Lessons from Matt Whineray

Matt Whineray led the New Zealand Superannuation Fund from 2014 to 2023, first as CIO and then as CEO. He systematically bought assets during market panics through a "strategic tilting" program and argued early on that climate change was a hard financial variable, not a moral preference. This profile outlines his frameworks for managing sovereign wealth, building long-horizon portfolios, and matching an organization's structure to its capital goals.

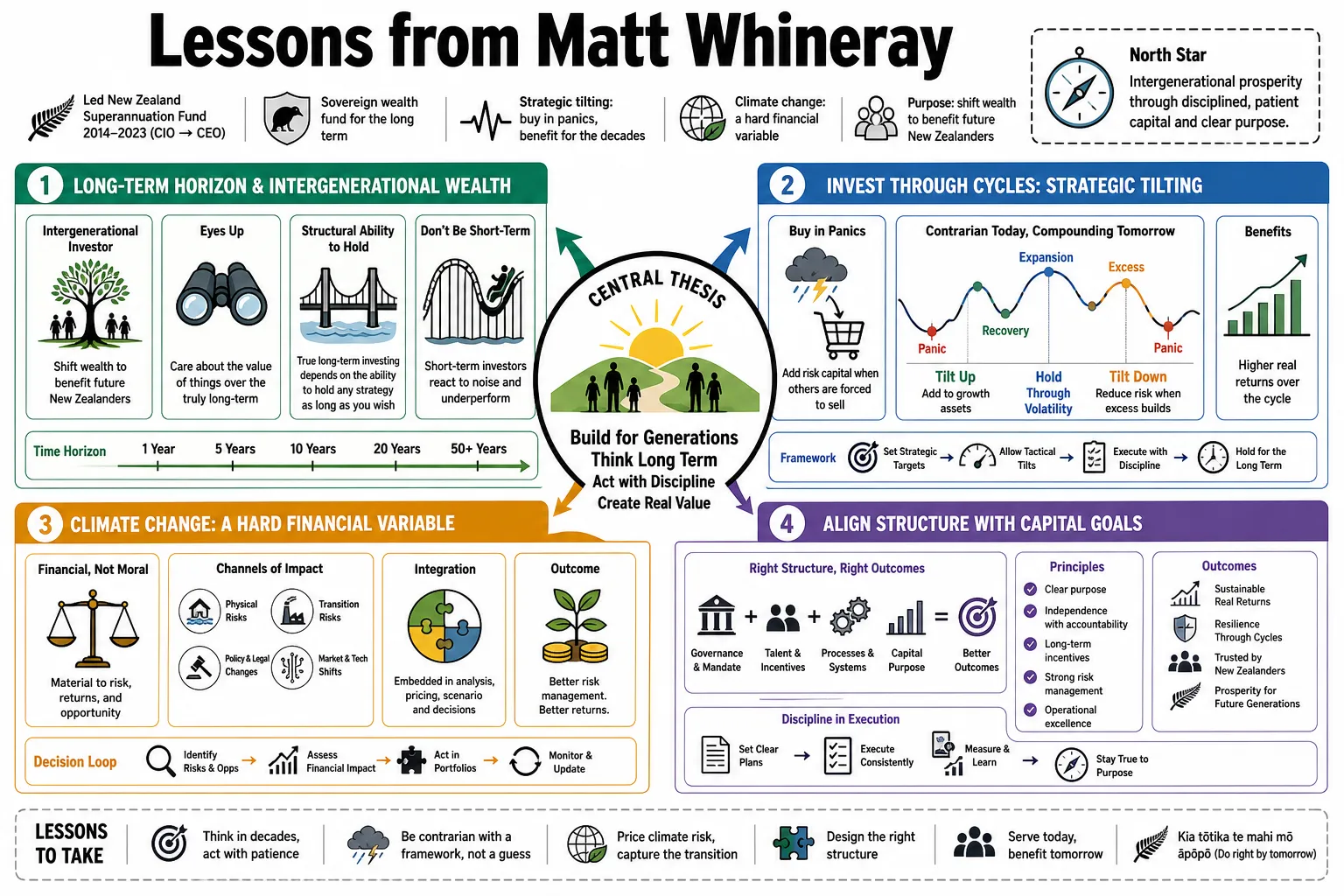

Part 1: Long-Term Horizon and Intergenerational Wealth

- On intergenerational investing: "We are a truly intergenerational investor, where we're shifting this wealth to benefit future New Zealanders." — Source: FCLTGlobal

