John Zito is the Co-President of Apollo Asset Management, where he helped transition the firm from a traditional private equity model into a principal-investing institution following its merger with Athene. He is known for challenging consensus views on private software valuations and arguing that private credit serves as a safer alternative during periods of macroeconomic volatility. This collection organizes his direct commentary on asset management strategy, the realities of AI disruption, and the mechanics of modern credit markets.

Part 1: The New Era of Private Credit

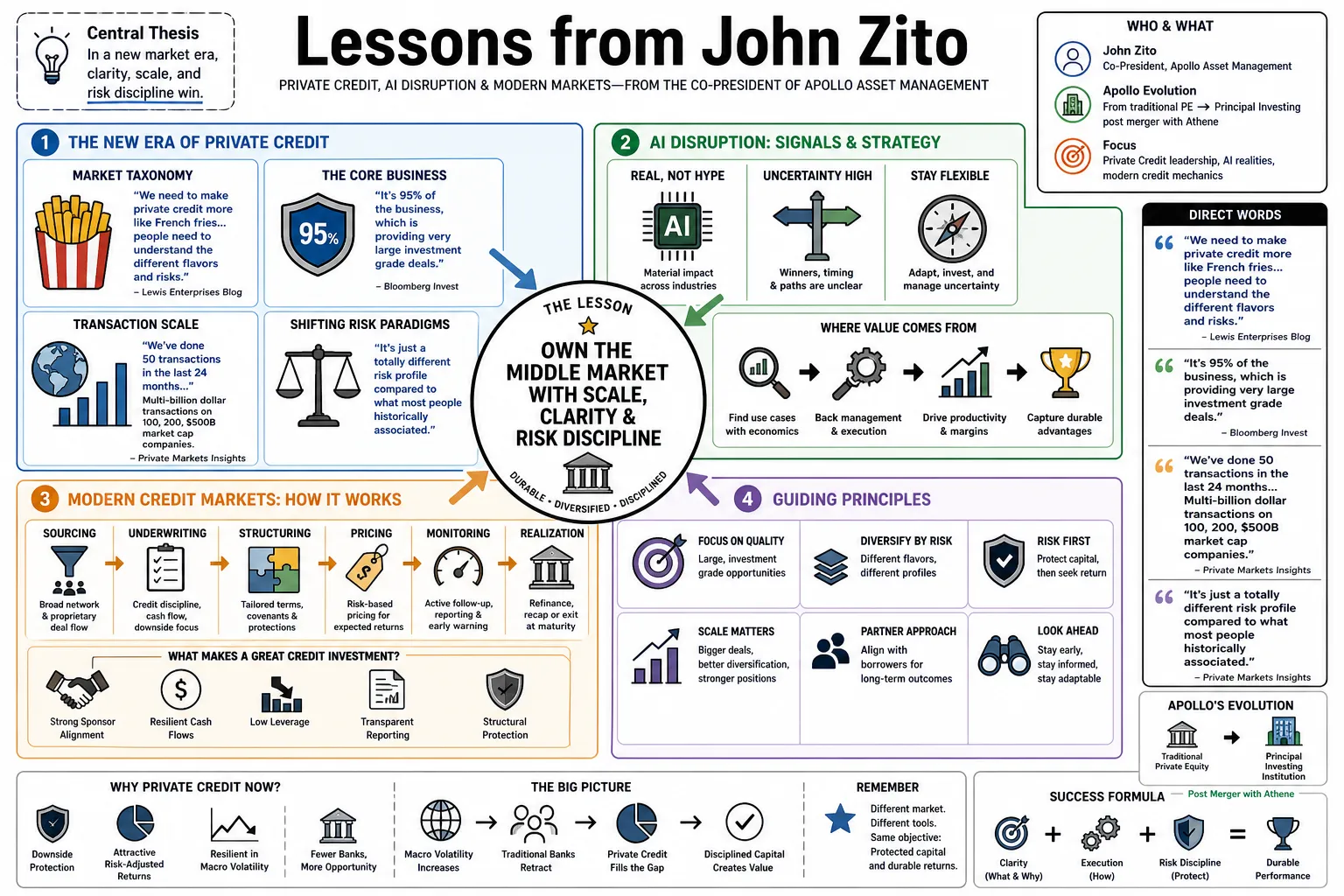

- On market taxonomy: "We need to make private credit more like French fries... people need to understand the different flavors and risks." — Source: Lewis Enterprises Blog

