Lessons from Mark Baumgartner

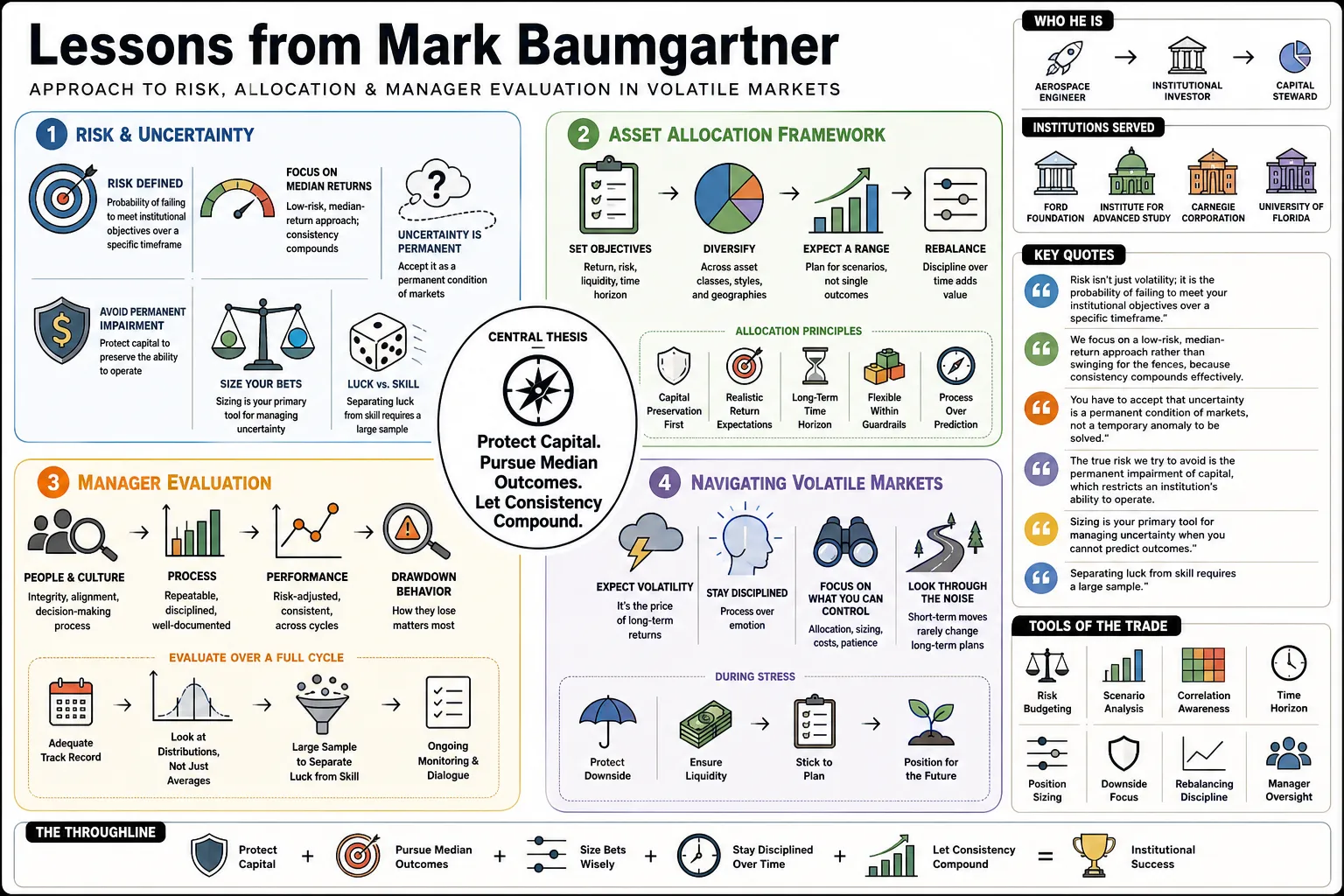

Mark Baumgartner is an aerospace engineer turned institutional investor who has managed capital for the Ford Foundation, the Institute for Advanced Study, the Carnegie Corporation, and the University of Florida. This profile details his approach to asset allocation, focusing on how he assesses risk and evaluates managers in volatile markets.