- On defining the horizon: "It means we have to keep our eyes up. We have to care about the value of things over the truly long-term." — Source: FCLTGlobal

- On true long-term investing: "True long-term investing depends less on the time horizon over which assets are held, and more on the structural ability to hold any strategy for as long as you wish." — Source: NZ Super Fund

- On short-term behaviors: "Short-term investors base decisions solely on expected returns over a year or two and react disproportionately to small pieces of news." — Source: NZ Super Fund

- On peer pressure: "Many short-term decisions are primarily motivated by the desire to avoid being a negative outlier compared to peer funds rather than fundamental value." — Source: NZ Super Fund

- On structural endowments: In FCLTGlobal's Going Long episode, Whineray describes the New Zealand Super Fund as a truly intergenerational investor; the page notes projections for the Fund to peak in size in 2070 and says that horizon lets it target uniquely long-term themes. — Reference: FCLTGlobal Going Long episode on the Fund as an intergenerational investor with a 2070 horizon

- On aligning horizons: "You have to ensure your internal structure, from remuneration to board reporting, matches the actual time horizon of the capital you are managing." — Source: Top1000funds

- On market pro-cyclicality: "When capital is focused only on the next quarter, it exacerbates market pro-cyclicality and leaves structural alpha on the table for those willing to wait." — Source: NZ Super Fund

- On patience: "Managing an intergenerational fund requires the discipline to stand by a thesis even when it remains underwater for significant periods." — Source: i3 Invest

- On stakeholder communication: "Regularly engaging with stakeholders is necessary to ensure they understand that a long-term focus will inevitably involve short-term volatility." — Source: FCLTGlobal

Part 2: Sustainable Finance and ESG Integration

- On the financial nature of ESG: "It needs to be from the investment perspective, because ultimately everything is financial. In the long term, those externalities all come home to roost." — Source: NZ Super Fund

- On integration versus exclusion: "We championed incorporating ESG factors directly into the overarching investment screening processes rather than allocating a small wedge of a portfolio to impact investments." — Source: NZ Super Fund

- On materiality: "Environmental, social, and governance factors are fundamentally material to long-term investment performance; they are not peripheral concerns." — Source: NZ Super Fund

- On risk management: "Good management of environmental risks, employee relations, and governance is a required tool for risk management and identifying new opportunities." — Source: Sustainable Finance

- On the evolution of responsible investing: "We oversaw a shift in the fund's strategy from a traditional responsible investment approach to one based on the broader principles of sustainable finance." — Source: NZ Super Fund

- On systemic issues: "For an investor of our size and horizon, systemic risks eventually become portfolio risks. You cannot diversify away from a failing system." — Source: John Treadgold Podcast

- On corporate engagement: "We use active ownership through voting and direct engagement to influence how companies manage sustainability risks rather than immediately divesting." — Source: NZ Super Fund

- On natural capital: "Wealth and well-being, including the preservation of natural capital, are deeply interconnected and essential for sustainable financial returns." — Source: John Treadgold Podcast

- On the politicization of ESG: "Ignoring ESG factors due to political weaponization is not a viable strategy for long-term investors; it is simply sensible risk management." — Source: Good Returns

- On best practices: "Sound ESG characteristics are an essential requirement of best-practice portfolio management, synonymous with good business." — Source: NZ Super Fund

Part 3: Climate Change as a Financial Reality

- On climate change and investment decisions: "When we created our climate change strategy we may not have known what the destination is or which pathway we're on, but I knew enough to know that bit is really, really one way." — Source: Good Returns

- On acting amidst uncertainty: "That gave us enough confidence to say in the context of all of this uncertainty, this is the right thing to do from a portfolio perspective." — Source: Good Returns

- On the role of investors: "The financial services sector's biggest mistake would be to think it is merely a bystander to the impacts of a changing climate." — Source: Good Returns

- On market participation: "People say to me 'oh, I'm stuck in traffic'. You're not stuck in traffic. You are traffic. You are traffic. That's what we are." — Source: Good Returns

