Lessons from Leon Cooperman

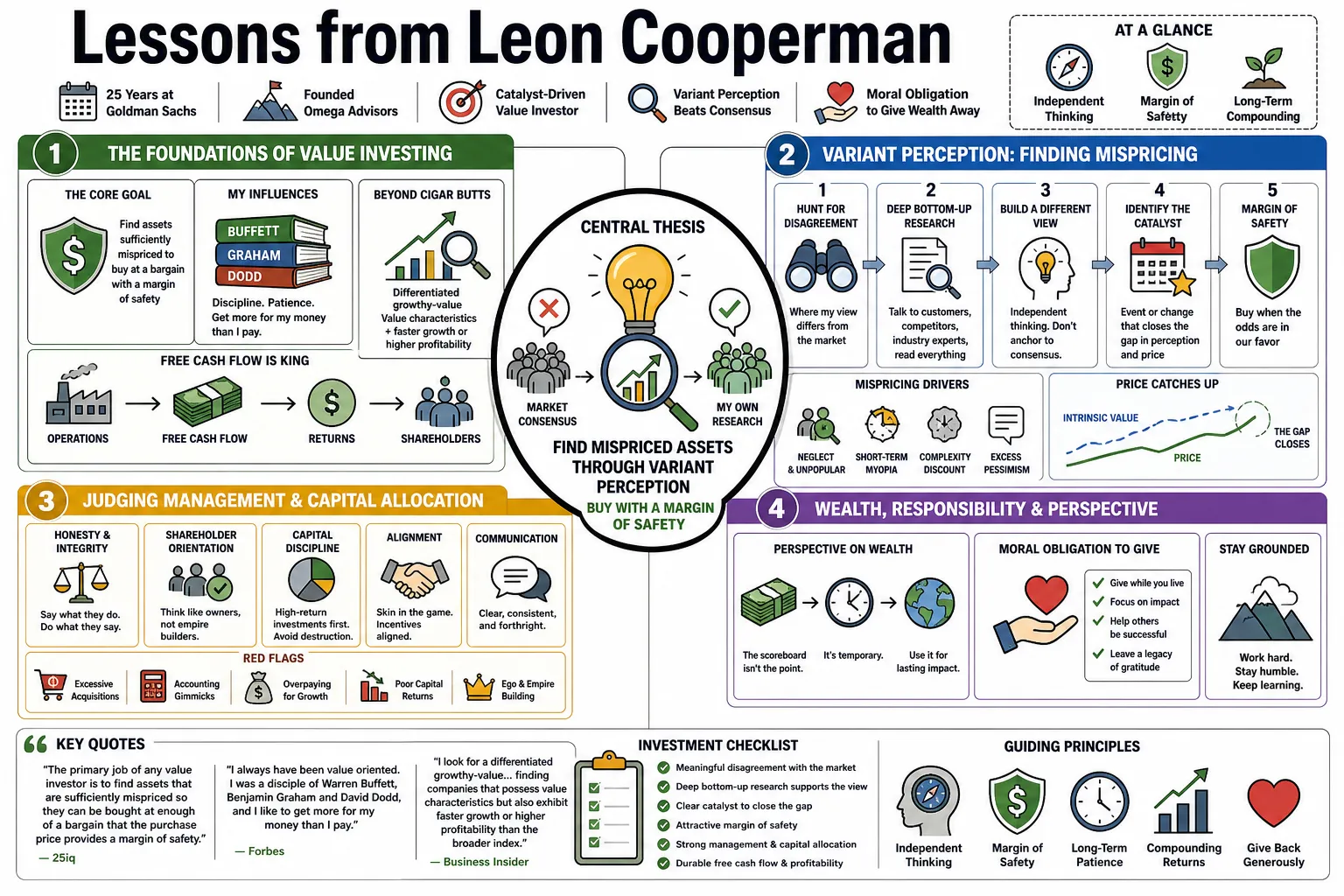

Leon Cooperman spent 25 years at Goldman Sachs before founding Omega Advisors, establishing a long track record as a catalyst-driven value investor. His strategy relies on "variant perception," which involves hunting for stocks where his own bottom-up research contradicts the market consensus. This profile outlines his approach to finding mispriced assets and judging management, alongside his belief in the moral obligation to give wealth away.

