Lessons from John Cochrane

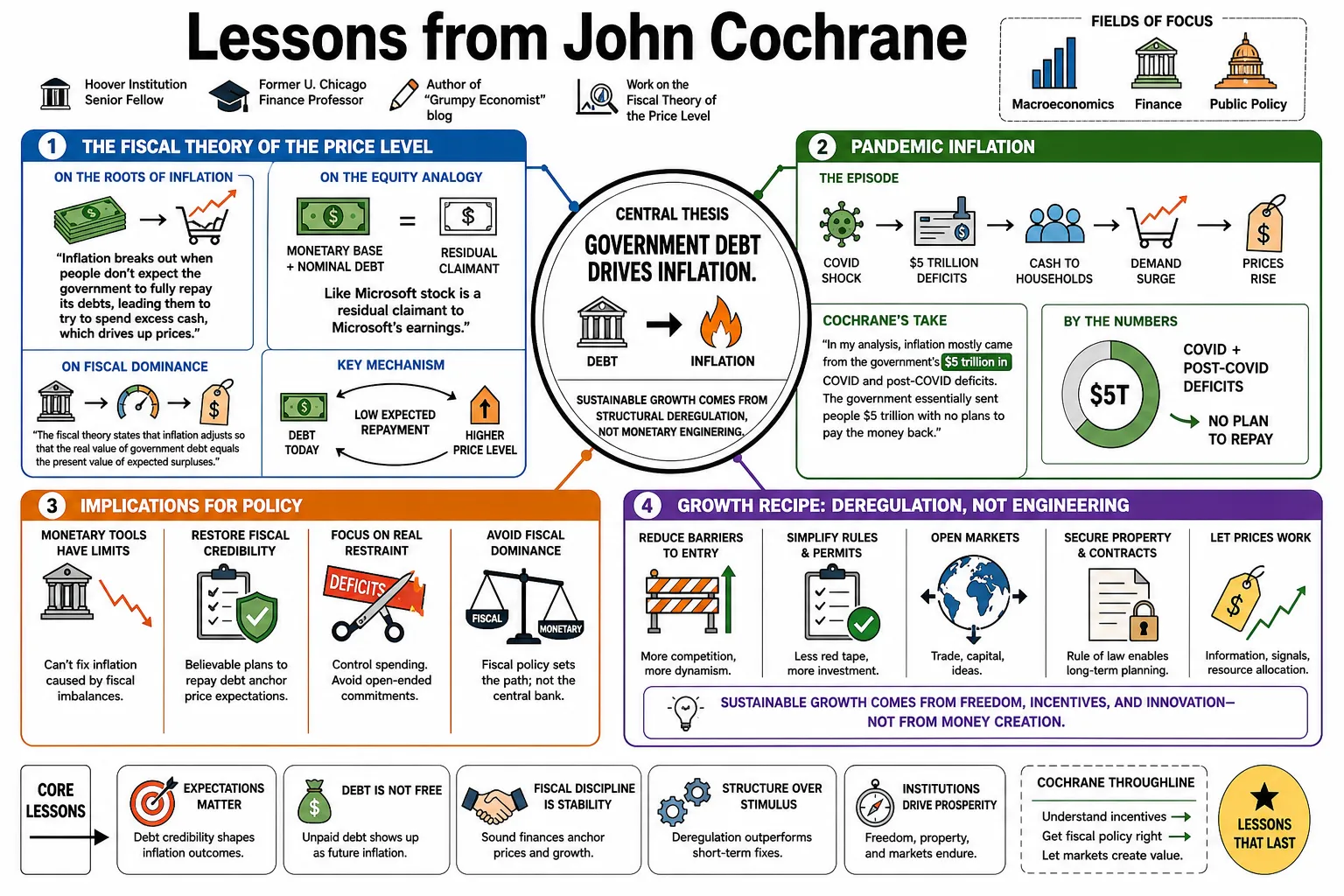

John Cochrane is a Hoover Institution senior fellow, former University of Chicago finance professor, and author of the "Grumpy Economist" blog. Known for his work on the Fiscal Theory of the Price Level, he argues that government debt drives inflation and that economic growth requires structural deregulation rather than monetary engineering. This profile catalogues his arguments across macroeconomics, finance, and public policy.

