Kipp deVeer is the Co-President of Ares Management and the former CEO of Ares Capital Corporation. He is a central figure in the institutionalization of private credit, known for scaling direct lending as traditional banks retreated from middle-market corporate finance. This profile gathers his insights on underwriting discipline, navigating market cycles, and the expansion of alternative investments into the retail wealth channel.

Part 1: The Evolution of Private Credit

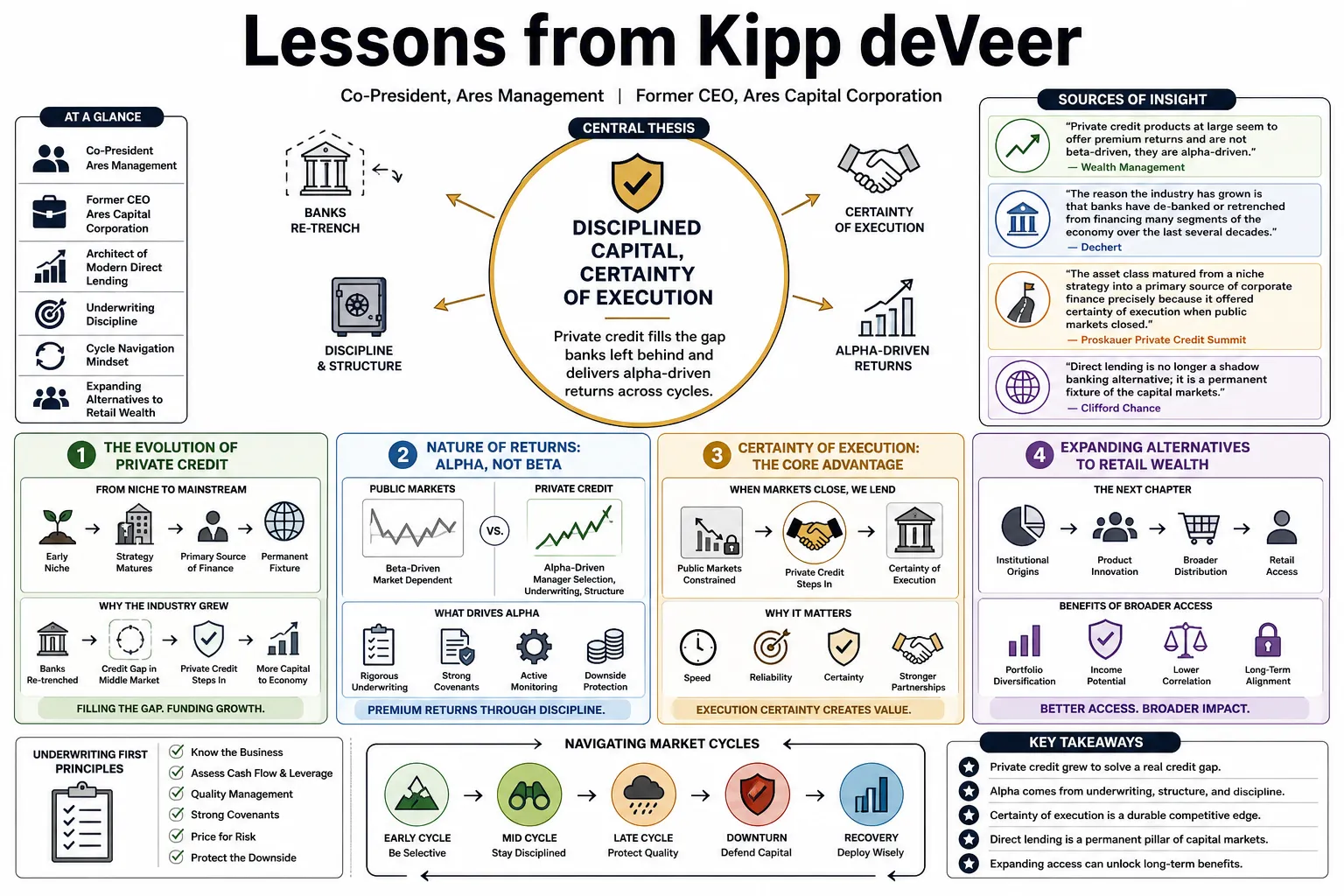

- On the nature of returns: "Private credit products at large seem to offer premium returns and are not beta-driven, they are alpha-driven." — Source: Wealth Management

