Lessons from Martín Escobari

As Co-President of General Atlantic, Martín Escobari oversees global growth equity investments. His investing approach is shaped by early experiences with Bolivian hyperinflation and co-founding the Brazilian e-commerce site Submarino, prioritizing strict unit economics and structural resilience. This profile breaks down his frameworks for evaluating durable businesses, assessing founder psychology, and making decisive moves during economic downturns.

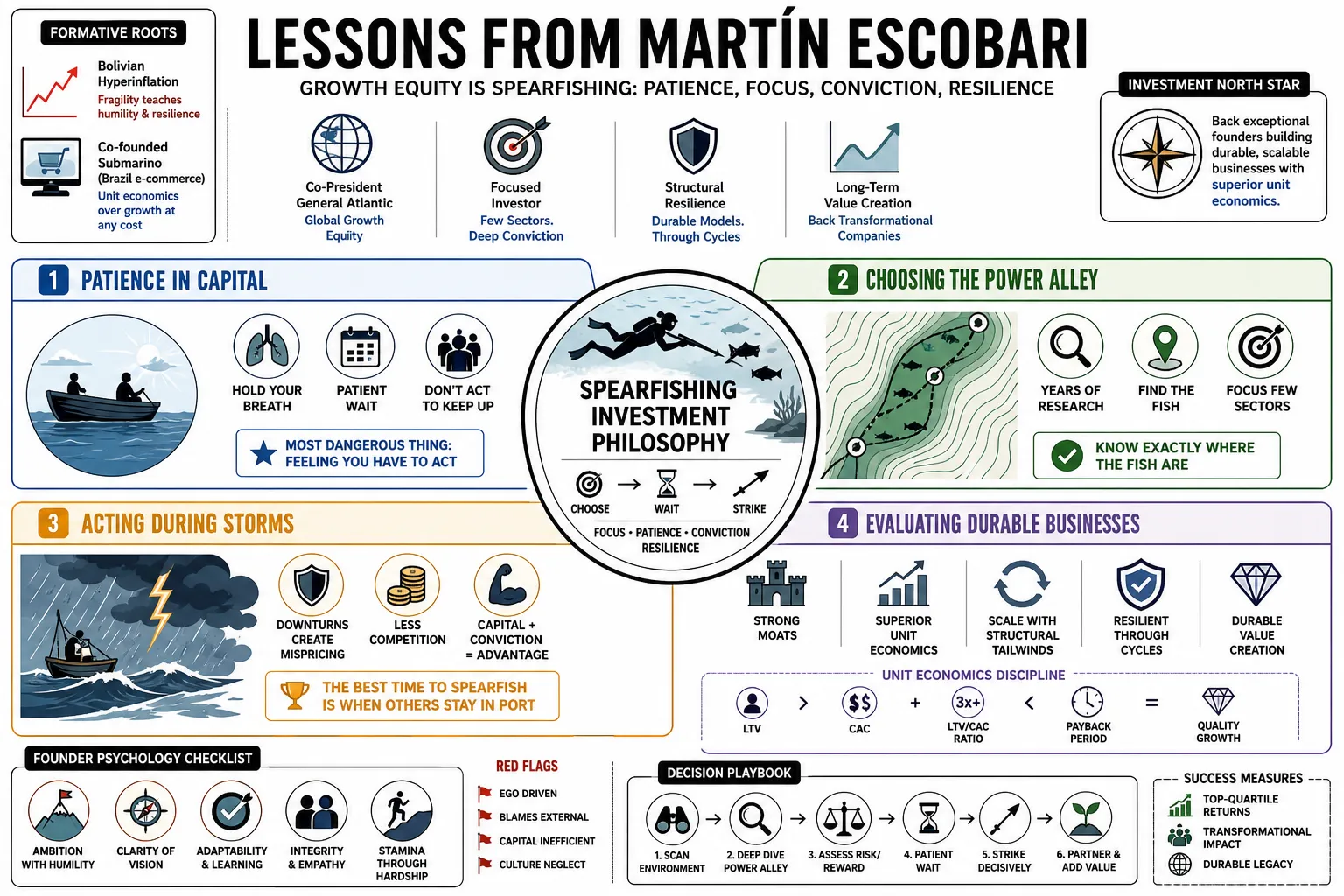

Part 1: The Spearfishing Investment Philosophy

- On the Spearfishing Metaphor: "Growth equity is like spearfishing. You do not cast a wide net; you choose your sector, wait patiently, and strike decisively when the right opportunity appears." — Source: [Invest Like the Best]

