Lessons from Kent Daniel

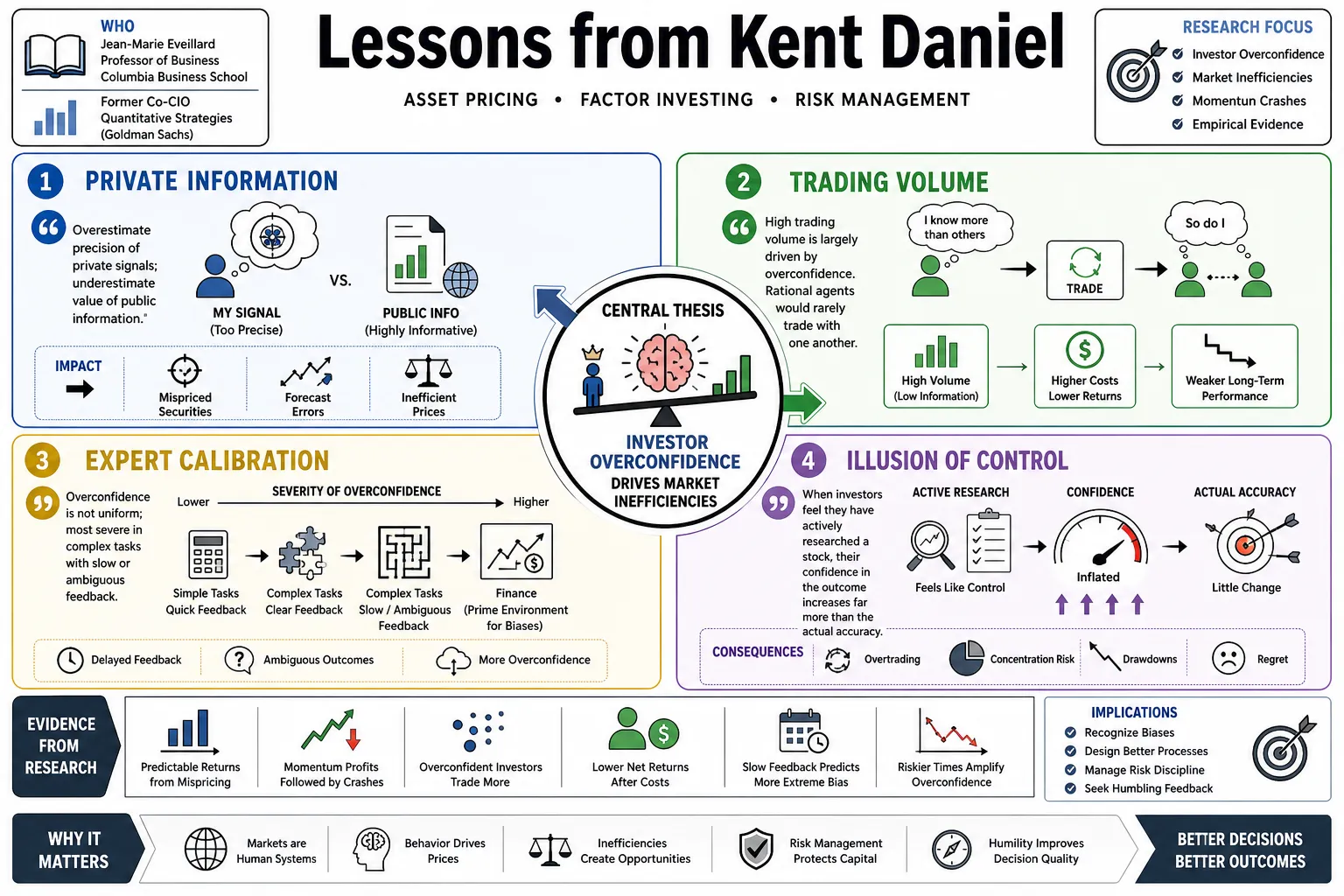

Kent Daniel is the Jean-Marie Eveillard Professor of Business at Columbia Business School and a former co-CIO of quantitative strategies at Goldman Sachs. His research documents how investor overconfidence creates market inefficiencies and explains the mechanics behind momentum crashes. This collection organizes his work on asset pricing, factor investing, and risk management.

