Lessons from Luke Ellis

Luke Ellis ran Man Group, one of the world's largest publicly traded hedge funds, from 2016 to 2023. He became known for balancing fundamental intuition with strict systematic discipline. This profile gathers his thoughts on central bank policy, managing talent, and why most market risks are entirely self-inflicted.

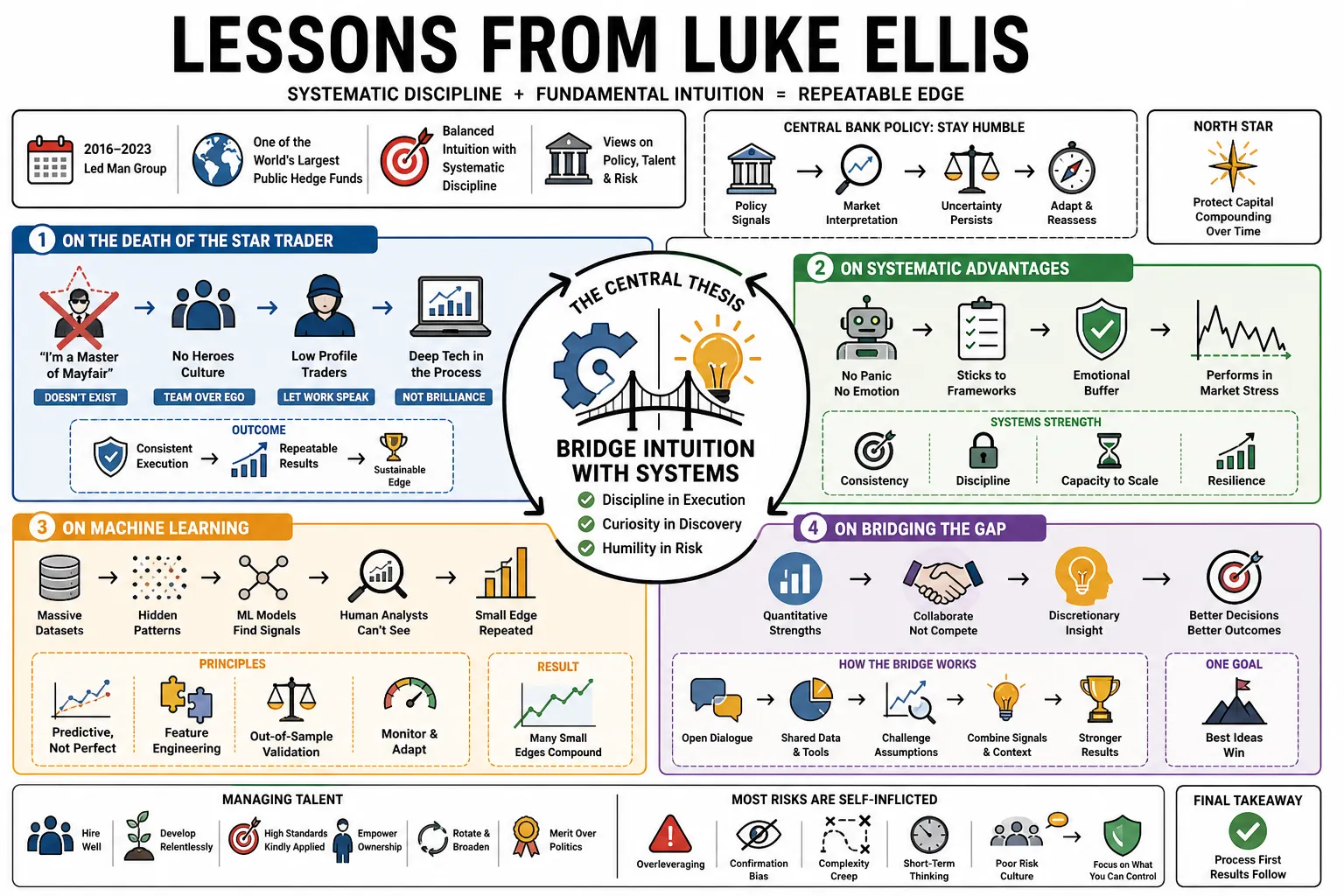

Part 1: Systematic and Discretionary Trading

- On the Death of the Star Trader: "The ones who’ve said 'I’m a Master of Mayfair', they don’t exist here, they won’t exist in the industry in the future." — Source: [Financial Times]

