Lessons from Larry Summers

Larry Summers is a former U.S. Treasury Secretary, director of the National Economic Council, and Harvard University president. He revived the "secular stagnation" theory to explain eras of persistent low growth and interest rates. This document compiles his statements on fiscal policy and technological change to show how he reads the modern economy.

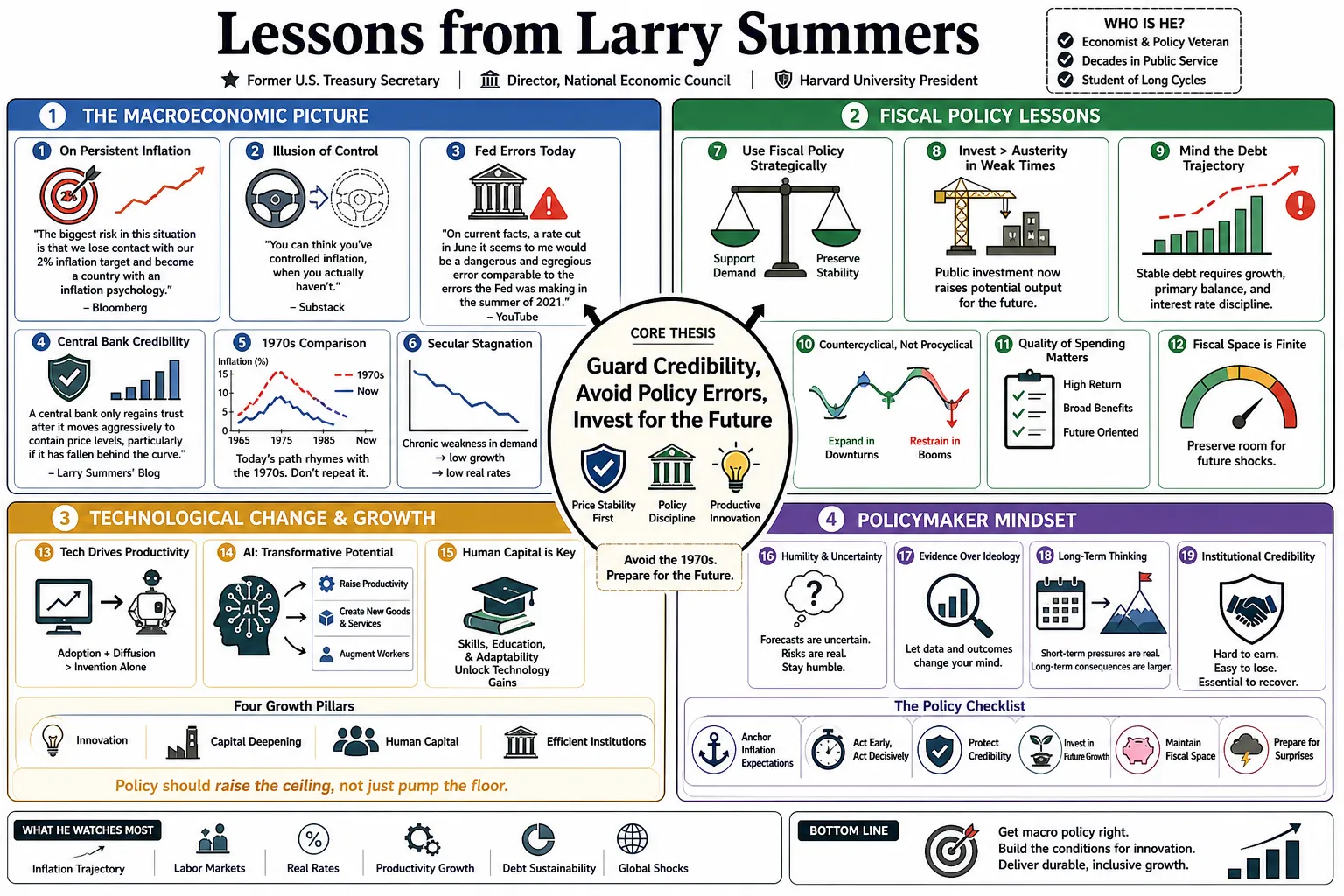

Part 1: The Macroeconomic Picture

- On persistent inflation: "The biggest risk in this situation is that we lose contact with our 2% inflation target and become a country with an inflation psychology." — Source: Bloomberg

