Lessons from Matthew McLennan

Matthew McLennan co-heads the Global Value team at First Eagle Investment Management, where he builds portfolios designed to survive severe market downturns. He focuses on protecting purchasing power rather than chasing short-term returns. This profile covers his contrarian approach, the psychology of patience, and his use of scarce assets like gold to stabilize investments.

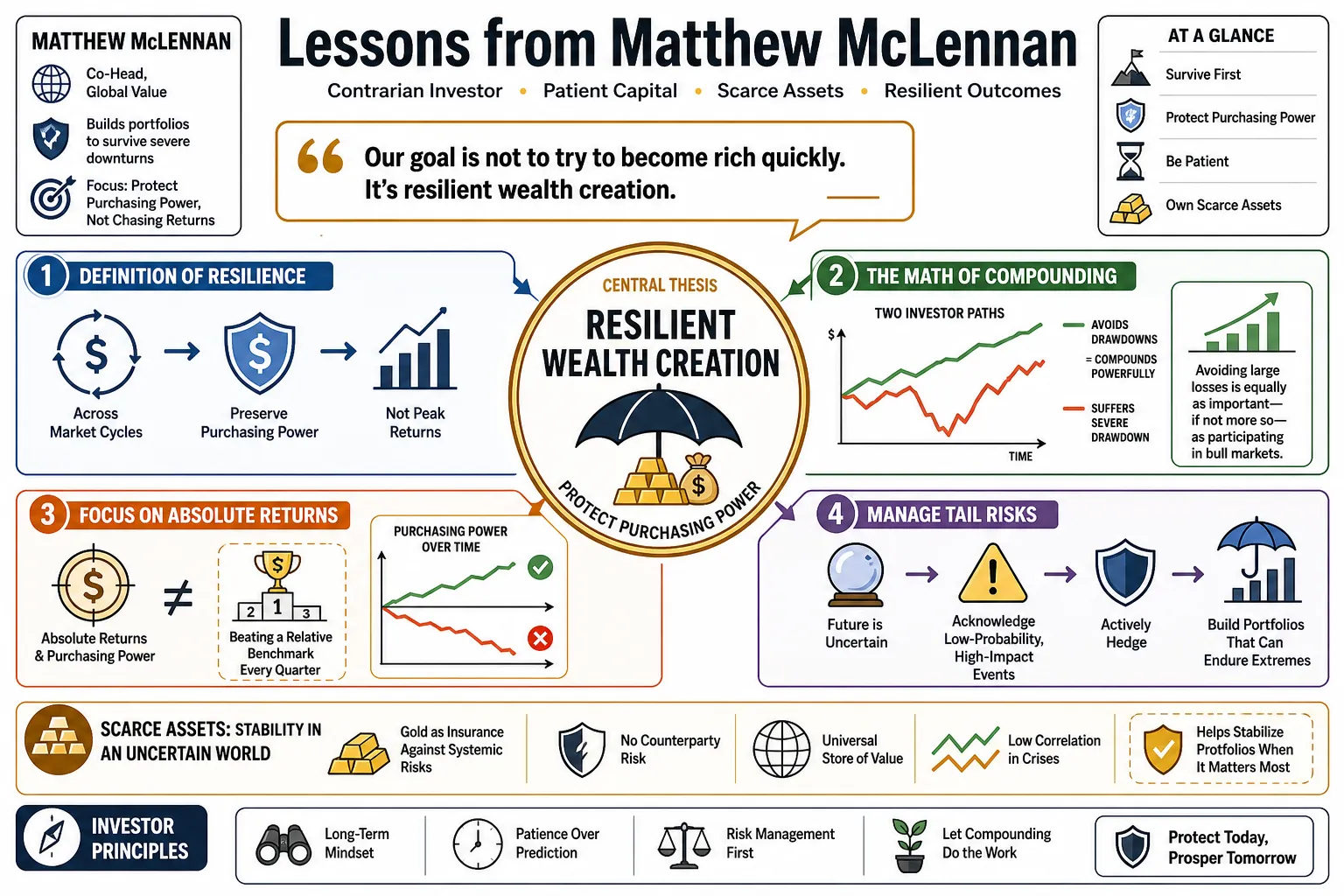

Part 1: Resilient Wealth Creation

- On the primary goal: "Our goal is not to try to become rich quickly. It's resilient wealth creation." — Source: [Richer, Wiser, Happier Podcast]

- On the definition of resilience: Resilient wealth creation means prioritizing the preservation of purchasing power across market cycles rather than chasing peak returns during boom times. — Source: [First Eagle Insights]

- On compounding: The math of compounding dictates that avoiding severe drawdowns is equally as important as participating in bull markets, if not more so. — Source: [WealthTrack]

- On absolute returns: The focus should remain on absolute returns and purchasing power rather than attempting to beat a relative benchmark every single quarter. — Source: [First Eagle Investments]

