Lessons from Kristin Gilbertson

Kristin Gilbertson is the Chief Investment Officer at Access Industries and the former CIO of the University of Pennsylvania's endowment. She is known for a strict approach to liquidity: her high cash and Treasury reserves allowed Penn to meet its capital calls during the 2008 financial crisis. This profile covers her methods for asset allocation, manager selection, and moving from an endowment to a family office.

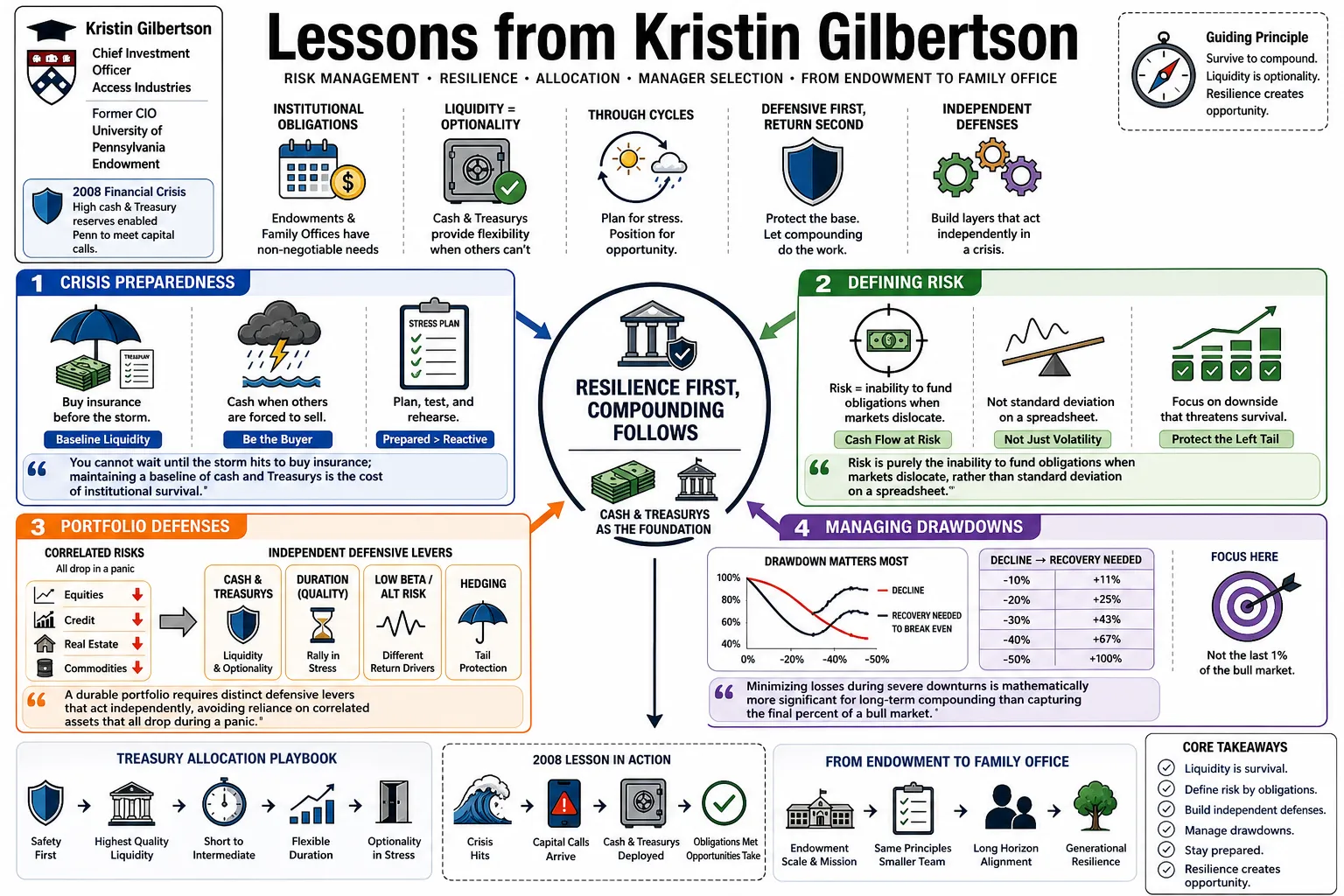

Part 1: Risk Management and Resilience

- On Crisis Preparedness: "You cannot wait until the storm hits to buy insurance; maintaining a baseline of cash and Treasurys is the cost of institutional survival." — Source: [University of Pennsylvania Almanac]

