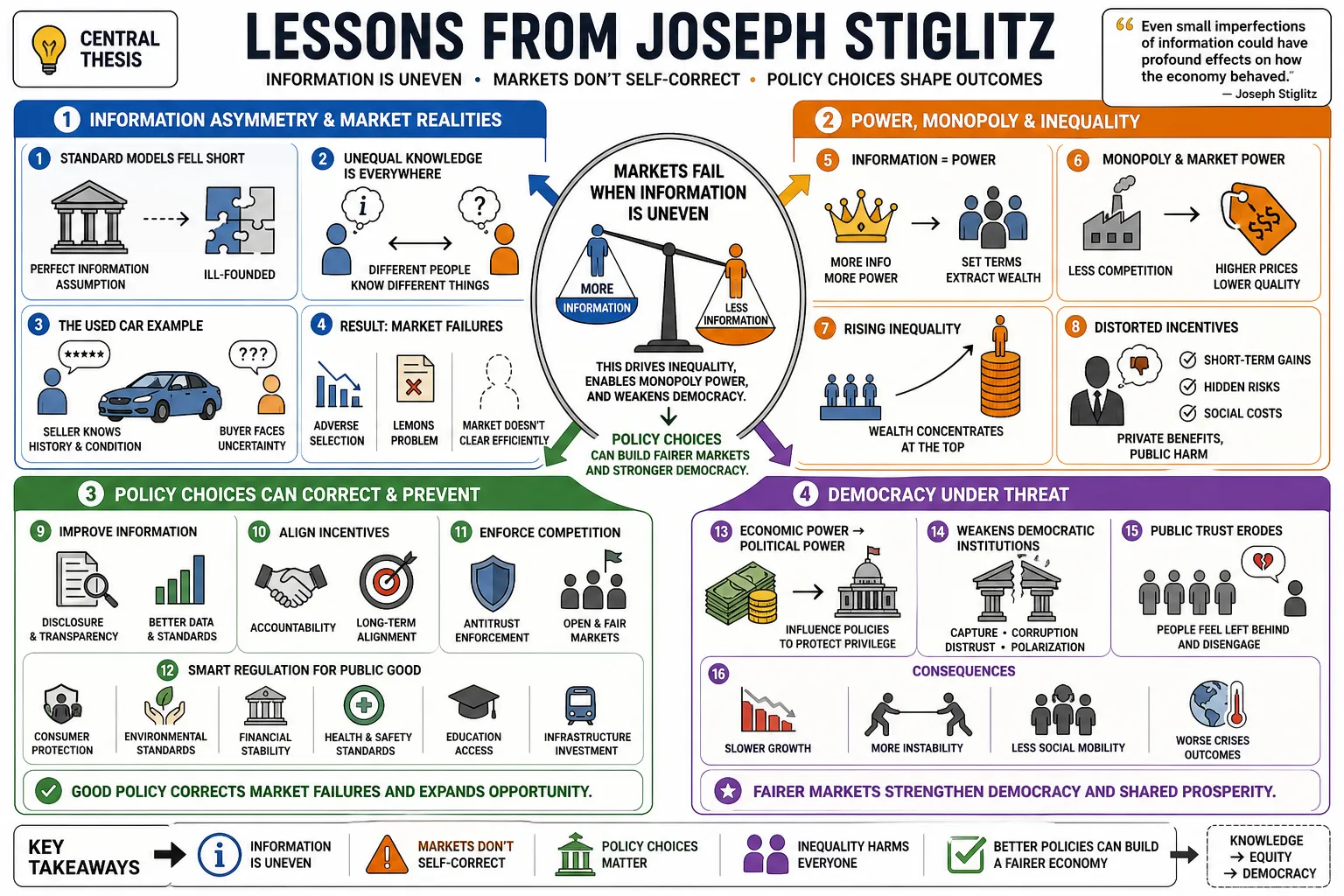

Joseph Stiglitz is an economist who proved that markets fail when buyers and sellers have unequal access to information, challenging the longstanding assumption that free markets naturally self-correct. He has spent his career examining how this dynamic drives inequality, allows monopolies to extract wealth, and undermines democratic institutions. This collection of his insights outlines how policy choices, rather than invisible hands, shape economic realities and what a fairer system might look like.

