Lessons from Lucas Swisher

Lucas Swisher is a General Partner at Coatue Management investing in growth-stage AI and enterprise software. He evaluates startups on the thesis that AI lets software compete for a $5.5 trillion global services budget rather than fighting over the $200 billion traditional technology market. This collection organizes his arguments on venture math, market concentration, and changing SaaS unit economics.

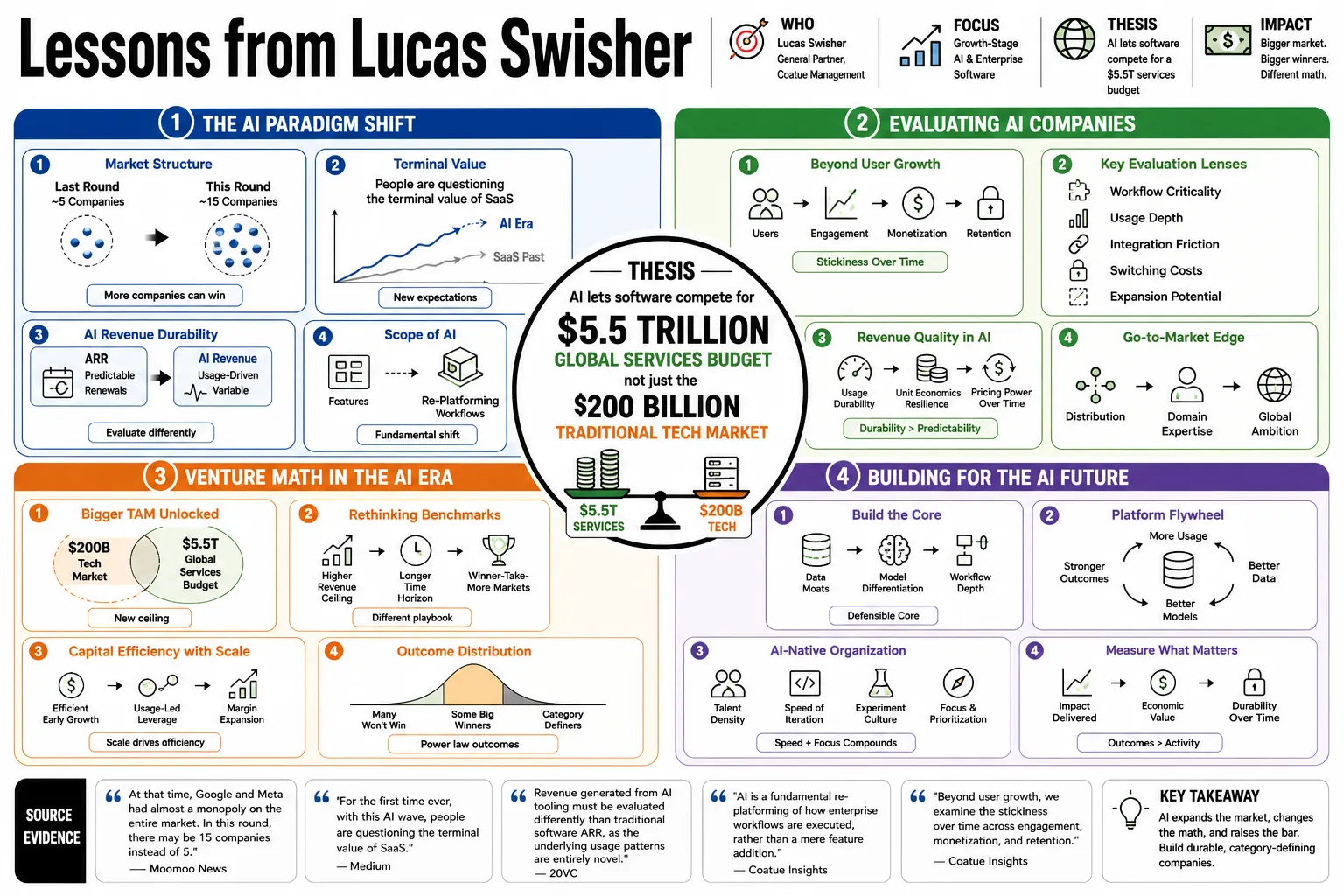

Part 1: The AI Paradigm Shift

- On the AI market structure: "At that time [the internet age], Google and Meta had almost a monopoly on the entire market. In this round, there may be 15 companies instead of 5." — Source: Moomoo News