- On the core business: "It's 95% of the business, which is providing very large investment grade deals." — Source: Bloomberg Invest

- On transaction scale: "We've done 50 transactions in the last 24 months... Multi-billion dollar transactions on 100, 200, $500 billion market cap companies." — Source: Private Markets Insights

- On shifting risk paradigms: "It's just a totally different risk profile compared to what most people historically associated with private lending." — Source: Bloomberg Invest

- On market headwinds: "The next 12 to 18 months will probably be more difficult." — Source: Livemint

- On systemic durability: "Recent waves of fund withdrawals are normal cyclical movements, not systemic issues." — Source: Livemint

- On the sweet spot: "Private credit offers a sweet spot of enhanced yield over public benchmarks while maintaining rigorous credit quality." — Source: Apollo Insights

- On financing infrastructure: "We are seeing a fundamental rewiring of how large-scale infrastructure is financed away from traditional banks." — Source: Invest Like the Best

- On the duration of turmoil: "The current turmoil in some segments of private credit could persist for up to 18 months." — Source: S&P Global Podcast

- On defining the asset class: "Private credit is often used as a vague, catch-all term. We must better segment and appreciate the various expressions of the asset class." — Source: Lewis Enterprises Blog

Part 2: Software, AI, and Valuation Realities

- On private market marks: "I literally think all the marks are wrong." — Source: Illuminem

- On the software industry's future: "The real risk is – is software dead?" — Source: Colorado AI News

- On AI's disruptive threat: "Companies in the wrong position regarding the new AI-led regime could see recovery values as low as 20 to 40 cents on the dollar." — Source: Yahoo Finance

- On industry hubris: "There is an arrogance across the private equity and credit sectors regarding the carrying values of software deals." — Source: Substack

- On reinventing tools: "Would you use a screwdriver, or invent a new one?" — Source: Colorado AI News

- On vintage vulnerabilities: "Assets acquired between 2018 and 2022 are often of lower quality than public competitors and may face significant losses." — Source: Yahoo Finance

- On the myth of stable growth: "Artificial intelligence is forcing a reevaluation of the software sector's long-standing assumptions of stable growth and premium pricing." — Source: Futunn

- On the marginal cost of software: "As the marginal cost of producing software trends toward zero, the market's valuation logic is being fundamentally reshaped." — Source: Apollo Insights

- On competitive moats: "The disruptive impact of AI is stripping away the defensive moats that software companies have relied on for the past decade." — Source: Bloomberg Talks

- On market corrections: "The private equity community must prepare for a reckoning in how they value their aging software portfolios." — Source: Illuminem

Part 3: The Athene Merger and Principal Investing

- On structural evolution: "We're building effectively a more merchant-focused, principal-focused, not agent-focused asset manager." — Source: Invest Like the Best

- On client alignment: "By acting as a principal investor that deploys its own capital alongside client funds, we create greater alignment with clients." — Source: Private Markets Insights

- On balance sheet risk: "We have a significant portion of our own balance sheet at risk, contrasting with the traditional asset management model that primarily collects fees." — Source: Wave

- On the Athene integration: "The merger with Athene shifted us from a traditional private equity firm to a large-scale, credit-oriented financial institution." — Source: Chronicle Journal

- On long-duration liabilities: Zito frames long-duration capital as central to financing infrastructure, energy, semiconductors, digital systems, and other projects whose scale and tenor public markets cannot easily absorb alone. — Reference: Apollo Bloomberg Invest recap on long-duration capital needs