Part 1: Risk and Uncertainty

- On defining risk: "Risk isn't just volatility; it is the probability of failing to meet your institutional objectives over a specific timeframe." — Source: [Capital Allocators Episode 78]

- On median returns: "We focus on a low-risk, median-return approach rather than swinging for the fences, because consistency compounds effectively." — Source: [Capital Allocators Episode 78]

- On uncertainty: "You have to accept that uncertainty is a permanent condition of markets, not a temporary anomaly to be solved." — Source: [Greenwich Economic Forum]

- On permanent impairment: "The true risk we try to avoid is the permanent impairment of capital, which restricts an institution's ability to operate." — Source: [Capital Allocators Episode 78]

- On sizing bets: "Sizing is your primary tool for managing uncertainty when you cannot predict outcomes." — Source: [Capital Allocators Episode 128]

- On luck vs. skill: "Separating luck from skill requires a large sample size and a deep understanding of the underlying process." — Source: [Capital Allocators Episode 78]

- On market efficiency: "Markets are mostly efficient, but they break down in specific, observable ways during periods of stress." — Source: [Business Today Interview]

- On risk models: "A model is a tool for thinking, not a substitute for judgment. If you follow a model blindly, you will eventually hit a wall." — Source: [Capital Allocators Episode 78]

- On expected value: "We evaluate every decision through the lens of expected value, accounting for the full distribution of potential outcomes." — Source: [Capital Allocators Episode 128]

- On tail risks: "You don't just insure against the tail risks you can imagine; you structure a portfolio to survive the ones you can't." — Source: [Greenwich Economic Forum]

Part 2: Market Crises

- On action vs. inaction: "There’s this gut reaction to kind of throw out things that don’t make sense to you, throw things out that you feel are useless, and act. And I would suggest that that is a decision; everything we do is a decision. So action or inaction are both decisions." — Source: [Capital Allocators Episode 128]

- On crisis planning: "I’d say the rule of thumb was, no matter what your project is, spend the first 10% of that project planning and thinking." — Source: [Capital Allocators Episode 128]

- On assessing market drops: "We have to ask: What is it that we’re really seeing here? Is this a head fake? What do we really believe about what’s coming?" — Source: [Capital Allocators Episode 128]

- On discounting the future: "During a crisis, you must determine if markets have properly discounted the future, or if there is something else underlying the panic." — Source: [Capital Allocators Episode 128]

- On rebalancing: "Rebalancing during a crisis is painful but necessary; it forces you to buy what is unloved and sell what feels safe." — Source: [Greenwich Economic Forum]

- On liquidity: "Liquidity is a resource you hoard during good times so you can deploy it when it becomes scarce and valuable." — Source: [Capital Allocators Episode 128]

- On market panic: "Panic is just the market repricing risk rapidly and uniformly. It creates the opportunity set for the next cycle." — Source: [Business Today Interview]

- On pausing: "Sometimes the best immediate reaction to a shock is simply to pause and ensure you understand the new environment." — Source: [Capital Allocators Episode 128]

- On historical precedents: "History doesn't give you a map for the current crisis, but it gives you a dictionary to understand the language the market is speaking." — Source: [Capital Allocators Episode 78]

- On portfolio resilience: "A resilient portfolio bends during a crisis but doesn't break, allowing you to participate in the eventual recovery." — Source: [Greenwich Economic Forum]

Part 3: Manager Selection

- On reference checks: "It is incredibly revealing to ask about past terminations and how a manager handled the exit of a client." — Source: [Capital Allocators Book]

- On tone awareness: "Ways that you don’t want to do this are to be tone-deaf. I’ve seen some very absurd asks coming through email... that I’m almost sure could not have had a human touch." — Source: [Capital Allocators Episode 128]

- On manager alignment: "We look for managers whose personal incentives and firm structure are perfectly aligned with our long-term goals." — Source: [Capital Allocators Episode 78]

- On organizational stability: "The best investment strategy in the world will fail if the organization executing it is unstable or fractured." — Source: [Business Today Interview]

