Lessons from Josh Kushner

Josh Kushner founded Thrive Capital in 2009 to run more like an operating company for founders than a standard venture fund. He made his name placing concentrated, early bets on tech companies like Instagram, OpenAI, and Oscar Health, which he co-founded. This profile covers his thinking on capital allocation, the limits of artificial intelligence, and how to build lasting partnerships.

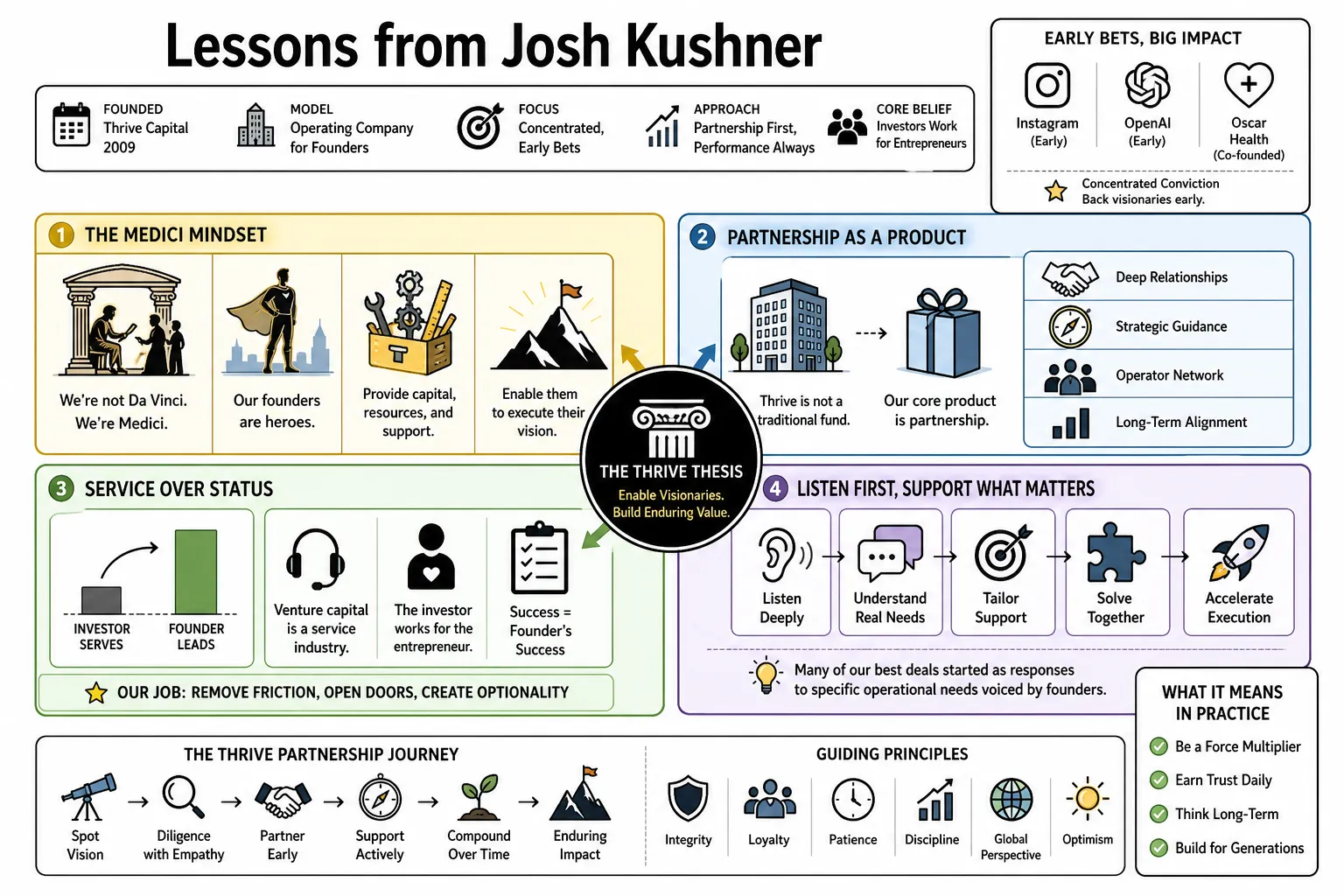

Part 1: The Medici Mindset

- On the venture capitalist's role: "We're not Da Vinci. We're Medici... our opportunity is to enable the artists that we're fortunate enough to support to create their masterpieces." — Source: [Sourcery]

- On partnership as a product: Thrive is not a traditional fund, but an operating company whose core product is partnership. — Source: [Sourcery]

- On enabling visionaries: "Our founders are heroes. It is our job to provide the capital, resources, and support necessary to enable them to execute their vision." — Source: [Podscripts]

- On service provision: Venture capital is ultimately a service industry, where the investor works for the entrepreneur. — Source: [Invest Like the Best: Josh Kushner]

