Lessons from Jonathan Lewinsohn

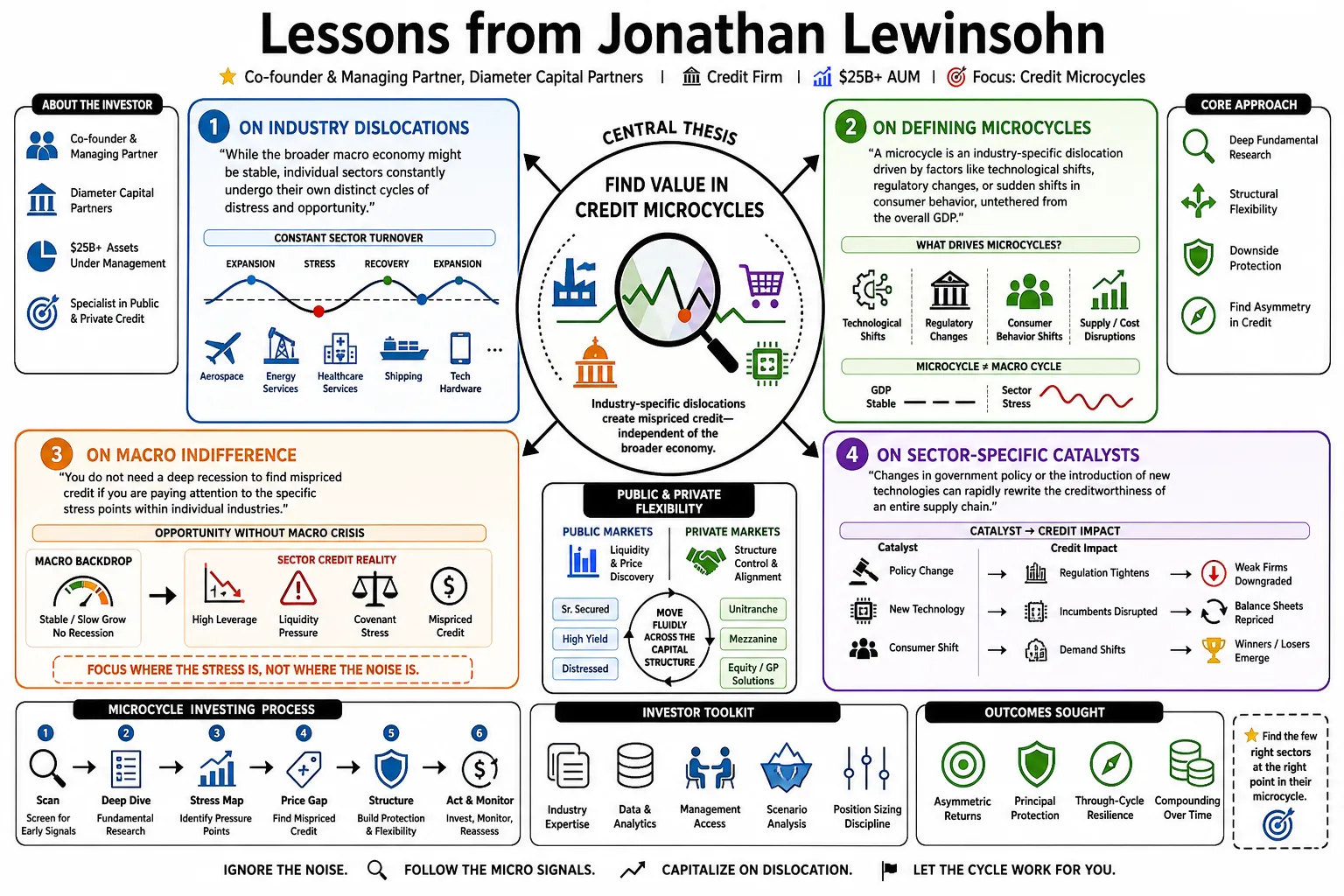

Jonathan Lewinsohn is the co-founder and Managing Partner of Diameter Capital Partners, a credit firm managing over $25 billion. His strategy centers on "credit microcycles," finding investments in industry-specific disruptions rather than broad economic shifts. This profile details how he navigates public and private debt markets through fundamental research and structural flexibility.