- On Defining Risk: "Risk is purely the inability to fund obligations when markets dislocate, rather than standard deviation on a spreadsheet." — Source: [Value Investing with Legends Podcast]

- On Portfolio Defenses: "A durable portfolio requires distinct defensive levers that act independently, avoiding reliance on correlated assets that all drop during a panic." — Source: [Chief Investment Officer Magazine]

- On Managing Drawdowns: "Minimizing losses during severe downturns is mathematically more significant for long-term compounding than capturing the final percent of a bull market." — Source: [Columbia Business School Directory]

- On Treasury Bonds: "High-quality sovereign debt is often derided in bull markets, yet it provides the exact liquidity needed when everything else freezes." — Source: [University of Pennsylvania Almanac]

- On Tail Risks: "Institutional investors must underwrite tail risks systematically, acknowledging that low-probability events happen more frequently than models suggest." — Source: [Value Investing with Legends Podcast]

- On Market Timing: "Tactical shifts are about recognizing when risk premiums no longer compensate you for the exposure, rather than calling the exact top or bottom." — Source: [Chief Investment Officer Magazine]

- On Liquidity Illusions: "Assets are only liquid when someone is willing to buy them at a reasonable price, regardless of what an internal model dictates." — Source: [Value Investing with Legends Podcast]

- On Structural Resilience: "A resilient portfolio is built on a foundation of structural liquidity that matches the organization's real-world cash needs." — Source: [Columbia Business School Directory]

Part 2: Endowment Strategy and Asset Allocation

- On the Endowment Model: "The traditional endowment model of heavy alternative investments works best only when you have the liquidity to survive the lock-up periods." — Source: [Chief Investment Officer Magazine]

- On Asset Allocation: "Strategic asset allocation should reflect the specific operational realities of the institution, instead of mimicking a peer group's average." — Source: [University of Pennsylvania Almanac]

- On Alternative Assets: "It is a mistake to race blindly into illiquid alternatives simply because other ivy league endowments are doing so." — Source: [Value Investing with Legends Podcast]

- On Rebalancing: "Disciplined rebalancing forces you to sell what has done well and buy what is hated, which is psychologically difficult but financially necessary." — Source: [Columbia Business School Directory]

- On Policy Portfolios: "The policy portfolio is the anchor; deviations from it must clear a very high hurdle of conviction and expected return." — Source: [Access Industries Profile]

- On Inflation Protection: "Endowments operate in perpetuity, making the preservation of purchasing power against inflation a primary objective." — Source: [University of Pennsylvania Almanac]

- On Private Equity Returns: "The illiquidity premium in private markets must be substantial enough to justify the loss of flexibility." — Source: [Chief Investment Officer Magazine]

- On Peer Comparison: "Chasing the returns of peer institutions can lead to misaligned risk profiles and unintended portfolio concentrations." — Source: [Value Investing with Legends Podcast]

- On Real Assets: "Tangible assets provide a specific type of diversification that financial engineering cannot replicate in an inflationary environment." — Source: [Access Industries Profile]

- On Institutional Constraints: "Every investment strategy must be tailored to the specific constraints of the capital pool, whether it is a university payout or a family's operating businesses." — Source: [Columbia Business School Directory]

Part 3: Navigating the 2008 Financial Crisis

- On Capital Calls: "When private equity managers issue capital calls during a crisis, you must have the unencumbered cash ready or face devastating defaults." — Source: [Value Investing with Legends Podcast]

- On Early Adjustments: "Taking risk off the table early in 2008 by reducing public equity exposure was driven by a focus on preserving the university's operating budget." — Source: [University of Pennsylvania Almanac]

- On Holding Cash: "Maintaining a 15% allocation in cash and Treasurys acted as the mechanism that allowed us to be opportunistic when others were forced sellers." — Source: [Chief Investment Officer Magazine]

- On Secondary Markets: "A crisis often reveals the true clearing price of private assets, which usually rests far below the last marked valuation." — Source: [Value Investing with Legends Podcast]

- On Board Communication: "In times of severe market stress, over-communicating with the investment committee is required to prevent panic-driven changes to the policy portfolio." — Source: [Columbia Business School Directory]

- On Stress Testing: "You have to stress test the portfolio against scenarios that seem historically impossible, because markets eventually break historical bounds." — Source: [University of Pennsylvania Almanac]

