Lauren Taylor Wolfe is the co-founder and managing partner of Impactive Capital, an investment firm that applies private equity tactics to public markets. She is recognized for demonstrating that active engagement on environmental, social, and governance issues can directly improve a company's operational efficiency and return on invested capital. This profile compiles her perspectives on collaborative activism, capital allocation, and driving long-term corporate value.

Part 1: The Modern Activist Playbook

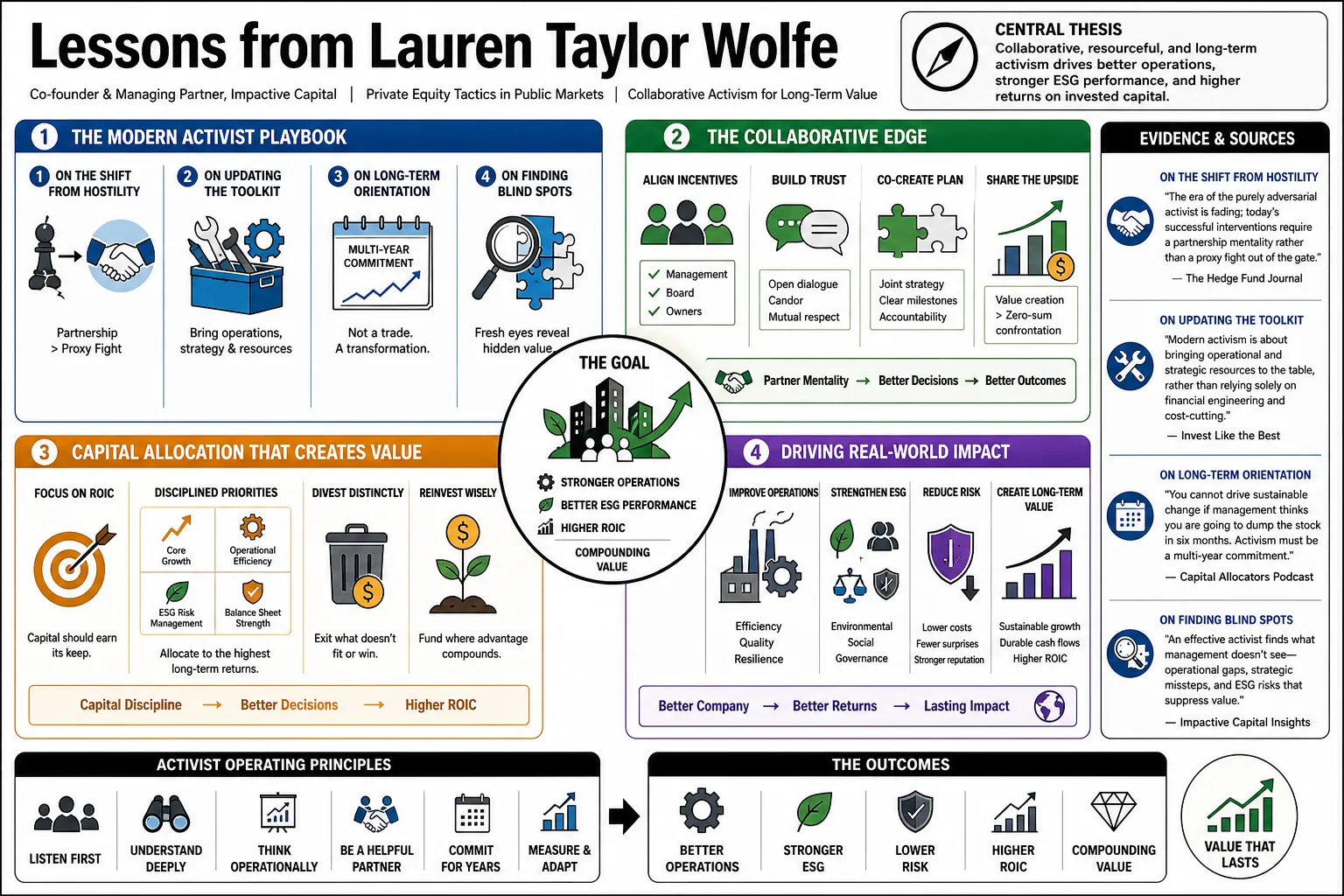

- On the shift from hostility: "The era of the purely adversarial activist is fading; today's successful interventions require a partnership mentality rather than a proxy fight out of the gate." — Source: The Hedge Fund Journal