Part 1: The Fiscal Theory of the Price Level

- On the Roots of Inflation: "Inflation breaks out when people don't expect the government to fully repay its debts, leading them to try to spend excess cash, which drives up prices." — Source: [Hoover Institution]

- On the Equity Analogy: "The monetary base, together with nominal debt, is a residual claimant to government surpluses, just as Microsoft stock is a residual claimant to Microsoft's earnings." — Source: [The Fiscal Theory of the Price Level]

- On Pandemic Inflation: "In my analysis, inflation mostly came from the government's $5 trillion in COVID and post-COVID deficits. The government essentially sent people $5 trillion with no plans to pay the money back." — Source: [The Grumpy Economist]

- On Fiscal Dominance: "The fiscal theory states that inflation adjusts so that the real value of government debt equals the present value of primary surpluses." — Source: [The Fiscal Theory of the Price Level]

- On Money's Value: "Money is valuable because we need money to pay taxes. If, on average, people have more money than they need to pay taxes, they try to buy things, driving up prices." — Source: [Uneasy Money Interview]

- On Central Bank Limits: "The Fed is a lot less powerful than people think. If the government continues to run massive, unfunded deficits, the central bank cannot stop inflation simply by manipulating interest rates." — Source: [Capitalisn't Podcast]

- On Self-Correcting Inflation: "The fiscal theory of the price level plus rational expectations says that the inflation will largely go away on its own, without the Fed needing to raise interest rates to 9 percent, so long as there aren't more fiscal shocks." — Source: [Capitalisn't Podcast]

- On Supply Shocks vs. Demand: "Supply shocks change relative prices. General inflation requires an expansion of aggregate demand, which in recent years was fueled entirely by massive fiscal expansion." — Source: [The Grumpy Economist]

- On the Venti Latte Parable: "If we priced a latte in fractions of an Apple share, our theory of the price level would start with the fact that Apple shares equal the present value of future dividends. Government money operates the same way based on future tax surpluses." — Source: [The Grumpy Economist]

- On Debt Sustainability: "A government cannot inflate away its debt if that debt is short-term. When the debt rolls over, investors will demand higher interest rates, neutralizing the inflation tax." — Source: [Hoover Institution Essays]

Part 2: Monetary Policy and the Federal Reserve

- On Quantitative Easing: "Quantitative Easing is essentially the government swapping short-term debt for long-term debt. It is not fundamentally different from the Treasury changing the maturity structure of its debt issuance, and it has minimal real economic effect." — Source: [The Grumpy Economist]

- On Forward Guidance: "Forward guidance relies on the central bank making credible promises about what it will do years in the future, which is something no committee of policymakers can legitimately guarantee." — Source: [The Grumpy Economist]

- On Price-Level Targeting: "A central bank should ideally target a specific price path rather than an inflation rate. If prices fall one year, they should be allowed to rise the next to return to the target path, stabilizing long-term contracts." — Source: [Hoover Institution Policy Papers]

- On Mission Creep: "When central banks expand their mandates into climate change, inequality, or social justice, they risk losing their independence by engaging in highly political capital allocation." — Source: [The Grumpy Economist]

- On the Phillips Curve: "The idea that there is a reliable, exploitable trade-off between inflation and unemployment is one of the most thoroughly debunked concepts in economics, yet policymakers refuse to let it go." — Source: [Rational Reminder Podcast]

- On Real Interest Rates: "The Federal Reserve controls the nominal overnight interest rate, but real interest rates are determined by broader macroeconomic forces, capital supply, and economic growth." — Source: [John Cochrane's Research]

- On Inflation Phobia: "Central banks spent a decade terrified of slight deflation when they should have recognized that mild price declines driven by productivity improvements are a sign of economic health, not a crisis." — Source: [The Grumpy Economist]

