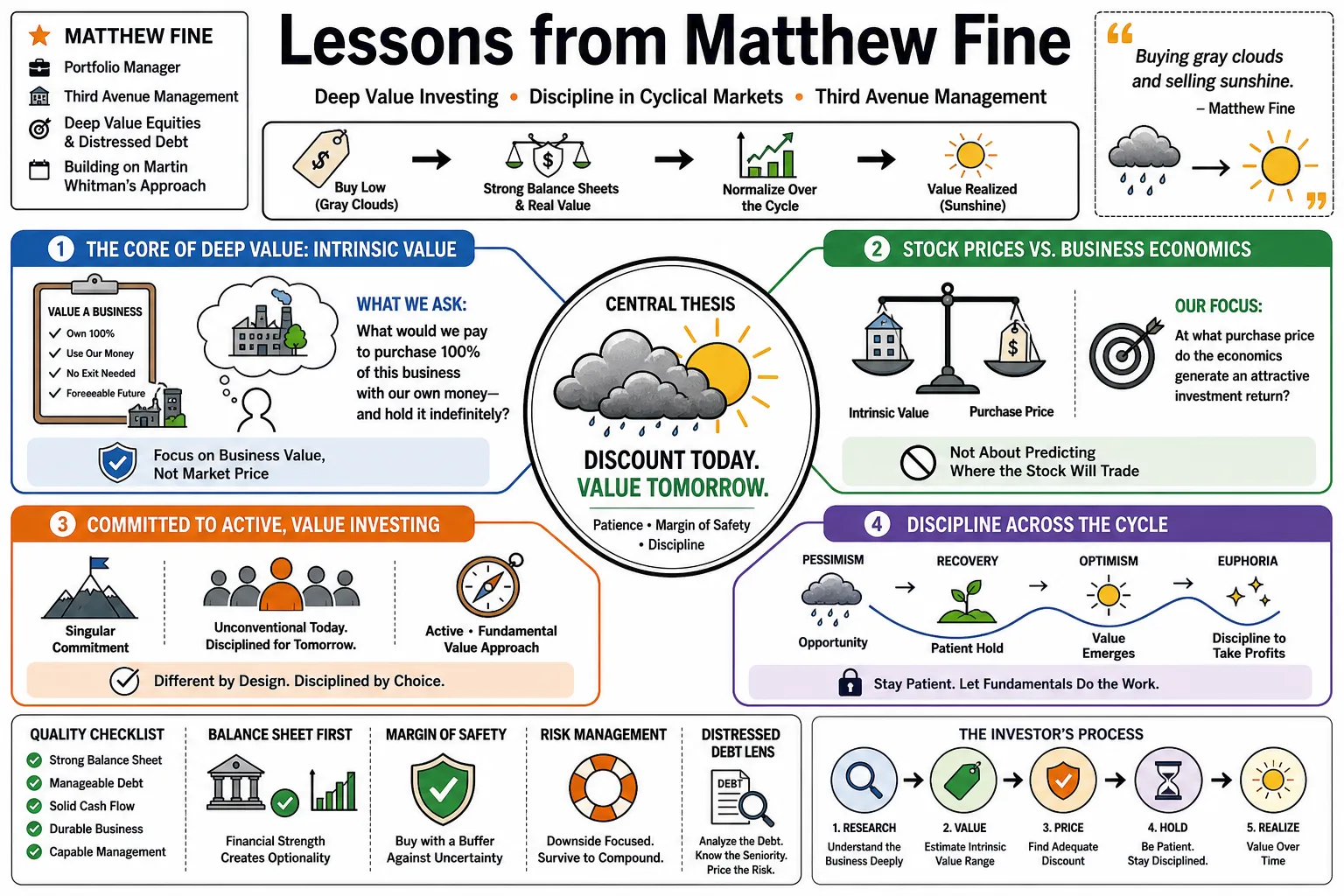

Lessons from Matthew Fine

Matthew Fine is a portfolio manager at Third Avenue Management who specializes in deep value equities and distressed debt. Building on founder Martin Whitman's approach, he targets heavily discounted companies with strong balance sheets, a strategy he describes as "buying gray clouds and selling sunshine." This compilation details his methods for evaluating financial risk and staying disciplined in cyclical markets.