- On updating the toolkit: "Modern activism is about bringing operational and strategic resources to the table, rather than relying solely on financial engineering and cost-cutting." — Source: Invest Like the Best

- On long-term orientation: "You cannot drive sustainable change if management thinks you are going to dump the stock in six months. Activism must be a multi-year commitment." — Source: Capital Allocators Podcast

- On finding blind spots: "An effective activist identifies operational blind spots that management may be too close to see." — Source: Goldman Sachs Exchanges

- On the role of public markets: "Public companies often face short-term earnings pressure. The activist's job is to provide the air cover needed to make long-term strategic pivots." — Source: CNBC Power Lunch

- On building trust: "Trust is an unappreciated currency in activist investing. Without it, even the most mathematically sound capital allocation plan will face internal resistance." — Source: Invest Like the Best

- On continuous engagement: "Activism is a continuous, iterative dialogue with the board and executive team." — Source: The Hedge Fund Journal

- On defining success: "A successful campaign leaves the company fundamentally more resilient and competitive, rather than with a temporarily inflated multiple." — Source: Impactive Capital Media

- On avoiding the limelight: "The best outcomes often happen behind closed doors. If we are in the headlines, it usually means the collaborative process has stalled." — Source: Capital Allocators Podcast

Part 2: ESG as a Value Driver

- On the core premise: "ESG without returns is simply unsustainable. The two must be linked to drive true value." — Source: Goldman Sachs Exchanges

- On environmental efficiencies: "Reducing waste and improving energy efficiency are direct contributors to expanding operating margins." — Source: Forbes

- On employee retention: "Companies that invest in their workforce see lower turnover, which directly reduces recruitment and training costs." — Source: Capital Allocators Podcast

- On moving beyond screening: "Passive ESG screening misses the point. The real alpha is generated by actively helping a lagging company improve its practices." — Source: Invest Like the Best

- On sustainability as a moat: "Implementing strong sustainability practices serves as a competitive moat, attracting both talent and ethically minded customers." — Source: CNBC

- On the materiality of ESG: "We only focus on ESG factors that are material to the specific business model. A software company's material issues look very different from an industrial manufacturer's." — Source: The Hedge Fund Journal

- On data transparency: "Encouraging companies to publish detailed sustainability reports often forces internal accounting of inefficiencies that were previously ignored." — Source: Goldman Sachs Exchanges

- On aligning incentives: "Executive compensation must be tied to the successful implementation of key ESG initiatives alongside financial metrics." — Source: Impactive Capital Media

- On the cost of capital: "Companies with strong, measurable ESG practices increasingly benefit from a lower cost of capital as a wider pool of institutional money becomes available to them." — Source: Forbes

- On the false dichotomy: "The idea that you have to choose between doing good and making money is outdated. We prove every day that doing good is how you make money." — Source: Capital Allocators Podcast

Part 3: Private Equity Approach in Public Markets

- On the PE mindset: "We bring a private equity approach to public markets, meaning we underwrite businesses with a multi-year horizon and look for operational turnarounds." — Source: Invest Like the Best

- On deep due diligence: "Our diligence process mirrors private equity, involving extensive primary research, customer interviews, and deep supply chain analysis before we take a position." — Source: The Hedge Fund Journal

- On operational enhancement: "We bring in operating partners to help companies optimize pricing, improve sales force efficiency, and restructure costs." — Source: Capital Allocators Podcast

- On ignoring daily volatility: "Viewing public equities through a private lens allows us to ignore daily price fluctuations and focus on the fundamental compounding of cash flows." — Source: Goldman Sachs Exchanges

- On value creation plans: "Every investment is accompanied by a detailed, hundred-day-style value creation plan that we share with the board and management." — Source: Invest Like the Best

- On board representation: "Like a private equity sponsor, we often seek board representation to ensure our long-term strategic initiatives are executed with urgency." — Source: CNBC Squawk on the Street

- On the advantage of liquidity: "The advantage of applying private equity tactics in public markets is that we have the liquidity to exit if the thesis fundamentally breaks." — Source: The Hedge Fund Journal

