Lessons from John Armitage

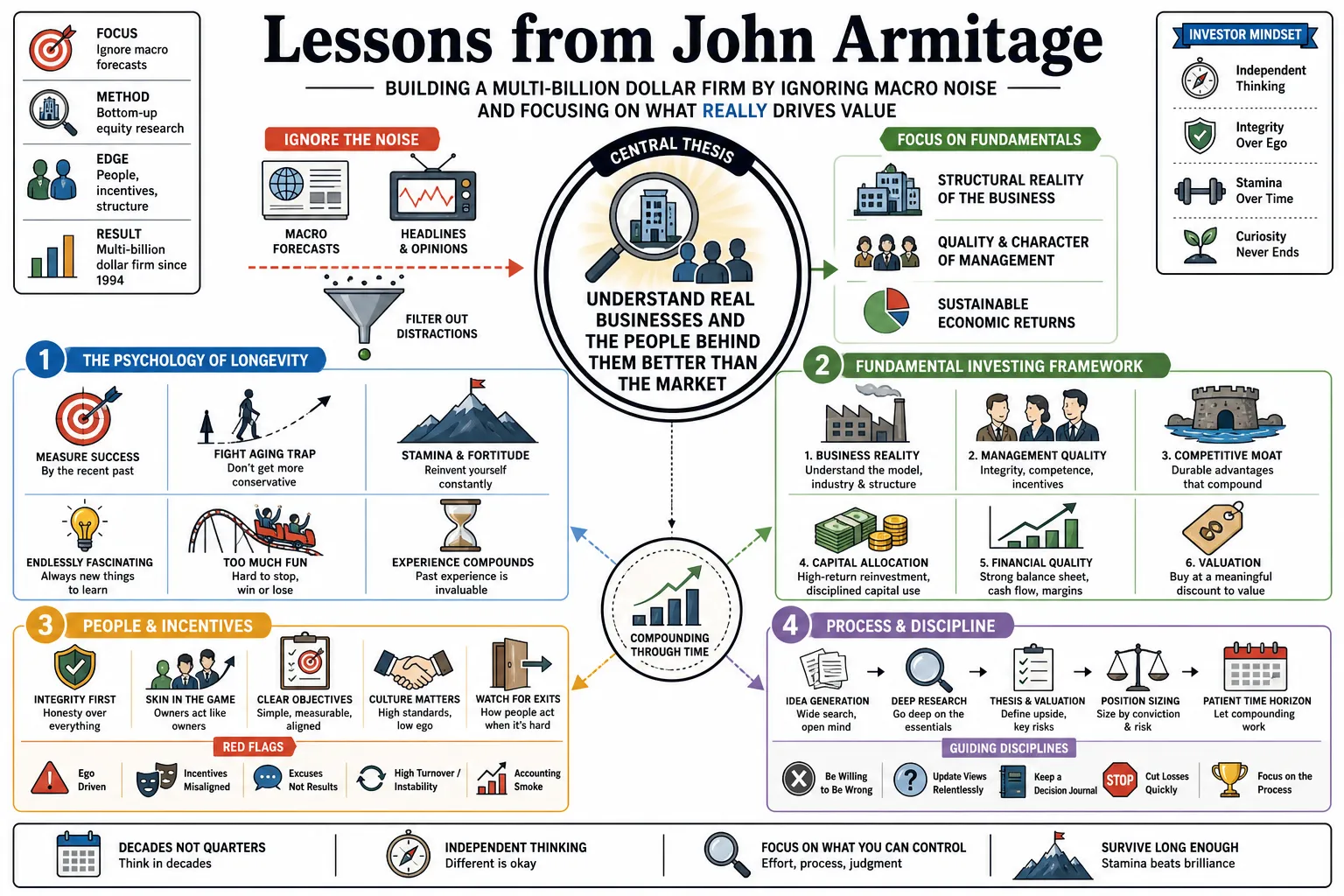

Since co-founding Egerton Capital in 1994, British hedge fund manager John Armitage has built a multi-billion dollar firm by ignoring macroeconomic forecasts and sticking to strict bottom-up equity research. He prefers to analyze the structural realities of individual companies and the character of the people running them. This profile collects his lessons on fundamental investing, from judging executive integrity to finding the stamina to survive decades in public markets.