- On Central Planning: "Monetary policy often suffers from the fatal conceit of central planning. A committee in Washington cannot optimally set the price of credit for a complex global economy." — Source: [Hoover Institution Essays]

- On the Standard Doctrine: "The standard doctrine assumes the Fed can control inflation entirely through the interest rate lever, completely ignoring the massive elephant in the room: the government's balance sheet." — Source: [The Grumpy Economist]

Part 3: Free Markets and Economic Growth

- On Escaping Debt: "The only reliable, historical way out of massive sovereign debt burdens is sustained economic growth. You cannot simply tax or inflate your way to prosperity." — Source: [GoodFellows Podcast]

- On the Supply Side: "The resurgence of inflation serves as a slap in the face to 2010s-era economic policies, proving that supply-side constraints are much more significant than the demand-side stimulus models acknowledged." — Source: [The Grumpy Economist]

- On Economic Simplification: "We need a Marie Kondo approach to economic policy: go through the regulatory code and throw out everything that does not spark joy or explicitly serve a clear, cost-benefit justified public purpose." — Source: [IEA Interview]

- On Industrial Policy: "Industrial policy is an invitation to crony capitalism. It replaces the harsh but efficient discipline of market profitability with political allocations to well-connected incumbents." — Source: [The Grumpy Economist]

- On Wealth Taxes: "A wealth tax destroys capital formation. If you aggressively tax wealth, you ensure that fewer people will take the risks necessary to build the productive capacity that drives wages and living standards." — Source: [Hoover Institution Profiles]

- On Inequality: "Economic inequality is often a symptom of underlying distortions, like restrictive zoning or failing schools, rather than the root problem of economic stagnation." — Source: [The Grumpy Economist]

- On Property Rights: "The foundation of any thriving market economy is secure property rights and a predictable rule of law. Without them, investment dries up and economies stagnate." — Source: [John Cochrane's Research]

- On Immigration: "Labor market flexibility, including a functional and expansive immigration system, is essential for avoiding labor shortages and sustaining long-term economic growth." — Source: [The Grumpy Economist]

- On Trade Fallacies: "Terms like imbalances, predatory competition, and industrial overcapacity are frequently used as rhetorical cover to justify protectionist government interventions that harm consumers." — Source: [The Grumpy Economist]

- On Economic Dynamism: "An economy needs churn to survive. Protecting dying industries under the guise of stability prevents the reallocation of capital and labor to their most productive uses." — Source: [Hoover Institution Essays]

Part 4: Regulation and the Administrative State

- On Regulatory Friction: "Regulation is the sand in the gears of the American economy. The cumulative weight of rules, permits, and compliance costs prevents us from building infrastructure and innovating." — Source: [The Grumpy Economist]

- On Environmental Reviews: "The National Environmental Policy Act has morphed from a reasonable check into an endless litigation tool that ironically stops green energy projects and modern infrastructure dead in their tracks." — Source: [Hoover Institution Essays]

- On Occupational Licensing: "Occupational licensing often serves no public safety purpose; it is merely a guild system designed to restrict supply, protect incumbents, and drive up prices for consumers." — Source: [The Grumpy Economist]

- On Housing Costs: "The housing affordability crisis is entirely a self-inflicted wound caused by zoning laws, building codes, and local review processes that artificially constrain the supply of new homes." — Source: [The Grumpy Economist]

- On Financial Regulation: "Dodd-Frank and similar complex financial regulations often create the exact systemic risks they aim to prevent by forcing all banks into the same correlated trades and compliance behaviors." — Source: [John Cochrane's Research]

- On Agency Fiat: "We have shifted from a system where Congress writes laws to one where administrative agencies issue vague edicts and enforce them through selective, extra-judicial pressure." — Source: [The Grumpy Economist]

- On Bailouts: "The doctrine of too big to fail institutionalizes moral hazard. If banks know the government will absorb their losses, they will take excessive risks with taxpayer money." — Source: [Hoover Institution Policy Papers]