Part 1: Information Asymmetry and Market Realities

- On the failure of standard models: "For two hundred years, economists used simple economic models that assumed that information was perfect... We showed that this notion was ill-founded: even small imperfections of information could have profound effects on how the economy behaved." — Source: ResearchGate

- On the ubiquity of uneven knowledge: Information asymmetry is a fundamental aspect of markets caused simply by the fact that different people in a transaction know different things. — Source: ResearchGate

- On the used car market: Sellers of used vehicles possess intimate knowledge about the car's condition and history that buyers cannot easily verify, creating an inherent imbalance. — Source: EBSCO

- On insurance markets: The people buying insurance often know far more about their personal risks—like their driving habits or underlying health conditions—than the insurance company providing the policy. — Source: NBER

- On labor market blind spots: Prospective workers generally hold better information regarding their own skills, work ethic, and abilities than the employers trying to hire them. — Source: ResearchGate

- On lending and credit: Borrowers applying for loans typically have a much clearer understanding of their ability and intention to repay than the bank lending the money. — Source: ResearchGate

- On market efficiency: When information is distributed asymmetrically across participants, markets rarely achieve Pareto efficiency, leading to systemic failures. — Source: NBER

- On credit rationing: Because banks cannot perfectly assess borrower risk, they often choose to limit the total number of loans they issue rather than simply raising interest rates to clear the market. — Source: NobelPrize.org

- On the breakdown of supply and demand: Standard economic laws fail when quality is linked directly to price, such as when worker productivity depends on the wage paid or loan defaults depend on the interest rate charged. — Source: Wikiquote

- On efficiency wages: Because firms cannot perfectly monitor how hard their employees are working, they often pay wages above the market rate to incentivize effort and penalize shrinking. — Source: EconLib

Part 2: The Myth of the Free Market

- On ideological blinders: Free market fundamentalism is a political ideology masquerading as an economic reality, resting on assumptions that rarely hold true in practice. — Source: Codesria

- On the invisible hand: The reason the invisible hand often seems invisible is that it is simply not there; markets are not naturally self-regulating. — Source: FinancialPolicy

- On the Washington Consensus: A rigid set of neoliberal policy prescriptions often harmed the developing nations it was supposed to help, particularly during periods of financial distress. — Source: Pambazuka

- On the 2008 financial crisis: Flawed ideas about self-correcting markets and minimal regulation directly contributed to the global financial disaster of 2008. — Source: Codesria

- On successful development: Countries in East Asia that actively regulated their financial markets experienced more successful development than those that blindly adopted free market fundamentalism. — Source: Pambazuka

- On government intervention: Because markets are characterized by widespread information asymmetries, government regulation is frequently necessary to protect the public interest. — Source: FinancialPolicy

- On neoliberalism's track record: Neoliberal capitalism has failed on its own economic terms by failing to deliver sustainable growth or shared prosperity. — Source: Capitalisn't

- On deregulation: Removing rules meant to protect consumers and workers does not unleash innovation, but rather invites exploitation and financial instability. — Source: Codesria

- On the predictable dangers of fundamentalism: Relying on unfettered markets creates predictable risks, shifting wealth upward while leaving the broader economy vulnerable to shocks. — Source: Wikipedia

- On religious belief in markets: Treating free markets as an article of faith prevents societies from addressing obvious market failures through pragmatic policy. — Source: Goodreads

Part 3: Globalization and its Discontents

- On the nature of globalization: "Globalization itself is neither good nor bad. It has the power to do enormous good... But in much of the world it has not brought comparable benefits. For many, it seems closer to an unmitigated disaster." — Source: SuperSummary

- On reshaping global systems: "I believe that globalization can be reshaped to realize its potential for good and I believe that the international economic institutions can be reshaped in ways that will help ensure that this is accomplished." — Source: SuperSummary

- On the International Monetary Fund: "A half century after its founding, it is clear that the IMF has failed in its mission. It has not done what it was supposed to do—provide funds for countries facing an economic downturn." — Source: SuperSummary

- On distant policymaking: "Modern high-tech warfare is designed to remove physical contact... Modern economic management is similar: from one's [office], one does not see the impact of policy on the lives of people." — Source: SuperSummary