Part 1: The Core of Deep Value

- On intrinsic value: "When we think about the value of a business in a very fundamental way, we think about what we would pay to purchase 100% of the business with our own money and without any type of exit for the foreseeable future." — Source: [Third Avenue Management Media Center]

- On stock prices: "At what purchase price would the actual economics of the business generate an attractive investment return? It has nothing to do with making predictions about where the stock might trade in the future." — Source: [Third Avenue Management Media Center]

- On active management: "Third Avenue Management has remained singularly committed to executing upon its unique form of active, fundamental, value investing. This has become an increasingly unconventional approach in recent years." — Source: [Business Wire]

- On market efficiency: "The market often reacts to news in ways that cause stock prices to diverge materially from long-term fundamentals, which creates the exact environments where deep value investors can profit." — Source: [Value Investing with Legends]

- On staying the course: "We have kept doing what we've always done. And we fought through that, against all odds. Fortunately, it paid off tremendously." — Source: [Business Insider]

- On buying distress: "We prefer to look at businesses that are emerging from difficult periods, because they have often straightened out their balance sheets but their stock is still priced as a bargain." — Source: [Validea]

- On the legacy of Marty Whitman: "The foundation of our approach was built on treating equities not as trading chips, but as fractional ownership in businesses with underlying assets and cash flows." — Source: [Third Avenue Management Media Center]

- On price versus value: "We are constantly evaluating whether the price being offered in the public markets reflects the true liquidation or ongoing economic value of the enterprise." — Source: [Third Avenue Value Fund Letter]

- On ignoring hype: "I was very young during the dot-com bubble... I got a valuable lesson out of it, seeing a huge number of people who invested their savings based on stories and hype from so-called professionals wiped out." — Source: [Third Avenue Management Media Center]

- On defining bargains: "A true bargain exists when the downside is backstopped by hard assets and the upside is free, rather than when a stock is simply down a certain percentage from its highs." — Source: [Third Avenue Value Fund Letter]

Part 2: Balance Sheets and Financial Strength

- On credit mindset: "We approach equity investing with a credit mindset, meaning our first question is always whether the company can survive the worst-case scenario." — Source: [Value Investing with Legends]

- On debt: "Excessive leverage is the enemy of the long-term equity holder because it removes the company's ability to weather inevitable cyclical downturns." — Source: [Third Avenue Value Fund Letter]

- On book value: "Accounting book value is a starting point, but it requires rigorous adjustment to understand the true economic value of the underlying assets." — Source: [Third Avenue Value Fund Letter]

- On financial flexibility: "Companies with strong balance sheets have the luxury of time, allowing them to wait out depressed markets and deploy capital when assets are cheap." — Source: [Value: After Hours Podcast]

- On corporate survival: "The most critical factor in a cyclical industry is making sure you own the businesses that are mathematically guaranteed to make it to the other side of the cycle." — Source: [Value Investing with Legends]

- On off-balance sheet liabilities: "You cannot just read the top-line numbers; evaluating real value means digging into footnotes to find hidden liabilities that might impair the equity." — Source: [Third Avenue Value Fund Letter]

- On asset quality: "Not all assets are created equal. We look for hard, tangible assets that retain their value even if the current operating business is struggling." — Source: [Value: After Hours Podcast]

- On cash generation: "We favor businesses that can generate free cash flow even in a depressed macro environment, as this organic cash builds a margin of safety." — Source: [Third Avenue Value Fund Letter]

- On capital structure: "Understanding where you sit in the capital structure is essential, because equity is a residual claim, and you need to know exactly who stands in line ahead of you." — Source: [Third Avenue Value Fund Letter]

- On distressed debt: "Sometimes the safest way to participate in a recovery is through the debt of a distressed company, where the assets provide adequate coverage." — Source: [Value Investing with Legends]

Part 3: Market Psychology and Contrarianism

- On contrarianism: "We make our living by buying gray clouds and selling sunshine." — Source: [Value Investing with Legends]

- On market panic: "Panic in the broader market is usually the necessary ingredient for creating the types of entry prices we demand." — Source: [Third Avenue Value Fund Letter]

- On consensus: "If everyone agrees with your investment thesis on day one, you probably paid too much for the stock." — Source: [Value: After Hours Podcast]

- On behavioral advantages: "The biggest edge a value investor has isn't an informational advantage, but a behavioral one—the willingness to look foolish in the short term." — Source: [Third Avenue Management Media Center]

- On selling sunshine: "It is just as important to sell when a business is universally loved and priced for perfection as it is to buy when it is hated." — Source: [Third Avenue Value Fund Letter]

- On narrative drift: "Markets are prone to narrative drift, where the story takes over the valuation. We try to completely decouple the story from the math." — Source: [Value Investing with Legends]

