Lessons from Mason Morfit

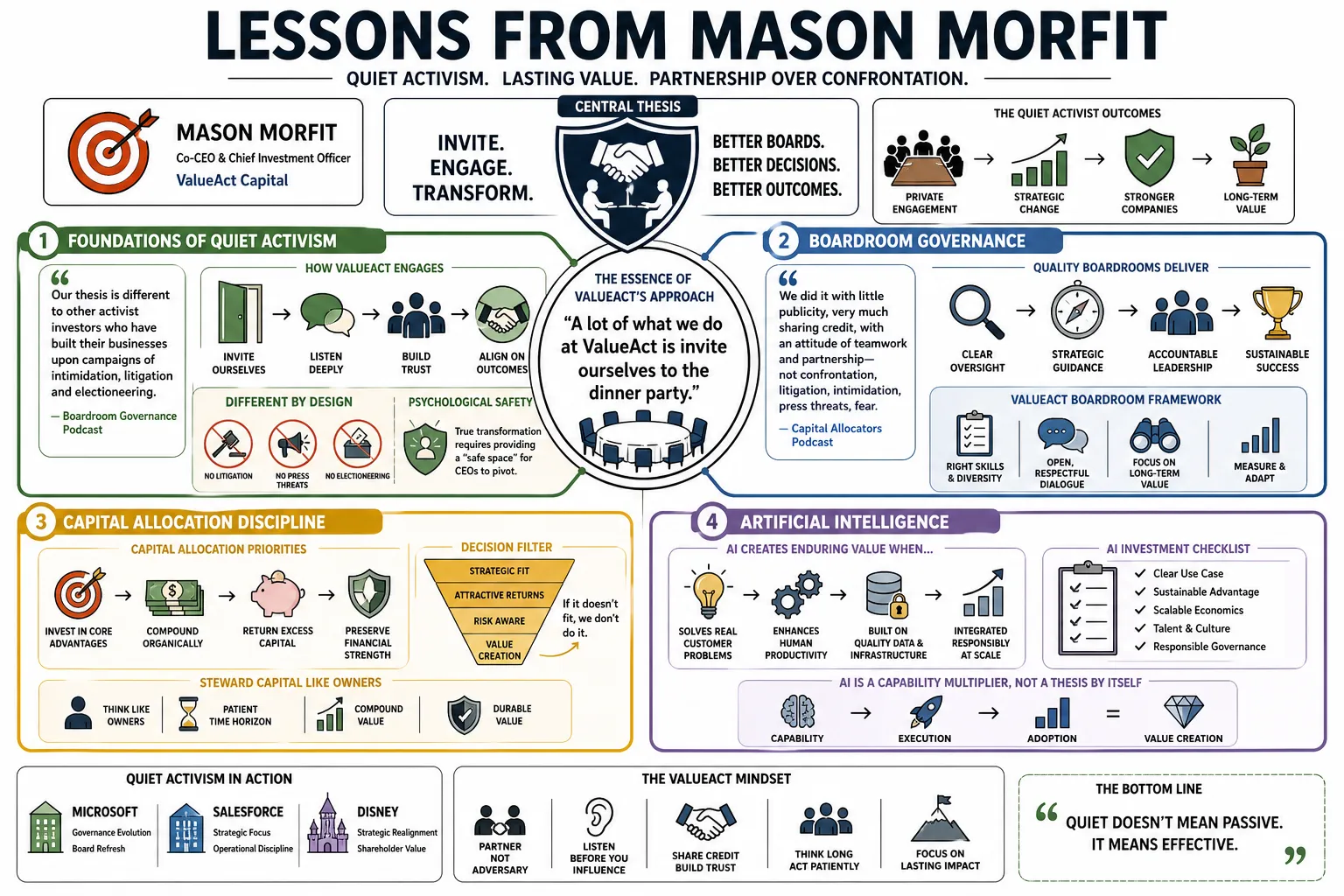

At ValueAct Capital, Co-CEO and Chief Investment Officer Mason Morfit practices "quiet activism," choosing to work privately with corporate boards instead of staging public proxy fights. He has used this long-term approach to drive changes at Microsoft, Salesforce, and Disney. This profile breaks down his specific frameworks for boardroom governance, capital allocation, and artificial intelligence.