- On Incumbent Protection: "Complex regulation is a competitive moat for large corporations. They can afford the compliance armies, while small competitors and startups are strangled in the crib." — Source: [EconTalk Podcast]

- On Structural Reform: "We cannot rely on monetary stimulus to cure structural malaise. The long-term health of the economy requires painful, structural deregulation." — Source: [GoodFellows Podcast]

Part 5: Finance, Asset Pricing, and Markets

- On Market Efficiency: "Markets are remarkably efficient, not because investors are perfectly rational, but because finding and exploiting mispricing is incredibly difficult and competitive." — Source: [Asset Pricing (Book)]

- On Return Predictability: "Returns are predictable over long horizons, but this predictability comes from time-varying risk premiums and discount rates, not from exploitable arbitrage opportunities." — Source: [Rational Reminder Podcast]

- On Discount Rates: "Most of the variation in asset prices is driven by changes in discount rates—how much investors demand to be compensated for holding risk—rather than changes in expected cash flows." — Source: [John Cochrane's Research]

- On Active Management: "The vast majority of active management alpha is an illusion. After fees, most active managers fail to beat simple, low-cost index funds." — Source: [Rational Reminder Podcast]

- On Digital Currencies: "Cryptocurrencies function decently as transaction technologies for evading capital controls, but without fiscal backing or a peg, they lack the fundamental anchor required to be a stable store of value." — Source: [The Grumpy Economist]

- On the Equity Premium: "The equity premium puzzle highlights that investors are highly averse to losses during macroeconomic downturns, requiring a massive historical premium to hold stocks." — Source: [Asset Pricing (Book)]

- On Corporate Finance: "In macroeconomics, we often forget the Modigliani-Miller theorem. Whether a firm or a bank finances itself with debt or equity doesn't change its underlying fundamental value, but it deeply affects its fragility." — Source: [Hoover Institution Essays]

- On Shadow Banking: "The danger in the financial system is not banking per se, but the issuance of short-term, run-prone debt by shadow banks to fund long-term, illiquid assets." — Source: [The Grumpy Economist]

- On Equity-Financed Banking: "If banks were funded with 100 percent equity instead of massive leverage, bank runs would be impossible, and the need for complex, heavy-handed financial regulation would evaporate." — Source: [EconTalk Podcast]

Part 6: Healthcare Economics

- On Employer Insurance: "The original sin of American healthcare is employer-sponsored insurance, a historical accident from WWII wage controls that traps workers and destroys consumer choice." — Source: [External Medicine Podcast]

- On Healthcare Costs: "Healthcare is ruinously expensive because it lacks the fundamental drivers of efficiency: transparent pricing and fierce, free-market competition." — Source: [The Grumpy Economist]

- On Hospital Monopolies: "Certificate of Need laws are explicitly designed to create local hospital monopolies by requiring new entrants to prove to a board of incumbents that their competition is needed." — Source: [Hoover Institution Profiles]

- On Supply Suppression: "From restricting the number of medical residencies to banning foreign-trained doctors, the medical industry artificially suppresses the supply of care to maintain high wages." — Source: [External Medicine Podcast]

- On True Insurance: "Health insurance today is mostly prepayment for routine maintenance. True insurance should protect against catastrophic, unpredictable ruin, not cover standard check-ups." — Source: [The Grumpy Economist]

- On Telemedicine: "Regulatory barriers that prevent doctors from practicing across state lines via telemedicine are purely protectionist and severely limit access to specialized care." — Source: [The Grumpy Economist]

- On the FDA: "The FDA's excessively cautious drug approval process costs countless lives by delaying access to life-saving treatments in the name of absolute safety." — Source: [Hoover Institution Essays]

- On Cash-Only Practices: "Cash-only medical practices and direct primary care models demonstrate that when third-party payers are removed, healthcare becomes dramatically cheaper and more patient-focused." — Source: [The Grumpy Economist]

- On Medicare Pricing: "Medicare and Medicaid do not negotiate prices; they dictate price controls, which distorts the entire medical market and forces costs onto private payers." — Source: [Hoover Institution Policy Papers]

