Joelle Kayden launched Accolade Partners in 2000, steering the venture capital fund-of-funds through the dot-com crash immediately after its inception. She is known for her strict manager selection process and early, consistent financial backing of diverse investment teams. This profile outlines her approach to portfolio construction, evaluating firm culture, and the changing responsibilities of limited partners.

Part 1: The Foundation: Investment Philosophy & Manager Selection

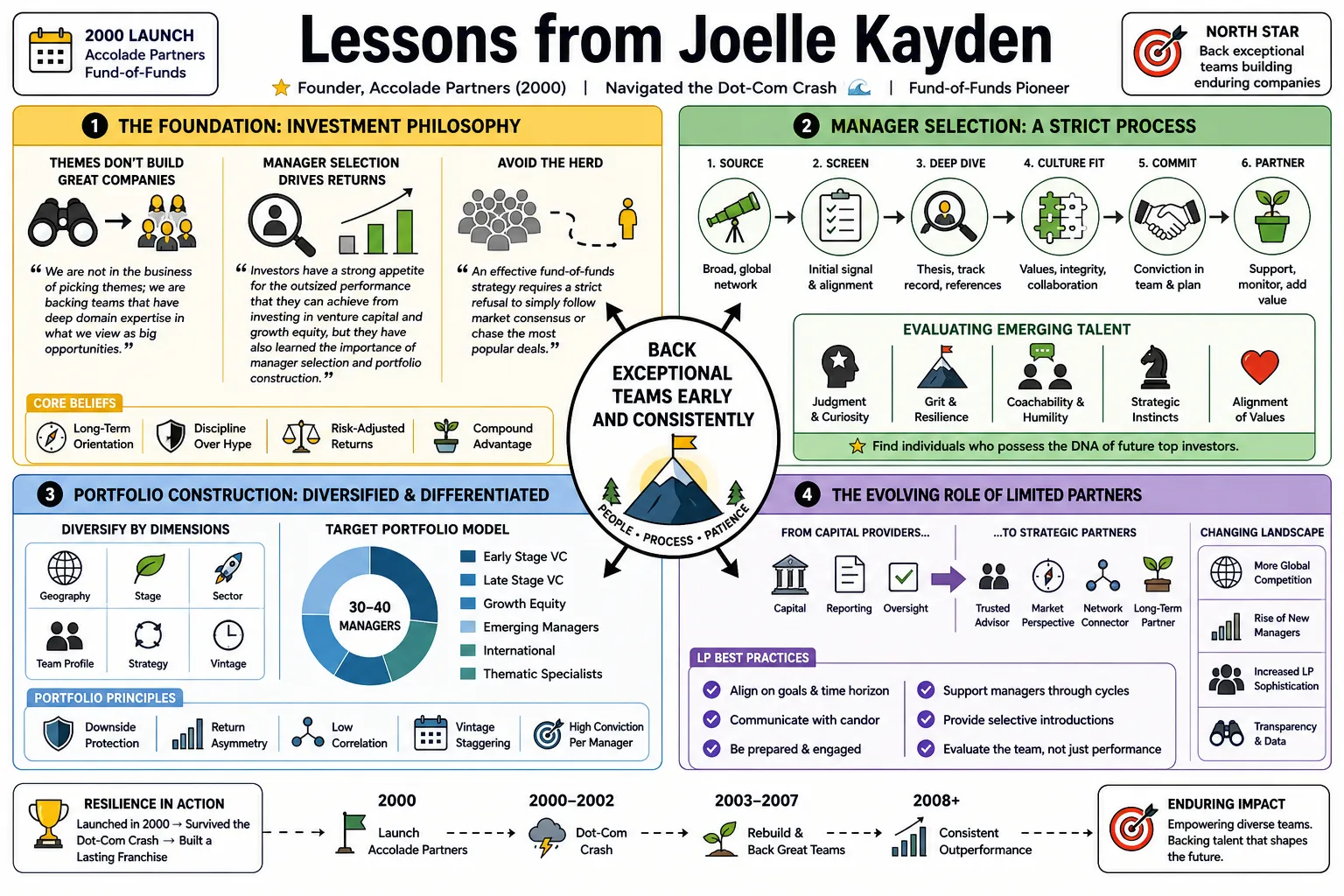

- On picking themes vs. teams: "We are not in the business of picking themes; we are backing teams that have deep domain expertise in what we view as big opportunities." — Source: [Accolade Partners]