- On structural market changes: "The reason the industry has grown is that banks have de-banked or retrenched from financing many segments of the economy over the last several decades." — Source: Dechert

- On the origin of direct lending: The asset class matured from a niche strategy into a primary source of corporate finance precisely because it offered certainty of execution when public markets closed. — Source: Proskauer Private Credit Summit

- On industry scale: Direct lending is no longer a shadow banking alternative; it is a permanent fixture of the capital markets that large sponsors rely on for reliable debt financing. — Source: Capital Allocators

- On the democratization of alternatives: Bringing private credit, real estate, and private equity to individual portfolios is a long-term shift that requires extensive financial education. — Source: Private Markets Insights

- On asset allocation: Institutional investors have realized that private credit offers a yield premium for illiquidity that justifies a permanent, growing allocation in their portfolios. — Source: Livewire Live

- On ETF structures: While liquidity is important, the immediate utility of private credit ETFs remains limited, as the underlying assets are fundamentally illiquid and require careful structuring. — Source: Wealth Management

- On market maturation: The private credit market has evolved from providing mezzanine debt to writing massive first-lien checks that historically would have required a large syndicated bank group. — Source: Greenwich Economic Forum

- On sponsor relationships: The growth of private equity directly correlates with the growth of private credit, as sponsors demand large, bespoke capital solutions. — Source: Morningstar

- On competitive advantages: The firms that win in this space are those with the largest balance sheets, the deepest sponsor relationships, and the most robust workout capabilities. — Source: Capital Allocators

Part 2: The Retreat of Traditional Banking

- On bank business models: "With that has come just a lesser interest in dealing with the companies that we deal with that tend to be smaller, middle market companies." — Source: Kalkine

- On regulatory pressure: "We believe that the banks remain constrained on new activity due to concerns regarding both capital and liquidity and which we believe makes our broad range of flexible capital solutions even more valuable." — Source: TMX

- On differing oversight: Banks and asset managers are both highly regulated, but they are regulated differently based on their specific funding sources and structural risks. — Source: Proskauer Private Credit Summit

- On market gaps: When banks exited traditional asset-based strategies, it created an immediate vacuum that non-bank lenders were well-capitalized to fill. — Source: Dechert

- On the changing banking landscape: Banks have grown larger and more concentrated, forcing them to focus on mega-cap clients rather than the middle market. — Source: CNBC Overtime

- On regional bank instability: Periods of stress among regional banks highlight the fragility of the traditional lending model and drive borrowers toward the stability of private capital. — Source: Houlihan Lokey

- On the syndicated market: The syndicated loan market often relies on the ability to distribute risk, which can freeze during volatility, whereas direct lenders hold the risk to maturity. — Source: Private Debt Investor

- On banking partnerships: deVeer argues that private credit does work banks no longer do in smaller companies, while many Ares funds still use bank-provided leverage and match assets to liabilities by duration. — Reference: Proskauer Private Market Talks transcript on bank leverage and private-credit funding

- On structural permanence: The shift away from bank lending is not cyclical; it is a permanent regulatory reality stemming from Dodd-Frank and Basel III. — Source: ECGI

- On borrower preferences: Mid-market companies often prefer private credit because it offers confidentiality, speed, and a single point of contact rather than a fragmented banking syndicate. — Source: Financial Content

Part 3: Underwriting and Risk Discipline

- On managing growth: "Maintaining underwriting discipline amid pro-cyclical flows will determine whether this expansion creates lasting value or repeats past mistakes that damaged investor confidence." — Source: Private Markets Insights

- On market pressure: "Transaction volumes are running below levels from last year and this has increased pressure on some to put capital to work, leading some aggressive behavior and lower quality underwriting by certain market participants." — Source: The Motley Fool

- On portfolio management: Strong historical performance is directly tied to an extensive knowledge of origination, underwriting, and active portfolio management processes. — Source: Portlandic

- On downside protection: The goal of direct lending is to generate consistent investment returns throughout market cycles by placing an absolute emphasis on downside protection. — Source: Morningstar

- On selectivity: During periods of high deal activity, keeping the selectivity rate on new transactions low is the only way to avoid marginal investments. — Source: TMX