- On targeting under-managed assets: "We look for great businesses that are currently under-managed or misallocated, where a private owner would immediately step in and make changes." — Source: Capital Allocators Podcast

- On alignment of interests: "The private equity model works because everyone is aligned around equity value creation. We strive to create that exact alignment in the public boards we join." — Source: Impactive Capital Media

Part 4: Capital Allocation and Long-Termism

- On the importance of capital allocation: "Capital allocation is the primary job of a CEO, yet many arrive in the role with zero formal training in it." — Source: Invest Like the Best

- On returning capital: "Share repurchases only create value if the stock is fundamentally undervalued. Buying back overvalued stock destroys long-term shareholder wealth." — Source: Capital Allocators Podcast

- On disciplined M&A: "Many management teams pursue acquisitions for empire-building. We demand strict, measurable hurdle rates for any acquisition activity." — Source: The Hedge Fund Journal

- On reinvesting in the business: "The highest return on capital is often found in organic reinvestment. We encourage companies to invest heavily in their core competitive advantages." — Source: Goldman Sachs Exchanges

- On balance sheet efficiency: "A lazy balance sheet is a drag on returns. We help companies optimize their capital structure to lower their weighted average cost of capital." — Source: CNBC Power Lunch

- On dividend policy: "Dividends should be a deliberate choice based on cash flow predictability, rather than a dogmatic commitment that starves the business of growth capital." — Source: Invest Like the Best

- On the ROIC metric: "Return on Invested Capital is the ultimate arbiter of a company's quality. If a business cannot consistently earn more than its cost of capital, it should not be retaining earnings." — Source: Capital Allocators Podcast

- On short-term earnings pressure: "We actively counsel our portfolio companies to ignore the quarterly earnings treadmill and make the difficult investments required for long-term dominance." — Source: Impactive Capital Media

- On stranded capital: "Identifying and divesting underperforming assets is often the fastest way to free up capital and improve the overall margin profile of the business." — Source: The Hedge Fund Journal

Part 5: Collaborative Engagement over Hostility

- On the Blue Harbour influence: "My time at Blue Harbour taught me that friendly engagement often yields faster, more durable results than hostile proxy fights." — Source: The Hedge Fund Journal

- On approaching management: "We approach management teams as peers and partners, bringing rigorous research to the table rather than ultimatums." — Source: Invest Like the Best

- On shared goals: "The key to collaborative activism is demonstrating early on that our goal is exactly the same as management's: to maximize the long-term value of the enterprise." — Source: Capital Allocators Podcast

- On providing resources: "We offer our network of industry experts and consultants to help management execute the transition." — Source: Goldman Sachs Exchanges

- On constructive friction: "Collaboration does not mean avoiding difficult conversations. Constructive friction is required to challenge entrenched corporate orthodoxies." — Source: CNBC

- On the cost of proxy fights: "Hostile proxy contests are a massive drain on corporate resources, management focus, and shareholder capital. They should be a weapon of absolute last resort." — Source: The Hedge Fund Journal

- On building consensus: "Effecting change from the inside requires building consensus among the board, the executive team, and other major shareholders." — Source: Invest Like the Best

- On active listening: "The first step in any engagement is to listen. Management often understands the problems perfectly well but lacks the mandate or resources to fix them." — Source: Capital Allocators Podcast

- On public vs. private critique: "Praise in public, critique in private. We prefer to hash out our disagreements in the boardroom, rather than in the press." — Source: Impactive Capital Media

- On mutual respect: In The Hedge Fund Journal, Taylor Wolfe describes collaborative activism as the right approach for Blue Harbour: the firm works alongside managers, avoids poison-pen letters and proxy contests, and relies on reputational goodwill with CEOs and boards. — Reference: The Hedge Fund Journal Q&A on Taylor Wolfe's collaborative activism and reputational goodwill with management teams

Part 6: Building a Concentrated Portfolio

- On the necessity of focus: "You cannot be an active, engaged owner of fifty companies. Our model requires a concentrated portfolio so we can dedicate the necessary time to each position." — Source: Capital Allocators Podcast

- On conviction sizing: "When you find a business with a wide moat, a fixable problem, and a receptive management team, you must size the position meaningfully to drive returns." — Source: Invest Like the Best

- On risk management through knowledge: "True risk management comes from a deep, granular understanding of the businesses you own." — Source: The Hedge Fund Journal