- On manager selection: "Investors have a strong appetite for the outsized performance that they can achieve from investing in venture capital and growth equity, but they have also learned the importance of manager selection and portfolio construction." — Source: [Accolade Partners]

- On avoiding the herd: An effective fund-of-funds strategy requires a strict refusal to simply follow market consensus or chase the most popular deals. — Source: [Capital Allocators]

- On evaluating emerging talent: Identifying the next generation of top investors requires finding individuals who possess both technical acumen and the determination needed to build a firm that lasts. — Source: [Accolade Partners]

- On domain expertise: Deep, highly specific knowledge in a sector is a better predictor of venture success than broad macroeconomic thesis building. — Source: [Capital Allocators]

- On portfolio construction: Successful venture investing at the LP level requires rigorous diligence combined with superior access to the asset class's most constrained capacity. — Source: [Accolade Partners]

- On the ways to win: Venture capital returns are driven by a specific set of distinct advantages, typically access, network, technical knowledge, or speed. — Source: [Capital Allocators]

- On identifying outliers: The goal is not to index the venture market, but to consistently identify and gain allocation in the top decile of managers who drive the majority of the industry's returns. — Source: [Origins Podcast]

- On sizing bets: Conviction must be reflected in allocation size; if a team has the necessary domain expertise and drive, an LP must back them meaningfully. — Source: [Capital Allocators]

- On long-term alignment: Manager selection is ultimately about finding partners whose time horizons and incentives perfectly align with the LP's mandate. — Source: [Origins Podcast]

Part 2: Navigating the Dot-Com Crash & Market Cycles

- On launching during a bubble: Starting a fund-of-funds in 2000 meant immediately facing a massive market correction, which forged a permanent discipline regarding valuation and capital deployment. — Source: [Capital Allocators]

- On surviving the nuclear winter: The post-2000 venture environment required extreme patience and a willingness to stand by managers when the broader market had abandoned the asset class. — Source: [Origins Podcast]

- On funding discipline: In challenging economic environments, the best venture capitalists tighten their checkbooks and focus strictly on fundamentals rather than growth at any cost. — Source: [Capital Allocators]

- On public market selloffs: When public equities decline sharply, the venture market eventually recalibrates, requiring LPs to assess which GPs are holding onto unrealistic valuations. — Source: [Capital Allocators]

- On dry powder: Having uncalled capital during a downturn is an advantage, provided the manager has the courage to deploy it when others are fearful. — Source: [Capital Allocators]

- On learning from history: The dot-com crash taught that paper returns are meaningless until liquidity is achieved, a lesson that applies equally to modern tech cycles. — Source: [McKinsey]

- On market exuberance: Rapidly escalating valuations and compressed diligence periods are clear indicators that an LP needs to heavily scrutinize a GP's discipline. — Source: [Capital Allocators]

- On vintage year diversification: Because it is impossible to perfectly time the market bottom, consistent deployment across multiple vintage years is the only reliable way to capture upside. — Source: [Origins Podcast]

- On the resilience of tech: Despite severe cyclical downturns, the underlying trend of technological innovation creating value has remained a constant force over decades. — Source: [Origins Podcast]

- On GP survival skills: The most revealing test of a venture capitalist is not how they invest during a bull market, but how they manage their portfolio companies through a recession. — Source: [Capital Allocators]

Part 3: The Imperative of Diversity in Venture

- On the intuition for diversity: "Intuitively, we expect diverse managers to back more diverse teams. We have seen diverse managers in our portfolio leverage their diverse networks to find differentiated deal flow, which can give them an edge." — Source: [Forbes]

- On edge through network: Diverse fund managers possess unique professional networks that grant them access to founders who might otherwise be overlooked by traditional VC hubs. — Source: [Forbes]

- On structural barriers: The venture capital industry has historically suffered from insularity; breaking those barriers is necessary for finding the best returns. — Source: [McKinsey]

- On women in venture: Increasing the number of female General Partners is necessary because they frequently spot market opportunities in sectors that male investors ignore. — Source: [McKinsey]

- On capital allocation as power: The most direct way to change the demographics of startup founders is to change the demographics of the people writing the checks. — Source: [Forbes]