Part 1: The Foundations of Quiet Activism

- On the essence of ValueAct's approach: "A lot of what we do at ValueAct is invite ourselves to the dinner party." — Source: Boardroom Governance Podcast

- On differentiating from traditional activists: "Our thesis is different to other activist investors who have built their businesses upon campaigns of intimidation, litigation and electioneering." — Source: Boardroom Governance Podcast

- On the goal of engagement: "We did it with little publicity, very much sharing credit, with an attitude of teamwork and partnership—not confrontation, litigation, intimidation, press threats, fear." — Source: Capital Allocators Podcast

- On providing psychological safety: True transformation requires providing a "safe space" for CEOs to pivot without the pressure of public berating. — Source: Master Investor Podcast

- On transformational vs. transactional activism: The focus must remain on working deeply with a company over years to improve strategy, rather than seeking short-term gains through financial engineering. — Source: Boardroom Governance Podcast

- On building long-term partnerships: The firm aims to be the "shareholder of choice for great companies navigating change." — Source: Boardroom Governance Podcast

- On the limits of public confrontation: Attacking management publicly only serves to make executives defensive and less open to structural change. — Source: Master Investor Podcast

- On early firm history: Reflecting on his start in 2000, he joked, "The firm had no assets under management, so it was a good fit." — Source: Institutional Investor

- On learning through trial and error: The firm's model was not fully formed on day one; it evolved through early engagements and learning from less-successful initial interventions. — Source: Market Folly Lectures

Part 2: Boardroom Dynamics and Governance

- On peripheral vision: "We can bring peripheral vision to the boardroom." — Source: Boardroom Governance Podcast

- On the information gap of independent directors: Boards often lack the time and granular, outside-in information necessary to make the best strategic decisions, relying too heavily on internal hierarchies. — Source: Boardroom Governance Podcast

- On synthesizing data for the board: An engaged shareholder can bridge the gap by synthesizing deep industry research, customer feedback, and supplier perspectives. — Source: Boardroom Governance Podcast

- On engaged ownership: Having a large, financially sophisticated owner at the table clarifies capital allocation debates and focuses the board on long-term value. — Source: Master Investor Podcast

- On the burden of independent directors: Effective change requires empathy for the difficulties and time constraints that independent directors face in their roles. — Source: Boardroom Governance Podcast

- On thinking like an investor: "Thinking like an investor with an investment thesis is a very crystallizing thought exercise. It will lead you to have a point of view about what the strategy should be." — Source: Boardroom Governance Podcast

- On the nature of board refreshment: Bringing in an outsider isn't an indictment of the current board; it is an injection of a specialized, analytical toolkit. — Source: Boardroom Governance Podcast

- On avoiding the echo chamber: The boardroom must actively resist becoming an echo chamber by seeking out unvarnished feedback from customers and the broader market. — Source: Capital Allocators Podcast

- On aligning board incentives: Directors must have real skin in the game to truly align their decision-making timeline with that of long-term shareholders. — Source: Stanford Closer Look Series

- On building consensus: Boardroom influence is not about having the loudest voice, but about consistently bringing the highest quality data to the table. — Source: Capital Allocators Podcast

Part 3: The CEO Scorecard and Leadership Transitions

- On the reality of CEO succession: "Succession processes are rarely smooth... Many are done when the business is struggling, the management team dysfunctional, or the company faces a significant external crisis." — Source: Stanford Closer Look Series

- On the emotion of leadership changes: Succession is inherently stressful, emotional, and taxing on personal relationships within the boardroom. — Source: Stanford Closer Look Series

- On avoiding vague criteria: Boards often make the mistake of selecting CEOs based on vague managerial qualities and adjectives rather than specific performance objectives. — Source: Stanford Closer Look Series

- On the outcomes-based scorecard: The selection process should match candidates' demonstrated skills against the specific, identified "value drivers" of the business. — Source: Stanford Closer Look Series

- On treating hiring like investing: The CEO selection process should resemble an investment decision, where skills are rigorously tested through data and evidence of past performance. — Source: Stanford Closer Look Series

- On defining success metrics: The scorecard must include both financial and non-financial Key Performance Indicators (KPIs) that map directly to forward-looking strategic goals. — Source: Stanford Closer Look Series

- On matching the CEO to the moment: A successful transformation requires a leader whose specific technical, operational, or cultural skills match the precise phase of the company's lifecycle. — Source: Stanford Closer Look Series