- On Patience in Capital: "You must be willing to sit on the boat holding your breath. The most dangerous thing an investor can do is feel they have to act simply because others are deploying capital." — Source: [Invest Like the Best]

- On Choosing the Power Alley: "Before you even get in the water, you have to know exactly where the fish are. We spend years researching a specific sector so that when the time comes, we act with conviction." — Source: [Masters in Business]

- On Acting During Storms: "The best time to spearfish is often during a storm. When markets are turbulent and others are retreating, that is when the best assets become available at fair prices." — Source: [People by WTF]

- On The Vulnerability of Discipline: "Saying no to mediocre deals feels vulnerable when your competitors are constantly announcing new investments. Discipline requires that temporary discomfort." — Source: [Invest Like the Best]

- On Long-Term Horizons: "We do not invest for the next quarter. We are underwriting secular themes that will play out over a decade, which allows us to ignore short-term market noise." — Source: [General Atlantic Perspectives]

- On Thesis-Driven Investing: "If you are reacting to deal flow, you are already too late. You must have a prepared mind and a developed thesis long before the pitch deck hits your desk." — Source: [20VC]

- On Recognizing Quality: "We are not looking for the cheapest company; we are looking for the absolute best company in a specific vertical. Growth equity is about backing the winner." — Source: [Invest Like the Best]

- On the Danger of Consensus: "Operating without the safety net of consensus is terrifying for most people, but it is the only way to generate outsized returns in private markets." — Source: [Masters in Business]

- On Capital Allocation: "Your most important decision is what you actively choose to pass on. The deals you reject define your portfolio as much as the ones you execute." — Source: [20VC]

Part 2: The Psychology of the Founder

- On the Founder's Wound: "The survivors of entrepreneurship are almost always people with a wound like intergenerational trauma, lost fortunes, or public failure, which refuses to let them sit still." — Source: [People by WTF]

- On Resilience: "You cannot teach resilience in a classroom. It is usually forged in environments of severe constraints and personal hardship." — Source: [Fintech Leaders]

- On the Motivation to Build: "People who have everything perfectly aligned rarely build massive companies. It is the people who feel they have something to prove to the world who endure the pain of company building." — Source: [People by WTF]

- On Assessing Leadership: "When I meet a founder, I try to figure out what happens when everything goes wrong. In a growth company, eventually, everything will go wrong." — Source: [Invest Like the Best]

- On the Role of Trauma: "Trauma functions as a superpower if it is channeled into productive ambition. It provides a level of endurance that normal incentives simply cannot match." — Source: [People by WTF]

- On Founder Empathy: "Having been a manager and an entrepreneur made me a better investor. I understand that hard things are genuinely hard." — Source: [Fintech Leaders]

- On the Illusion of the Spreadsheet: "I understand that a spreadsheet is a theoretical document. What matters is what gets implemented in the real world by real people with real customers and real competitors." — Source: [Fintech Leaders]

- On Partnership: "We are not trying to replace the founder; we provide the scaffolding around them so their specific genius can scale without breaking the company." — Source: [General Atlantic Perspectives]

- On Self-Awareness: "The best founders know exactly what they are bad at. They never try to hide their weaknesses; they hire aggressively to cover them." — Source: [20VC]

- On Evaluating Drive: "I look for a specific kind of unreasonable optimism. You have to be slightly delusional to start a company, but highly rational to scale it." — Source: [Invest Like the Best]

Part 3: Beautiful Business Models

- On Defining Beauty in Business: "A beautiful business captures significant gross margin by selling products at a high markup relative to their production cost, and doing it repeatedly." — Source: [Masters in Business]

- On the Durability of Margins: "The true test of beauty is whether those margins are sustainable over a lifetime or if they will be eroded by competitors." — Source: [Masters in Business]

- On Economic Moats: "To protect margins, a company must possess a moat. This is created through economies of scale, learning externalities, and network effects." — Source: [Masters in Business]

- On Agility as a Defense: "In modern markets, static moats are insufficient. Agility itself has become a primary defensive characteristic for beautiful businesses." — Source: [Masters in Business]

- On Unit Economics: "You cannot scale a flawed business model and expect the math to fix itself at the bottom line. The unit economics must be pristine early on." — Source: [20VC]

- On Pricing Power: "The ultimate indicator of a beautiful business model is pricing power. If you can raise prices without losing your customer base, you have created real value." — Source: [Invest Like the Best]