- On listening over prescribing: Many of the firm's most significant deals were direct responses to specific operational needs voiced by founders, rather than abstract strategy plays. — Source: [Sourcery]

- On founder heroism: Investors must recognize that the real magic happens at the operational level, driven by the founders. — Source: [Podscripts]

- On capital as a tool: Capital is merely an enabler; the true masterpiece is the business built by the founder. — Source: [Sourcery]

- On humility in investing: Approaching venture capital requires humility, trust, and serving founders first. — Source: [Invest Like the Best: Josh Kushner]

- On long-term belief: "There will be bad quarters, there'll be bad years, but if you believe in the people who are running the business, ultimately everything works out." — Source: [Sourcery]

Part 2: Conviction and Concentration

- On portfolio strategy: Venture capital requires a highly concentrated investment strategy rather than a broad, indexed approach. — Source: [Invest Like the Best: Josh Kushner]

- On the real estate analogy: "We invest in Fifth Avenue." Backing top-tier companies ensures compound growth over time. — Source: [Wave]

- On depth of understanding: The only way to develop true context for an industry is through intimate, time-intensive involvement. — Source: [Sourcery]

- On making massive bets: A firm must be willing to make high-conviction investments when they believe in the long-term potential of the business. — Source: [Podwise]

- On the power law: Venture returns are driven by a power law where fewer, larger bets yield the best outcomes. — Source: [Invest Like the Best: Josh Kushner]

- On evaluating fundamentals: "Do we believe in the fundamentals of the space that we're working in? Do we believe that the long term trends associated with technology innovation are going to move in a very particular direction?" — Source: [Wave]

- On capital intensity: "OpenAI is a very capital-intensive business. It was our job to get them that capital." — Source: [Sourcery]

- On missing opportunities: "As an investor, you do not get all investments right all the time; sometimes you miss out on lucrative opportunities." — Source: [YU Observer]

- On the barbell strategy: It is effective to maintain a barbell approach—backing early-stage seed startups while aggressively chasing growth-stage rounds in breakout companies. — Source: [Product Market Fit]

- On conviction over consensus: Real conviction means betting heavily when the rest of the market is uncertain. — Source: [Time]

Part 3: Ignoring the Noise

- On external validation: "External validation can distort even the most disciplined minds." — Source: [Sourcery]

- On staying focused: "I think it's really important that we ignore the noise, keep our heads down." — Source: [Sourcery]

- On the risks of success: Success carries its own risks; maintaining a disciplined culture requires deliberate insulation from praise. — Source: [Sourcery]

- On insulating the firm: An investment firm must actively shield itself from both external adulation and criticism. — Source: [Sourcery]

- On continuous learning: Prioritize learning over self-promotion, listen deeply, and avoid seeking constant external feedback. — Source: [Wave]

- On independent thinking: First principles thinking requires stripping away market trends to evaluate a company's fundamental value. — Source: [Josh Kushner on AI and Thrive]

- On market fluctuations: It is vital to ignore short-term market cycles and focus on building enduring companies. — Source: [Sourcery]

- On media romanticization: Entrepreneurship is often romanticized in the media, but in reality, it is incredibly difficult to build a business. — Source: [AlleyWatch]

- On self-belief: "Believing that you can move mountains sometimes is more important than actually having the ability to do so." — Source: [AZ Quotes]

Part 4: Artificial Intelligence and OpenAI

- On the AI race: Maintaining U.S. dominance in artificial intelligence is "the most important moment in our lifetimes." — Source: [Josh Kushner on AI and Thrive]

- On national security: AI competition must be treated as a national priority to ensure systems are built with democratic values. — Source: [Josh Kushner on AI and Thrive]

- On OpenAI's market position: "To use the Lord of the Rings analogy, Sam, Greg, OpenAI have the Ring, and everyone is willing to do whatever they can to take it." — Source: [Business Insider]

- On power and corruption: When asked if power corrupts in the context of the AI race, he answered simply, "Yes." — Source: [Business Insider]

- On loyalty to founders: During the OpenAI leadership crisis, Thrive Capital immediately went to war to support Sam Altman. — Source: [Business Insider]

- On human behavior around power: Proximity to OpenAI provided a front-row seat to how people behave when value becomes concentrated in a single company. — Source: [Business Insider]

- On AI policy: Securing American access to compute, energy, and talent is a critical matter of public policy. — Source: [Josh Kushner on AI and Thrive]

- On mega-scale valuations: Private companies driven by AI have the potential to reach unprecedented valuations of half a trillion or a trillion dollars. — Source: [Sourcery]

- On applied AI: The next wave of value creation will come from transforming legacy industries through AI-native infrastructure. — Source: [PitchBook]

Part 5: The "Long Humans" Thesis

- On the value of human labor: "Human labor will gain value despite AI automation." — Source: [Digg]