Part 1: Investor Overconfidence and Market Efficiency

- On Private Information: "Investors tend to systematically overestimate the precision of their private signals while underestimating the value of public information." — Source: [Investor Psychology and Security Market Under- and Overreactions]

- On Trading Volume: "High trading volume in financial markets is largely driven by overconfidence; rational agents with identical priors and no liquidity needs would rarely trade with one another." — Source: [Overconfident Investors, Predictable Returns, and Excessive Trading]

- On Expert Calibration: "Overconfidence is not uniform; it is most severe in complex tasks where feedback is slow or ambiguous, making finance a prime environment for psychological biases." — Source: [Overconfidence, Arbitrage, and Equilibrium Asset Pricing]

- On the Illusion of Control: "When investors feel they have actively researched a stock, their confidence in the outcome increases far more than the actual accuracy of their prediction." — Source: [Investor Psychology and Security Market Under- and Overreactions]

- On Market Efficiency: "Anomalies in asset returns are not necessarily proof of shifting risk premiums; they often reflect the predictable errors of overconfident traders interacting with limits to arbitrage." — Source: [Overconfidence, Arbitrage, and Equilibrium Asset Pricing]

- On Limits to Arbitrage: "Rational arbitrageurs cannot fully correct the mispricing caused by overconfident investors because they face severe risks and constraints, allowing behavioral inefficiencies to persist." — Source: [Overconfident Investors, Predictable Returns, and Excessive Trading]

- On the Roots of Mispricing: "Mispricing is fundamentally a struggle between the biased private valuations of confident noise traders and the constrained capital of rational arbitrageurs." — Source: [Overconfidence, Arbitrage, and Equilibrium Asset Pricing]

- On Intangible Information: "Markets struggle most with pricing intangible information, where the variance of interpretation is high and overconfidence can heavily influence the consensus." — Source: [Value Investing with Legends Podcast]

- On Risk vs. Behavior: "Attempts to explain all market anomalies through rational, risk-based frameworks often require assuming highly implausible variations in the risk aversion of the average investor." — Source: [Overconfident Investors, Predictable Returns, and Excessive Trading]

- On Information Processing: "The issue is not a lack of information in modern markets, but rather the biased heuristic processes by which market participants weight and integrate that information." — Source: [Investor Psychology and Security Market Under- and Overreactions]

Part 2: Self-Attribution Bias and Market Dynamics

- On Asymmetric Learning: "Individuals suffer from biased self-attribution: they attribute investment successes to their own skill and dismiss failures as bad luck." — Source: [Investor Psychology and Security Market Under- and Overreactions]

- On Momentum's Origin: "Momentum in stock prices can be explained by delayed overreaction; as confirming public information arrives, investor confidence rises, pushing prices further away from fundamentals." — Source: [Investor Psychology and Security Market Under- and Overreactions]

- On Reversals: "Long-term return reversals occur when the accumulated overreaction of overconfident investors finally corrects as fundamental value reasserts itself." — Source: [Investor Psychology and Security Market Under- and Overreactions]

- On Earnings Announcements: "Post-earnings announcement drift is a classic symptom of underreaction, where investors anchor on their prior beliefs and fail to adequately update upon seeing new, contradictory public data." — Source: [Overconfident Investors, Predictable Returns, and Excessive Trading]

- On the Dynamics of Confidence: "Confidence is not static; it scales up as trades move in the investor's favor, continuously fueling the momentum effect until the overreaction breaks." — Source: [Investor Psychology and Security Market Under- and Overreactions]

- On Public vs. Private Signals: "When public news confirms an investor's private thesis, their confidence jumps. When it contradicts, their confidence barely moves, leading to a ratchet effect in market pricing." — Source: [Overconfidence, Arbitrage, and Equilibrium Asset Pricing]