- On moving past the agent model: "Merely acting as an agent collecting fees on third-party assets is no longer sufficient for the scale we want to achieve." — Source: Invest Like the Best

- On the convergence of markets: "We are witnessing the convergence of private and public markets in how capital is sourced and deployed." — Source: Wave

- On scaling operations: "Integrating insurance and retirement assets allows us to underwrite complex transactions that traditional banks cannot touch." — Source: S&P Global Podcast

- On strategic transformation: "This was a transformative move that fundamentally rewired how we source capital and price risk." — Source: Buy Side Digest

Part 4: Redefining the Asset Management Model

- On the limitations of traditional PE: "The traditional private equity buyout model is just one small expression of what an alternative asset manager can do today." — Source: Invest Like the Best

- On capital origination: "Our ability to originate our own assets is what separates a modern principal-focused firm from a legacy allocator." — Source: S&P Global Podcast

- On the banking transition: "We are not trying to be a bank, but we are stepping into the void left by banks as they retreat from large-scale corporate lending." — Source: Bloomberg Live

- On underwriting standards: "When you invest your own balance sheet, the underwriting standards inherently become more rigorous." — Source: Private Markets Insights

- On market positioning: "We position ourselves not merely as a participant in capital markets, but as an architect reshaping how they function." — Source: Invest Like the Best

- On the ecosystem approach: "It’s about building a self-sustaining ecosystem where origination, capital, and risk management all feed into each other." — Source: Wave

- On the obsolescence of silos: "The old silos of public versus private, or equity versus debt, are becoming irrelevant to the ultimate owners of capital." — Source: Futunn

- On continuous evolution: "An asset manager today must continuously reinvent its capital supply chain to stay relevant." — Source: S&P Global Podcast

- On redefining scale: "Scale in asset management is no longer strictly about AUM; it’s about the breadth and depth of your origination capabilities." — Source: Bloomberg Invest

Part 5: Cultivating Unconventional Culture

- On hiring criteria: "We want people who are willing to test some of those norms and just be outside-the-box thinkers." — Source: Puck News

- On the Apollo Credit Olympics: "It is a skill-style event designed to foster unconventional thinking and camaraderie within the credit team." — Source: Puck News

- On childhood inspiration: "The relay race involving greased codfish was inspired by my childhood experiences in Milbridge, Maine." — Source: Puck News

- On liberal arts value: "My liberal arts education at Amherst College was instrumental in fostering an out-of-the-box mindset." — Source: Futunn

- On testing boundaries: "We encourage our teams to actively challenge the conventional wisdom of Wall Street." — Source: S&P Global Podcast

- On team dynamics: "Building a high-performing team requires a culture where creative problem-solving is rewarded over rigid conformity." — Source: S&P Global Podcast

- On cultural rituals: "Events like the Credit Olympics break down hierarchical barriers and build trust under pressure." — Source: Puck News

- On intellectual agility: "The modern credit market demands intellectual agility, not purely analytical horsepower." — Source: Invest Like the Best

- On embracing eccentricity: "We don't mind a bit of eccentricity if it leads to better, more differentiated investment outcomes." — Source: S&P Global Podcast

Part 6: Risk, Volatility, and Capital Protection

- On recognizing safety: "Everyone is acknowledging we will be in a higher-volatility regime, but they are not acknowledging credit is actually the typical safer place to be." — Source: Milken Institute

- On structural advantages: "Senior secured credit offers a structural advantage that protects capital when equity valuations contract." — Source: Bloomberg Talks

- On the new volatility regime: "We are transitioning into a sustained period of higher macroeconomic volatility where capital protection is paramount." — Source: Omny FM

- On pricing risk: "When volatility spikes, the ability to act as a principal allows us to price risk accurately when others are panicking." — Source: Bloomberg Live

- On the illusion of public liquidity: "The perceived liquidity of public markets often vanishes precisely when you need it most during a volatile regime." — Source: Milken Institute

- On disciplined underwriting: "You cannot compromise on the fundamental discipline of underwriting just because capital is abundant." — Source: S&P Global Podcast

