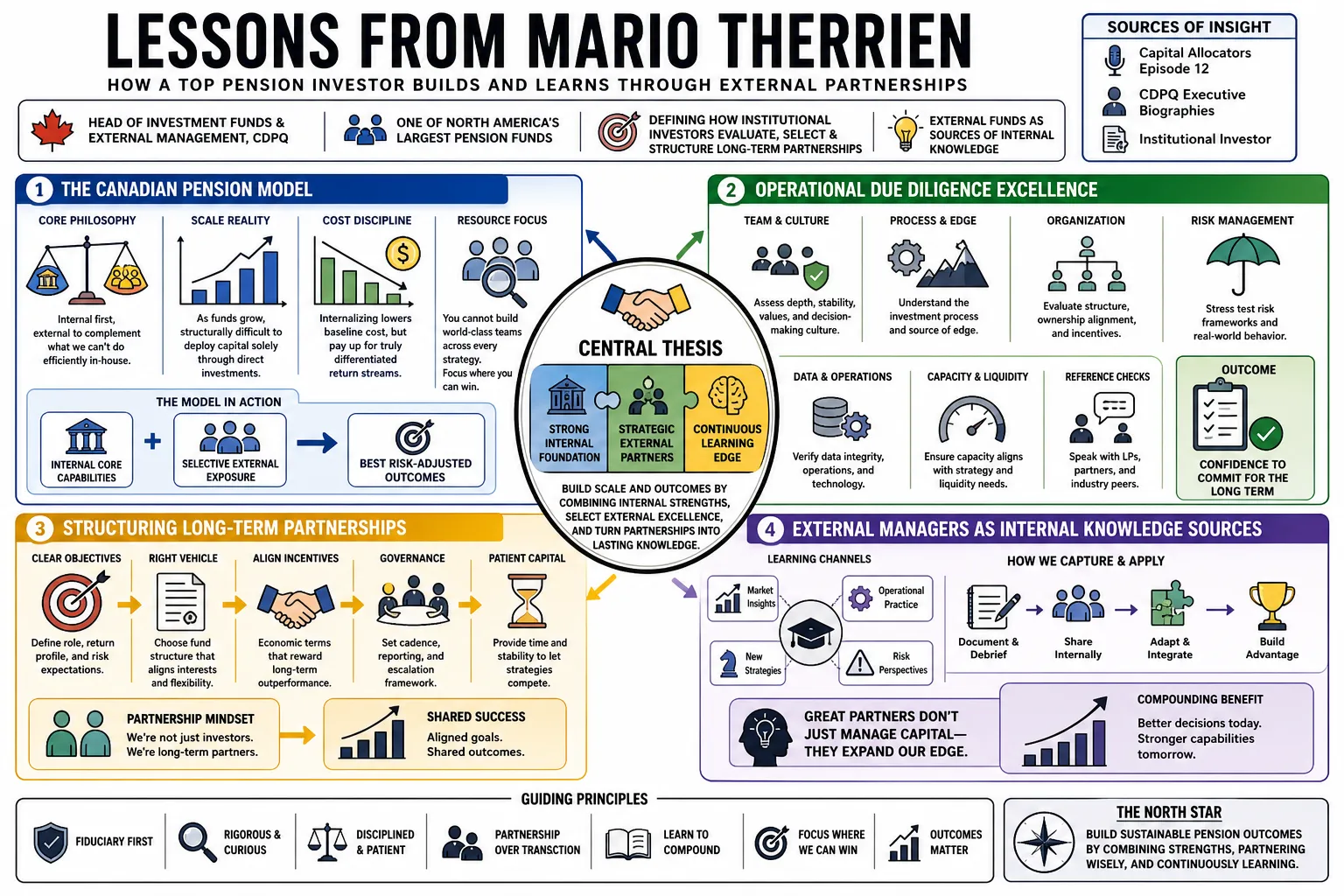

Mario Therrien serves as the Head of Investment Funds and External Management at CDPQ, one of North America's largest pension funds. He is known for defining how large institutional investors evaluate, select, and structure long-term partnerships with external asset managers. This profile compiles his practical insights on the Canadian pension model, operational due diligence, and treating external funds as sources of internal knowledge.