- On the failure rate of successions: Research indicates that a significant majority—around 61% in observed activist engagements—of CEO successions are disorderly. — Source: Stanford Closer Look Series

- On reducing bias in selection: An empirical, scorecard-driven approach helps remove the subconscious biases and political maneuvering that often plague succession committees. — Source: Stanford Closer Look Series

- On post-succession alignment: Once the CEO is selected, the scorecard serves as the foundational document for ongoing board-level evaluation and alignment. — Source: Stanford Closer Look Series

Part 4: The Disease of Abundance and Corporate Focus

- On the halo effect of success: When a company generates high returns on capital, it experiences a halo effect in markets that can mask underlying operational bloat. — Source: Master Investor Podcast

- On the definition of the disease: The "disease of abundance" occurs when cash-rich companies lose focus, diversifying into peripheral activities that do not benefit the core business. — Source: Master Investor Podcast

- On the erosion of standards: Abundance can lead companies to become lax with cost structures and allow strict performance standards to slip over time. — Source: Capital Allocators Podcast

- On the loss of corporate identity: The ultimate symptom of this disease is that the company effectively loses its distinct corporate culture and strategic focus. — Source: Master Investor Podcast

- On the cure for bloat: ValueAct aims to cure this by partnering with management to refocus on core strengths and rigorously optimize capital allocation. — Source: Master Investor Podcast

- On analyzing content spending: During the tech boom years, operating expenses and content funding at platforms like Spotify exploded, requiring a reassessment of what was truly driving returns. — Source: Financial Times

- On distinguishing durable value: Companies must ruthlessly differentiate between what was built to last and what was built for the bubble. — Source: Financial Times

- On restoring operational discipline: Activism in the modern era often involves helping high-growth technology companies implement the operational discipline of mature enterprises. — Source: Capital Allocators Podcast

- On capital reallocation: The hard work of the boardroom is shifting resources away from legacy cash-drains toward the genuine engines of future compounding. — Source: Capital Allocators Podcast

Part 5: Artificial Intelligence and The Messy Middle

- On the core investment theme of the era: "Everything digitizes, everything organizes, everything automates." — Source: Master Investor Podcast

- On the true AI bottleneck: While AI models are transformative, the real challenge is not the algorithms, but the foundational work of preparing the enterprise for them. — Source: Master Investor Podcast

- On the "messy middle": The most critical, yet overlooked, step in AI implementation is the messy middle—the complex process of organizing data and securing digital rights. — Source: Master Investor Podcast

- On the advantage of incumbents: Despite the fear of disruption, established incumbents possess the proprietary data necessary to win the AI race if they can organize it effectively. — Source: Master Investor Podcast

- On the prerequisite for automation: Before an enterprise can effectively automate processes with AI, it must first successfully digitize and meticulously organize its internal knowledge graph. — Source: Master Investor Podcast

- On infrastructure over hype: Investors should focus on the companies building the data architecture of the AI revolution, rather than just the consumer-facing applications. — Source: Master Investor Podcast

- On the complexity of digital rights: The Spotify example proves that the hardest part of tech disruption is building the global infrastructure of rights, standards, and audits that allows automation to flourish. — Source: Master Investor Podcast

- On the fear of new technology: New technology is inherently terrifying to established businesses, but those who embrace the messy work of data integration will emerge stronger. — Source: Master Investor Podcast

- On continuous compounding: Once the messy middle is resolved, AI allows companies to achieve compounding returns on their organized data, creating a massive competitive moat. — Source: Master Investor Podcast

Part 6: Case Studies in Transformation

- On the Microsoft inflection point (2013): "Microsoft is a world-class company with tremendous long-term potential. At this critical inflection point... I look forward to actively working together with the board and Microsoft's management team to continue to create value." — Source: Microsoft Press Release

- On the Microsoft pivot: The Microsoft engagement is the textbook example of an engaged shareholder helping a CEO reallocate capital away from struggling hardware toward high-growth cloud infrastructure. — Source: Market Folly Lectures

- On facing difficult facts: The success of the Microsoft turnaround was rooted in the board and management's willingness to accept unvarnished feedback and face the difficult reality of their mobile position. — Source: Market Folly Lectures

- On the Disney partnership: "Disney is the world's leading entertainment company. It has the best intellectual property, sports brand and parks & experiences assets in the industry." — Source: The Walt Disney Company