- On transparency: "Transparency isn't just about getting data; it's about understanding how a manager thinks when things go wrong." — Source: [Capital Allocators Episode 128]

- On strategy drift: "We monitor closely for style drift, because we hire managers to perform a specific function within the broader portfolio." — Source: [Capital Allocators Episode 78]

- On capacity constraints: "Great strategies often have limited capacity. A manager's willingness to close their fund is a strong signal of integrity." — Source: [Greenwich Economic Forum]

- On competitive advantage: "You have to be able to clearly articulate a manager's edge. If you can't, they probably don't have one." — Source: [Capital Allocators Episode 78]

- On manager communication: "How a manager communicates during a drawdown tells you more about their character than how they communicate during a bull market." — Source: [Capital Allocators Episode 128]

- On due diligence: "Due diligence is an ongoing process of verifying that the reasons you underwrote the investment remain intact." — Source: [Business Today Interview]

Part 4: Asset Allocation

- On the primary mandate: "The mandate is not to choose a strategy and stick to it; the mandate is to achieve an objective given the opportunity set that we face." — Source: [Capital Allocators Episode 128]

- On opportunity sets: "Your allocation should dynamically adapt as the opportunity set expands or contracts across different asset classes." — Source: [Capital Allocators Episode 128]

- On diversification: "True diversification means holding assets that will behave differently under varying macroeconomic regimes." — Source: [Capital Allocators Episode 78]

- On illiquidity premiums: "You should only lock up capital if the illiquidity premium compensates you adequately for the loss of optionality." — Source: [Greenwich Economic Forum]

- On private markets: "Private investments require a different underwriting standard because mistakes are much harder to correct." — Source: [Capital Allocators Episode 78]

- On absolute return: "Absolute return strategies serve as a buffer, providing uncorrelated performance when equities face headwinds." — Source: [Business Today Interview]

- On asset class labels: "Don't get trapped by labels. Look at the underlying risk factors of an investment to understand its true role in the portfolio." — Source: [Capital Allocators Episode 78]

- On compounding: "Asset allocation is ultimately an exercise in allowing uninterrupted compounding to do the heavy lifting over decades." — Source: [Capital Allocators Episode 128]

- On benchmark constraints: "If you tie yourself too closely to a benchmark, you forfeit the ability to take advantage of obvious dislocations." — Source: [Greenwich Economic Forum]

Part 5: Institutional Governance

- On board relations: "A successful investment office requires a board that provides oversight without interfering in day-to-day manager selection." — Source: [Capital Allocators Episode 78]

- On institutional missions: "The portfolio exists entirely to serve the mission of the institution. We cannot forget the end beneficiary." — Source: [Business Today Interview]

- On spending rules: "The spending policy and the investment policy must be tightly linked; a mismatch will eventually lead to institutional stress." — Source: [Capital Allocators Episode 128]

- On committee structures: "Investment committees function best when they focus on policy and risk tolerance, empowering the CIO to execute the strategy." — Source: [Greenwich Economic Forum]

- On policy portfolios: "A policy portfolio sets the baseline expectation, but the investment team must have the flexibility to deviate when conditions warrant." — Source: [Capital Allocators Episode 78]

- On reporting: "Transparency with the investment committee builds the trust necessary to sustain difficult positions during periods of underperformance." — Source: [Business Today Interview]

- On time horizons: "Endowments have the rare advantage of a perpetual time horizon. Governance must protect that advantage from short-term pressures." — Source: [Capital Allocators Episode 128]

- On risk tolerance: "An institution's true risk tolerance is only revealed during a severe drawdown, not during the planning phase." — Source: [Capital Allocators Episode 78]

- On staff retention: "Building a top-tier investment team requires creating a culture where intellectual curiosity is rewarded and debate is encouraged." — Source: [Greenwich Economic Forum]

Part 6: Engineering Frameworks in Finance

- On systems thinking: "An engineering background trains you to view the portfolio as a complex system of interacting components, rather than isolated bets." — Source: [Capital Allocators Episode 78]