- On capital structures: A disciplined underwriter must ensure that borrowers have adequate equity cushions to absorb macroeconomic shocks. — Source: Capital Allocators

- On fundamental analysis: Private credit is driven by fundamental, bottom-up credit analysis rather than macroeconomic timing. — Source: Seeking Alpha

- On avoiding surprises: A successful credit platform operates under the philosophy of trying not to be surprised by underperformance in any given quarter. — Source: Institutional Investor

- On documentation: Covenants and tight loan documentation are critical tools that give lenders a seat at the table before a company's performance deteriorates beyond repair. — Source: Private Debt Investor

Part 4: Navigating Market Volatility

- On finding value: "We continue to see better risk/reward for investment opportunities in the middle market." — Source: Mercer Capital

- On higher rates: While a higher-for-longer interest rate environment generally benefits credit yields, extreme rate volatility can dampen M&A activity and complicate deal pricing. — Source: Financial Content

- On mitigating rate risk: The firm seeks to mitigate volatility associated with interest rate changes through floating-rate investment structures, even though no transaction can fully eliminate risk. — Source: SEC Filings

- On market insulation: Middle-market direct lending tends to be slower to react to broader capital market volatility than liquid, publicly traded credit markets. — Source: Private Debt Investor

- On deploying capital: In CNBC's volatility-focused interview, deVeer discusses the opportunity for private credit amid bank consolidation, rising rates, and a changing deal-activity outlook. — Reference: CNBC Closing Bell Overtime interview on private credit in volatile lending markets

- On consistent income: A diverse portfolio allows a lender to generate consistent income and maintain dividends even when there are bumps along the macroeconomic road. — Source: The Motley Fool

- On avoiding the herd: When transaction volumes drop, it is better to remain inactive than to chase yield by participating in lower-quality deals. — Source: The Motley Fool

- On market resilience: The asset class has proven its resilience across multiple cycles, including the 2008 financial crisis, the 2020 pandemic, and the 2023 rate hikes. — Source: Capital Allocators

- On liquidity: Investors use private credit to seek returns outside the daily price fluctuations of public stock and bond markets. — Source: Business Insider

Part 5: The Middle Market Opportunity

- On scale and leadership: "Driven by our strong origination and risk management capabilities, Ares Capital has been one of the most active direct lending participants in the middle-market for more than 10 years." — Source: Loan Connector

- On crowding in the lower market: "The lower middle market remains quite crowded in our opinion with competitors that lack differentiation and a real ability to compete." — Source: Mercer Capital

- On segment differences: "These upper middle market businesses are very different from lower middle market businesses in terms of resiliency, access to capital and depth of management." — Source: The Motley Fool

- On future deployment: "As we enter 2025, we believe we are well positioned for what we expect will be an increasingly active investing market for acquisition finance and growth capital opportunities." — Source: Zacks

- On the core borrower: deVeer describes Ares direct lending as financing leveraged companies across a wide EBITDA range by underwriting forecasts and whether each company can make interest payments and execute its plans. — Reference: Proskauer Private Market Talks transcript on underwriting leveraged companies

- On value creation: Providing flexible capital to middle-market companies supports local businesses, creates jobs, and generates value for communities. — Source: Morningstar

- On origination networks: Winning in the middle market requires a massive, decentralized origination network capable of sourcing deals that are not broadly marketed. — Source: Capital Allocators

- On the sponsor premium: Competition in mid-market sponsored deals is intense, leading to a widening gap between sponsor-backed and non-sponsor deals in terms of pricing and covenants. — Source: Private Debt Investor

- On incumbent advantages: Being an incumbent lender to a middle-market company provides an informational advantage that leads to safer, more profitable follow-on investments. — Source: Seeking Alpha

Part 6: Retail Investors and the Wealth Channel

- On manager selection: "If you're an FA... most of the FAs we talk to will say, I want three to five managers that have a pretty well curated set of products." — Source: Private Markets Insights

- On the risks of retailization: "Growth that's too fast with not enough education, that's just not good for the growth of this industry." — Source: Private Markets Insights

- On industry responsibility: The private wealth revolution in alternatives represents both the industry's greatest opportunity to scale and its biggest inherent risk if products are mis-sold. — Source: Private Markets Insights

- On advisor education: Financial advisors need deep education on the illiquidity premium and the mechanical differences between private credit and public bonds. — Source: CAIS Live