- On Survival: "During 2008, the goal shifted from maximizing alpha to ensuring the basic fiduciary survival of the institution's funding mechanisms." — Source: [Chief Investment Officer Magazine]

- On Counterparty Risk: "The crisis taught us that the identity and financial health of the institution holding your assets matters equally to the assets themselves." — Source: [Access Industries Profile]

- On Post-Crisis Opportunities: "The best vintages for private investments are often raised during the depths of a recession, but participation requires protecting your liquidity beforehand." — Source: [Value Investing with Legends Podcast]

Part 4: Family Office Investing Dynamics

- On Capital Duration: "Family office capital has an entirely different duration and tax profile compared to a tax-exempt university endowment, changing how returns are compounded." — Source: [Access Industries Profile]

- On Direct Investing: "Family offices often have the flexibility to make direct investments alongside their managers, capturing economics that funds cannot." — Source: [Value Investing with Legends Podcast]

- On Concentrated Bets: "Unlike an endowment, a single-family office can afford to take highly concentrated bets if they align with the principal's specific expertise." — Source: [Columbia Business School Directory]

- On Speed of Execution: "The lack of bureaucratic committees allows family offices to deploy capital rapidly when market dislocations occur." — Source: [Access Industries Profile]

- On Aligning Structures: "Investing for a family requires understanding the intersection of their operating businesses, their philanthropic goals, and their generational wealth transfer plans." — Source: [Value Investing with Legends Podcast]

- On Permanent Capital: "True permanent capital doesn't face arbitrary redemption pressures, allowing it to capture the premium of long-term illiquidity." — Source: [Chief Investment Officer Magazine]

- On Sourcing: "In the family office space, sourcing is often driven by the principal's global network, requiring the CIO to evaluate highly idiosyncratic deals." — Source: [Columbia Business School Directory]

- On Tax Efficiency: "Every basis point of return in a family office must be evaluated on an after-tax basis, fundamentally altering asset allocation models." — Source: [Access Industries Profile]

- On Fiduciary Duty: "The fiduciary duty in a family office is deeply personal; you are directly managing the legacy and security of an individual and their heirs." — Source: [Value Investing with Legends Podcast]

Part 5: Manager Selection and Partnerships

- On Evaluating Managers: "We look for managers who have a definable edge and a repeatable process, avoiding those with a track record of simply being in the right sector at the right time." — Source: [Columbia Business School Directory]

- On Alignment of Interests: "The fee structure must ensure that the manager gets wealthy by delivering returns to the LP rather than by gathering assets." — Source: [Chief Investment Officer Magazine]

- On Sizing Allocations: "An allocation must be large enough to move the needle for your portfolio, but small enough that you can withstand the manager being wrong." — Source: [Value Investing with Legends Podcast]

- On Manager Turnover: "Firing a manager is often harder than hiring one, but you must act decisively when the thesis for their inclusion is broken." — Source: [University of Pennsylvania Almanac]

- On Niche Strategies: "Outsized returns often come from managers operating in capacity-constrained niches that are too small for mega-funds to target." — Source: [Access Industries Profile]

- On Diligence: "True due diligence involves understanding how a manager behaved when things went wrong, completely separate from reviewing their winning trades." — Source: [Value Investing with Legends Podcast]

- On Co-investments: "Co-investments are attractive for reducing fee drag, but they require the internal staff to have the underwriting capabilities of a direct investor." — Source: [Columbia Business School Directory]

- On Style Drift: "A manager who suddenly changes their strategy to chase a hot sector is signaling a lack of discipline; style drift is a primary reason to redeem." — Source: [Chief Investment Officer Magazine]

- On Emerging Managers: "Backing a hungry, emerging manager often yields better alignment than allocating to a legacy firm that has transitioned into an asset gatherer." — Source: [Value Investing with Legends Podcast]

- On Transparency: "You cannot invest with a manager who treats their portfolio like a black box; transparency is required to understand your aggregate risk." — Source: [Access Industries Profile]

Part 6: Public Equities and Market Efficiency

- On Market Efficiency: "Public markets are highly efficient at pricing widely available information, meaning your edge must come from duration, behavior, or deep structural analysis." — Source: [Columbia Business School Directory]

- On Active Management: "The default should be passive indexation in highly efficient markets, reserving active management fees for areas with structural inefficiencies." — Source: [Value Investing with Legends Podcast]

- On Mega-Cap Valuations: "Concentration in mega-cap technology stocks creates index-level risks that must be actively managed by institutional allocators." — Source: [Access Industries Profile]