- On the Future of Trading: "The industry has moved toward traders who keep a low profile and integrate deep technology into their processes rather than relying on individual bursts of brilliance." — Source: [Financial Times]

- On Systematic Advantages: "Algorithms do not panic or deviate from their designated frameworks during periods of market stress, providing a vital emotional buffer." — Source: [Bloomberg Invest]

- On Machine Learning: "The value of artificial intelligence in finance lies in finding small, repeatable patterns across massive datasets that human analysts cannot perceive." — Source: [Man Group Insights]

- On Bridging the Gap: "There should be no war between quantitative and discretionary investing. The most successful firms blend fundamental insight with systematic discipline." — Source: [Goldman Sachs Exchanges]

- On Data Quality: "A quantitative model is only as useful as the hygiene of the data fed into it. Spending time scrubbing data is often more profitable than building a complex algorithm." — Source: [Masters in Business]

- On Emotional Bias: "Discretionary traders often convince themselves they are adapting to new information when they are simply rationalizing their previous mistakes." — Source: [Bloomberg Front Row]

- On Consistency: "A mediocre systematic strategy executed flawlessly over a decade will usually outperform a brilliant discretionary strategy plagued by human inconsistency." — Source: [Man Group Insights]

- On Algorithmic Limits: "Systematic models excel at normal market behavior but struggle when underlying macroeconomic rules fundamentally change overnight." — Source: [Bloomberg Invest]

Part 2: Market Dynamics and Efficiency

- On Market Behavior: "The market often takes the most painful route to the most obvious place." — Source: [The Macro Tourist]

- On Liquidity Illusions: "Investors often confuse rising prices with abundant liquidity, only realizing their error when everyone tries to exit the same door simultaneously." — Source: [Masters in Business]

- On Efficiency: "Markets are generally efficient over the long term but remain persistently inefficient in the short term due to human psychology and structural constraints." — Source: [Goldman Sachs Exchanges]

- On Asset Pricing: "There is a distinct difference between the fundamental value of an asset and the price someone is willing to pay for it on a Tuesday afternoon." — Source: [Financial Times]

- On Crowded Trades: "The danger in financial markets rarely comes from an isolated bad idea. It comes from a mediocre idea that too many smart people have borrowed money to execute." — Source: [Bloomberg Invest]

- On Volatility: "Volatility is simply the price of admission for long-term returns, whereas risk is the permanent loss of capital." — Source: [Man Group Insights]

- On Market Memory: "Financial markets have an incredibly short memory, predictably forgetting the lessons of the previous crisis just in time to participate in the next one." — Source: [Masters in Business]

- On Passive Investing: "The relentless flow of capital into passive index funds creates localized distortions that active managers with flexible mandates can exploit." — Source: [Financial Times]

- On Timing: "Being early in finance is often indistinguishable from being wrong, especially if you lack the capital to wait for the market to agree with you." — Source: [Goldman Sachs Exchanges]

Part 3: Central Bank Policy and Inflation

- On Controlling Inflation: "Central bankers have to keep rates high enough to cause pain and that will break things if they genuinely want to bring inflation under control." — Source: [The Wealth Advisor]

- On Unemployment: "Bringing down persistent inflation requires a willingness to see the unemployment rate rise despite the political unpopularity of such a move." — Source: [Bloomberg Invest]

- On Banking Crises: "We will have a significant number of more banks that will not exist 12 months to 24 months from now that exist today." — Source: [The Wealth Advisor]

- On the Era of Free Money: "A decade of zero interest rates fundamentally distorted capital allocation by rewarding speculative growth over cash-generating fundamentals." — Source: [Financial Times]

- On Policy Lag: "Changes in interest rates take time to permeate the real economy, meaning central banks are almost always driving while looking in the rearview mirror." — Source: [Masters in Business]

- On Inflation Psychology: "Once inflation becomes embedded in consumer psychology and wage negotiations, it requires significantly higher terminal rates to eradicate." — Source: [Bloomberg Invest]

- On Credit Suisse: "The failure of major legacy institutions highlights that regulatory capital buffers mean nothing if clients lose confidence and withdraw their deposits overnight." — Source: [Bloomberg Invest]

- On Central Bank Communication: "Forward guidance paints central banks into a corner, forcing them to choose between maintaining credibility and doing what the immediate data requires." — Source: [Goldman Sachs Exchanges]