- On brand recognition: Retail investors and advisors tend to gravitate toward established, institutional brands that have managed capital through multiple credit cycles. — Source: Capital Allocators

- On portfolio construction: Including private credit in a retail portfolio provides an income-generating anchor that reduces overall reliance on the 60/40 equity-to-bond model. — Source: Greenwich Economic Forum

- On structural vehicles: BDCs and non-traded REITs are the primary vehicles allowing retail investors to access institutional-grade private markets. — Source: Wealth Management

- On liquidity expectations: It is critical to align the liquidity terms of retail products with the fundamental illiquidity of the underlying middle-market loans. — Source: Capital Allocators

- On distribution scaling: Capital Allocators frames Ares' private-wealth buildout around dedicated resources, scaling distribution, servicing financial advisors, building brand recognition, and maintaining underwriting discipline during growth. — Reference: Capital Allocators episode notes on scaling private wealth globally in credit

Part 7: Managing Defaults and Portfolio Health

- On portfolio resilience: "It's really difficult to have an impact in any way, shape or form on our Company's operating profile with a single or even a couple of defaults, even in larger names." — Source: The Motley Fool

- On granting concessions: Lenders must carefully evaluate the risk and reward of granting additional concessions to struggling borrowers. — Source: The Motley Fool

- On default correlation: Analyzing the likelihood that loans in a portfolio might default at the same time is a core component of defensive portfolio construction. — Source: The Motley Fool

- On sponsor support: When a portfolio company struggles, a lender expects the private equity sponsor to step up and inject fresh equity to support the business. — Source: Institutional Investor

- On proactive restructuring: The best outcomes in distressed situations occur when lenders take a proactive, hands-on approach to restructuring the balance sheet early. — Source: Capital Allocators

- On recovery rates: Private credit historically enjoys higher recovery rates in the event of default compared to syndicated loans due to tighter documentation and smaller lender groups. — Source: Proskauer Private Credit Summit

- On credit deterioration: Monitoring early warning signs, such as tightening margins or delayed reporting, allows lenders to intervene before a technical default occurs. — Source: Seeking Alpha

- On diversification: A highly diversified portfolio across industries and vintage years is the best mathematical defense against localized economic shocks. — Source: SEC Filings

- On holding the pen: Direct lenders have a structural advantage in restructurings because they control the voting blocks and dictate the terms of the workout. — Source: Capital Allocators

- On absorbing losses: A well-underwritten portfolio generates enough current income to easily absorb the inevitable, idiosyncratic credit losses that occur in lending. — Source: The Motley Fool

Part 8: The Future of Alternatives and Direct Lending

- On infrastructure debt: "Over the last four years, our Infrastructure Debt strategy has reinforced its differentiated capabilities and scale... with a continued focus on directly originated investments." — Source: TMX

- On global expansion: The private credit model, initially perfected in the US, is rapidly scaling across Europe and Asia as companies globally seek alternative financing. — Source: Capital Allocators

- On new asset classes: Alternative asset managers are successfully applying the direct lending playbook to adjacent asset classes, including real estate debt and sports/media financing. — Source: Livewire Live

- On insurance capital: The convergence of private credit and the insurance industry provides permanent, long-dated capital that perfectly matches the duration of illiquid loans. — Source: Greenwich Economic Forum

- On team building: "She brings a wealth of experience and deep relationships that will help to further cultivate our network of strong banking partnerships and advance our origination efforts." — Source: Pulse 2.0

- On competitive moats: deVeer points to scale advantages in direct lending: broader borrower reach, larger EBITDA financing capacity, deeper origination, stronger teams, better deal flow, and longer relationships with companies. — Reference: Proskauer Private Market Talks transcript on scale advantages in direct lending

- On technological efficiency: As the asset class scales, investing in data analytics and portfolio management software becomes a critical differentiator for large alternative managers. — Source: Capital Allocators

- On economic cycles: Direct lending is no longer a bull-market phenomenon; it has matured into an all-weather asset class that performs regardless of the macroeconomic backdrop. — Source: CNBC Overtime

- On the end goal: deVeer describes Ares Credit as spanning loans, high yield, U.S. and European direct lending, opportunistic credit, and alternative credit strategies that lend against or buy contractual credit cash flows. — Reference: Proskauer Private Market Talks transcript on Ares Credit and alternative credit