- On Unshackling Supply: "The only way to sustainably lower healthcare costs is to radically unshackle the supply side: let nurses do more, let software diagnose, and let new clinics open without permission." — Source: [The Grumpy Economist]

Part 7: Climate Policy and Economic Realities

- On Climate Risk: "Climate change is a manageable economic risk requiring technological adaptation, not an existential crisis that justifies abandoning economic growth and free markets." — Source: [The Grumpy Economist]

- On Financial Mandates: "Using financial regulation and bank stress tests to enforce climate policy is an illegitimate end-run around the democratic legislative process." — Source: [GoodFellows Podcast]

- On Carbon Taxes: "If you want to reduce carbon emissions, a simple, uniform carbon tax is vastly superior to the labyrinth of inefficient subsidies, mandates, and bans currently favored by politicians." — Source: [Hoover Institution Essays]

- On Innovation: "The only mathematically viable solution to global carbon emissions is technological innovation that makes clean energy cheaper than fossil fuels in developing nations." — Source: [The Grumpy Economist]

- On ESG Investing: "ESG investing is largely a politicized marketing gimmick that reduces returns and distracts corporate boards from their primary fiduciary duty of maximizing shareholder value." — Source: [Rational Reminder Podcast]

- On Energy Transitions: "Mandating a rapid transition away from fossil fuels before reliable, scalable baseline alternatives exist guarantees severe economic disruptions and energy poverty." — Source: [The Grumpy Economist]

- On Green Jobs: "The concept of green jobs as an economic stimulus is a broken window fallacy. Forcing the economy to use more labor to produce the same amount of energy makes society poorer, not richer." — Source: [The Grumpy Economist]

- On Stress Tests: "Climate risk stress tests for banks are a masquerade; they are designed not to ensure financial stability, but to starve politically disfavored industries of capital." — Source: [Hoover Institution Policy Papers]

- On Adaptation: "Economic growth is the best defense against climate impacts. A wealthy society can build seawalls, invent new crops, and adapt; a poor society cannot." — Source: [The Grumpy Economist]

Part 8: Fallacies, Narratives, and Methodology

- On Accounting Identities: "A persistent error in macroeconomics is reasoning from an accounting identity—assuming that because two variables must balance, one mechanistically causes the other." — Source: [The Grumpy Economist]

- On Greedflation: "The narrative of greedflation is economic nonsense. Corporations did not suddenly become greedy in 2021; they simply raised prices in response to massive government-induced demand." — Source: [The Grumpy Economist]

- On Economic Rigor: "Good economics requires rigorous, math-based models to check the internal consistency of our logic. Without equations, policy debates devolve into storytelling and political wishful thinking." — Source: [John Cochrane's Research]

- On Micro Foundations: "Macroeconomics must be grounded in sound microeconomic foundations. If a macroeconomic theory assumes people behave in ways they never would in individual markets, the theory is wrong." — Source: [The Fiscal Theory of the Price Level]

- On Trade Imbalances: "The obsession with bilateral trade deficits is fundamentally misplaced; trade is about comparative advantage and capital flows, not a zero-sum scorecard." — Source: [The Grumpy Economist]

- On Macro Forecasting: "Large-scale macroeconomic forecasting is a failed enterprise. The economy is too complex and subject to unpredictable shocks for central banks to fine-tune it based on quarter-ahead predictions." — Source: [Hoover Institution Profiles]

- On Structural vs. Cyclical: "Policymakers constantly misidentify structural supply constraints as temporary cyclical shocks, leading them to apply demand-side stimulus to problems that require deregulation." — Source: [GoodFellows Podcast]

- On Blaming Speculators: "Whenever price controls create shortages, politicians inevitably blame speculators and hoarders rather than admitting their policies destroyed the price mechanism." — Source: [The Grumpy Economist]

- On Economic Skepticism: "The job of an economist is to be grumpy—to point out the hidden costs, the unintended consequences, and the mathematical impossibilities of utopian political promises." — Source: [The Grumpy Economist]