- On the Return of Bonds: "As interest rates normalize, fixed income once again becomes a viable asset class rather than a parking space for dormant cash." — Source: [Man Group Insights]

Part 4: Risk and Portfolio Management

- On Self-Inflicted Wounds: "A lot of mistakes in life come when you think risk is caused by external forces, when in fact the weight of your own success is enough to pull you down without any outside help." — Source: [The Macro Tourist]

- On Diversification: "True diversification requires finding assets that behave differently under extreme stress instead of simply buying assets with different names on their ticker symbols." — Source: [Masters in Business]

- On Leverage: "Leverage does not make a bad trade good. It simply ensures that a bad trade will remove you from the industry faster." — Source: [Financial Times]

- On Tail Risk: "Investors spend too much time worrying about frequent small losses and too little time preparing for the rare catastrophic events that actually destroy portfolios." — Source: [Man Group Insights]

- On the Definition of Risk: "Risk is not a single number on a spreadsheet. It is the probability of failing to meet your long-term obligations to your clients." — Source: [Goldman Sachs Exchanges]

- On Position Sizing: "The difference between a great investor and a bankrupt one is rarely the quality of their ideas, but their discipline in sizing those ideas appropriately." — Source: [Bloomberg Front Row]

- On Drawdowns: "Every strategy will eventually experience a drawdown. A firm's survival depends entirely on having a pre-determined plan for when that happens." — Source: [Masters in Business]

- On Uncorrelated Returns: "True alpha is incredibly difficult to find, which is why clients pay premium fees when managers can deliver it without correlation to the broader market." — Source: [Man Group Insights]

- On Risk Limits: "A firm must enforce hard risk limits regardless of a trader's past performance, because the market does not care about historical track records." — Source: [Financial Times]

- On Hedging: "A hedge bought only after the market has already crashed is a panic tax." — Source: [Bloomberg Invest]

Part 5: Cryptocurrencies and Speculation

- On Crypto's Value: "If you look at cryptocurrencies as a whole, it is a pure trading instrument. There is no inherent worth in it whatsoever. It is a tulip bulb." — Source: [Integrity Risk International]

- On Trading Volatility: "While crypto lacks fundamental value, its extreme price volatility makes it fertile ground for quantitative trading strategies designed to capture momentum." — Source: [Financial Times]

- On Store of Value: "A reliable store of value cannot routinely lose half its purchasing power in a matter of weeks based on social media posts." — Source: [Bloomberg Front Row]

- On Blockchain Technology: "The underlying distributed ledger technology has genuine applications for settlement and clearing, entirely distinct from the speculation in digital tokens." — Source: [Goldman Sachs Exchanges]

- On Regulatory Arbitrage: "Much of the early profit in the crypto space was derived from operating outside traditional financial regulations, a window that is rapidly closing." — Source: [Financial Times]

- On Speculative Bubbles: "Financial history is filled with assets that people bought simply because they believed someone else would pay more for them tomorrow. Crypto is the digital version." — Source: [Masters in Business]

- On Institutional Adoption: "Institutional investors require custodial safety and regulatory clarity, which many crypto ecosystems still fail to provide reliably." — Source: [Bloomberg Invest]

- On Retail Speculation: "It is concerning when retail investors allocate significant portions of their retirement savings to assets that operate completely detached from cash flows." — Source: [Financial Times]

- On Tokenization: "Tokenizing traditional assets like real estate or bonds may improve administrative efficiency, but it does not inherently change the value of the underlying asset." — Source: [Man Group Insights]

- On Market Maturation: "If cryptocurrencies are to survive long-term, the space must transition from a casino mentality to providing actual utility in the global payment system." — Source: [Goldman Sachs Exchanges]

Part 6: Talent, Diversity, and Hiring

- On Vetting Candidates: "We kiss a lot of frogs before finding the right portfolio managers. The process requires deep patience and rigorous screening." — Source: [Investment Week]

- On Diversity Initiatives: "Efforts to improve diversity are not about box ticking. They are simply about hiring and keeping the best people." — Source: [eFinancialCareers]

- On Repeatable Processes: "When hiring investment talent, the focus should be on whether they have a clear, structured, and repeatable process rather than past return numbers." — Source: [Investment Week]

- On Cognitive Diversity: "A room full of people who went to the same universities and studied the same subjects will inevitably miss the same tail risks." — Source: [Bloomberg Front Row]