Part 1: The Philosophy of Microcycles

- On Industry Dislocations: "While the broader macro economy might be stable, individual sectors constantly undergo their own distinct cycles of distress and opportunity." — Source: [Capital Allocators]

- On Defining Microcycles: "A microcycle is an industry-specific dislocation driven by factors like technological shifts, regulatory changes, or sudden shifts in consumer behavior, untethered from the overall GDP." — Source: [Brown Advisory]

- On Macro Indifference: "You do not need a deep recession to find mispriced credit if you are paying attention to the specific stress points within individual industries." — Source: [Diameter Capital]

- On Sector-Specific Catalysts: "Changes in government policy or the introduction of new technologies can rapidly rewrite the creditworthiness of an entire sub-sector in a matter of months." — Source: [Capital Allocators]

- On Avoiding Generalizations: "Credit investing becomes dangerous when you assume all high-yield debt will behave the same way under a given set of interest rates." — Source: [Bloomberg]

- On Capitalizing on Panic: "When an industry faces a structural shift, broad index selling often punishes the debt of fundamentally sound companies within that sector, creating an entry point." — Source: [Private Debt Investor]

- On the Limits of Economic Forecasting: "Predicting inflation or the Fed's next move is notoriously difficult; predicting how a specific regulatory change will impact a specific telecom issuer's balance sheet is an analytical problem we can actually solve." — Source: [Capital Allocators]

- On Granular Analysis: "Our returns are largely generated by isolating the idiosyncratic risks of a business rather than betting on the direction of the S&P 500." — Source: [Diameter Capital]

- On Structural Stresses: "The transition to new business models often requires heavy capital expenditure, which can temporarily strain balance sheets and create mispriced debt." — Source: [Brown Advisory]

- On Persistent Opportunities: "Even in a bull market, there is always an industry undergoing a microcycle of distress." — Source: [Capital Allocators]

Part 2: Agility and the Speed of Capital

- On Organizational Speed: "In modern credit markets, the ability to deploy capital quickly when a dislocation occurs is a structural advantage." — Source: [Bloomberg]

- On Being Safely Fast: "Speed without discipline is reckless. Being safely fast requires doing the fundamental research long before the crisis actually hits." — Source: [Brown Advisory]

- On Fund Sizing: "Excessive size is the enemy of nimbleness. If a fund grows too large, it is forced to buy the market rather than selectively hunting for the best opportunities." — Source: [Capital Allocators]

- On Market Reactions: "When a dislocation happens, the first movers capture the widest spreads; by the time the broader market understands the narrative, the alpha has compressed." — Source: [Diameter Capital]

- On Execution: "The best investment thesis is useless if your trading desk cannot efficiently source and execute the bonds in a distressed tape." — Source: [Bloomberg]

- On Decision Chains: "A flat investment committee structure allows us to react to real-time market data without getting bogged down in institutional bureaucracy." — Source: [Capital Allocators]

- On Readiness: "We track hundreds of capital structures constantly so that when a price moves irrationally, we do not need three weeks to build a model." — Source: [Diameter Capital]

- On Liquidity Management: "Maintaining a portion of the portfolio in highly liquid, performing credit ensures we have the dry powder to act when volatility spikes." — Source: [Brown Advisory]

- On Competitive Advantage: "Scale can provide access, but agility generates outperformance in complex credit environments." — Source: [Bloomberg]

Part 3: Bottom-Up Research and Knowing the Names

- On Fundamental Underwriting: "You cannot rely on rating agencies or broad market sentiment; you must understand the covenants, the cash flows, and the assets backing the paper." — Source: [Capital Allocators]

- On Knowing the Names: "Credit investing is inherently a bottom-up exercise. You have to know the specific names, their management teams, and their unique vulnerabilities." — Source: [Bloomberg]

- On Covenant Analysis: "In downside scenarios, the legal documentation of a bond or loan dictates the recovery. Reading the fine print is not optional." — Source: [Diameter Capital]

- On Management Behavior: "Assessing how a management team has historically treated creditors versus equity holders is a critical input in pricing distressed debt." — Source: [Brown Advisory]

- On Asset Valuation: "When a company approaches default, enterprise value becomes a theoretical concept; what matters is the liquidation value of the specific collateral securing your tranche." — Source: [Capital Allocators]

- On Capital Structure Complexity: "Opportunities often hide in the mispricing between different tiers of debt within the exact same company." — Source: [Diameter Capital]

- On Defensive Posturing: "Our research process is inherently skeptical. We start by asking how a business might break, rather than how much it could grow." — Source: [Private Debt Investor]