- On Capital Efficiency: "The best models grow efficiently, rather than merely growing quickly. They generate their own capital to fund future expansion." — Source: [General Atlantic Perspectives]

- On Recurring Revenue: "Predictability allows for long-term planning. Business models that require you to hunt for your dinner every single day are exhausting and rarely beautiful." — Source: [20VC]

- On Market Size: "You can have a beautiful model and a great team, but if the market size is tiny, the outcome will be tiny. We need massive total addressable markets to justify growth equity." — Source: [20VC]

Part 4: Artificial Intelligence and Technology

- On the Scale of AI: "AI is the greatest innovation since electricity. It is a fundamental platform shift that will rewrite how businesses operate at every level." — Source: [People by WTF]

- On White-Collar Automation: "The technology today is ready to automate we believe 60 to 70% of all white-collar workers. The implications for productivity are staggering." — Source: [People by WTF]

- On the Barrier of Diffusion: "The primary barrier to AI adoption is no longer the capability of the technology itself, but diffusion, meaning how quickly large organizations can actually integrate it into their workflows." — Source: [People by WTF]

- On Incumbents versus Upstarts: "AI is unique because it often empowers incumbents who already possess the data, rather than exclusively favoring scrappy startups. Data gravity matters immensely." — Source: [General Atlantic Perspectives]

- On Investment Professionals and AI: "AI will not replace the investment professional entirely, but an investment professional using AI will absolutely replace one who ignores it." — Source: [Capital Decanted]

- On the Speed of Innovation: "We are moving from a world of linear technological progress to exponential compounding. The planning cycles of businesses must shorten accordingly." — Source: [Invest Like the Best]

- On Healthcare and AI: "The intersection of artificial intelligence and healthcare is where we will see some of the most dramatic human and economic impacts over the next decade." — Source: [People by WTF]

- On Evaluative Frameworks for Tech: "When evaluating new tech, we ask whether it creates a completely new behavior, or simply makes an existing behavior slightly cheaper. The former creates generational wealth." — Source: [20VC]

- On the Utility Analogy: "Like electricity, the true value of AI lies in the millions of distinct applications and appliances built on top of the grid." — Source: [People by WTF]

Part 5: Navigating Market Cycles and Crises

- On the Darkest Moment: "Founders must survive the darkest moment of the night to take advantage of the opportunities that emerge in the morning." — Source: [Bloomberg Linea]

- On Preparing for Downturns: "We are not always in the darkest moment of the night, but it will inevitably come. You manage your balance sheet for the night, never the day." — Source: [Bloomberg Linea]

- On Bubbles: "Market bubbles are a feature of human psychology. Your job as an investor is to ensure you are not reliant on them continuing indefinitely." — Source: [Invest Like the Best]

- On Hyperinflation Lessons: "Growing up in Bolivia during hyperinflation taught me that money is an illusion and macro stability is a luxury. It wires you to look for fundamental value, not nominal growth." — Source: [People by WTF]

- On Market Corrections: "A correction is simply the market returning to gravity. The businesses with real unit economics survive; the ones funded solely by cheap capital disappear." — Source: [Masters in Business]

- On Playing Offense in a Crisis: "If you have preserved your capital and maintained discipline during the boom, a crisis is when you shift to aggressive offense." — Source: [20VC]

- On the Danger of Leverage: "Excessive debt is what kills companies during a cyclical downturn. Growth should be funded by equity and operating cash flow, not structural leverage." — Source: [General Atlantic Perspectives]

- On Managing Fear: "During a crisis, fear spreads faster than fundamentals deteriorate. If you can stay analytical when everyone else is emotional, you have an edge." — Source: [Invest Like the Best]

- On Economic Turbulence: "Turbulence shakes out the tourists. The founders who are building for the right reasons are the ones left standing when the easy money leaves." — Source: [Fintech Leaders]

Part 6: Emerging Markets and Global Growth

- On the Global South: "The next phase of massive consumer technology growth will happen across Latin America, India, and Southeast Asia, rather than entirely in Silicon Valley." — Source: [Masters in Business]

- On the Importance of Role Models: "In emerging markets, one massive success story alters the psychology of an entire generation. Success proves that building a global giant from your home country is actually possible." — Source: [People by WTF]

- On Operating in Latin America: "Latin America requires a specific operational resilience. You cannot rely on perfect infrastructure, so the business model itself must be highly adaptable." — Source: [General Atlantic Perspectives]