- On the Limits of Learning: "Self-attribution bias prevents markets from strictly learning over time, as traders fail to accurately calibrate their own forecasting errors." — Source: [Investor Psychology and Security Market Under- and Overreactions]

- On Market Bubbles: "Bubbles are the aggregate manifestation of self-attribution bias operating at scale, where a sequence of confirming signals creates widespread, unjustified conviction." — Source: [Overconfident Investors, Predictable Returns, and Excessive Trading]

- On the Life Cycle of a Trade: "The predictable lifecycle of a behavioral anomaly is short-lag underreaction followed by long-lag overreaction and eventual reversal." — Source: [Investor Psychology and Security Market Under- and Overreactions]

- On Rational Arbitrage: "Arbitrageurs often ride the trend created by overconfident investors rather than correcting it immediately, which exacerbates the momentum effect." — Source: [Overconfidence, Arbitrage, and Equilibrium Asset Pricing]

Part 3: Momentum Crashes

- On the Vulnerability of Momentum: "While momentum has historically generated high average returns, it is susceptible to rare but catastrophic losses that can wipe out years of accumulated gains." — Source: [Momentum Crashes]

- On Panic States: "Momentum crashes do not happen in normal environments; they occur in 'panic' states, typically following multi-year market drawdowns when market volatility is extremely high." — Source: [Momentum Crashes]

- On the Rebound Effect: "The most severe momentum losses happen precisely when a battered market suddenly rebounds, causing the 'loser' portfolio to skyrocket." — Source: [Momentum Crashes]

- On the Beta of Losers: "In bear markets, the 'loser' stocks in a momentum portfolio take on high market betas, making the short leg of the momentum trade highly geared to a market recovery." — Source: [Momentum Crashes]

- On the Call Option Analogy: "Holding a standard momentum portfolio in a panic state is akin to writing an out-of-the-money call option on the market; the upside is limited, but the downside in a rebound is severe." — Source: [Momentum Crashes]

- On Forecasting Crashes: "Because crashes are tied to identifiable market states—specifically high volatility following bear markets—they are partially forecastable." — Source: [Momentum Crashes]

- On 1932 and 2009: "The mechanics of the momentum crash in 2009 were almost identical to the crash in 1932, driven by the explosive mean-reversion of distressed stocks when credit conditions improved." — Source: [Momentum Crashes]

- On Asymmetric Risk: "The distribution of momentum returns is deeply negatively skewed; it behaves like an insurance selling strategy that collects small premiums but occasionally pays out a massive claim." — Source: [Momentum Crashes]

- On the Risk Premium Debate: "The severity and specific timing of momentum crashes cast doubt on the idea that momentum is simply a reward for bearing macroeconomic risk." — Source: [Momentum Crashes]

- On Liquidity and Reversals: "During a crash, the short covering of distressed losers creates a liquidity vacuum, accelerating the violent upward trajectory of the poorest quality stocks." — Source: [Momentum Crashes]

Part 4: Dynamic Strategies and Tail Risk

- On Dynamic Momentum: "By dynamically scaling momentum exposure based on the ex-ante forecast of mean and variance, investors can largely avoid crashes and significantly improve the strategy's Sharpe ratio." — Source: [Momentum Crashes]

- On Volatility Scaling: "Constant-weight strategies ignore the time-varying nature of risk; scaling exposure inversely to forecasted volatility is essential for surviving extreme market environments." — Source: [Momentum Crashes]

- On Hidden Markov Models: "Using hidden Markov models allows us to empirically identify 'turbulent' versus 'calm' market states, providing a more robust framework for managing tail risk." — Source: [Tail Risk in Momentum Strategy Returns]

- On Tail Risk Management: "Risk management in quantitative strategies is not just about reducing volatility; it is about specifically truncating the left tail of the return distribution during regime shifts." — Source: [Tail Risk in Momentum Strategy Returns]

- On Strategy Design: "A well-designed factor strategy must actively account for the conditional distribution of its returns, rather than assuming a static normal distribution." — Source: [Momentum Crashes]

