Lessons from Kim Lew

Kim Lew is the President and CEO of the Columbia Investment Management Company and the former Chief Investment Officer of the Carnegie Corporation of New York. She approaches institutional portfolios with discipline, insisting that diversity of thought is a strict performance requirement rather than a human resources initiative. This profile details her frameworks for asset allocation, manager selection, and leading teams that actively challenge industry consensus.

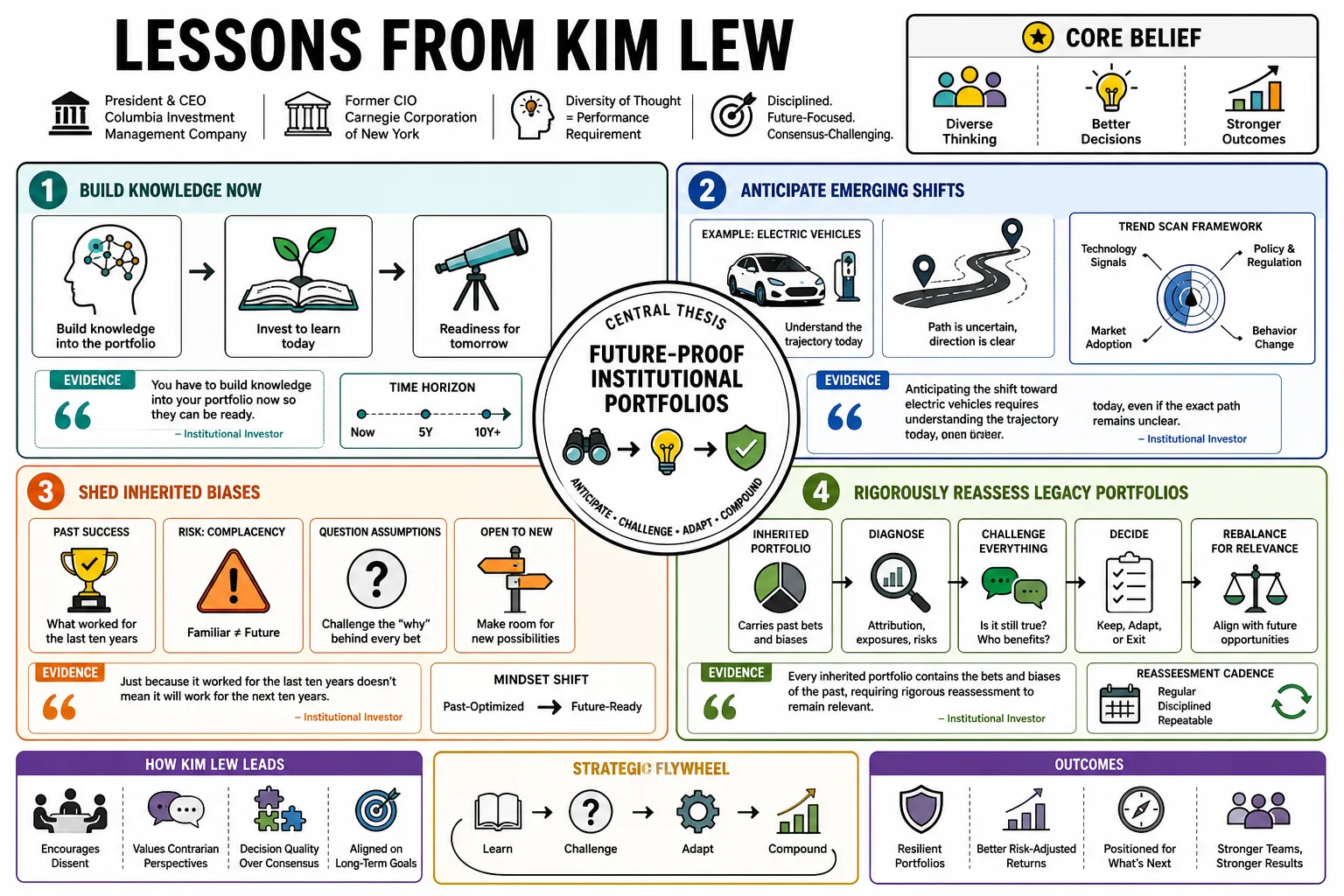

Part 1: Future-Proofing and Long-Term Strategy

- On the goal of future-proofing: "You have to build knowledge into your portfolio now so they can be ready." — Source: Institutional Investor