- On the AI wave: "For the first time ever, with this AI wave, people are questioning the terminal value of SaaS." — Source: Medium

- On AI revenue durability: "Revenue generated from AI tooling must be evaluated differently than traditional software ARR, as the underlying usage patterns are entirely novel." — Source: 20VC

- On the scope of AI: "AI is a fundamental re-platforming of how enterprise workflows are executed, rather than a mere feature addition." — Source: Coatue Insights

- On evaluating AI companies: "Beyond user growth, we examine the stickiness of the underlying model and the compute efficiency of the product." — Source: Run the Numbers

- On enterprise intelligence: "Enterprise intelligence has liftoff, driven by foundational models that are finally capable of parsing complex, unstructured corporate data." — Source: Coatue Insights

- On the pace of AI adoption: "The adoption curve for generative AI in the enterprise is compressing what used to take a decade into a matter of quarters." — Source: Forbes

- On AI native workflows: "The most exciting companies are building native workflows that assume AI from day one, rather than bolting it onto old architectures." — Source: The Generalist

- On the terminal value of legacy tools: "Incumbent SaaS providers that fail to deeply integrate AI are facing an existential threat to their long-term enterprise value." — Source: Medium

Part 2: Re-evaluating Software Value

- On the technology budget: "The traditional software market is roughly a $200 billion opportunity." — Source: The Generalist

- On the services budget: "The services market that AI can now address represents roughly $5.5 trillion." — Source: The Generalist

- On total addressable market expansion: "Moving from the software budget to the services budget represents a 25x difference in total addressable market for technology companies." — Source: The Generalist

- On capturing service spend: "AI enables software to move beyond competing for the limited technology budget to competing for the much larger services budget." — Source: Substack

- On software unit economics: "The unit economics of a business selling AI as a service look fundamentally different because you are replacing human labor instead of legacy code." — Source: Run the Numbers

- On the future of SaaS: "SaaS companies must prove they can capture margin in a world where AI models are commoditizing basic software functionalities." — Source: Medium

- On enterprise automation: "The value of a software tool is now directly proportional to the amount of manual service labor it can reliably automate." — Source: Coatue Insights

- On software margins: "Gross margins in the AI era will face pressure from compute costs, requiring a fundamental shift in how we model long-term profitability." — Source: 20VC

- On market sizing: "Market size evaluations must factor in the shadow IT budget and outsourced services, which AI tools are rapidly absorbing." — Source: Forbes

- On the 25x thesis: "When software companies target the $5.5 trillion services budget, the traditional SaaS valuation frameworks break down completely." — Source: The Generalist

Part 3: Portfolio Strategy and Concentration

- On portfolio concentration: "We were doing this analysis of looking at every unicorn company. And what we found is 60% of the market cap is in the top 20 names." — Source: Run the Numbers

- On top-heavy markets: "50% of the market cap is in the top three names of the entire Unicorn economy." — Source: Run the Numbers

- On investment strategy: "Our view is we gotta just be in the top 20." — Source: Run the Numbers

- On mega-fund returns: "Generating venture returns with a mega-fund requires an absolute commitment to finding and funding the absolute outliers." — Source: 20VC

- On index vs. concentration: "Venture capital is a game of extremes; indexing a portfolio across dozens of mediocre companies guarantees underperformance." — Source: Forbes

- On capital allocation: "Deploying capital effectively at scale means leaning aggressively into your winners rather than trying to salvage the bottom quartile." — Source: Coatue Insights