- On the Value of Timing: "While broadly timing the market is difficult, timing the exposure to specific factors like momentum based on observable market stress is both feasible and necessary." — Source: [Momentum Crashes]

- On Adaptive Investing: "Quantitative investing requires adaptability; strategies must be built to recognize when the structural relationship between assets has temporarily broken down." — Source: [Tail Risk in Momentum Strategy Returns]

- On the Cost of Hedging: "Static tail-risk hedging can be an expensive drag on portfolio performance; dynamic factor scaling often provides a more cost-effective method of downside protection." — Source: [Tail Risk in Momentum Strategy Returns]

- On Realized Variance: "Spikes in realized market variance are one of the strongest leading indicators that a momentum portfolio is exposed to severe crash risk." — Source: [Momentum Crashes]

Part 5: Characteristics vs. Covariances

- On Firm Characteristics: "It is the characteristics of firms—such as their size and book-to-market ratios—that drive expected returns, not the covariance structure of their returns." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On the Fama-French Model: "The Fama-French factors appear to price assets successfully because factor loadings are highly correlated with firm characteristics, but when you separate the two, characteristics win out." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On the Risk Premium Assumption: "If returns are driven by characteristics rather than covariances, it challenges the fundamental assumption that value and size premiums are compensation for bearing systematic risk." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On Distressed Firms: "The value premium is often attributed to distress risk, but even non-distressed firms with high book-to-market ratios exhibit the same return premiums, pointing toward behavioral mispricing rather than risk." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On Factor Loadings: "Stocks with similar characteristics but different loadings on the HML or SMB factors do not exhibit significantly different returns." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On Empirical Asset Pricing: "Empirical asset pricing must be careful not to conflate statistical factor structures with true economic risk factors; a factor can explain variance without explaining the risk premium." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On Portfolio Construction: "When building portfolios, grouping stocks strictly by their covariances is less effective for capturing premiums than sorting them directly by their underlying accounting characteristics." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On the Value Premium: "The value anomaly is better understood through the lens of investor overextrapolation of past growth rates rather than compensation for holding risky, distressed assets." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On the Evolution of Factors: "The debate between characteristics and covariances forces the industry to rigorously justify whether a new factor is a genuine risk exposure or simply a proxy for behavioral mispricing." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

Part 6: Quantitative Investing and Strategy Decay

- On Strategy Conviction: "You can't blindly abandon a strategy just because it has suffered a drawdown; you have to evaluate if the underlying economic rationale still holds." — Source: [Robeco Quant Quarterly Interview]

- On Factor Persistence: "Factors like value and momentum have endured for decades precisely because they are rooted in fundamental human behavioral biases that are difficult to arbitrage away." — Source: [Robeco Quant Quarterly Interview]

- On Data Mining: "The financial industry is plagued by data mining; separating a true structural anomaly from statistical noise requires a strong prior theoretical framework." — Source: [Value Investing with Legends Podcast]

- On Institutional Pressures: "Asset managers often abandon sound quantitative strategies at exactly the wrong time due to the career risk associated with prolonged periods of underperformance." — Source: [Robeco Quant Quarterly Interview]

- On Strategy Decay: "Anomalies decay when capital flows into them, but behavioral anomalies decay much slower than structural arbitrage opportunities because the 'dumb money' constantly replenishes the mispricing." — Source: [Overconfident Investors, Predictable Returns, and Excessive Trading]

- On Out-of-Sample Testing: "A quantitative strategy is only as good as its out-of-sample performance; in-sample backtests are mostly an exercise in fitting historical noise." — Source: [Value Investing with Legends Podcast]

- On the Limits of Arbitrage: "Arbitrage is heavily constrained by margin requirements, liquidity limits, and the fundamental risk that prices can diverge further from fair value before they converge." — Source: [Overconfidence, Arbitrage, and Equilibrium Asset Pricing]

- On Separating Signal from Noise: "Quantitative research must focus on the economic friction or behavioral bias that creates the signal, rather than just the statistical significance of the backtest." — Source: [Robeco Quant Quarterly Interview]