- On emerging trends: "Anticipating the shift toward electric vehicles requires understanding the trajectory today, even if the exact path remains unclear." — Source: Institutional Investor

- On shedding inherited biases: "Just because it worked for the last ten years doesn't mean it will work for the next ten years." — Source: Institutional Investor

- On evaluating legacy strategies: "Every inherited portfolio contains the bets and biases of the past, requiring rigorous reassessment to remain relevant." — Source: Institutional Investor

- On personalized medicine: "Integrating big ideas like personalized medicine into an endowment ensures the institution is positioned ahead of mass market adoption." — Source: Institutional Investor

- On holding long-term conviction: "You cannot rely solely on historical performance when structural shifts dictate new market realities." — Source: Value Investing with Legends

- On continuous reassessment: "What constitutes a good portfolio today will inevitably drift into mediocrity without active, forward-looking adjustments." — Source: Institutional Investor

- On global shifts: "Tracking the evolving economic importance of regions like Southeast Asia must happen before the themes can be fully executed." — Source: Institutional Investor

- On long-horizon investing: "Building a portfolio for the next decade requires accepting that some investments will take years to prove their thesis." — Source: Value Investing with Legends

- On foundational readiness: "The purpose of future-proofing is not predicting exact outcomes, but ensuring the institution is structurally prepared to act when trends materialize." — Source: Institutional Investor

Part 2: Diversity of Thought as a Performance Imperative

- On defining diversity: "True diversity goes beyond surface-level representation; it must encompass varied social, professional, and life backgrounds." — Source: Charles Skorina & Co.

- On team value: "Diversity of thought is the biggest value of our team." — Source: Carnegie Corporation of New York

- On avoiding echo chambers: "Assembling teams with overlapping life experiences guarantees blind spots and groupthink during critical investment decisions." — Source: Medium

- On the performance imperative: "Diverse decision-making is a strict performance imperative required to generate alpha, rather than a philanthropic exercise." — Source: NMS Management

- On recruiting sources: "Talent and investment ideas must be sourced outside of traditional networks to bring fresh ways of thinking." — Source: Emerging Manager Monthly

- On utilizing perspectives: "Having diverse perspectives is entirely meaningless if the organizational culture does not actively utilize them." — Source: NMS Management

- On navigating modern markets: "A team with different professional experiences is an absolute requirement for decoding modern global market dynamics." — Source: Chief Investment Officer

- On challenging consensus: "The best investment outcomes happen when team members feel empowered to view the world differently than their peers." — Source: Capital Allocators

- On cognitive friction: "A healthy investment team requires the friction of differing opinions to stress-test high-stakes allocations." — Source: Capital Allocators

- On identifying talent: "Proactively seeking varied viewpoints positions an institution to uncover unique insights that others miss." — Source: Charles Skorina & Co.

Part 3: Navigating Risk and Uncertainty

- On structural shocks: "Navigating uncertainty requires organizational adaptability and a detailed understanding of macro dynamics." — Source: Value Investing with Legends

- On balancing markets: Lew treats asset allocation as a role-by-role portfolio problem: public equities, fixed income, alternatives, private equity, venture, and real assets each need to fit the endowment's risk-management job. — Reference: Value Investing with Legends on risk management and asset allocation

- On defining risk: "Risk must be evaluated through the specific mission-driven goals of the organization, separating the needs of an endowment from those of a foundation." — Source: Sapphire Ventures