Part 1: The Foundations of Value Investing

- On the core goal of value investing: "The primary job of any value investor is to find assets that are sufficiently mispriced so they can be bought at enough of a bargain that the purchase price provides a margin of safety." — Source: 25iq

- On defining his style: "I always have been value oriented. I was a disciple of Warren Buffett, Benjamin Graham and David Dodd, and I like to get more for my money than I pay." — Source: Forbes

- On evolving past cigar butts: "I look for a differentiated growthy-value... finding companies that possess value characteristics but also exhibit faster growth or higher profitability than the broader index." — Source: Business Insider

- On free cash flow as a metric: "Free cash flow gives companies the luxury to do good things, whether it's pay dividends, buy back stock, or invest in new equipment." — Source: The Economic Times

- On the necessity of a catalyst: "We follow a 'value with a catalyst' strategy. Value without a catalyst can often just be a value trap." — Source: CNBC

- On bottom-up portfolio construction: "While I utilize a top-down approach for sector selection and macro awareness, my portfolio construction is strictly bottom-up." — Source: Insider Monkey

- On the importance of footnotes: "Penetrating research means reading the footnotes, analyzing the balance sheet, and truly understanding a company’s normalized earnings power." — Source: Moat Radar

- On staying within your competence: "You have to invest within your circle of competence and understand exactly what is in your portfolio." — Source: Validea

- On long-term orientation: "When the conviction remains high and the fundamentals are intact, you hold the position. I held shares of Teledyne for 25 years." — Source: Validea

- On avoiding index funds if you want alpha: "If you don’t want to work and think, buy a low-cost index fund. Outperformance requires critical thinking." — Source: The Economic Times

Part 2: Variant Perception and Contrarianism

- On defining variant perception: "Where does your view differ from the consensus that could spark the reason you're getting the return you're looking for? You see things that someone else doesn't see." — Source: Market Folly

- On the necessity of divergence: "If your view is not different from the crowd, there is little reason to expect superior returns." — Source: The Economic Times

- On seasonal analogies: "We are trying to look for the straw hats in the winter. In the winter, people don't buy straw hats, so they're on sale." — Source: 25iq

- On market memory: "Stocks have a memory. They know where they came from, so I tend to look at either the new low list or things in the middle of their trading range to get involved." — Source: The Economic Times

- On avoiding the herd: "I don't like to buy the new high list. When everyone is on the same side of the boat, it is a significant risk indicator." — Source: Forbes

- On capitalizing on fear: "You want to buy assets that are out of favor and mispriced by the market due to fear or neglect." — Source: 25iq

- On thesis building: "Every investment requires a thesis that specifically articulates why the market is currently pricing the asset incorrectly." — Source: Market Folly

- On challenging consensus: "The consensus is often priced in. Your job is to find the gap between perception and fundamental reality." — Source: GuruFocus

- On the nature of opportunity: "Opportunities are created when the market overreacts to short-term noise while ignoring long-term fundamentals." — Source: Insider Monkey

Part 3: Market Psychology and Behavioral Finance

- On identifying market peaks: "Euphoria and excessive exuberance are among the clearest signs that a market might be nearing a top." — Source: Yahoo Finance

- On speculative bubbles: "When you see retail frenzies and Robinhood markets driving valuations devoid of fundamentals, the market is heading for a correction." — Source: Forbes

- On the monetary illusion: "Beware of the monetary illusion, where asset prices rise due to policy stimulus and liquidity rather than fundamental economic strength." — Source: CNBC Events

- On emotional discipline: "You have to separate your emotions from your capital. Panic is not an investment strategy." — Source: Fox Business