Part 1: The Canadian Pension Model

- On the core philosophy: "The Canadian model relies heavily on internal management capabilities, but we use external managers strategically to complement what we cannot do efficiently in-house." — Source: Capital Allocators Episode 12

- On scale: "As pension funds grow, it becomes structurally difficult to deploy capital solely through direct investments without altering your risk profile." — Source: CDPQ Executive Biographies

- On cost management: "Internalizing asset management fundamentally lowers the baseline cost, but you must be willing to pay a premium when an external manager offers a truly differentiated return stream." — Source: Institutional Investor

- On resource allocation: "You cannot build world-class teams for every single niche market. The model requires honesty about your internal limitations." — Source: Top1000Funds

- On alignment of interests: "We are managing capital for depositors. Every structural decision in the Canadian model is anchored to ensuring the people managing the money share the long-term horizon of those depositors." — Source: CAIA Association Podcast

- On independence: "A key feature of the model is governance independence. The investment team must be insulated from political cycles to make decisions with a ten-to-twenty year horizon." — Source: Capital Allocators Episode 12

- On illiquidity: "The Canadian model takes advantage of our long liabilities by capturing the illiquidity premium in private markets, which is difficult for retail investors to replicate." — Source: Institutional Investor

- On agility: "Even with billions in assets, the internal structure must allow for rapid deployment when market dislocations occur. Bureaucracy is the enemy of alpha." — Source: Top1000Funds

- On benchmarking: "We measure our internal teams with the same exact rigor and against the same hurdles as any external manager we might hire." — Source: Capital Allocators Episode 12

- On peer collaboration: "Canadian pensions often share notes on best practices. There is a healthy competition for returns, but a unified approach to improving the industry's structural standards." — Source: CDPQ Governance Reports

Part 2: External Manager Selection

- On finding edges: "We look for managers who operate at the fringes. If they are just hugging an index, we can do that ourselves for a fraction of the cost." — Source: Institutional Investor

- On qualitative assessment: "You can screen data all day, but selecting a manager ultimately comes down to understanding the culture of their firm and how they handle adversity." — Source: Capital Allocators Episode 12

- On capacity constraints: "The best managers often close their funds. Part of our job is identifying talent early enough, before they hit their asset ceiling and their returns begin to dilute." — Source: Top1000Funds

- On strategy drift: "A manager changing their mandate because a new asset class is trendy is a massive red flag. We hire them for their specific expertise, not to be generalists." — Source: CAIA Association Podcast

- On evaluating failure: "I want to see how a manager explains a bad year. If they blame the market, it shows a lack of introspection. If they explain the flaw in their process, we can work with that." — Source: Capital Allocators Episode 12

- On team dynamics: "We pay close attention to succession planning. A fund highly dependent on a single founder is a different risk profile than a fund with a deep, incentivized bench." — Source: SBAI Publications

- On the interview process: "The most revealing question during diligence is often asking a manager what their superpower is, and then testing if their portfolio actually reflects that claim." — Source: Capital Allocators Book

- On manager turnover: "Firing a manager is expensive and time-consuming. We do our diligence with the intention of holding the relationship for a decade." — Source: Top1000Funds

- On quantitative metrics: "Past performance is a poor indicator of the future, but the volatility of that past performance tells you a lot about how they manage risk." — Source: CDPQ Strategy Documents

- On specialized mandates: "We prefer managers who know exactly what they are good at and refuse to stray from it, even when raising capital would be easy." — Source: Institutional Investor

Part 3: Generating Alpha & Risk Management

- On defining alpha: "True alpha is scarce. Most of what the industry calls alpha is just a disguised beta factor that can be replicated systematically." — Source: Capital Allocators Episode 12

- On risk appetite: "Taking risk is not the problem; failing to understand the risk you are taking is where institutions lose money." — Source: CAIA Association Podcast

- On portfolio construction: "You do not generate alpha by stacking fifty managers together. You just end up paying active fees for an index fund. Concentration is required." — Source: Top1000Funds

- On downside protection: "We spend more time analyzing how a strategy behaves during a market drawdown than we do projecting its upside during a bull market." — Source: Institutional Investor