- On ignoring climate risks: "Failing to account for these risks is akin to having one's head in the sand; integrating these considerations is a sensible financial decision." — Source: National Business Review

- On market mispricing: "Financial markets have historically under-priced climate-related risks, which means a long-term investor must actively integrate these into decision-making." — Source: NZ Super Fund

- On the low-carbon transition: "Reducing exposure to carbon-intensive assets functions as a risk-management mechanism and a way to capture returns during the global transition." — Source: Top1000funds

- On multi-faceted strategies: "Our approach to climate change combines index selection, deep analysis, active engagement with companies, and direct investment in the transition." — Source: NZ Super Fund

- On stranded assets: "As the transition accelerates, the risk of holding stranded assets increases, requiring forward-looking adjustments to capital allocation." — Source: AI-CIO

- On climate reporting: "Transparent climate reporting is essential because it allows the market to accurately price risk and direct capital to more resilient businesses." — Source: Infrastructure Investor

Part 4: Strategic Tilting and Volatility

- On dynamic asset allocation: "The idea was to take advantage of our belief that we can have a more constant relative risk aversion than the market." — Source: i3 Invest

- On mean reversion: "If we have a long-run view of the equilibrium value of a particular asset class, then as it gets depressed, we can add exposure or as it gets excited, we can reduce exposure." — Source: i3 Invest

- On systematic execution: "You must execute tilting in a systematic way to remove the behavioral biases that often plague discretionary market timing." — Source: i3 Invest

- On holding the line: "It was interesting because we had said to the board: 'Look, we may be out of the money for a long period of time and we will all have to hold hands and make sure that works.'" — Source: i3 Invest

- On early success and expectations: "And then what happened was we put some positions on and the market immediately went off and the board said: 'Oh, that was easy. Why don't you do some more?'" — Source: i3 Invest

- On surviving drawdowns: "Strategic tilting requires patience, as positions can remain underwater for significant periods before the fundamental basis reasserts itself." — Source: i3 Invest

- On market tension: "During periods of market tension, leaders must step back from short-term P&L and re-evaluate whether the belief in long-run value still holds true." — Source: i3 Invest

- On liquidity provision: "In times of severe market stress, a sovereign fund with no near-term liabilities acts as a liquidity provider, buying when others are forced to sell." — Source: Capital Allocators

- On counter-cyclical investing: "You have to be prepared to look wrong for a long time to eventually be right; that is the price of counter-cyclical investing." — Source: Top1000funds

Part 5: Active Management and Portfolio Construction

- On active returns: "It might sound counter-intuitive to say we had a strong year with the drop in value of the fund. However, our active investment strategies have performed extremely well." — Source: Interest.co.nz

- On team skill: "Strong relative performance in a down market is a reflection of the excellent work and skill of the team over many years." — Source: Interest.co.nz

- On the total fund approach: "Evaluating the portfolio as a single integrated entity over siloed asset classes yields a more accurate assessment of underlying risks and correlations." — Source: Fiftyfaces Podcast

- On competitive advantage: "We must constantly ask ourselves what our structural endowments are and only pursue active management where we have a demonstrable edge." — Source: Capital Allocators

- On internal versus external management: "The decision to manage money internally versus externally should be driven by where we can access the highest quality execution net of all costs and complexities." — Source: Capital Allocators

- On reference portfolios: "A passive reference portfolio provides the critical benchmark for the board to assess whether the active risks taken by management are actually delivering value." — Source: Top1000funds

- On scaling capabilities: "As the fund grows, the types of investments that move the dial change, requiring continuous evolution of our internal capabilities and direct investment models." — Source: Top1000funds

- On illiquidity premiums: "Locking up capital in illiquid assets is only justified if you are being adequately compensated for the loss of optionality compared to public markets." — Source: i3 Invest

- On simplicity: "Complexity in portfolio construction should be avoided unless it demonstrably adds value; otherwise, it only introduces hidden risks and higher costs." — Source: NZ Super Fund

Part 6: Governance and Institutional Culture

- On organizational alignment: "The success of any long-term strategy is entirely dependent on the alignment between the board's governance model and the management's execution." — Source: Institute of Directors NZ

- On effective governance culture: "A high-performance culture requires an environment where team members feel safe to challenge assumptions and debate investment theses rigorously." — Source: Institute of Directors NZ