- On organizational strategy: "Maintaining portfolio resilience requires a durable organizational strategy that can withstand market shocks alongside careful asset allocation." — Source: Value Investing with Legends

- On venture investing: "The risk profile of venture capital requires a specialized approach compared to standard institutional asset classes." — Source: Sapphire Ventures

- On macro risks: Lew links risk management to adaptability, organizational strategy, market dynamics, and understanding global trends rather than treating volatility as a purely mechanical hedging problem. — Reference: Value Investing with Legends on risk management and asset allocation

- On adapting to change: "Adapting quickly to new market realities is a better risk management tool than relying on outdated hedging models." — Source: Value Investing with Legends

- On liquidity management: Lew starts with the university's payout need: the endowment has to fund annual operating costs while preserving enough purchasing power to cover future students and research. — Reference: Bloomberg Wealth interview

- On private credit: "Exploring private credit offers structural protections, but it requires deep due diligence into the specific terms." — Source: CIO Conversations

- On avoiding mediocrity: "I am trying to avoid doing too much at one time and having any of it be mediocre; I want all eyes on it." — Source: Chief Investment Officer

Part 4: Manager Selection and True Partnership

- On true partnership: "A successful allocation requires partnering with firms that possess genuine company-building expertise." — Source: Columbia University

- On due diligence: "Digging into a manager's process means understanding how they think, rather than simply looking at their historical returns." — Source: Capital Allocators

- On venture capital allocations: "Growing a venture capital footprint requires maintaining incredibly high standards for who you let manage your capital." — Source: Chief Investment Officer

- On evaluating conviction: "You must assess whether a manager truly understands their edge or if they are simply riding a favorable market cycle." — Source: Capital Allocators

- On long-term relationships: "The best manager relationships are built on transparency and the ability to navigate poor performance periods together." — Source: Capital Allocators

- On avoiding groupthink in managers: "Selecting managers who all share the same network and background will ultimately concentrate your portfolio risk." — Source: Capital Allocators

- On niche investments: "Exploring new global territories and niche strategies requires finding local managers who possess distinct, specialized knowledge." — Source: Chief Investment Officer

- On assessing talent: "The interview process for managers should reveal how they handle behavioral biases during periods of market stress." — Source: Capital Allocators

- On private asset managers: "Investing in private assets demands a granular understanding of how a firm creates operational value within its portfolio companies." — Source: CIO Conversations

Part 5: Challenging the Status Quo

- On bucking the norm: "Achieving top-tier performance often requires a deliberate willingness to buck the established norms of institutional investing." — Source: Medium

- On contrarian thinking: "Cultivating a contrarian mindset allows an investment team to look for opportunities in areas abandoned by consensus." — Source: Medium

- On breaking routines: "If your investment process looks exactly like every other endowment, your returns will eventually regress to the mean." — Source: Capital Allocators

- On structural changes: "Implementing structural changes within an established organization requires both cultural sensitivity and unwavering conviction." — Source: CIO Conversations

- On reassessing old bets: "You must have the courage to dismantle legacy positions that no longer serve the forward-looking strategy of the portfolio." — Source: Institutional Investor

- On unconventional talent: "Hiring individuals who do not fit the traditional finance mold is a feature of a high-performing team." — Source: Medium

- On standing alone: "True contrarian investing means being comfortable with peer risk and the discomfort of underperforming in the short term." — Source: Value Investing with Legends

- On shifting focus: "Moving capital away from comfortable assets into emerging spaces is necessary to generate future alpha." — Source: Institutional Investor

- On questioning success: "It is dangerous to assume that past success was due entirely to skill; rigorous self-auditing prevents future complacency." — Source: Institutional Investor

Part 6: Intellectual Curiosity and Adaptability

- On the primary trait: "Intellectual curiosity is a foundational trait for successful investors and high-performing teams." — Source: Value Investing with Legends