- On leverage: "Leverage does not create returns; it only magnifies them. If the underlying strategy has a flaw, leverage will expose it violently." — Source: SBAI Board Communications

- On correlation: "The biggest risk in a large portfolio is hidden correlation. Managers who look different on paper often hold the exact same trades when liquidity dries up." — Source: Capital Allocators Episode 12

- On liquidity mismatch: "You cannot offer daily liquidity to your investors if you are investing in assets that take months to sell. That structure always breaks." — Source: CDPQ Annual Reports

- On conviction: "If a manager has a high conviction idea, it needs to be sized appropriately in the fund. A one percent position does not move the needle for them or for us." — Source: Top1000Funds

- On market cycles: "Strategies that work in a declining rate environment will not necessarily work when rates rise. The alpha generation engine must be adaptable." — Source: CAIA Association Podcast

- On risk culture: "Risk management cannot be a separate department that just says 'no'. It has to be integrated into the portfolio manager's daily process." — Source: SBAI Publications

Part 4: Strategic Partnerships & Relationships

- On the nature of partnerships: "We do not want to be just a source of capital. We want to be a strategic partner who can offer insights, co-investment capital, and scale." — Source: CDPQ Executive Biographies

- On co-investments: "Co-investing allows us to deploy more capital alongside our best managers without paying the standard fee structure on the additional assets." — Source: Institutional Investor

- On communication: "The best partnerships feature transparent communication, especially when things are going poorly. I want the manager to call me before I read about it in the news." — Source: Capital Allocators Episode 12

- On structuring fees: "Fee structures need to ensure the manager gets rich alongside us, not just from our management fees regardless of performance." — Source: SBAI Publications

- On mutual benefit: "A partnership only lasts if it solves a problem for both sides. We provide stable capital; they provide access to specialized deal flow." — Source: Top1000Funds

- On term sheets: "The legal negotiation sets the tone for the entire relationship. If they fight us on basic transparency rights, the partnership is usually doomed." — Source: CAIA Association Podcast

- On capacity rights: "When a manager does well, we want the right to scale up our investment. Negotiating capacity early is critical." — Source: Capital Allocators Episode 158

- On sharing networks: "We regularly introduce our external managers to one another if we think they can collaborate or share insights on different markets." — Source: Institutional Investor

- On crisis management: "You find out who your real partners are during a liquidity crunch. The managers who treat you fairly when capital is scarce are the ones you keep." — Source: Top1000Funds

Part 5: Knowledge Management & Talent

- On intellectual capital: "We treat our external manager network as an extension of our internal research department. The knowledge they provide is often as valuable as the returns." — Source: Top1000Funds

- On internal sharing: "If an external manager gives us a brilliant macro insight, it is useless unless we have a system to route that information to our internal trading desks." — Source: Capital Allocators Episode 12

- On intellectual humility: "You have to accept that there are people in the market who know specific sectors better than you do. That is why you hire them." — Source: CAIA Association Podcast

- On talent retention: "The hardest part of building an internal team is keeping your best people from leaving to start their own funds. You have to offer them a unique culture and scale." — Source: Institutional Investor

- On continuous learning: "The market is a constantly evolving mechanism. An investment team that stops reading and updating its priors will underperform within three years." — Source: Capital Allocators Book

- On manager transparency: "We expect managers to walk us through their exact investment thesis on specific trades. If they say it is a 'black box', we pass." — Source: SBAI Publications

- On mentoring: "Senior investors have an obligation to train the next generation. The apprenticeship model is the only way this business actually transfers skill." — Source: CDPQ Executive Biographies

- On data utilization: "Firms have more data than ever, but less wisdom. The differentiator is having talent that knows what data to ignore." — Source: CAIA Association Podcast

- On cross-pollination: "We learn about private market trends from our public market managers, and vice versa. Connecting those dots is where an allocator earns their keep." — Source: Top1000Funds

Part 6: Hedge Funds & Alternative Investments

- On the role of alternatives: "Hedge funds should not be expected to beat the S&P 500 during a massive bull market. They are in the portfolio to provide uncorrelated returns." — Source: Capital Allocators Episode 158

- On industry maturity: "The alternative investment industry has grown up. It is no longer just a cottage industry of star traders; it requires institutional infrastructure." — Source: SBAI Board Communications