- On the future of expertise: As AI automates routine tasks, uniquely human qualities like trust and expertise will appreciate. — Source: [Substack]

- On time-tested relationships: Trust accumulated over time cannot be synthesized by an algorithm. — Source: [RK Library]

- On human-centric business: Investing in businesses where human involvement remains critical is a core strategy in the AI era. — Source: [Digg]

- On the limits of automation: Technology solves for efficiency, but humans are required for empathy and judgment. — Source: [Substack]

- On acquiring services firms: The firm's strategy includes acquiring advisory firms with the belief that AI will elevate the importance of human expertise. — Source: [Substack]

- On the "Hold Forever" principle: Investments in human capital compound indefinitely, requiring a long-term holding strategy. — Source: [Jupiter]

- On the dichotomy of AI and humanity: Investing in AI infrastructure simultaneously necessitates investing in the human systems that deploy it. — Source: [Substack]

- On human resilience: Even in an era of rapid AI advancement, human intuition remains an irreplaceable asset class. — Source: [Digg]

Part 6: Oscar Health and Disruption

- On navigating complex industries: "This is not Tumblr. This is not Spotify. This is not Square. This is a really complicated business. It's a real business." — Source: [Inc.]

- On the consumer experience: "Our ethos and mission is to create a good consumer experience. We wanted to create an experience like having a doctor in the family." — Source: [Medium]

- On legacy complacency: "The existing players don't care about satisfying the customer." — Source: [Medium]

- On the state of healthcare: "A lot of people in this industry are just evil," referring to the slow pace of innovation and resistance to change. — Source: [Forbes]

- On the bar for innovation: "Health insurance companies, today, do everything they can to acquire customers but, after that, everything they can to avoid them." — Source: [AlleyWatch]

- On consumerization: Healthcare requires consumerization to force necessary improvements and real competition. — Source: [CBS News]

- On technological transparency: The goal of tech in healthcare is to make insurance pricing and networks easy to understand. — Source: [Wikipedia]

- On building for yourself: "Our ambition is to create the consumer experience that we would want for ourselves." — Source: [AlleyWatch]

- On disrupting incumbents: Challenging legacy firms requires treating the new venture as a technology-first company from day one. — Source: [Healthcare Dive]

Part 7: Founder Psychology and Support

- On extreme difficulty: Building a startup is far less glamorous than it appears; it is an inherently grueling process. — Source: [AlleyWatch]

- On conviction in people: When quarters are bad, the ultimate safety net is your belief in the people running the business. — Source: [Sourcery]

- On founder trust: The investor-founder relationship must be built on mutual trust, especially when facing systemic crises. — Source: [Business Insider]

- On enabling the unproven: Sometimes the best investments are backing founders before they have explicit permission from the market. — Source: [Invest Like the Best: Josh Kushner]

- On handling chaos: Observing how individuals behave when power and value concentrate reveals their true character. — Source: [Business Insider]

- On backing the artist: The role of the capital provider is to stay out of the way of the visionary's execution while providing necessary scaffolding. — Source: [Podscripts]

- On the burden of leadership: Founders bear an emotional weight that investors must respect and attempt to alleviate. — Source: [Sourcery]

- On navigating hype cycles: Founders must actively resist being swept up in the narrative of their own success to maintain execution quality. — Source: [Wave]

- On dealing with failure: Missing lucrative opportunities or having companies stumble is an inherent feature of the venture landscape. — Source: [YU Observer]

- On character under pressure: A company's true culture is revealed during leadership crises and market downturns. — Source: [Business Insider]

Part 8: Early Lessons & Building Thrive

- On organizational design: Keep the investment team surprisingly small to maintain a high level of involvement and an entrepreneurial culture. — Source: [Invest Like the Best: Josh Kushner]

- On team autonomy: Hire exceptional people and provide them with total autonomy and transparency. — Source: [Podwise]

- On avoiding the fund label: Structuring Thrive as an operating company changes how the team interacts with the market. — Source: [Sourcery]

- On the necessity of struggle: Early startup failures provide the operational scars necessary for good investing. — Source: [Wikipedia]

- On depth over breadth: A small team forces an organization to prioritize depth with a few companies rather than spreading attention. — Source: [Product Market Fit]

- On defining success: True success in venture capital is measured by the enduring impact of the companies built, not just assets under management. — Source: [YU Observer]

- On early agility: Securing allocations in breakout companies requires moving with unprecedented speed and conviction. — Source: [AlleyWatch]

- On independent identity: Building an independent venture franchise requires deliberately separating one's professional identity from legacy family businesses. — Source: [Medium]

- On compounding relationships: The venture business is ultimately about compounding relationships over decades, not optimizing single transactions. — Source: [Sourcery]

- On the product of VC: Capital is a commodity; the true product a venture firm sells is the quality of its partnership. — Source: [Sourcery]