Part 1: The Psychology of Longevity

- On measuring success: "I like working. I never feel successful. I measure success by the recent past." — Source: [Behind the Balance Sheet]

- On the danger of aging: "You have to fight against the natural tendency to get more conservative as you get older." — Source: [Schroders]

- On stamina: "You have to have a lot of fortitude, a lot of stamina, you have to constantly try and reinvent yourself." — Source: [Schroders]

- On staying motivated: "Firstly, investing is endlessly fascinating and there are always new things to learn." — Source: [Schroders]

- On the trap of retiring: "If you’re doing badly you feel you can’t go out on a low while if you’re doing well it’s too much fun to stop." — Source: [Schroders]

- On past experience: "Experience is useful, but it's not always useful." — Source: [Behind the Balance Sheet]

- On continuous effort: "It’s quite remarkable that the more I practice, the luckier I get... You need to work hard, but you also need to catch a zeitgeist at certain times." — Source: [Behind the Balance Sheet]

- On annual resets: "Treating every year as a clean start prevents portfolio managers from becoming overly attached to historical winners." — Source: [Egerton Capital]

- On emotional resilience: "The market will repeatedly test your convictions, requiring an emotional baseline that remains steady despite daily price movements." — Source: [Invest for Kids Chicago]

Part 2: Assessing Management and Culture

- On core executive traits: "The most important qualities in a management team are focus, integrity, and an ability to admit mistakes." — Source: [Behind the Balance Sheet]

- On organizational alignment: "Look for companies with a common culture, where the quality and consistency of answers provided by employees at all levels reflect a shared objective." — Source: [Behind the Balance Sheet]

- On admitting errors: "Leaders who conceal early mistakes inevitably compound them; those who admit them quickly can correct course without destroying capital." — Source: [Schroders]

- On financial discipline: "The best management teams maintain low-cost operations and a strong balance sheet to navigate debt effectively, even in cyclical industries." — Source: [Invest for Kids Chicago]

- On evaluating talent: "Spotting exceptional executives requires looking beyond their charisma and evaluating the competence of the people they choose to surround themselves with." — Source: [Behind the Balance Sheet]

- On corporate identity: "A unified corporate identity, where cost discipline is understood by every employee from the front line to the boardroom, offers a massive advantage." — Source: [Egerton Capital]

- On executive focus: "Management teams that chase multiple unrelated strategic initiatives rarely succeed; exceptional leaders strip away distractions." — Source: [Behind the Balance Sheet]

- On corporate humility: "The moment a management team believes they have permanently solved their industry's challenges is usually the moment they begin to lose market share." — Source: [Schroders]

- On consistent messaging: "When middle management gives the exact same strategic answers as the CEO, you have found a company with genuine operational clarity." — Source: [Egerton Capital]

Part 3: The Primacy of Bottom-Up Analysis

- On analytical edge: "An investor's edge comes from understanding individual businesses better than the market, rather than attempting to predict macroeconomic trends." — Source: [Behind the Balance Sheet]

- On ignoring macro noise: "Time spent trying to forecast interest rates or GDP growth is usually time taken away from understanding business fundamentals and barriers to entry." — Source: [Invest for Kids Chicago]

- On structural tailwinds: "The best long-term investments are found in companies that benefit from inevitable industry shifts, rather than those relying on short-term cyclical bounces." — Source: [Egerton Capital]

- On scalability: "A business model must be inherently scalable to warrant a long-term position; fixed costs must decline as a percentage of revenue as the company grows." — Source: [Schroders]

- On forensic research: "Deep analysis of a company's financial statements often reveals realities that the management's investor relations presentations attempt to obscure." — Source: [Behind the Balance Sheet]

- On avoiding hype: "Investment strategies built on identifying the next big trend frequently underperform those built on analyzing sustainable cash flows." — Source: [Schroders]

- On competitive moats: "A high return on invested capital is only valuable if the company possesses the barriers to entry necessary to defend it against new entrants." — Source: [Egerton Capital]

- On capital allocation: "How a company spends its free cash flow is the most reliable indicator of management's true priorities and competence." — Source: [Invest for Kids Chicago]