- On the illusion of control: "You can think you've controlled inflation, when you actually haven't." — Source: Substack

- On Federal Reserve errors: "On current facts, a rate cut in June it seems to me would be a dangerous and egregious error comparable to the errors the Fed was making in the summer of 2021." — Reference: Harvard Kennedy School summary of Summers on Bloomberg Wall Street Week opposing a June 2024 Fed rate cut

- On central bank credibility: A central bank only regains trust after it moves aggressively to contain price levels, particularly if it has fallen behind the curve. — Source: Larry Summers' Blog

- On the 1970s comparison: Charting the current inflationary trajectory against the 1970s provides a sobering reminder of what happens when central banks lose their grip on price stability. — Source: Semafor

- On transitory inflation: It is a mistake to dismiss rising prices as a temporary consequence of supply chain bottlenecks when large fiscal stimulus is actively deployed. — Source: The Washington Post

- On the inflation-unemployment tradeoff: Policymakers face a dilemma where attempting to ease unemployment too quickly shifts the balance of risk back toward uncontrollable inflation. — Source: Harvard Gazette

- On price controls: Imposing artificial caps on prices to combat inflation addresses the symptom rather than the underlying macroeconomic disease, ultimately leading to shortages. — Source: Project Syndicate

- On fiscal responsibility during expansion: The appropriate time for vast government borrowing is during a profound slump, not when the economy is already straining at full capacity. — Source: Financial Times

- On reading economic indicators: True inflation is often masked by volatile categories, requiring analysts to look beyond headline numbers to understand the entrenched reality of core prices. — Source: The Wall Street Journal

Part 2: Secular Stagnation and Long-Term Growth

- On the defining challenge: "Secular Stagnation—a prolonged period in which satisfactory growth can only be achieved by unsustainable financial conditions—may be the defining macro-economic challenge of our times." — Source: Larry Summers' Blog

- On deflationary risks: "Deflation and secular stagnation are the risks of our time." — Source: World Economic Forum

- On structural sluggishness: The slow recovery from the Great Recession was not merely a temporary hangover but a sign that neutral real interest rates had declined significantly. — Source: Bruegel

- On savings and investment imbalances: When an economy suffers from a persistent excess of saving over investment, the natural tendency is for interest rates to drift dangerously close to the zero lower bound. — Source: American Economic Association

- On updating economic assumptions: Economic facts change, and as neutral interest rates appear higher today, the era of secular stagnation may finally be giving way to a different regime. — Source: Bocconi University

- On demand shortages: The fundamental constraint on economic growth in the twenty-first century has often been a lack of demand rather than a lack of supply capacity. — Source: Foreign Affairs

- On infrastructure investment: The most effective antidote to long-term stagnation is aggressive public investment in infrastructure, which puts excess savings to productive use. — Source: Financial Times

- On demographic headwinds: Aging populations across the developed world inherently drag down aggregate demand, exacerbating the conditions for secular stagnation. — Source: NBER

- On monetary policy limits: Central banks cannot solve secular stagnation alone; when interest rates hit zero, fiscal policy must become the primary engine of macroeconomic stabilization. — Source: Brookings Institution

- On technological stagnation: Despite the rise of digital platforms, the failure to generate broad-based physical productivity gains has contributed heavily to a low-growth environment. — Source: The Atlantic

Part 3: Artificial Intelligence and the Future of Labor

- On the scale of AI's impact: "If one takes a view over the next generation, this could be the biggest thing that has happened in economic history since the Industrial Revolution." — Source: Reddit

- On the uniqueness of AI: "Of course, I think that this [AI] technology potentially has implications greater than any past technology, because fire doesn't make more fire, electricity doesn't make more electricity. But AI has the capacity to be self-improving." — Source: Conversable Economist

- On white-collar displacement: "This offers the prospect of not replacing some forms of human labor, but almost all forms of human labor." — Source: Unusual Whales