- On diverse deal flow: A homogeneous partnership will invariably see a homogeneous pipeline of deals; diversity at the partnership level is a prerequisite for a truly broad funnel. — Source: [Forbes]

- On bias in pattern matching: Venture capital relies heavily on pattern recognition, but if the historical pattern is flawed or exclusionary, investors will miss the next generation of massive companies. — Source: [Forbes]

- On LPs driving change: Limited Partners hold the purse strings and therefore have both the ability and the responsibility to demand better diversity metrics from the funds they back. — Source: [McKinsey]

- On performance and inclusion: Backing managers from underrepresented backgrounds is a deliberate strategy to find alpha in less crowded spaces. — Source: [Forbes]

- On the future of the industry: The venture firms that will dominate the next two decades will look fundamentally different from the partnerships that dominated the 1990s. — Source: [McKinsey]

Part 4: Assessing Team Culture & Dynamics

- On internal fund dynamics: A venture firm's culture is essential to its long-term survival and ability to back founders effectively. — Source: [Capital Allocators]

- On assessing partnership health: Diligence must extend beyond spreadsheets to understand how a partnership resolves conflicts and shares economics. — Source: [Capital Allocators]

- On succession planning: The failure of older generations of GPs to properly transition power and economics to younger partners is a primary cause of firm mortality. — Source: [Origins Podcast]

- On ego in investing: Venture capital attracts high egos, but the most successful partnerships have mechanisms to ensure that the best idea wins, regardless of who sponsored the deal. — Source: [Capital Allocators]

- On generational handoffs: Observing how a firm promotes its principals and handles its first major generational transition is the ultimate test of its institutional durability. — Source: [Origins Podcast]

- On solo GPs vs. teams: While solo capitalists can be highly effective, scaling a firm requires building a complementary team where distinct skill sets cover each other's blind spots. — Source: [Origins Podcast]

- On attribution: It is essential for an LP to dig into track records and determine who actually sourced, worked with, and exited a successful company, rather than accepting firm-wide attribution. — Source: [Capital Allocators]

- On alignment of interest: The way a firm distributes its carried interest is the truest reflection of its internal culture and values. — Source: [Origins Podcast]

- On institutionalizing success: A firm only moves from being a collection of good investors to a lasting institution when it creates repeatable processes for sourcing and supporting founders. — Source: [Capital Allocators]

Part 5: The Role of the Limited Partner (LP)

- On the LP value-add: A good fund-of-funds provides capital alongside market intelligence and a sounding board for GPs facing strategic decisions. — Source: [Capital Allocators]

- On re-upping decisions: The decision to invest in a GP's next fund should never be automatic; it requires re-underwriting the team based on their current hunger and market position. — Source: [Capital Allocators]

- On LP and GP communication: The best GPs communicate bad news quickly and transparently; obfuscation is the fastest way to lose an LP's trust. — Source: [Origins Podcast]

- On navigating advisory boards: Serving on an LPAC requires balancing the protective interests of the LP base with giving the GP the necessary latitude to execute their strategy. — Source: [Capital Allocators]

- On concentration: A high-performing LP portfolio requires concentrating capital in the highest conviction managers rather than spreading small checks across too many funds. — Source: [Origins Podcast]

- On reference checking: The most valuable reference calls are not the ones provided by the GP, but the off-list conversations with founders whose companies failed. — Source: [Capital Allocators]

- On fund size discipline: When a GP drastically increases their fund size without a corresponding change in strategy, it often signals a shift from generating returns to accumulating management fees. — Source: [Capital Allocators]

- On patience: Because venture capital has a multi-decade feedback loop, LPs must develop the stomach to endure early drawdowns without losing faith in the underlying managers. — Source: [Origins Podcast]

- On being a trusted partner: In highly competitive allocations, a GP will choose an LP who has proven they will remain steady and supportive during macroeconomic turbulence. — Source: [Origins Podcast]

Part 6: Blockchain, Crypto, & The Tech Frontier

- On crypto market downturns: Navigating the volatility of digital assets requires a tactical approach; funds have succeeded by aggressively pursuing early stablecoin investments and staking strategies. — Source: [The Economic Times]

- On tactical token management: In the blockchain space, venture funds must possess the specific capability to actively manage and selectively buy or sell tokens, which is fundamentally different from holding equity. — Source: [The Economic Times]