- On one-size-fits-all policies: International institutions frequently imposed uniform neoliberal policies, like rapid privatization, without accounting for the specific social contexts of developing nations. — Source: Bookey

- On institutional power imbalances: Global economic institutions lack democratic accountability and routinely prioritize the interests of wealthy nations and multinational corporations over developing countries. — Source: Bookey

- On the true meaning of development: Authentic economic development requires transforming the actual lives of people, rather than simply transforming macroeconomic indicators. — Source: Goodreads

- On managed integration: Globalization works best when countries are allowed to integrate into the international economy at their own pace and on their own terms. — Source: UTexas

- On the cost of rapid liberalization: Forcing developing nations to open their markets prematurely often destroyed local industries before new ones could take their place. — Source: Reddit

- On capital market liberalization: Removing controls on the flow of international capital often leads to speculative bubbles and devastating financial crises rather than stable investment. — Source: Reddit

Part 4: Rent-Seeking and Wealth Extraction

- On defining rent-seeking: "Economists have a name for these activities; they call them rent seeking, getting income not as a reward to creating wealth but by grabbing a larger share of the wealth that would have otherwise been produced without their effort." — Source: Independent

- On sustainable monopolies: "The simplest way to a sustainable monopoly is getting the government to give you one." — Source: Independent

- On misaligned incentives: "In a rent-seeking economy such as ours is becoming, private and social returns are badly misaligned." — Source: Goodreads

- On extraction versus creation: Much of modern wealth is not created through innovation, but extracted through control of existing assets, lobbying, and regulatory capture. — Source: World Bank

- On shaping the rules: Powerful interests use their resources to shape the economic rules of the game in their favor, embedding advantages in complex tax laws and bankruptcy codes. — Source: World Bank

- On monopoly rents: Firms with unchecked market power extract value by overcharging consumers and suppressing wages, which stifles broader economic growth. — Source: INET Economics

- On too big to fail: State guarantees for massive financial institutions encourage reckless behavior by socializing the risks while privatizing the rewards. — Source: Columbia University

- On corporate welfare: Government subsidies directed at profitable industries represent a direct transfer of wealth from taxpayers to politically connected corporations. — Source: The Guardian

- On the suppression of competition: Monopolies dedicate significant resources not to improving their products, but to creating barriers to entry that prevent new competitors from challenging their dominance. — Source: Columbia University

Part 5: The Price of Inequality

- On the trajectory of society: "Whether we will fall to the depths of some countries, where the gates grow higher and the societies split farther and farther apart, I do not know. It is, however, the nightmare towards which we are slowly marching." — Source: Goodreads

- On market distortions: "Part of the reason for this is that much of America's inequality is the result of market distortions, with incentives directed not at creating new wealth but at taking it from others." — Source: Goodreads

- On the concentration of wealth: "In America the share of national income going to the top .01%... has risen from just over 1% in 1980 to almost 5% now – an even bigger slice than the top .01% got in the Gilded Age." — Source: BigBenComedy

- On political and economic disparity: "Societies with more economic inequality tend to have more political inequality, especially when it reaches the outsize levels." — Source: BigBenComedy

- On economic instability: "Inequality undermines the strength of our economy and contributes to economic instability." — Source: Columbia University

- On the myth of upward mobility: "The chances of an American citizen making this way from the bottom to the top are less than those of citizens in other advanced industrial countries." — Source: BigBenComedy

- On political choices: The current extremes of inequality are not the inevitable result of market forces, but the direct outcome of specific political and economic policy decisions. — Source: Sobrief

- On weakened institutions: High levels of wealth disparity inevitably lead to a less efficient economy and systematically weaken democratic institutions. — Source: Sobrief

- On the loss of social cohesion: When a society becomes deeply divided between the ultra-rich and the struggling majority, the basic social contract and sense of shared national purpose begin to fray. — Source: Columbia University

Part 6: Measuring What Matters

- On the power of metrics: "What we measure affects what we do. If we measure the wrong thing, we will do the wrong thing." — Source: Sustainable Prosperity