- On Retaining Talent: "The best quantitative minds want access to the cleanest data, the fastest compute power, and a culture that lets them test ideas without corporate bureaucracy." — Source: [Man Group Insights]

- On Ego: "The ideal hire is highly intelligent and deeply curious, but lacks the destructive ego that prevents them from admitting when their model is broken." — Source: [Masters in Business]

- On Training: "You cannot teach someone to have a high tolerance for ambiguity, but you can teach a mathematically gifted person the mechanics of financial markets." — Source: [Financial Times]

- On the Long Game: "Identifying top talent often takes years of relationship building. It is a long-term investment instead of a transactional hiring process." — Source: [Investment Week]

- On Team Construction: "The most resilient trading desks are built by pairing individuals with complementary skill sets, rather than hiring exact replicas of the current top performer." — Source: [Goldman Sachs Exchanges]

Part 7: Corporate Culture and Behavior

- On Ethical Standards: "Finance is terrible for accepting bad behaviour, particularly if somebody makes money. But that is a terrible shortcut and it is a shortcut to ruin, because if you accept bad behaviour it will spread." — Source: [Investment Week]

- On Environmental Responsibility: "Climate change is an urgent challenge and asset managers can and must act as powerful drivers for much-needed climate action." — Source: [Net Zero Asset Managers]

- On Accountability: "A healthy corporate culture requires holding high earners to the exact same behavioral standards as junior analysts." — Source: [Bloomberg Front Row]

- On Career Progression: "I have immensely enjoyed my career; it's hard to choose highlights and lowlights as everything has been a path to get me to where I am today." — Source: [University of Bristol]

- On Transparency: "When a trade goes wrong, the culture must encourage immediate transparency rather than hiding the loss. Problems only compound in the dark." — Source: [Masters in Business]

- On Collaboration: "Modern asset management requires fluid collaboration across technology, data, and execution teams, ending the era of siloed traders guarding ideas from colleagues." — Source: [Financial Times]

- On Institutional Arrogance: "Success often breeds dangerous organizational complacency. The firm must constantly act as though its competitive advantage is expiring." — Source: [Goldman Sachs Exchanges]

- On Fiduciary Duty: "The primary obligation is always to the client's capital, which means checking personal ego at the door when constructing portfolios." — Source: [Man Group Insights]

- On Leading Through Crisis: "During periods of market panic, leadership is about over-communicating with clients and ensuring the operational machinery of the firm remains flawless." — Source: [Bloomberg Invest]

- On Adaptability: "An enduring financial institution must be willing to rebuild its core technological infrastructure every few years, regardless of the temporary discomfort." — Source: [Masters in Business]

Part 8: The Hedge Fund Industry's Future

- On Consolidation: "The barrier to entry in the quantitative hedge fund space is rising exponentially, heavily favoring established firms with massive technology budgets." — Source: [Financial Times]

- On Fee Structures: "Clients will only pay hedge fund fees if the manager can explicitly prove they are providing returns impossible to attain through cheap passive vehicles." — Source: [Goldman Sachs Exchanges]

- On Data as a Moat: "In the future, a firm's most valuable asset will be its proprietary pipelines of unstructured, high-quality data rather than its trading algorithms." — Source: [Man Group Insights]

- On Regulatory Evolution: "The industry must accept that increased regulatory scrutiny is a permanent fixture, and compliance should be viewed as a operational core competency rather than a burden." — Source: [Bloomberg Front Row]

- On Customization: "Institutional clients no longer want off-the-shelf funds. They expect highly customized solutions tailored to their specific liability profiles and ESG requirements." — Source: [Financial Times]

- On the Death of the Maverick: "The romanticized image of the rogue trader acting on gut instinct has been permanently replaced by teams of analysts evaluating statistical probabilities." — Source: [Masters in Business]

- On Speed vs. Intelligence: "The arms race for microsecond execution speed has yielded diminishing returns. The new frontier is building models that can interpret complex data faster than competitors." — Source: [Bloomberg Invest]

- On ESG Integration: "Sustainable investing is a fundamental shift in capital allocation, independent of marketing trends." — Source: [Man Group Insights]

- On Institutional Longevity: "A successful hedge fund must transition from being reliant on its founders to operating as an enduring firm with institutionalized processes." — Source: [Goldman Sachs Exchanges]