- On deep research: "Curiosity drives the relentless due diligence necessary to understand shifting market dynamics." — Source: Carnegie Corporation of New York

- On maintaining an edge: "Generating alpha in modern markets requires identifying new areas of opportunity long before they become mainstream." — Source: NMS Management

- On hiring criteria: "When evaluating talent, seeking out individuals who possess a natural drive to ask difficult questions is paramount." — Source: Value Investing with Legends

- On the think tank environment: "Cultivating an atmosphere that functions like a think tank ensures that ideas are debated vigorously and objectively." — Source: Carnegie Corporation of New York

- On continuous learning: "The investment environment changes so rapidly that an unwillingness to learn new sectors is a fatal flaw." — Source: Value Investing with Legends

- On broad perspectives: "Curious minds from diverse backgrounds analyzing the exact same data set create a clear competitive advantage." — Source: NMS Management

- On related fields: "Professionals in investor relations must also be deeply curious to communicate strategies with genuine authority." — Source: Dokumen

- On adapting to change: "Intellectual agility allows a portfolio to survive when historical correlations break down." — Source: Value Investing with Legends

Part 7: Building and Leading Investment Teams

- On leadership environments: "A successful leader cultivates an environment where junior members feel safe challenging the assumptions of senior management." — Source: Medium

- On team structure: "Designing an investment office requires balancing deep sector specialization with a comprehensive view of the overall portfolio." — Source: CIO Conversations

- On the Carnegie Way: "Serving as a training ground for future investment leaders means prioritizing mentorship as highly as immediate returns." — Source: Capital Allocators

- On cultural shifts: "Changing the culture of an established endowment requires patience, clear communication, and leading by example." — Source: CIO Conversations

- On cognitive diversity: "The true test of a leader is their ability to synthesize competing viewpoints without watering down the final decision." — Source: Charles Skorina & Co.

- On empowering staff: "When analysts are given ownership over their ideas, their level of diligence and accountability naturally increases." — Source: Medium

- On overcoming bias: "Conscious and subconscious biases must be actively managed during both the hiring process and manager selection." — Source: Capital Allocators

- On retaining talent: "High-performing individuals stay when they are intellectually stimulated and feel their diverse perspectives actually matter." — Source: NMS Management

- On unified goals: "Every member of the team must deeply understand the mission of the underlying institution to make cohesive decisions." — Source: Sapphire Ventures

Part 8: Asset Allocation and The Role of Endowments

- On mission alignment: Lew says university endowments fund today's students and activities while supporting future students, research, and long-term institutional needs. — Reference: Bloomberg Wealth interview

- On private markets: "Achieving target returns for an endowment increasingly relies on a well-constructed allocation to private equity and venture capital." — Source: Chief Investment Officer

- On foundation versus endowment: "While both are mission-driven, the spending rules and risk tolerance of a foundation dictate a different allocation strategy than a university." — Source: Sapphire Ventures

- On inflation protection: Lew says the endowment job is to earn the payout plus inflation, while also recognizing that older inflation hedges may not work the same way in a changed environment. — Reference: Bloomberg Wealth interview

- On cryptocurrency: Lew says crypto is likely here to stay and may play a role, but Columbia should only dabble enough to learn, build relationships, and understand the expertise before committing serious capital. — Reference: Bloomberg Wealth interview

- On liquidity profiles: Lew argues alternatives fit foundations and endowments because they are long-duration assets; Columbia can accept investments that may take 10 or 20 years to mature because the university expects to exist for centuries. — Reference: Bloomberg Wealth interview

- On strategic patience: "Endowments have the unique structural advantage of being able to wait out market dislocations that force other investors to sell." — Source: Value Investing with Legends

- On portfolio construction: "Adding a new asset class should only be done if it explicitly serves a role that the existing portfolio cannot fulfill." — Source: Chief Investment Officer

- On generational capital: "The ultimate measure of an endowment's success is its ability to fund the institution decades into the future, rather than its year-over-year returns." — Source: Columbia University