meaning the ultimate financial rewards flow to consumers rather than early investors." — Source: [Blogspot]

- On Structural Economic Shifts: "The integration of global markets and rapid technological innovation provides a structural mechanism to successfully navigate the demographic transition of an aging populace." — Source: [World Economic Forum]

Part 7: Investor Psychology & Behavioral Biases

- On the Power of Fear: "Fear incites human action far more urgently than does the impressive weight of historical evidence." — Source: [Of Dollars and Data]

- On Excitement and Overpayment: "Excitement over their prospects often induces investors to pay too high a price, ignoring the fundamental mathematics of long-term compounding." — Source: [Goodreads]

- On Market Normalcy: "What feels like unprecedented and terrifying market volatility in the moment is frequently just a normal part of long-term historical market cycles." — Source: [A Wealth of Common Sense]

- On Self-Exploration: "The stock market is an incredibly costly place for individuals to discover their true risk tolerance and emotional limitations." — Source: [Futu]

- On Quality as Protection: "The best protection against volatility is long-term ownership of high-quality stocks, shielding investors from the urge to panic sell during corrections." — Source: [Hubfinance]

- On Short-term Thinking: "Human psychology naturally overweights recent events, causing investors to inappropriately project short-term crises into permanent, structural market declines." — Source: [Vermillion Private Wealth]

- On Loss Aversion: "The psychological pain of market declines frequently overwhelms logic, pushing investors to abandon well-constructed financial plans at the worst possible times." — Source: [Rational Reminder]

- On Bear Market Certainty: "I don't know when we'll see the next bear market. But like you, I know it's coming... it's not a matter of 'if,' but 'when.'" — Source: [The Motley Fool]

- On Patience: "Holding steady during temporary market corrections, which typically drop 5% to 10%, is a psychological requirement for securing long-term equity returns." — Source: [World Economic Forum]

Part 8: The Federal Reserve & Monetary Policy

- On Fed Mistakes: "The Fed is making the same mistake it made a year ago, and possibly the biggest mistake in its history... It makes absolutely no sense to me whatsoever, way too tight." — Source: [Business Insider]

- On Fed Support: "The good thing is, I think the Fed has our back. They're essentially saying, 'if we do see a slowdown, we will cut.'" — Source: [Stocktwits]

- On Monetary Excess: "I've been angry at the Fed for two years. I mean, the excess of monetary growth in 2020 and 2021 was inexcusable, in my opinion, and it's caused all the inflation." — Source: [Fox Business]

- On Jerome Powell's Pace: "Federal Reserve chair Jerome Powell is far too cautious and far too deliberate... the deliberateness of his thinking is too slow." — Source: [BNN Bloomberg]

- On Market Anticipation: "Investors have become so geared to watching and anticipating Fed policy that the effect of its tightening and easing is already discounted in the market." — Source: [Goodreads]

- On Pre-Priced Policy: "If investors expect the Fed to stabilize the economy, this will be built into stock prices long before the Fed even begins to take its stabilizing actions." — Source: [Goodreads]

- On Lagging Indicators: "The central bank consistently relies on lagging economic indicators, missing real-time data that often shows inflation cooling much earlier than official reports suggest." — Source: [Business Insider]

- On Fiscal Stimulus Interaction: "In an environment characterized by growing money supply and expansive fiscal stimulus, the Federal Reserve has very little actual room to safely cut interest rates." — Source: [TheStreet]

- On Central Bank Resilience: "The sheer size of central bank balance sheets and their willingness to inject liquidity have fundamentally altered the mechanics of traditional market recessions." — Source: [CNBC]

- On Economic Surprises: "Despite restrictive monetary policy and high interest rates, the U.S. economy has repeatedly demonstrated remarkable resilience through sustained labor market strength." — Source: [WisdomTree]