- On Missing Nubank: "Missing the early opportunity to invest in Nubank taught me a painful lesson about underestimating the size of the total addressable market in emerging economies." — Source: [20VC]

- On Cross-Border Scaling: "Helping companies scale internationally is the highest form of value creation a growth equity firm can provide today." — Source: [Masters in Business]

- On Local Nuance: "You cannot copy a US business model directly into India or Brazil. The underlying consumer behavior and regulatory frameworks require deep, local adaptation." — Source: [People by WTF]

- On Emerging Market Volatility: "Volatility in emerging markets is a constant. You invest in teams that know how to use the volatility against their competitors." — Source: [Masters in Business]

- On Leapfrogging Technologies: "Emerging markets frequently bypass older phases of technology; they often leapfrog entirely, moving straight to mobile-first and AI-native solutions." — Source: [General Atlantic Perspectives]

- On Talent in the Developing World: "The distribution of ambition and intellect is global, but the distribution of capital has historically been local. Bridging that gap is the core mandate of global growth equity." — Source: [Invest Like the Best]

Part 7: Operational Reality versus Spreadsheets

- On the Operator Advantage: "My time building Submarino gave me an allergy to purely theoretical business plans. I know what happens when the warehouse system crashes on Black Friday." — Source: [Masters in Business]

- On the Limits of Financial Models: "A financial model is a translation of your assumptions. If your assumptions about human behavior are wrong, the precision of your model is useless." — Source: [Fintech Leaders]

- On Execution: "Ideas are entirely commoditized. The premium in the market is paid exclusively for the relentless, compounding execution of those ideas." — Source: [20VC]

- On Scaling Culture: "Culture is what people do when the CEO leaves the room. As a company scales from 100 to 1,000 employees, preserving that culture is the hardest operational challenge." — Source: [Invest Like the Best]

- On Firing Fast: "One of the most common operational mistakes founders make is keeping the wrong executives for too long out of a misplaced sense of loyalty. It damages the entire organization." — Source: [Fintech Leaders]

- On Building Scaffolding: "Our job as growth investors is to build the corporate scaffolding like finance, HR, and compliance so the founder can stay focused on the product." — Source: [General Atlantic Perspectives]

- On Customer Reality: "You have to walk the factory floor, or the digital equivalent. You cannot understand a business strictly from board decks." — Source: [Masters in Business]

- On Managing Growth: "Growth breaks things. If nothing is breaking, you probably aren't growing fast enough, but if everything is breaking, you are out of control. It is a delicate equilibrium." — Source: [20VC]

- On Focus: "Strategy is fundamentally about resource allocation. It is the art of concentrating overwhelming force on your highest-conviction opportunity." — Source: [Invest Like the Best]

Part 8: Mentorship, Career, and Regret Minimization

- On the Regret Minimization Framework: "When facing a massive career decision, I project myself to age 80 and ask which choice will result in the least amount of regret. It clarifies everything immediately." — Source: [Fintech Leaders]

- On Taking Risks: "We systematically overestimate the risk of trying something new and vastly underestimate the risk of staying exactly where we are." — Source: [Fintech Leaders]

- On Mentoring Founders: "Mentorship is about asking the exact right question that forces the founder to see their own blind spots, rather than giving them the answers directly." — Source: [Invest Like the Best]

- On Continual Learning: "The moment you think you have the market completely figured out, you become vulnerable. Intellectual humility is a survival requirement in investing." — Source: [Masters in Business]

- On Building Trust: "Trust in business is built through consistent behavior during difficult times, not through shared celebrations when times are easy." — Source: [20VC]

- On Career Transitions: "Moving from an operator to an investor requires a complete rewiring of your ego. As an operator, you are the star; as an investor, you are the coach." — Source: [Fintech Leaders]

- On Personal Growth: "You have to continually put yourself in rooms where you are no longer the smartest person. If you are comfortable, you are stagnating." — Source: [People by WTF]

- On Legacy: "Ultimately, the companies we help build will outlast us. Our job is to ensure they are built on foundations that actually deserve to endure." — Source: [General Atlantic Perspectives]

- On Navigating Chaos: "Chaos is a ladder for the prepared mind. Learning to be comfortable operating in chaotic environments is the ultimate career advantage." — Source: [People by WTF]

- On the Value of Time: "Capital is a commodity, but time is strictly finite. The most important framework you can develop is how you filter who and what gets your time." — Source: [Fintech Leaders]