- On assessing frontier tech: Evaluating managers in nascent sectors like AI or crypto means looking for intense technical fluency rather than an ability to speak to high-level market trends. — Source: [Accolade Partners]

- On regulatory risk: Investing in web3 and crypto requires managers who deeply understand and can navigate the evolving regulatory environment alongside the underlying code. — Source: [The Economic Times]

- On specialized vs. generalist funds: In highly complex new sectors, specialized funds with dedicated infrastructure often have a significant edge over generalist funds trying to dabble in the space. — Source: [Accolade Partners]

- On the velocity of innovation: The pace of development in AI and blockchain forces LPs to continually refresh their own knowledge base to properly assess whether a GP's thesis remains relevant. — Source: [Accolade Partners]

- On technological paradigm shifts: Major shifts like the internet, mobile, and AI follow similar patterns of initial skepticism, market corrections, and eventual foundational value creation. — Source: [Origins Podcast]

- On technical diligence: Managers investing in deep tech must have the ability to evaluate the actual underlying architecture of a product rather than relying on the founder's pitch deck. — Source: [Accolade Partners]

- On identifying persistent value: The challenge in frontier tech is separating the teams building infrastructure that will endure multiple cycles from those merely capitalizing on short-term retail excitement. — Source: [The Economic Times]

Part 7: Career Transitions: From Banking to LP

- On the value of banking experience: Spending nearly two decades in technology investment banking provided an invaluable view of how companies are capitalized and eventually taken public. — Source: [Capital Allocators]

- On inside access: Being the first CFO of ABS Ventures allowed for an intimate understanding of venture fund mechanics and partnership structures before ever becoming an LP. — Source: [Origins Podcast]

- On shifting perspectives: Moving from banking to fund-of-funds requires shifting from a transactional mindset to a deeply relational, multi-decade time horizon. — Source: [Capital Allocators]

- On the unexpected path: Careers in finance are rarely linear; entering the industry often comes down to seizing an unexpected opportunity and quickly mastering the domain. — Source: [McKinsey]

- On building a network: The relationships forged during the early days of tech banking in the 1980s and 1990s became the foundational network for sourcing top-tier venture access later on. — Source: [Origins Podcast]

- On assessing risk: Investment banking teaches the strict financial mechanics of risk, but venture capital requires learning to evaluate the unquantifiable risk of early-stage team execution. — Source: [Capital Allocators]

- On solo founding: Launching a firm as a solo founder requires immense conviction and a willingness to personally bear the operational and financial burden of the early years. — Source: [Origins Podcast]

- On the evolution of finance: Watching the tech industry mature from niche hardware components to global software infrastructure provided a blueprint for how to spot the next massive wave. — Source: [Origins Podcast]

- On career endurance: Surviving in finance for multiple decades requires an ability to constantly adapt to new market realities while maintaining core investment principles. — Source: [McKinsey]

Part 8: Building Accolade Partners

- On initial vision: Accolade was built on the premise that specialized, boutique access to venture capital would consistently outperform broad, generalized asset management approaches. — Source: [Accolade Partners]

- On firm scaling: Growing a fund-of-funds means deliberately expanding the team's expertise to cover new sectors without diluting the firm's central investment philosophy. — Source: [Capital Allocators]

- On maintaining access: Sustaining a top-tier venture portfolio requires constantly proving value to oversubscribed GPs who do not strictly need your capital. — Source: [Origins Podcast]

- On independent thinking: A successful firm culture must fiercely protect independent thought and require team members to defend their convictions against internal pushback. — Source: [Capital Allocators]

- On generational firm building: The ultimate goal of building Accolade has been to create an institution that outlives its founders by establishing a culture of rigorous, repeatable diligence. — Source: [Origins Podcast]

- On adapting to size: As a firm's assets under management grow, it must resist the temptation to drift into larger, safer bets that historically yield lower multiples. — Source: [Capital Allocators]

- On LP base construction: Just as GPs select their LPs, a fund-of-funds must carefully select its own investors to ensure they possess the necessary patience for venture timelines. — Source: [Origins Podcast]

- On organizational focus: Accolade's enduring edge relies on remaining hyper-focused on its core mandate of finding and backing exceptional tech and healthcare managers. — Source: [Accolade Partners]

- On legacy: The mark of a successful venture career is the returns generated as well as the broader ecosystem of diverse, high-performing funds that were empowered to exist. — Source: [McKinsey]