- On the danger of resting: "In this business, you cannot rest on your laurels. You have to always be on the balls of your feet." — Source: Business Insider

- On dealing with being wrong: "You have to stay disciplined and recognize that you can be dead wrong in your market predictions. Humility is essential." — Source: Fox Business

- On reactions to price drops: "If a stock goes down, re-evaluate the thesis. If the fundamentals are intact, it's an opportunity to buy more. If the thesis is broken, exit." — Source: Market Folly

- On market cycles: "Markets are cyclical. Understanding where you are in the cycle helps you dictate your aggressive or defensive posture." — Source: GuruFocus

- On independent thinking: "You cannot outperform the market by doing exactly what everyone else is doing." — Source: The Economic Times

Part 4: Assessing Management and Capital Allocation

- On the two-step management evaluation: "You evaluate management twice in the decision-making process. Once, through the face-to-face interrogation... and in addition, the quality of management also manifests itself in the numbers." — Source: QuotesWise

- On numerical evidence of leadership: "Look for management quality in ROE, return on total capital, growth rate, industry position, trend of market share, and profit margins." — Source: QuotesWise

- On capital allocation: "I look for management teams that demonstrate a commitment to creating shareholder value through disciplined capital allocation." — Source: Hedge Fund Alpha

- On share buybacks: "A willingness to buy back stock at sensible prices is a strong signal of management's confidence and shareholder alignment." — Source: Hedge Fund Alpha

- On cash flow stewardship: "It is crucial to evaluate how management handles free cash flow—whether they use it to benefit shareholders through dividends, buybacks, or productive reinvestment." — Source: The Economic Times

- On cycle-tested leaders: "I prioritize cycle-tested companies run by reliable management teams who have navigated through different economic environments." — Source: GuruFocus

- On integrity: "Leadership must be capable, trustworthy, and focused on long-term business health rather than short-term market optics." — Source: GuruFocus

- On insider ownership: "I prefer to invest alongside management teams who have a significant personal financial stake in the outcome of the business." — Source: Insider Monkey

- On face-to-face meetings: "Interrogating management directly helps you gauge their candor, their understanding of the business, and their strategic vision." — Source: QuotesWise

Part 5: Risk Management and Macro Context

- On position sizing: "After forming a conviction, determine the appropriate exposure and sizing in the context of prudent risk control and liquidity." — Source: 25iq

- On market timing: "I don't believe in pure market timing, but understanding the macro environment is essential for determining your overall portfolio exposure." — Source: The Economic Times

- On navigating overvalued markets: "When the market is expensive, you are better off focusing on finding specific undervalued opportunities than betting on the direction of the overall market." — Source: Daily Hodl

- On the S&P 500 index: "At historically high valuations, the broader index offers limited upside. The real money is made in individual stock selection." — Source: Business Insider

- On inflation risks: "A painful combination of slow economic growth and high inflation is one of the primary threats to market stability." — Source: Business Insider

- On interest rate environments: "The Fed forcing people out on the risk curve by keeping interest rates too low for too long inevitably creates malinvestment." — Source: Forbes

- On adjusting to market levels: "When the market's high, I have to figure out how I can get hedged, and when the market's low, I have to figure out how I can get leveraged to the opportunity." — Source: QuotesWise

- On true risk management: "Risk management is less about hedging every move and more about the quality of the investment, the margin of safety, and the structure of the portfolio." — Source: 25iq

- On avoiding unforced errors: "Do not over-concentrate in positions that cannot be defended if the market turns against you." — Source: Market Folly

- On macro awareness vs. stock picking: "You must be aware of the macro environment to manage risk, but your returns ultimately come from bottom-up fundamental analysis." — Source: GuruFocus

Part 6: Work Ethic and the PHD Mindset

- On the formula for success: "People ask me what I attribute my success to, and I say hard work and luck, which are easy to understand, and intuition." — Source: Forbes

- On the PHD mindset: "I seek out individuals who have a PHD mindset—not an academic degree, but those who are Poor, Hungry, and Driven." — Source: Lovable