- On board engagement: "Management must proactively educate the board on complex strategies during calm markets so the board can hold the line during volatile ones." — Source: Top1000funds

- On talent retention: "Attracting and retaining top talent in a public institution means offering a clear, purpose-driven culture that compensates for the lack of private-sector economics." — Source: Capital Allocators

- On navigating crises: In NZ Super Fund's 2018 Double Shot interview, Whineray says the Fund's long horizon and operational independence help it survive market storms and avoid being forced to sell when markets are panicking. — Reference: NZ Super Fund Double Shot interview on long horizon, operational independence, and not being forced to sell in panicking markets

- On institutional memory: "Documenting investment beliefs ensures that the core philosophy outlasts any individual CEO or CIO, providing stability through transitions." — Source: Top1000funds

- On sovereign wealth mandates: "We operate with a dual mandate: maximize returns without undue risk, while avoiding prejudice to New Zealand’s reputation as a responsible global citizen." — Source: NZ Super Fund

- On operational autonomy: "The operational independence of the fund from day-to-day political interference is the foundational pillar that allows us to invest effectively." — Source: FCLTGlobal

- On continuous learning: "In finance, if your culture does not support continuous learning and adaptation, your established edges will inevitably be arbitraged away." — Source: Fiftyfaces Podcast

Part 7: Risk Allocation and Measurement

- On defining risk: "For an endowment, risk means more than the daily volatility of returns; it is the mathematical probability of failing to meet the long-term objective of the capital." — Source: Capital Allocators

- On risk budgets: "Allocating a specific risk budget to different strategies ensures that no single active position can disproportionately damage the total fund." — Source: Capital Allocators

- On downside protection: "Protecting capital during severe market dislocations is often more impactful to long-term compounding than capturing the final percentages of a bull market." — Source: Interest.co.nz

- On measuring success: "You cannot evaluate the success of a 20-year strategy based on a single quarter's performance; the metrics must match the timeframe." — Source: FCLTGlobal

- On uncompensated risk: "The primary job of an allocator is to strip out uncompensated risks from the portfolio and concentrate capital where the edge is clearest." — Source: i3 Invest

- On debt and scaling: "Using debt appropriately allows a fund to scale its low-risk active strategies without compromising the overall liquidity profile." — Source: Top1000funds

- On scenario planning: "We do not predict the future; we use scenario analysis to understand how the portfolio would behave under various extreme but plausible conditions." — Source: NZ Super Fund

- On behavioral traps: "The biggest risk to long-term returns is often the behavioral urge to intervene and adjust the portfolio at exactly the wrong moment." — Source: FCLTGlobal

- On conviction sizing: "If you have a genuine structural advantage, you must size the position meaningfully enough for it to impact the total fund's performance." — Source: Capital Allocators

Part 8: Leadership and Industry Collaboration

- On industry progress: "Advancing the finance sector requires collaboration—we must be willing to share our mistakes and learn from the best practices of our global peers." — Source: Sustainable Finance

- On driving systemic change: "Major institutional investors have a responsibility to use their scale to drive systemic changes in how capital addresses global challenges." — Source: Sustainable Finance

- On professional transitions: "Moving from CIO to CEO requires a shift in focus from pure portfolio construction to managing complex stakeholder networks and broader organizational health." — Source: Top1000funds

- On collaborative frameworks: "Collaborating with other sovereign wealth funds on climate frameworks amplifies our influence and helps standardize expectations for asset managers globally." — Source: SWFI

- On domestic infrastructure: "Partnering on models like the SuperBuild allows us to deploy capital efficiently into domestic infrastructure while maintaining our required return hurdles." — Source: NZ Super Fund

- On leading through crises: "During the global financial crisis and the pandemic, the leadership mandate was to provide stability and ensure the team focused on execution, not the news cycle." — Source: Top1000funds

- On sustainable platforms: "Establishing the Centre for Sustainable Finance was about creating a collaborative platform to rewire the financial system for a more resilient future." — Source: Sustainable Finance

- On transparency: "Being radically transparent about our investment beliefs and processes builds the public trust necessary to operate a sovereign fund effectively." — Source: NZ Super Fund

- On legacy: "The ultimate measure of leadership in this role is leaving the institution stronger, more resilient, and better equipped for the next generation." — Source: Fiftyfaces Podcast