- On empirical evidence: "Theoretical models of how a business should perform must always yield to the empirical reality of how it is actually generating revenue." — Source: [Behind the Balance Sheet]

- On deep specialization: "Generalist knowledge is insufficient; analysts must understand the granular details of their specific sectors better than the competitors trading against them." — Source: [Egerton Capital]

Part 4: Cultivating a High-Performance Firm

- On firm structure: "Egerton operates as a benevolent autocracy, ensuring clear accountability while maintaining a highly collaborative research environment." — Source: [Schroders]

- On collegiate debate: "Research should be debated openly and vigorously among analysts, but the final portfolio decision must rest with a single, accountable individual." — Source: [Behind the Balance Sheet]

- On avoiding groupthink: "Investment committees often dilute high-conviction ideas into mediocre consensus trades; centralized decision-making preserves the advantage of dissenting views." — Source: [Schroders]

- On retaining talent: "A firm maintains its edge by continually challenging its analysts and providing them with the resources to pursue endlessly fascinating research questions." — Source: [Behind the Balance Sheet]

- On structural stability: "Independent, partner-owned investment firms align the long-term interests of the managers directly with the long-term returns of the clients." — Source: [Egerton Capital]

- On intellectual honesty: "A high-performance culture requires individuals to publicly update their views when presented with new evidence that contradicts their initial thesis." — Source: [Invest for Kids Chicago]

- On limiting distractions: "Keeping a low public profile allows the investment team to focus entirely on analyzing businesses rather than managing media narratives." — Source: [Behind the Balance Sheet]

- On adapting to change: "The firm must constantly try to reinvent its processes to prevent the organizational decay that accompanies resting on past laurels." — Source: [Schroders]

- On long-term alignment: "True return generation requires a firm structure that protects portfolio managers from the pressure to produce short-term, cosmetic quarterly results." — Source: [Egerton Capital]

Part 5: Portfolio Construction

- On concentration: "Building high-conviction positions in a select few outstanding companies is preferable to holding a diluted basket of mediocre ideas." — Source: [Egerton Capital]

- On benchmark independence: "Active managers should not feel bound by benchmark index weightings; they must have the freedom to deviate significantly to capture real returns." — Source: [Behind the Balance Sheet]

- On liquidity: "Managing significant assets globally requires a strict focus on liquid, large-cap equities to ensure the portfolio can adapt quickly to changing realities." — Source: [Schroders]

- On sizing positions: "The size of an investment should directly correlate with the depth of the analyst's conviction and the asymmetric nature of the risk-reward ratio." — Source: [Behind the Balance Sheet]

- On letting winners run: "A primary mistake investors make is trimming their best ideas too early simply to lock in a profit, cutting off the long tail of compounding returns." — Source: [Egerton Capital]

- On cutting losses: "When the fundamental thesis of an investment is broken, the position must be exited immediately, regardless of the current market price or sunk costs." — Source: [Invest for Kids Chicago]

- On cash as a tool: "Holding cash is a valid active decision when high-quality, reasonably priced opportunities are absent from the market." — Source: [Schroders]

- On avoiding diversification for its own sake: "Adding a twentieth stock to a portfolio that you understand poorly simply to reduce volatility usually increases underlying risk." — Source: [Behind the Balance Sheet]

- On evaluating private vs public: "Public markets offer daily liquidity and transparency, which often outweigh the perceived, yet illiquid, advantages of private market valuations." — Source: [Schroders]

Part 6: Navigating Market Psychology

- On contrarianism: "Achieving market-beating returns requires the willingness to take positions that are temporarily unpopular or misunderstood by the broader financial community." — Source: [Behind the Balance Sheet]

- On market panics: "Periods of high volatility and market distress are usually the best environments to acquire exceptional businesses at discounts to their intrinsic value." — Source: [Invest for Kids Chicago]

- On the danger of consensus: "When every analyst agrees on a stock's trajectory, the current price usually reflects all possible positive outcomes, leaving no margin of safety." — Source: [Egerton Capital]

- On separating price from value: "The daily quotation of a stock is simply a transaction record; it does not change the underlying cash generation capabilities of the business." — Source: [Schroders]

- On narrative violation: "Some of the best investments occur when a company successfully executes a strategy that directly violates the prevailing industry narrative." — Source: [Behind the Balance Sheet]