- On Cash Flow Visibility: "A business with predictable cash flows can sustain higher leverage, but when that visibility clouds, the credit risk reprices violently." — Source: [Bloomberg]

- On Industry Expertise: "Generalist knowledge is insufficient for distressed investing; you need analysts who understand the specific operational metrics of the sector they cover." — Source: [Capital Allocators]

- On Independent Verification: "We rely on our own proprietary models and legal analysis to assess risk, rather than accepting the street's consensus view." — Source: [Diameter Capital]

Part 4: Private Credit and the Changing Lending Landscape

- On the Rise of Private Credit: "The secular shift of lending from banks to private funds has permanently altered the mechanics of corporate restructuring." — Source: [Capital Allocators]

- On Illiquidity Premiums: "Investors must ensure they are actually getting compensated for the lack of liquidity in direct lending, rather than simply accepting a yield that matches public markets." — Source: [Brown Advisory]

- On Refinancing Cycles: "The true test for recent private credit vintages will emerge when highly levered companies face a wall of maturities in a higher-rate environment." — Source: [Private Debt Investor]

- On Documentation Loopholes: "As private markets grew crowded, borrower-friendly documentation became common, which will limit creditor recoveries in the next default cycle." — Source: [Capital Allocators]

- On Public vs. Private Markets: "We prefer a broad mandate because there are times when public bonds offer better risk-adjusted returns than bespoke private loans." — Source: [Diameter Capital]

- On Sponsor Behavior: "Private equity sponsors are highly rational actors; understanding their incentives is essential when investing in sponsor-backed debt." — Source: [Bloomberg]

- On Capital Solutions: "Direct lending is no longer just about vanilla loans; it increasingly involves providing complex capital solutions to companies that traditional banks cannot serve." — Source: [Private Debt Investor]

- On Default Dynamics: "Defaults in private credit often happen quietly behind closed doors, negotiated between the sponsor and a single lender, unlike the public bankruptcy processes of the past." — Source: [Capital Allocators]

- On Market Maturation: "The direct lending asset class has matured rapidly, meaning managers must differentiate through sourcing and structuring rather than just capital availability." — Source: [Brown Advisory]

Part 5: Disruption and Technological Shifts

- On AI's Credit Impact: "Artificial intelligence is a classic microcycle trigger; it will dramatically reduce costs for some companies while completely destroying the business models of others." — Source: [Brown Advisory]

- On Software Lending: "Lending to software companies requires analyzing not just current recurring revenue, but the risk that a new technological paradigm renders their core product obsolete." — Source: [Capital Allocators]

- On Legacy Infrastructure: "Technological shifts often leave legacy infrastructure assets stranded, severely impacting the long-term debt backed by those assets." — Source: [Diameter Capital]

- On Adoption Curves: "The speed at which an industry adopts a disruptive technology determines the window of opportunity for credit investors to short or avoid the losers." — Source: [Bloomberg]

- On Telecom and Media: "The transition from traditional broadcast to streaming, and the corresponding infrastructure build-out, has created continuous, investable volatility in media credit." — Source: [Capital Allocators]

- On Capital Intensity: "Disruptive industries often require massive upfront capital, creating a reliance on debt markets that can become precarious if execution falters." — Source: [Brown Advisory]

- On Retail Microcycles: "E-commerce disruption was one of the clearest early examples of a microcycle, systematically dismantling the credit profiles of mall-based retailers while the broader economy grew." — Source: [Diameter Capital]

- On Obsolescence Risk: "In credit, you do not need a company to grow endlessly, but you must be certain its product will remain relevant until the bond matures." — Source: [Capital Allocators]

- On Energy Transitions: "The shift toward renewable energy policies creates intense capital needs and unpredictable regulatory environments, ideal conditions for distressed debt generation." — Source: [Bloomberg]

- On Identifying Winners: "It is often easier in credit to identify the businesses that will be destroyed by technology than to pick the ultimate equity winners." — Source: [Brown Advisory]

Part 6: Navigating the Full Credit Spectrum

- On Flexibility: "A rigid mandate forces you to invest in a specific asset class even when it is fully priced; a flexible mandate allows you to rotate to where the risk-reward is actually compelling." — Source: [Diameter Capital]

- On Investment Grade to Distressed: "We evaluate everything from performing investment-grade paper to deeply distressed restructuring situations using the same fundamental lens." — Source: [Capital Allocators]

- On Relative Value: "The core of our strategy is constantly comparing the yield of a senior secured loan against a high-yield bond or a CLO tranche to find the cheapest entry point for a given risk." — Source: [Bloomberg]