- On the limits of GDP: Gross Domestic Product focuses heavily on material production and entirely misses crucial factors like health, education, and environmental degradation. — Source: Social Europe

- On policy distortion: Relying solely on GDP provides a distorted view of national progress, leading policymakers to prioritize output over actual societal well-being. — Source: Columbia University

- On a dashboard approach: Rather than condensing an economy into a single number, governments should use a dashboard of indicators that capture sustainability, security, and inequality. — Source: New Forum

- On existential threats: When governments only look at GDP growth, they become dangerously complacent about slow-moving crises like climate change that don't immediately dent economic output. — Source: Columbia University

- On resource depletion: An economy can show strong GDP growth while simultaneously destroying the natural resources and environment required to sustain that growth in the future. — Source: The Guardian

- On inequality and averages: GDP is an aggregate measure that can rise even while the majority of citizens see their personal incomes stagnate or decline. — Source: Europa

- On the value of unpriced work: Traditional economic metrics fail to account for the immense value of unpaid domestic labor and caregiving, distorting our understanding of productive effort. — Source: Europa

- On the Commission on the Measurement of Economic Performance: The effort to move beyond GDP was driven by a need to align statistical indicators with the actual lived experiences of citizens. — Source: Europa

Part 7: The Euro and European Economics

- On the single currency's reality: "The euro was born with great hopes. Reality has proven otherwise." — Source: Goodreads

- On Europe's underlying mistake: "While there are many factors contributing to Europe's travails, there is one underlying mistake: the creation of the single currency, the euro." — Source: Forbes

- On unintended consequences: "The euro [currency] was supposed to usher in greater prosperity, which in turn would lead to renewed commitment to European integration. It has done just the opposite." — Source: Quora

- On a flawed design: The euro was flawed at birth because it prioritized economic integration over the political integration necessary to make a shared currency function. — Source: Columbia University

- On the divergence of states: Rather than bringing European economies closer together, the structure of the eurozone has actively promoted divergence between member nations. — Source: LSE

- On misguided austerity: Policies pushed by the European Central Bank focused heavily on austerity, which directly caused stagnation and unemployment in Southern Europe. — Source: Forbes

- On the loss of flexibility: By adopting the euro, countries lost the ability to devalue their own currency to regain competitiveness during economic downturns. — Source: The Guardian

- On internal devaluation: Without currency control, struggling eurozone nations are forced into painful internal devaluations—slashing wages and prices—which often leads to prolonged economic depression. — Source: Reddit

- On the future of the project: A well-managed end to the single-currency experiment might be necessary, and would not necessarily mean the end of the broader European project. — Source: Columbia University

Part 8: Progressive Capitalism and Public Policy

- On serving society: "Progressive capitalism is not an oxymoron; we can indeed channel the power of the market to serve society." — Source: Marcellus

- On the social contract: "Progressive capitalism [is] a social contract where the role of the state is reinstated with respect to making regulations that encourage competition that can balance out the powers between corporates and workers." — Source: Marcellus

- On economic priorities: In a Rockefeller Foundation Bellagio profile, Stiglitz defines progressive capitalism around the same priority: people do not exist to serve the economy; the economy exists to serve people and societal wellbeing. — Reference: Rockefeller Foundation Bellagio profile quoting Stiglitz on progressive capitalism and the economy serving people

- On freedom and wolves: Citing Isaiah Berlin, the reality of unregulated markets is often that "freedom for the wolves has often meant death to the sheep." — Source: Fast Company

- On the good society: A truly good society requires public investment in education, technology, and infrastructure to ensure individuals have the opportunity to reach their full potential. — Source: Cato Institute

- On restoring balance: Economic power has become too concentrated, and policies must actively curb monopolies and empower workers to ensure prosperity is shared. — Source: Goodreads

- On managing externalities: Active government involvement is required to manage the externalities that markets ignore, such as environmental destruction and systemic financial risk. — Source: Capitalisn't

- On redefining freedom: True freedom for citizens is not merely the absence of government regulation, but the freedom to live without the constant fear of poverty and unemployment. — Source: Fast Company

- On resolving conflicts: A core function of the state in a progressive capitalist system is to act as an arbiter, resolving conflicting interests and preventing the exploitation of the vulnerable. — Source: Medium