- On the unicorn economy: "The label of 'unicorn' has lost its utility; the real metric is whether a company is positioned to be a generational category leader." — Source: The Generalist

- On missing the top names: "If you miss the top three companies in a given technological wave, your portfolio will struggle to return the fund regardless of other successes." — Source: 20VC

- On identifying outliers: "The data clearly shows that power-law dynamics are intensifying, making concentration a mathematical necessity rather than a stylistic choice." — Source: Run the Numbers

Part 4: Data-Driven Investing

- On Coatue's Mosaic: "We rely heavily on proprietary data platforms to strip away the narrative and look at the raw underlying growth metrics." — Source: Run the Numbers

- On data vs. narrative: "Founders can craft compelling stories, but credit card data, developer activity, and usage telemetry provide the ground truth." — Source: Forbes

- On systemic deal sourcing: "Using data systematically allows us to track breakout velocity before a company formally begins a fundraising process." — Source: Coatue Insights

- On evaluating growth: "Outside of AI, no company is growing like this." — Source: EOMag

- On real-time analytics: "The latency between a company's performance and our visibility into that performance has been reduced to near zero." — Source: Run the Numbers

- On quantitative analysis in VC: "Venture capital is transitioning from a relationship-driven asset class to a fundamentally quantitative one." — Source: 20VC

- On tracking talent: "Monitoring where top-tier engineering talent is migrating often predicts the next major platform shift before revenue materializes." — Source: The Generalist

- On red flags: "A divergence between a company's reported ARR and their underlying product usage metrics is the clearest signal to walk away." — Source: Run the Numbers

- On public vs. private data: "Bridging the gap between public market data and private market valuations provides a critical lens for pricing rounds accurately." — Source: Coatue Insights

- On scaling diligence: "Data platforms allow us to conduct deep diligence across hundreds of companies simultaneously, removing the bottleneck of human capacity." — Source: Forbes

Part 5: Assessing Founder Quality

- On founder velocity: "The best founders ship product at a cadence that breaks the internal processes of their competitors." — Source: 20VC

- On adapting to AI: "Founders who refuse to rewrite their core product architecture to accommodate AI are choosing to become obsolete." — Source: Medium

- On technical depth: "In the current wave, a founder's ability to deeply understand model architecture is often more valuable than their go-to-market experience." — Source: Run the Numbers

- On market obsession: "We look for founders who are pathologically obsessed with a specific customer pain point, rather than those hunting for a trend." — Source: Forbes

- On capital efficiency: "The era of zero-interest rates masked poor operational discipline; today's top founders treat capital as a scarce, expensive weapon." — Source: Coatue Insights

- On pivoting: "A high-quality founder will aggressively kill their own darlings when the data indicates a feature isn't driving core retention." — Source: 20VC

- On recruiting: "The ultimate test of leadership in a seed-stage company is the ability to poach senior engineers from established tech giants." — Source: The Generalist

- On founder-market fit: "When evaluating founders, we index heavily on their unique insight into a market inefficiency that others have accepted as standard." — Source: Run the Numbers

- On balancing public and private pressure: In the Run the Numbers episode summary, Swisher explains that Coatue balances short-term public market pressure with the longer time horizon of private investing, which supports the broader lesson that he values founders who can stay steady through volatility instead of only looking good in easy financing environments. — Reference: Run the Numbers episode summary with Lucas Swisher

Part 6: Venture Capital Math

- On price sensitivity: "Why price matters least is that in the top three companies, the compounding growth overwhelms the initial entry valuation." — Source: 20VC

- On entry valuations: "Overpaying for a generational company is a temporary accounting problem; missing a generational company is a permanent fund problem." — Source: 20VC

- On fund sizing: "The mechanics of a $70 billion machine require us to deploy large checks into highly derisked, high-velocity assets." — Source: Run the Numbers

- On ownership targets: "Optimizing for exact ownership percentages can sometimes cause investors to miss the broader trajectory of a category-defining business." — Source: Forbes