- On Process over Outcomes: "In quantitative investing, the focus must remain strictly on the integrity of the process; short-term outcomes are heavily dominated by variance." — Source: [Value Investing with Legends Podcast]

Part 7: Climate Uncertainty and Carbon Pricing

- On Applying Asset Pricing to Climate: "Climate change is fundamentally a risk management problem; determining the social cost of carbon requires applying the same asset pricing tools we use for financial uncertainty." — Source: [Declining CO2 Price Paths]

- On the Risk Premium of Carbon: "Because climate damages are likely to be severe in states of the world where consumption is already depressed, carbon emissions carry a massive risk premium." — Source: [Declining CO2 Price Paths]

- On the Cost of Delay: "Delaying climate action drastically increases the probability of catastrophic tail risks, meaning the optimal price of carbon should be high today, not later." — Source: [Declining CO2 Price Paths]

- On the EZ-Climate Model: "By incorporating Epstein-Zin preferences into climate models, we can capture society's aversion to both risk over time and uncertainty across different climate states." — Source: [Declining CO2 Price Paths]

- On Declining Price Paths: "Contrary to standard models that suggest slowly raising carbon taxes, a risk-based approach dictates a high initial price that declines as uncertainty is resolved." — Source: [Declining CO2 Price Paths]

- On Tail Risks in Climate Outcomes: "Traditional integrated assessment models fail because they use certainty-equivalent assumptions; climate economics must center on the extreme, irreversible tail events." — Source: [Declining CO2 Price Paths]

- On the Role of Insurance: "Investing in emissions reductions today is economically identical to purchasing insurance against catastrophic consumption losses in the future." — Source: [Declining CO2 Price Paths]

- On Resolving Uncertainty: "As we learn more about the true climate sensitivity over time, the uncertainty premium embedded in the optimal carbon price will naturally decrease." — Source: [Declining CO2 Price Paths]

- On Economic Disruption: "The economic damages from climate change will not be smooth or linear; they will manifest as sudden structural breaks that traditional deterministic models cannot price." — Source: [Declining CO2 Price Paths]

Part 8: Bridging Physics, Academia, and Industry

- On the Physics Background: "A background in physics teaches you to respect empirical data and build models from first principles, an approach that is highly effective for deconstructing financial anomalies." — Source: [Value Investing with Legends Podcast]

- On the Value of Rigorous Modeling: "Behavioral finance must move beyond merely listing psychological biases; it requires rigorous mathematical modeling to trace how those biases aggregate into market prices." — Source: [Overconfidence, Arbitrage, and Equilibrium Asset Pricing]

- On Translating Theory to Practice: "The transition from academia to industry reveals that transaction costs, market impact, and financing constraints often destroy elegant theoretical strategies." — Source: [Value Investing with Legends Podcast]

- On the Complexity of Markets: "Financial markets are vastly more complex than physical systems because the basic units—human beings—change their behavior in response to the models being built." — Source: [Value Investing with Legends Podcast]

- On the Goldman Sachs Experience: "Working in quantitative strategies at scale highlights the brutal difference between a paper portfolio and managing real liquidity during a market dislocation." — Source: [Value Investing with Legends Podcast]

- On the Limits of Elegant Models: "An elegant mathematical model that makes incorrect predictions about the cross-section of returns is useless to a practitioner." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On the Importance of Empirical Evidence: "Finance is an observational science. When the empirical evidence firmly rejects the theory—as with characteristics versus covariances—the theory must be discarded." — Source: [Evidence on the Characteristics of Cross Sectional Variation in Stock Returns]

- On the Evolution of Quantitative Finance: "The next frontier of quantitative finance is not just finding new factors, but understanding the time-varying state of the market that dictates when those factors work." — Source: [Momentum Crashes]

- On Bridging the Gap: "The best academic research in finance is directly informed by the practical frictions observed in the industry, and the best industry strategies are grounded in rigorous academic theory." — Source: [Robeco Quant Quarterly Interview]