- On institutional constraints: "Many institutional investors are constrained by tracking error and short-term performance metrics, which forces them to sell exactly when they should be buying." — Source: [Third Avenue Value Fund Letter]

- On emotional discipline: "You have to cultivate an emotional detachment from the daily quoted prices of your portfolio, focusing entirely on the underlying business performance." — Source: [Value Investing with Legends]

- On market cycles: "Cyclicality is a permanent feature of markets, yet investors repeatedly price peak earnings as if they will last forever." — Source: [Value: After Hours Podcast]

- On finding opportunity: "The best opportunities usually reside in sectors that are actively undergoing structural or cyclical stress, where capital is fleeing rather than entering." — Source: [Third Avenue Value Fund Letter]

Part 4: Distressed Assets and Restructurings

- On bankruptcy: "Companies emerging from bankruptcy often have the cleanest balance sheets in their industries, yet their equities are heavily discounted due to stigma." — Source: [Validea]

- On structural advantages: "Post-restructuring equities can be incredibly attractive because the debt burden that caused the initial distress has been entirely wiped out." — Source: [Third Avenue Value Fund Letter]

- On complex situations: "Complexity is a moat for investors willing to do the work; the harder a restructuring is to analyze, the more likely it is to be mispriced." — Source: [Value Investing with Legends]

- On forced selling: "We look for situations where non-economic actors are forced to sell, such as distressed debt funds liquidating equity they received in a reorganization." — Source: [Third Avenue Value Fund Letter]

- On capital flight: "When a sector is out of favor, the lack of capital availability forces companies into distressed situations, creating generational buying opportunities for those with cash." — Source: [Value: After Hours Podcast]

- On operational turnarounds: "A clean balance sheet buys a company the time it needs to execute an operational turnaround without the ticking clock of debt maturities." — Source: [Third Avenue Value Fund Letter]

- On evaluating distress: "In distressed situations, you must accurately underwrite the liquidation value of the assets to understand your true downside risk." — Source: [Value Investing with Legends]

- On offshore energy: "Sectors like offshore energy went through massive restructurings, leaving the survivors with right-sized balance sheets and significantly reduced competition." — Source: [Third Avenue Management Media Center]

- On legal frameworks: "A thorough understanding of bankruptcy law and creditor rights is essential when investing in distressed situations to protect your position in the capital stack." — Source: [Third Avenue Value Fund Letter]

Part 5: Resource Conversion and Value Realization

- On resource conversion: "We actively seek companies that can engage in resource conversion—mergers, acquisitions, liquidations, or spin-offs—to unlock the underlying asset value." — Source: [Third Avenue Value Fund Letter]

- On catalysts: "While we do not rely solely on catalysts, a management team actively pursuing resource conversion can dramatically accelerate the realization of value." — Source: [Value Investing with Legends]

- On capital allocation: "The most effective way for a discounted company to create shareholder value is through aggressive, opportunistic share repurchases when the stock is cheap." — Source: [Third Avenue Value Fund Letter]

- On special dividends: "Selling non-core assets and returning the proceeds via special dividends is a clear signal that management is aligned with equity holders." — Source: [Third Avenue Management Media Center]

- On M&A: "We prefer management teams that act as intelligent capital allocators, selling assets when private market values vastly exceed public market valuations." — Source: [Value: After Hours Podcast]

- On spin-offs: "Corporate spin-offs frequently create mispriced securities because the spun-off entity is often sold indiscriminately by the parent company's shareholder base." — Source: [Third Avenue Value Fund Letter]

- On private versus public value: "There is often a significant arbitrage opportunity between what a business trades for in the public markets and what a strategic buyer would pay for it in a private transaction." — Source: [Third Avenue Value Fund Letter]

- On liquidation: "If a business cannot earn its cost of capital, the best course of action is often an orderly liquidation to return cash to the owners." — Source: [Value Investing with Legends]

- On shareholder activism: "While we are primarily passive investors, we support actions that force the realization of intrinsic value when a stock trades at a persistent discount." — Source: [Third Avenue Value Fund Letter]

Part 6: Assessing Management and Strategy

- On alignment: "We look for management teams that are heavily incentivized by long-term equity ownership rather than short-term cash bonuses." — Source: [Third Avenue Management Media Center]

- On competence: "A competent management team understands that their primary job is capital allocation, not just operational execution." — Source: [Third Avenue Value Fund Letter]