- On Disney's digital transition: "As legacy technologies transition to digital platforms, we believe Disney can lead the media industry forward." — Source: The Walt Disney Company

- On joining the Salesforce board: The investment in Salesforce was an extension of the quiet activism playbook, providing a supportive environment for the company to focus on profitability and AI integration. — Source: Salesforce Investor Relations

- On the New York Times turnaround: The engagement with the New York Times demonstrated the value of pushing legacy media to embrace cost discipline and aggressively migrate subscribers to digital bundles. — Source: Financial Times

- On the 21st Century Fox legacy: Fox serves as a prime historical case study for how ValueAct helps bridge legacy media assets through periods of profound industry disruption. — Source: Boardroom Governance Podcast

- On Spotify's economic model: Spotify succeeded because it combined exceptional engineering with the organizational tenacity required to build an entirely new economic model for the music industry. — Source: Financial Times

- On the Valeant experience: Even in complex, highly scrutinized turnarounds, the role of the activist is to remain focused on governance, capital structure, and long-term recovery. — Source: Bausch Health Communications

Part 7: Lessons from the Japanese Market

- On the potential of Japan: The Japanese market represents an area of unmatched potential for governance-driven, long-term value creation. — Source: Capital Allocators Podcast

- On adapting the playbook: Applying activism in Japan requires a deep respect for local cultural nuances and a strictly collaborative, behind-the-scenes approach. — Source: Capital Allocators Podcast

- On the Olympus engagement: The successful partnership with Olympus proved that foreign investors can add significant value by bringing global trends to the attention of Japanese management without micromanaging operations. — Source: KED Global

- On the Seven & i strategy: Engagements with conglomerates like Seven & i focus on highlighting the hidden value of core assets and advocating for structural streamlining. — Source: Investing.com

- On the JSR privatization: ValueAct's involvement in JSR Corporation illustrates how quiet board-level engagement can facilitate major strategic outcomes, including taking a company private to accelerate restructuring. — Source: Investing.com

- On investing in Nintendo: Building a position in a beloved institution like Nintendo requires patience and a recognition of the company's unique creative culture alongside its capital allocation potential. — Source: Institutional Investor

- On cultural sensitivity in governance: Western activists cannot simply export aggressive tactics to Japan; success relies on building consensus and demonstrating genuine respect for corporate heritage. — Source: Capital Allocators Podcast

- On unlocking trapped capital: The primary opportunity in Japan lies in helping cash-rich, overly diversified companies realize that returning capital and focusing on core competencies serves all stakeholders. — Source: Capital Allocators Podcast

- On patience as a strategy: Transforming Japanese corporate governance is a multi-decade process that rewards investors willing to commit to long investment horizons. — Source: Capital Allocators Podcast

Part 8: Multidisciplinary Thinking and Personal Philosophy

- On sociological awareness: "I played on a Little League baseball team with all Japanese kids and a Japanese coach who didn't speak English. I think this background gave me a sociological awareness... a feeling of outsider looking in, observing." — Source: Capital Allocators Podcast

- On group dynamics: A multicultural upbringing fosters a lasting sensitivity to group dynamics, which is an invaluable skill when navigating complex boardroom politics. — Source: Capital Allocators Podcast

- On the "learn-it-all" mindset: Success requires moving away from being a know-it-all to embracing a learn-it-all approach, maintaining the courage to constantly revise your worldview. — Source: Sidwell Friends Podcast

- On the value of a liberal arts foundation: A background in political economy and the liberal arts provides the necessary context for understanding the human psychology and sociology behind corporate decisions. — Source: Boardroom Governance Podcast

- On the three pillars of problem-solving: Effective strategy blends the optimization of engineering, the governance rules of law, and the contextual understanding of the liberal arts. — Source: Boardroom Governance Podcast

- On the role of early education: Early environments that foster confidence and an openness to continuous learning are critical in developing the resilience needed for a career in investing. — Source: Sidwell Friends Podcast

- On good intentions: Approaching high-stakes corporate interventions with genuine good intentions and transparency is the only way to build lasting trust with skeptical management teams. — Source: Sidwell Friends Podcast

- On understanding psychology: Effective change in any organization requires deep empathy for the individual psychological burdens carried by executives and founders. — Source: Master Investor Podcast

- On the ultimate goal of investing: The truest measure of success is not just financial return, but leaving a company structurally sounder, culturally healthier, and better positioned for the next decade. — Source: Master Investor Podcast