- On patience: "The gap between analyzing a correct thesis and the market finally recognizing that value can test the resolve of even the most experienced investors." — Source: [Schroders]

- On ignoring the crowd: "An investor must cultivate the intellectual independence to watch peers generate short-term profits in lower-quality assets without feeling the compulsion to join them." — Source: [Egerton Capital]

- On enduring underperformance: "Even the most successful strategies will experience periods of underperformance; abandoning the strategy during these troughs guarantees permanent capital loss." — Source: [Invest for Kids Chicago]

- On the cost of anxiety: "Trading based on macroeconomic anxiety rather than microeconomic reality destroys more portfolios than actual economic recessions." — Source: [Behind the Balance Sheet]

Part 7: The Nuances of Long/Short Equity

- On the purpose of shorting: "Short selling serves a dual purpose: it manages portfolio risk and generates independent returns in flat markets, rather than simply betting against failing companies." — Source: [Egerton Capital]

- On identifying shorts: "The best short candidates are often companies facing structural technological obsolescence rather than merely temporary cyclical headwinds." — Source: [Behind the Balance Sheet]

- On valuation shorts: "Shorting a stock purely because its valuation appears high is dangerous; expensive stocks can remain expensive longer than a fund can remain solvent." — Source: [Schroders]

- On accounting irregularities: "Companies that continuously change their reporting metrics or rely heavily on adjusted earnings are prime candidates for deep forensic short analysis." — Source: [Invest for Kids Chicago]

- On the asymmetry of shorting: "Unlike long positions, the maximum return on a short is one hundred percent, while the potential loss is infinite, requiring significantly tighter risk management." — Source: [Schroders]

- On capital structure: "Highly indebted companies in deteriorating industries offer the clearest catalyst for a successful short position when credit markets eventually tighten." — Source: [Behind the Balance Sheet]

- On management behavior in shorts: "Aggressive insider selling combined with rapid executive turnover is often the final signal that a flawed business model is about to fracture." — Source: [Egerton Capital]

- On shorting frauds: "While fraudulent companies are attractive targets, their management teams are completely unconstrained by reality, making the timing of their collapse highly unpredictable." — Source: [Invest for Kids Chicago]

- On pair trading: "Hedging a high-quality long position with a short position in a low-quality competitor isolates the specific operational returns from broader sector movements." — Source: [Egerton Capital]

- On short-term catalysts: "A successful short thesis requires both a fundamental flaw in the business and a clear upcoming catalyst that will force the market to recognize that flaw." — Source: [Schroders]

Part 8: The Continuous Process of Learning

- On historical context: "A background in history provides a mental framework for understanding that current geopolitical and economic crises are rarely unprecedented." — Source: [Behind the Balance Sheet]

- On intellectual curiosity: "The desire to constantly learn new things is the primary defense against the cognitive decline and rigid thinking that plagues aging investors." — Source: [Schroders]

- On reading widely: "Successful investing requires consuming information far outside of standard financial reports to understand the shifts impacting consumer behavior." — Source: [Invest for Kids Chicago]

- On admitting ignorance: "The most dangerous phrase for an investor is believing they fully understand a complex system; maintaining a healthy sense of doubt prevents catastrophic arrogance." — Source: [Behind the Balance Sheet]

- On evolving frameworks: "The mental models that generated outsized returns in the previous decade must be continuously audited to ensure they still apply to current market conditions." — Source: [Egerton Capital]

- On studying mistakes: "Analyzing why a high-conviction investment failed yields far more educational value than celebrating the outcome of a successful one." — Source: [Behind the Balance Sheet]

- On technological disruption: "Investors must maintain enough technical curiosity to distinguish between genuine paradigm shifts and heavily marketed vaporware." — Source: [Egerton Capital]

- On cross-disciplinary thinking: "Solutions to complex valuation problems are often found by applying logic and frameworks derived from entirely different academic disciplines." — Source: [Schroders]

- On the limits of data: "While quantitative analysis is necessary, the final investment decision often relies on judgments about human behavior and leadership ethics." — Source: [Behind the Balance Sheet]

- On the lifelong journey: "The pursuit of market outperformance is never completed; it requires a permanent state of inquiry and adaptation." — Source: [Schroders]