- On the rise of emotional intelligence: AI will substitute for a doctor making a difficult diagnosis before it substitutes for a nurse's ability to hold a patient's hand, making emotional intelligence more valuable than IQ. — Source: Reddit

- On the pace of innovation: "The right general rule with respect to technological innovation is that things take longer to happen than you think they will, and then they happen faster than you thought they could." — Source: Unusual Whales

- On the productivity J-curve: We should not expect an immediate productivity miracle from artificial intelligence in the near term, as systemic integration always lags behind invention. — Source: Unusual Whales

- On the last mile of deployment: The most difficult phase of technological disruption is the final stretch of making a new system reliable and accessible to everyday enterprises. — Source: Unusual Whales

- On governance and regulation: Summers argues that AI cannot be left only to developers: companies and society need strong regulation and public oversight to manage safety, national-security, and deployment risks. — Reference: Benzinga report on Summers saying society cannot leave AI only to developers and needs strong regulation

- On cognitive labor: For the first time in history, technology is coming for the people who think and write before it comes for the people who do physical labor. — Source: The New York Times

- On capital versus labor: The proliferation of artificial intelligence threatens to shift the balance of economic returns away from labor and toward those who own the underlying capital and computing power. — Source: Project Syndicate

Part 4: Higher Education and the Role of Universities

- On institutional complacency: An excessive attachment to tradition is the greatest threat to a university's preeminence; institutions must constantly choose between nostalgia and progress. — Source: Harvard Magazine

- On feeling out of place: "For my first six months in the United States Senate, I couldn't figure out why I was there. For the rest of my time in the United States Senate, I couldn't figure out why many of the rest of them were there." — Source: Harvard Gazette

- On the core mission of academia: The primary duty of a university is to act as an engine for new ideas and a training ground for future leaders. — Source: Harvard University

- On economic opportunity in education: Elite universities have a moral responsibility to aggressively reduce financial barriers for low-income families. — Source: Harvard Gazette

- On global engagement: There is no substitute for living abroad if a student wishes to truly understand their own country and the broader complexities of the world. — Source: Harvard Gazette

- On intellectual freedom: A tradition of open debate is necessary to pursue truth, and institutions must prevent political correctness from stifling inquiry. — Source: Harvard Magazine

- On the illusion of average: It is an educational irony that in surveys of highly competitive incoming classes, the vast majority of freshmen believe they are in the bottom half. — Source: Harvard University

- On university governance: Running a university is less about issuing commands and more about persuading deeply independent scholars to row in roughly the same direction. — Source: The Chronicle of Higher Education

- On ideological purity: The university must remain a place where ideas are tested by their validity and rigor, not by their adherence to a prevailing social orthodoxy. — Source: The Wall Street Journal

Part 5: Globalization, Trade, and the World Economy

- On prioritizing efficiency: "Both the officials responsible for competition policy and those responsible for international trade have explicitly rejected economic efficiency as a central guide for economic policy. This, I would suggest, is a costly and consequential error." — Source: The Money Illusion

- On global poverty reduction: "Relative to the time when I was chief economist of the World Bank at the beginning of the 1990s, child mortality rates are less than half of what they were then. Literacy rates are more than twice what they were then." — Source: The Money Illusion

- On protectionism: Erecting tariffs and engaging in trade wars ultimately punishes domestic consumers while failing to protect the industrial jobs of the past. — Source: Financial Times

- On the shifting global center: The center of gravity of the world economy is moving East, requiring the West to adapt its diplomatic and economic strategies. — Source: Three Takeaways

- On global cooperation: The most pressing crises of the twenty-first century, from pandemics to climate change, cannot be solved unilaterally by any single nation. — Source: Foreign Affairs

- On the benefits of free trade: Despite its localized disruptions, global integration remains the most powerful force in human history for lifting populations out of extreme poverty. — Source: World Bank

- On industrial policy: Governments are notoriously poor at picking corporate winners, and state-directed economic planning often results in misallocated capital. — Source: Bloomberg

- On currency markets: A strong national currency is generally in the best interest of a country, reflecting underlying economic health rather than a disadvantage to be manipulated. — Source: The Wall Street Journal

- On emerging markets: The rapid integration of billions of people in Asia into the global market economy is the most significant economic event of our lifetimes. — Source: Project Syndicate