- On Emerging Markets: "Investing in emerging markets requires a different framework for assessing political risk and rule-of-law than developed markets." — Source: [Chief Investment Officer Magazine]

- On Factor Investing: "Understanding the underlying factor exposures of your active managers is necessary to ensure you aren't paying alpha fees for beta returns." — Source: [University of Pennsylvania Almanac]

- On Behavioral Biases: "The greatest advantage in public equities is often structural patience, which allows an investor to hold an out-of-favor asset longer than the market expects." — Source: [Value Investing with Legends Podcast]

- On ETFs: "Exchange-traded funds are excellent tools for swift, low-cost tactical asset allocation adjustments without disrupting the core manager roster." — Source: [Columbia Business School Directory]

- On Corporate Governance: "A company's governance structure is a direct leading indicator of how minority shareholders will be treated during a downturn." — Source: [Access Industries Profile]

- On Volatility: "Volatility in public markets is the price of admission for liquidity, and it should be harvested rather than feared." — Source: [Chief Investment Officer Magazine]

Part 7: Liquidity and Capital Calls

- On the Price of Liquidity: "Liquidity is an asset class of its own, and you must demand a premium when you give it up in private markets." — Source: [Value Investing with Legends Podcast]

- On Capital Call Modeling: "Unfunded commitments must be modeled against the worst-case scenario of public market drawdowns, rather than average historical pacing." — Source: [Columbia Business School Directory]

- On Cash Drag: "The perceived cash drag in a bull market is actually the insurance premium you pay to maintain optionality in a bear market." — Source: [University of Pennsylvania Almanac]

- On Distressed Selling: "The quickest way to destroy an endowment is being forced to sell illiquid assets at a steep discount to meet immediate payout needs." — Source: [Chief Investment Officer Magazine]

- On Lock-ups: "Long lock-up periods only make sense if the underlying asset fundamentally requires time to mature or execute a turnaround." — Source: [Access Industries Profile]

- On Pacing Models: "Vintage year diversification is mandatory; you cannot pause your private market commitments during a recession without breaking the pacing model." — Source: [Value Investing with Legends Podcast]

- On Distributions: "Relying on distributions from private equity to fund new capital calls works fine until the exit window closes simultaneously for all managers." — Source: [Columbia Business School Directory]

- On Market Freezes: "When spreads widen and credit markets freeze, having uncommitted capital allows you to act as a liquidity provider to desperate sellers." — Source: [University of Pennsylvania Almanac]

- On Absolute Return Strategies: "Hedge funds should be evaluated on their ability to provide uncorrelated absolute returns and liquidity, completely separate from acting as leveraged equity." — Source: [Chief Investment Officer Magazine]

Part 8: Institutional Leadership and Career Building

- On Team Culture: "An effective investment office requires a culture where junior analysts feel empowered to challenge the assumptions of the CIO." — Source: [Columbia Business School Directory]

- On Fiduciary Stewardship: "The role of the CIO is to protect the purchasing power of the institution for future generations, avoiding the temptation to generate headlines with outsized risks." — Source: [University of Pennsylvania Almanac]

- On Board Dynamics: "Managing the investment committee is as important as managing the portfolio; if the board lacks conviction, the strategy will fail under pressure." — Source: [Value Investing with Legends Podcast]

- On Foundational Training: "Starting a career at organizations like the World Bank forces an investor to understand macroeconomic frameworks before picking individual securities." — Source: [Access Industries Profile]

- On Mentorship: "Apprenticeship is the core of investment training; learning how seasoned professionals react to bad news is invaluable." — Source: [Columbia Business School Directory]

- On Intellectual Honesty: "You must have the intellectual honesty to admit when an investment thesis is broken and move on without anchoring to your original cost." — Source: [Chief Investment Officer Magazine]

- On Continuous Learning: "The markets are constantly evolving; an investment professional who stops reading and questioning their assumptions will quickly become obsolete." — Source: [Value Investing with Legends Podcast]

- On Hiring Analysts: "I look for intellectual curiosity and an understanding of history; financial modeling can be taught, but judgment takes time to develop." — Source: [Access Industries Profile]

- On Navigating Academia: "Teaching wealth management at the business school level forces a practitioner to translate intuitive decisions into structured, explainable frameworks." — Source: [Columbia Business School Directory]

- On Legacy: "The true measure of a CIO's success is whether the institution is financially stronger and better equipped to handle the next crisis when they leave." — Source: [University of Pennsylvania Almanac]