- On macroeconomic shifts: "The era of zero interest rates masked a lot of underwriting mistakes that higher volatility will expose." — Source: Bloomberg Television

- On downside protection: "Our primary mandate in this environment is constructing portfolios with obsessive attention to downside protection." — Source: Milken Institute

- On significant risk transfers: "Significant risk transfer deals are becoming a critical tool for banks to manage capital in a volatile regulatory environment." — Source: Bloomberg Live

- On market dislocations: "Higher volatility regimes create the precise dislocations where disciplined private capital can generate outsized returns." — Source: S&P Global Podcast

Part 7: Democratizing Access for Retail Investors

- On structural inevitability: "Bringing private credit to retail investors via ETFs is a structural inevitability rather than a gimmick." — Source: Private Markets Insights

- On retail access: "This allows retail portfolios to access return potential previously reserved for institutional investors." — Source: Bloomberg Invest

- On managing liquidity: "The key to democratizing private markets is ensuring that the liquidity mechanisms are managed correctly and transparently." — Source: Bloomberg Invest

- On portfolio construction: Zito and State Street frame retail private-credit products as a way to give individual investors incremental yield and diversification through familiar ETF wrappers with liquidity and transparency features. — Reference: Apollo Bloomberg Invest recap on retail access, yield, and diversification

- On the ETF vehicle: "The ETF structure is proving to be an efficient bridge between illiquid private assets and retail demand." — Source: Private Markets Insights

- On educational hurdles: "The biggest barrier to retail adoption isn't product design; it's educating the market on what these assets actually are." — Source: Bloomberg Invest

- On the shifting retail mindset: "We are seeing a generational shift in how individual investors view the necessity of alternatives in their portfolios." — Source: Apollo Insights

- On regulatory alignment: "Democratization must be done in lockstep with regulators to ensure investor protections are not compromised." — Source: Bloomberg Invest

- On the scale of the retail market: Apollo describes the expansion of private credit into retail markets as an important evolution, with core-plus products combining public and private credit as credit allocations rise. — Reference: Apollo Bloomberg Invest recap on retail private-credit expansion

Part 8: Artistry at Scale and the Future of Finance

- On defining the concept: "Artistry at scale is about maintaining the craftsmanship of bespoke deal-making while deploying tens of billions of dollars." — Source: Invest Like the Best

- On the AI infrastructure boom: Zito says AI, power, infrastructure, and chips require multiple trillions of dollars of bespoke, long-duration capital, and Apollo links private credit to financing the next generation of AI and semiconductor infrastructure. — Reference: Apollo Bloomberg Invest recap on AI, power, infrastructure, and chips

- On institutional growth: "Building a major financial institution requires balancing the entrepreneurial spirit of a boutique with the rigorous processes of a global bank." — Source: Wave

- On the future of credit: Zito emphasizes Apollo's capacity to originate billion-dollar-plus corporate loans and asset-backed finance, while Apollo's ABF materials describe private direct origination, flexible capital, and bespoke solutions for issuers. — Reference: Apollo Bloomberg TV recap on corporate loans and asset-backed finance

- On scaling culture: "The hardest part of scaling is ensuring that the artistry of the investment process isn't diluted by bureaucracy." — Source: Invest Like the Best

- On data and technology: The Invest Like the Best episode notes frame technology and data management as tools for tailored investment advice and optimized decision-making, while still tying the discussion to Apollo's large information base and human judgment. — Reference: PodPulse notes on Zito episode technology and data-management themes

- On the next decade: "The next decade of finance will be defined by those who can bridge the gap between permanent capital and complex, long-term economic needs." — Source: S&P Global Podcast

- On global mega-trends: "Our strategy is entirely oriented around financing the global mega-trends: energy transition, digital infrastructure, and retirement demographics." — Source: S&P Global Podcast

- On the ultimate goal: "We are not just trying to be a participant in the market; we want to be the foundation upon which the future of capital markets is built." — Source: Invest Like the Best