- On defensive strategy: "In cyclical industries, we prefer managers who operate with a defensive posture, maintaining excess liquidity to survive the lean years." — Source: [Value Investing with Legends]

- On track records: "We study a management's track record of capital allocation during previous industry downturns to see if they acted opportunistically or defensively." — Source: [Third Avenue Value Fund Letter]

- On capital discipline: "A management team's willingness to shrink the capital base rather than chase unprofitable growth is a rare and highly valued trait." — Source: [Value: After Hours Podcast]

- On realistic expectations: "We avoid companies led by executives who constantly promise rosy outlooks; we prefer those who realistically acknowledge industry headwinds." — Source: [Third Avenue Value Fund Letter]

- On insider buying: "Significant open-market purchases by insiders are one of the most reliable indicators that the internal view of value is materially higher than the market price." — Source: [Third Avenue Management Media Center]

- On corporate governance: "Strong corporate governance and a board that holds management accountable for returns on invested capital are non-negotiable for long-term investments." — Source: [Third Avenue Value Fund Letter]

- On operator versus allocator: "The ideal CEO in a mature industry acts more like an investor managing a portfolio of cash flows than a traditional operating manager." — Source: [Value Investing with Legends]

Part 7: Risk Management and Downside Protection

- On margin of safety: "Margin of safety is not just a function of a low valuation multiple; it is derived from the tangibility and quality of the underlying assets." — Source: [Third Avenue Management Media Center]

- On permanent capital loss: "Our primary objective before considering the upside potential is to structure the portfolio to avoid permanent impairments of capital." — Source: [Third Avenue Value Fund Letter]

- On position sizing: "We size positions based on the quality of the balance sheet and the depth of the discount; higher financial risk requires a smaller portfolio weighting." — Source: [Value Investing with Legends]

- On macroeconomic forecasting: "We do not base our investments on macroeconomic forecasts; instead, we buy businesses that can survive a variety of negative macro scenarios." — Source: [Third Avenue Value Fund Letter]

- On valuation risk: "Paying a high multiple for a rapidly growing business introduces severe valuation risk, because any stumble in growth leads to a violent downward rerating." — Source: [Value: After Hours Podcast]

- On illiquidity: "Illiquidity in a security can be an advantage for the patient investor, as it often causes the asset to trade at a deeper discount to its fundamental value." — Source: [Third Avenue Value Fund Letter]

- On downside scenarios: "You must constantly underwrite the worst-case scenario. If the worst case still yields a recovery of your principal, the investment is usually sound." — Source: [Third Avenue Management Media Center]

- On concentration: "A concentrated portfolio of well-understood, deeply discounted, and financially robust companies is often less risky than a highly diversified portfolio of average businesses." — Source: [Third Avenue Value Fund Letter]

- On cyclical bottoms: "Investing at the bottom of a cycle feels inherently risky because the news flow is terrible, but mathematically, the risk is actually at its lowest." — Source: [Value Investing with Legends]

Part 8: The Long-Term Mindset

- On patience: "Value investing requires a structural time horizon advantage. You have to be willing to wait years for a thesis to fully play out." — Source: [Value: After Hours Podcast]

- On compounding: "The most powerful wealth creation occurs when a business can reinvest cash flows at high rates of return over decades, undisturbed by market volatility." — Source: [Third Avenue Value Fund Letter]

- On short-termism: "The financial industry's obsession with quarterly earnings estimates creates persistent opportunities for investors who are looking three to five years out." — Source: [Third Avenue Management Media Center]

- On investment horizons: "When we underwrite a business, we are implicitly asking if we would be comfortable holding it if the stock market closed for the next five years." — Source: [Value Investing with Legends]

- On cyclical endurance: "Endurance is the most underrated quality in investing. The ability to simply survive bad markets is what allows you to thrive in good ones." — Source: [Third Avenue Value Fund Letter]

- On adapting: "The core principles of value investing do not change, but you must constantly adapt your application of them to new industries and market structures." — Source: [Third Avenue Management Media Center]

- On the nature of value: "Value is not a static number; it is a dynamic range that evolves with the business, requiring constant reassessment and fundamental rigor." — Source: [Third Avenue Value Fund Letter]

- On market noise: "Turning off the screens and focusing on reading annual reports and indentures is the best way to block out the noise and focus on reality." — Source: [Value: After Hours Podcast]

- On ultimate success: "Ultimately, success in this business comes down to knowing what you own, knowing why you own it, and having the fortitude to hold it when others are panicking." — Source: [Value Investing with Legends]