- On Market Dislocation: "In moments of severe market stress, high-quality, performing assets are often liquidated indiscriminately, creating immediate relative value opportunities." — Source: [Brown Advisory]

- On CLO Liabilities: "Investing in the liabilities of Collateralized Loan Obligations requires understanding the underlying loan portfolios as well as the structural mechanics of the vehicle itself." — Source: [Private Debt Investor]

- On Distressed Debt: "True distressed investing is not merely trading discounted paper; it involves taking an active role in restructuring a company's balance sheet to unlock value." — Source: [Capital Allocators]

- On Shifting Capital: "The ability to smoothly shift capital from private lending back into public markets when public spreads widen is a massive structural advantage." — Source: [Diameter Capital]

- On Capital Preservation: "When yields across the spectrum are tight, the mandate is to preserve capital and wait; you cannot force a distressed cycle." — Source: [Bloomberg]

- On Trading Technicals: "Fundamental research tells you what an asset is worth, but understanding market technicals tells you when and how to buy it." — Source: [Brown Advisory]

Part 7: Risk Management and Sizing

- On Sizing Discipline: "The difference between a good idea and a profitable trade often comes down to sizing it correctly relative to its liquidity and downside risk." — Source: [Capital Allocators]

- On Portfolio Construction: "A well-constructed credit portfolio balances concentrated, high-conviction distressed positions with diversified, liquid performing names." — Source: [Diameter Capital]

- On Avoiding Dilution: "We actively cap our asset growth in certain strategies to ensure we are never forced to deploy capital into mediocre ideas just to put money to work." — Source: [Bloomberg]

- On Downside Protection: "Our primary job is to measure the floor. If we are highly confident in the worst-case recovery value, the upside will generally take care of itself." — Source: [Brown Advisory]

- On Managing Volatility: "Volatility in credit is not necessarily risk; it is often the mechanism that creates the mispricing we exploit." — Source: [Capital Allocators]

- On Hedge Execution: "Shorting credit effectively requires highly specific catalysts and an understanding of the exact instruments that will react to a company's deterioration." — Source: [Diameter Capital]

- On Information Asymmetry: "Risk is elevated when you are relying on the same public information as the rest of the market; safety comes from doing the harder, deeper diligence." — Source: [Private Debt Investor]

- On Interest Rate Sensitivity: "We manage duration risk carefully, ensuring that our returns are driven by our credit underwriting rather than a directional bet on the yield curve." — Source: [Bloomberg]

- On Capital Lock-ups: "Matching the liquidity of our liabilities with the liquidity of our underlying investments prevents forced selling during periods of market stress." — Source: [Capital Allocators]

Part 8: Law, Policy, and Markets

- On Legal Backgrounds: "A background in law fundamentally changes how you view a capital structure; you read a credit agreement looking for the exact mechanism of failure or enforcement." — Source: [Capital Allocators]

- On Judicial Influence: "Clerking in the federal appellate system teaches you to strip away market noise and focus strictly on the text and precedents that govern a dispute." — Source: [Brown Advisory]

- On Regulatory Shifts: "Changes in antitrust enforcement or environmental policy are classic catalysts for industry microcycles, drastically altering the cost of capital for specific sectors." — Source: [Bloomberg]

- On Bankruptcy Proceedings: "The US bankruptcy code is a dynamic arena; understanding how different jurisdictions and judges approach restructuring is a critical edge in distressed debt." — Source: [Diameter Capital]

- On Creditor-on-Creditor Violence: "We are currently in an era where aggressive sponsors and select creditors exploit loose documents to subordinate other lenders. You have to read the documents defensively." — Source: [Capital Allocators]

- On Policy Interventions: "Government intervention in markets can delay a credit cycle, but it rarely cures the underlying insolvency of a flawed business model." — Source: [Private Debt Investor]

- On Structuring Transactions: "The most lucrative credit investments often involve structuring a new legal solution to a borrower's liquidity crisis, rather than buying existing bonds." — Source: [Diameter Capital]

- On Institutional Constraints: "Many market inefficiencies exist simply because regulatory or mandate constraints force banks or insurance companies to sell downgraded debt regardless of price." — Source: [Bloomberg]

- On The Rule of Law: "The entire credit ecosystem relies on the predictable enforcement of contracts; when that predictability is challenged, risk premiums must widen." — Source: [Capital Allocators]