Part 6: Financial Crises and Market Stability

- On financial transparency: "If you ask why the American financial system succeeds, at least my reading of the history would be that there is no innovation more important than that of generally accepted accounting principles." — Source: YourDictionary

- On the nature of panics: Financial crises are rarely caused by a single dramatic failure; they usually result from a slow accumulation of hidden debt. — Source: NBER

- On moral hazard: Bailing out failing institutions without wiping out their equity holders fundamentally distorts the risk-taking behavior of the entire financial system. — Source: Financial Times

- On market discipline: The requirement that companies report their activities on a comparable, standardized basis imposes a necessary discipline on corporate management. — Source: YourDictionary

- On crisis response: In the midst of a severe financial panic, the only viable response for a government is to inject overwhelming liquidity to break the cycle of fear. — Source: The Washington Post

- On regulatory oversight: Financial regulation must evolve continually because markets inevitably seek out the least regulated corners to hide risk. — Source: Bloomberg

- On the housing bubble: The belief that real estate prices could only go up nationally was a collective delusion that blinded regulators and investors alike. — Source: The New York Times

- On capital requirements: Forcing banks to hold significantly more capital is the cheapest and most reliable insurance policy a society can buy against financial ruin. — Source: Project Syndicate

- On the role of the Treasury: The ultimate job of the Treasury during a meltdown is to act as the adult in the room, prioritizing systemic survival over political popularity. — Source: Hoover Institution

Part 7: Human Capital and Inequality

- On information age investments: "If investments in factories were the most important investments in the industrial age, the most important investments in an information age are surely investments in the human brain." — Source: YourDictionary

- On the skills gap: The divergence in economic fortunes is defined by the gap between workers who possess advanced technical skills and those who do not. — Source: Brookings Institution

- On early childhood education: The highest return on investment available to any government is the funding of comprehensive early childhood education programs. — Source: NBER

- On the hollowing of the middle class: The decline of routine manufacturing work has removed the traditional ladder of upward mobility for workers without college degrees. — Source: The Atlantic

- On taxation and inequality: Addressing wealth inequality requires closing loopholes and ensuring that capital gains are taxed as rigorously as wage income. — Source: The Washington Post

- On labor unions: A healthy economy requires a counterweight to corporate power, and the weakening of collective bargaining has contributed to wage stagnation. — Source: The New York Times

- On the cost of college: Expanding access to higher education is meaningless if the cost of attendance sentences a generation to decades of crippling debt. — Source: Harvard Magazine

- On social mobility: A society that fails to provide its poorest children with a legitimate pathway to the middle class is failing its most fundamental economic test. — Source: Project Syndicate

- On female labor force participation: Integrating women fully and equally into the global workforce remains one of the largest untapped opportunities for macroeconomic growth. — Source: World Bank

Part 8: Public Policy and Government Interventions

- On translating theory to reality: The challenge of economic policymaking involves calculating the correct mathematical response and persuading a reluctant political system to implement it. — Source: PBS

- On the limits of government: While government intervention is necessary during crises, continuous micromanagement of private enterprise generally stifles innovation. — Source: Hoover Institution

- On carbon pricing: A predictable, gradually increasing tax on carbon is the most economically efficient mechanism for addressing the threat of climate change. — Source: Financial Times

- On infrastructure decay: Allowing roads, bridges, and airports to crumble while interest rates are low is an act of intergenerational economic malpractice. — Source: The Wall Street Journal

- On tailored communication: Effective leadership in government requires the ability to distill complex macroeconomic models into narratives that make sense to the public. — Source: S&P Global

- On policy trade-offs: Every major economic decision involves choosing between imperfect alternatives, as there are rarely flawless solutions. — Source: Bloomberg

- On evaluating administration policies: When assessing an administration's economic strategy, one must look past the rhetoric and examine the underlying theory of the case driving their resource allocation. — Source: Substack

- On the national debt: While borrowing is justified for productive investments, allowing the structural deficit to balloon during times of peace poses a long-term threat. — Source: The Washington Post

- On intellectual humility: The most dangerous policymakers are those who are completely certain of their models, ignoring the unpredictable reality of human behavior. — Source: The New York Times