- On absolute return: "An absolute return mandate means exactly that. We expect positive returns regardless of whether the broader equity markets are up or down." — Source: CDPQ Strategy Documents

- On quantitative strategies: "Systematic funds remove human emotion, but they introduce model risk. You have to understand the assumptions hardcoded into the algorithm." — Source: Capital Allocators Manager Meetings

- On illiquidity premiums in credit: "Private credit has stepped in where banks retreated, but investors must accurately price the fact that they cannot exit these loans quickly." — Source: Institutional Investor

- On venture capital: "Venture requires the longest time horizon and tolerance for failure. You are paying for the option on a handful of massive outliers." — Source: CDPQ Executive Biographies

- On strategy crowding: "When too much capital chases a specific arbitrage strategy, the spread collapses. We track how crowded a trade is before we allocate." — Source: Top1000Funds

- On short selling: "Short selling is structurally difficult and expensive, but managers who can do it well provide essential ballast to a portfolio." — Source: CAIA Association Podcast

- On fee compression: "There is downward pressure on alternative fees, which is healthy. Managers must justify their 2-and-20 by delivering pure alpha, not levered beta." — Source: Capital Allocators Episode 158

Part 7: Standards, Transparency & Due Diligence

- On standardization: "Standardized practices across the alternative industry reduce friction. It allows allocators to compare apples to apples when evaluating managers." — Source: SBAI Publications

- On operational due diligence: "A brilliant trader with a terrible back office is uninvestable. Operational risk can wipe out a fund just as fast as market risk." — Source: Capital Allocators Episode 12

- On valuation practices: "Illiquid assets must be marked accurately. If a manager controls their own valuation process without third-party checks, the conflict of interest is too high." — Source: SBAI Board Communications

- On ESG integration: "Environmental, social, and governance factors are not just marketing tools; they are material financial risks that managers must explicitly model." — Source: CDPQ Strategy Documents

- On cyber security: "We vet the cyber infrastructure of our external managers as rigorously as their balance sheets. A data breach is a direct threat to our capital." — Source: Top1000Funds

- On regulatory compliance: "A culture of compliance starts at the top. If the founder treats the chief compliance officer as an annoyance, that is a severe cultural flaw." — Source: Institutional Investor

- On reporting: "Transparency is not just sending us a monthly performance number. We need to see position-level data to analyze true exposures." — Source: SBAI Publications

- On background checks: "Character matters in this business. We do extensive background checks because when markets panic, you need to trust the person managing the money." — Source: CAIA Association Podcast

- On independent boards: "Funds need independent directors who are actually willing to challenge the founder, not just rubber-stamp their decisions." — Source: SBAI Board Communications

Part 8: Institutional Governance & Alignment

- On fiduciary duty: "Every decision we make traces back to the pensioners. If an investment does not serve their long-term security, we do not make it." — Source: CDPQ Executive Biographies

- On time horizons: "Institutions have a distinct advantage over retail investors: time. We can afford to endure short-term volatility to capture long-term premiums." — Source: Top1000Funds

- On committee structures: "Investment committees exist to test assumptions, not to manage portfolios by consensus. Consensus usually leads to mediocre returns." — Source: Capital Allocators Episode 12

- On evolving mandates: "An institution must be willing to rewrite its rulebook when macroeconomic conditions shift permanently. Dogma destroys capital." — Source: Institutional Investor

- On incentive design: "If you pay an allocator an annual bonus based on short-term returns, they will never make the difficult, long-term investments the fund actually needs." — Source: CAIA Association Podcast

- On leaving a legacy: "Our responsibility is to leave the industry in a better state than we found it, pushing for better standards and fairer structures." — Source: SBAI Publications

- On institutional memory: "When senior people retire, they take decades of context with them. Building a system to preserve institutional memory is a critical governance task." — Source: Top1000Funds

- On strategic patience: "Sometimes the best investment decision an institution can make is to hold cash and do absolutely nothing while the market acts irrationally." — Source: Capital Allocators Episode 12

- On the ultimate goal: "We are not here to beat an arbitrary benchmark for bragging rights. We are here to ensure that capital is there when people retire." — Source: CDPQ Executive Biographies