- On durable growth at high prices: In Coatue's writeup on private-market pricing, Swisher argues that the key question is not whether an entry price looks high but whether growth is durable, noting that sustained 70% to 100% plus growth with improving margins can compress an expensive multiple quickly. That supports the broader lesson that late-stage investors should underwrite durability and execution rather than fixate on the sticker price alone. — Reference: Coatue note on private-market pricing by Lucas Swisher

- On DPI (Distributions to Paid-In Capital): "Paper markups are irrelevant if the firm lacks a clear, disciplined strategy for realizing liquidity in the public markets." — Source: The Generalist

- On public market alignment: "Private market valuations eventually converge with public market multiples, and investors must underwrite rounds with that terminal state in mind." — Source: Coatue Insights

- On downside protection: "Structuring deals with heavy liquidation preferences can misalign incentives; the focus should remain on enterprise value creation." — Source: Run the Numbers

- On the velocity of capital: "Speed of deployment must be matched by a rigorous, data-informed conviction, otherwise you are simply indexing the market." — Source: 20VC

Part 7: AI Services vs. Software Budget

- On displacing services: "The next wave of decacorns will be built by companies that sell work output, rather than software licenses." — Source: Substack

- On pricing models: "Pricing on a per-seat basis makes little sense when an AI agent can perform the work of ten seats." — Source: Medium

- On the transition to outcomes: "Customers will increasingly pay for verified business outcomes rather than access to a tool." — Source: Coatue Insights

- On B2B services: "BPO (Business Process Outsourcing) is the most vulnerable sector to the current generation of large language models." — Source: The Generalist

- On enterprise intelligence adoption: "Partnering with Decagon showed us that the new customer experience is driven by instant, highly accurate AI resolution." — Source: Coatue Insights

- On software's ceiling: "The traditional SaaS model has hit a natural ceiling constrained by the total number of knowledge workers available to buy seats." — Source: Forbes

- On AI agents: "Autonomous agents capable of executing multi-step workflows represent the transition from software as a tool to software as an employee." — Source: Run the Numbers

- On margin profiles of service businesses: "When you replace a human service firm with an AI service firm, the gross margins shift from 30% to 80%." — Source: 20VC

- On the $5.5 trillion prize: "Capturing even a fraction of the $5.5 trillion services market dwarfs the entire historical value created by cloud software." — Source: The Generalist

- On re-architecting work: "We are moving away from software that helps humans do their jobs, toward software that simply does the job." — Source: Substack

Part 8: The Future of Growth Investing

- On the crossover model: "Firms that operate across both public and private markets have a structural advantage in accurately pricing late-stage private rounds." — Source: Coatue Insights

- On the normalization of multiples: "The reversion to the mean in software multiples forced a necessary discipline back into the growth investing ecosystem." — Source: Run the Numbers

- On capital moats: "In capital-intensive sectors like foundational AI, access to massive amounts of capital becomes a primary competitive moat." — Source: 20VC

- On sector specialization: "Generalist growth funds will struggle to compete with sector-specific teams that deeply understand the technical nuances of their domains." — Source: Forbes

- On global reach: "The best software companies are global from day one, and growth investors must be able to support international scaling immediately." — Source: Coatue Insights

- On hardware and compute: "Investing in AI requires a fundamental understanding of the semiconductor supply chain and the underlying compute infrastructure." — Source: The Generalist

- On regulatory risk: "As technology companies encroach on massive service sectors, regulatory capture and compliance become core diligence items." — Source: Run the Numbers

- On crossover market discipline: The Run the Numbers episode summary says Swisher discussed how Coatue navigates both public and private markets and balances near-term public signals against longer-term private positions, which supports the broader lesson that liquidity and portfolio decisions require active crossover discipline rather than treating private holdings as isolated from public-market reality. — Reference: Run the Numbers episode summary with Lucas Swisher

- On the next decade: "The coming decade of growth investing will be defined by identifying which application layers can sustainably capture the value created by underlying AI models." — Source: 20VC