- On constraints: "Just like in aerospace engineering, in finance you optimize for an objective function subject to very specific, non-negotiable constraints." — Source: [Business Today Interview]

- On stress testing: "We subject the portfolio to rigorous stress tests, similar to how you would test a physical structure for breaking points." — Source: [Capital Allocators Episode 78]

- On feedback loops: "Good systems have built-in feedback loops that force you to re-evaluate your assumptions as new data arrives." — Source: [Capital Allocators Episode 128]

- On margin of safety: "Engineering teaches you to build in a margin of error. In investing, that translates to a margin of safety on valuation." — Source: [Greenwich Economic Forum]

- On process over outcome: "You cannot control the market outcome, but you can engineer a robust decision-making process that tilts probabilities in your favor." — Source: [Capital Allocators Episode 78]

- On complexity: "Unnecessary complexity in a portfolio introduces failure points. We prefer elegant, straightforward solutions whenever possible." — Source: [Business Today Interview]

- On quantitative tools: "Quantitative models are excellent for identifying structural anomalies, but human judgment is required to understand the context." — Source: [Capital Allocators Episode 78]

- On continuous improvement: "An investment process should iterate. You build it, test it, find its flaws, and refine it continuously." — Source: [Greenwich Economic Forum]

Part 7: Active Management

- On the future of active management: "I think active management is going to have a golden resurgence here in the coming years." — Source: [Capital Allocators Episode 128]

- On passive investing: "Passive investing is a useful tool for cheap beta, but it provides zero protection when the broad market fundamentals deteriorate." — Source: [Greenwich Economic Forum]

- On market dislocations: "Active managers earn their fees by navigating dislocations that index funds are structurally forced to absorb." — Source: [Capital Allocators Episode 128]

- On niche strategies: "The best active opportunities are often found in niche, complex markets where capital is scarce and expertise is required." — Source: [Business Today Interview]

- On structural inefficiencies: "We want to partner with managers who exploit structural inefficiencies rather than taking cyclical, directional bets." — Source: [Capital Allocators Episode 78]

- On manager conviction: "High conviction is required for active management to work. If a manager isn't willing to concentrate their best ideas, they become a closet indexer." — Source: [Capital Allocators Episode 78]

- On fee structures: "We are happy to pay performance fees for true alpha, but we refuse to pay active fees for passive beta." — Source: [Greenwich Economic Forum]

- On contrarian thinking: "Successful active management requires the willingness to look foolish in the short term to be proven right in the long term." — Source: [Business Today Interview]

- On agility: "Smaller, nimble managers often have an advantage over mega-funds because they can navigate specialized markets without moving the price." — Source: [Capital Allocators Episode 128]

Part 8: Leadership and Team Dynamics

- On intellectual honesty: "The most important trait in an investment team is intellectual honesty—the ability to admit when an initial thesis was wrong." — Source: [Capital Allocators Episode 78]

- On cognitive diversity: "You don't want a team of people who think exactly like you. You want a team that approaches the same problem from entirely different angles." — Source: [Greenwich Economic Forum]

- On debate: "We structure our meetings to encourage dissenting opinions. If everyone agrees immediately, we haven't thought about it hard enough." — Source: [Business Today Interview]

- On decision journals: "Writing down the rationale for a decision before you make it prevents hindsight bias from clouding your post-mortems." — Source: [Capital Allocators Episode 78]

- On mentorship: "Developing young talent requires giving them real responsibility and allowing them to make guided mistakes." — Source: [Greenwich Economic Forum]

- On crisis communication: "During a market shock, clear and frequent communication with your team and your board is the only way to maintain institutional stability." — Source: [Capital Allocators Episode 128]

- On patience: "In investing, patience is an active discipline. Waiting for the right pitch is often the hardest part of the job." — Source: [Business Today Interview]

- On delegation: "As a CIO, your job shifts from picking assets to picking the people who pick the assets, and managing the overall risk framework." — Source: [Capital Allocators Episode 78]

- On ultimate accountability: "You can delegate authority, but you can never delegate accountability. The CIO owns the final outcome." — Source: [Greenwich Economic Forum]