- On the research bar: "The bar for entry into a ten to fifteen stock portfolio is incredibly high. We reject dozens of good ideas to find the exceptional ones." — Source: Goldman Sachs Exchanges

- On time allocation: "A concentrated portfolio allows our team to function as an extension of the companies' strategic planning departments." — Source: CNBC Power Lunch

- On weathering volatility: "When you own a small number of deeply researched names, you can use market volatility to add to positions rather than panicking out of them." — Source: Invest Like the Best

- On active share: "To generate outsized alpha, you must look completely different from the benchmark. Concentration is the direct path to high active share." — Source: The Hedge Fund Journal

- On deep partnerships: "We view our portfolio companies as true partnerships. You can only maintain that level of intimacy with a select few." — Source: Capital Allocators Podcast

- On exiting positions: "In a concentrated strategy, selling a winner is often the hardest decision, but capital must be continuously recycled into the highest-conviction operational turnaround." — Source: Impactive Capital Media

Part 7: Governance and Accountability

- On the board's role: "The board is not there to rubber-stamp the CEO's agenda; it exists to hold management accountable and rigorously evaluate capital allocation." — Source: Wake Up WEX Presentation

- On director skill sets: "Too many boards are filled with generalists. We advocate for adding directors with specific, relevant operational expertise that matches the company's current challenges." — Source: The Hedge Fund Journal

- On board refreshment: "Tenure limits and regular board refreshment are essential to prevent groupthink and ensure the board's skills evolve with the market." — Source: Capital Allocators Podcast

- On executive compensation: "Compensation structures must be tied to Return on Invested Capital and long-term value creation." — Source: Invest Like the Best

- On independent oversight: "An effective board requires a strong, independent lead director who is willing to challenge the CEO in executive sessions." — Source: Wake Up WEX Presentation

- On diversity of thought: "True board diversity is about bringing together different industry backgrounds, operational experiences, and cognitive approaches." — Source: Goldman Sachs Exchanges

- On the activist as a director: "When an activist joins a board, they bring a shareholder's mindset directly into the room, shifting the conversation from process to performance." — Source: CNBC Squawk on the Street

- On challenging the status quo: "A healthy boardroom is one where respectful disagreement is encouraged and the status quo is constantly forced to justify itself." — Source: Impactive Capital Media

- On succession planning: "One of the most essential, yet often neglected, duties of the board is rigorous, ongoing CEO succession planning." — Source: The Hedge Fund Journal

- On governance as a foundation: "Strong corporate governance is the bedrock upon which all other operational and ESG improvements must be built." — Source: Capital Allocators Podcast

Part 8: Navigating Small and Mid-Cap Opportunities

- On market inefficiencies: "The small and mid-cap space is inherently less efficient, offering far more opportunities to find high-quality businesses that have been orphaned by the broader market." — Source: Brown Advisory CIO Perspectives

- On the lack of analyst coverage: "As sell-side coverage of mid-cap stocks declines, the advantage shifts dramatically to firms willing to do deep, fundamental primary research." — Source: Invest Like the Best

- On operational scale: "Smaller companies often have massive embedded operating advantages. A few strategic tweaks to their cost structure can meaningfully increase cash flow." — Source: Capital Allocators Podcast

- On agility: "Mid-cap companies are generally more agile. When we propose a strategic pivot or a new ESG initiative, the implementation timeline is much faster than at a mega-cap." — Source: Goldman Sachs Exchanges

- On M&A targets: "High-quality mid-cap companies with optimized balance sheets and clean operations naturally become highly attractive acquisition targets for larger strategic buyers." — Source: The Hedge Fund Journal

- On the value of engagement: "The impact of active engagement is magnified in smaller companies, where management teams often lack internal resources and welcome external operational expertise." — Source: Forbes

- On index fund dominance: "The rise of passive investing has created distinct dislocations in the small and mid-cap markets, leaving excellent businesses systematically undervalued." — Source: CNBC Power Lunch

- On niche dominance: "We look for mid-cap companies that dominate a specific, defensible niche, giving them pricing power that isn't immediately obvious to casual observers." — Source: Brown Advisory CIO Perspectives

- On compounding potential: "It is mathematically much easier to compound capital at high rates when you start with a two billion enterprise value rather than a two hundred billion one." — Source: Invest Like the Best