- On total commitment: "To be successful in your chosen field of endeavor, be ready to give of your mind, of your body, and of your soul." — Source: Roger Williams University

- On the lion and the gazelle: In a CSIS transcript, Cooperman says he made hires read the lion-and-gazelle parable, then draws the lesson this way: "It doesn't matter whether you are a lion or a gazelle. When the sun comes up, you'd better be running." — Reference: CSIS transcript where Cooperman recounts the lion-and-gazelle parable

- On generating your own luck: "The harder I worked, the luckier I got. Hard work is the fundamental driver of opportunity." — Source: The Economic Times

- On hours vs. passion: "I work 80-hour workweeks, but I never looked at it as work. I enjoyed what I did." — Source: Forbes

- On resting on laurels: "You cannot be complacent. The market changes every day, and you must put in the continuous effort to adapt." — Source: Business Insider

- On humble beginnings: "I grew up the son of a plumber in the South Bronx. I never knew need, but I learned the value of relentless effort." — Source: QuotesWise

- On ambition over pedigree: "Intense work ethic and unyielding ambition will almost always outperform a purely academic pedigree." — Source: Lovable

- On continuous engagement: "There is no secret sauce for investment success. It requires deep, thorough research and total commitment to the clients' interests." — Source: Market Folly

Part 7: Career Advice and Life Lessons

- On finding the right career: "The most important advice I give youngsters is that the only way to be successful is to do what you love and love what you do." — Source: Forbes

- On choosing colleagues: "Find work you like to do and work with people you admire and respect." — Source: The Economic Times

- On hiring strategy: "Don’t ever be threatened by hiring strong people. You should always hire people who are smarter than you." — Source: Columbia University

- On the cost of kindness: "Be good to everyone. It is one of the most important pieces of advice, and it costs absolutely nothing." — Source: Columbia University

- On leveraging education: "Education is the ultimate equalizer and the primary tool you have to become competitive in the world." — Source: Horatio Alger Association

- On avoiding complacency: "If you are coasting, you are going downhill. You must constantly challenge your own assumptions." — Source: QuotesWise

- On building a reputation: "Your reputation is your most valuable asset in business. Guard it with unwavering integrity." — Source: Forbes

- On the reality of the industry: "Wall Street is not about making quick money; it is about enduring discipline and intellectual rigor over decades." — Source: Business Insider

- On perspective: "Never lose sight of where you came from. It keeps you grounded when success arrives." — Source: QuotesWise

Part 8: Wealth and the Moral Imperative of Philanthropy

- On the purpose of wealth: "Toby and I feel it is our moral imperative to give others the opportunity to pursue the American Dream by sharing our financial success." — Source: The Giving Pledge

- On keeping money: "Shrouds don't have pockets and I don't intend to take the money with me." — Source: NJPAC

- On the Giving Pledge: "When I took the Giving Pledge I told Warren Buffett asking for half is not asking for enough. I intend to give it all away." — Source: The American Prospect

- On capitalism with a heart: In eJewishPhilanthropy, Cooperman connects wealth to giving: after saying financially secure people should share success with the less fortunate and help others in need, he adds, "I'm a committed capitalist, but I'm a capitalist with a heart." — Reference: eJewishPhilanthropy on Cooperman linking capitalism, philanthropy, and helping people in need

- On true net worth: "As the Talmud says, a man's net worth is measured not by what he earns but rather what he gives away." — Source: The Giving Pledge

- On the American Dream: "I made a lot of money, I'm giving it away. That's the American Dream." — Source: RealClear Public Affairs

- On Carnegie's wisdom: "I align with Andrew Carnegie's philosophy: He who dies rich, dies disgraced." — Source: The Giving Pledge

- On Churchill's perspective: "We make a living by what we get, but we make a life by what we give." — Source: The Giving Pledge

- On the wealthy class: "Rather than assume that the wealthy are a monolithic, selfish lot... set a tone that encourages people of good will to meet in the middle." — Source: AZQuotes