- On tail risks: Building resilience means explicitly acknowledging that the future is uncertain and actively hedging against extreme events that could permanently impair capital. — Source: [The Investor's Podcast]

- On systemic shocks: Investors must construct portfolios that can survive environments they hope will never actually materialize. — Source: [Richer, Wiser, Happier Podcast]

- On the long-term horizon: True wealth creation is measured in decades, requiring a structure that allows capital to survive structural shifts in the economy. — Source: [First Eagle Insights]

- On purchasing power: The real enemy of the long-term investor is the erosion of purchasing power through inflation and poor capital allocation, rather than merely short-term price volatility. — Source: [WealthTrack]

- On avoiding zeroes: The surest path to wealth destruction is taking on uncompensated risk that exposes a portfolio to a permanent loss of capital. — Source: [The Art of Value Investing]

- On top-down vs. bottom-up: "We often don’t like the state of the world top-down, so we try to craft resilience in the portfolio from the bottom up." — Source: [First Eagle Insights]

Part 2: The Philosophy of Value and Margin of Safety

- On margin of safety: A margin of safety is more than a mathematical discount to intrinsic value; it is a conceptual buffer against our own ignorance about the future. — Source: [Graham & Doddsville]

- On defining value: Value investing is fundamentally about buying businesses for less than they are intrinsically worth, demanding a cushion for error. — Source: [First Eagle Investments]

- On price vs. value: The market frequently misprices assets because it extrapolates recent trends too far into the future, creating opportunities for those focused on structural reality. — Source: [Richer, Wiser, Happier Podcast]

- On style cycles: "Trees don't grow to the sky. No one investing style will always be in favor." — Source: [GuruFocus]

- On intrinsic value: True intrinsic value is rooted in a company's ability to generate free cash flow over the long term, avoiding distractions from its short-term earnings momentum. — Source: [First Eagle Insights]

- On conservative assumptions: When estimating the value of a business, it is safer to assume mean reversion in profit margins rather than indefinite expansion. — Source: [WealthTrack]

- On capital impairment: The margin of safety is what protects an investor when an initially sound thesis proves to be incorrect. — Source: [Graham & Doddsville]

- On valuation discipline: Paying a high multiple for an excellent business can turn a wonderful company into a mediocre investment if growth expectations are not met. — Source: [The Investor's Podcast]

- On market efficiency: The market is mostly efficient over the long term, but emotional overreactions create pockets of gross inefficiency in the short term. — Source: [First Eagle Investments]

Part 3: The Psychology of Patience

- On inactivity: A well-constructed portfolio should often resemble a "portrait of inactivity," as rapid trading usually destroys value. — Source: [The Art of Value Investing]

- On emotional discipline: The primary advantage of a successful investor is not necessarily raw intellect, but the emotional temperament to remain rational when others are panicking. — Source: [Richer, Wiser, Happier Podcast]

- On time arbitrage: In a market obsessed with the next quarter, an investor who is willing to wait three to five years possesses a significant structural advantage. — Source: [First Eagle Insights]

- On decision making: Investors should focus on the quality of their "decisions, not results," as short-term outcomes involve luck while long-term outcomes reflect process. — Source: [The Art of Value Investing]

- On hyperactive markets: The modern financial ecosystem encourages constant action, making patience an increasingly rare and valuable commodity. — Source: [WealthTrack]

- On doing nothing: Often, the most difficult and most rewarding action in investing is simply choosing to do nothing while waiting for the right pitch. — Source: [Graham & Doddsville]

- On delayed gratification: Successful investing requires a willingness to look foolish in the short term to achieve superior results in the long term. — Source: [The Investor's Podcast]

- On gardening: Investing is akin to gardening; you plant seeds, ensure the soil is healthy, and then step back to let nature take its course over time. — Source: [Richer, Wiser, Happier Podcast]

- On avoiding noise: Filtering out daily market noise is essential for maintaining the conviction needed to hold long-term positions. — Source: [First Eagle Investments]

- On suffering: Enduring periods of underperformance is the psychological toll that must be paid to adhere to a disciplined value strategy. — Source: [WealthTrack]

Part 4: Contrarianism and Being Short Social Acceptance

- On social acceptance: Practicing true value investing requires you to be comfortable being "short social acceptance." — Source: [First Eagle Insights]

- On contrarianism: "The key to the success of value investing is that it is basically contrarian investing." — Source: [Archive.org]

- On independence: "At the end of the day, we're paid to see the world through a different prism." — Source: [Studylib]

- On pain: It is often "painful and not socially acceptable to be out of the most revered sectors of the market." — Source: [The Art of Value Investing]

- On consensus thinking: If you own the same assets as everyone else and share the same consensus views, you cannot reasonably expect differentiated returns. — Source: [Graham & Doddsville]

- On finding value: Bargains are rarely found in assets that are universally celebrated; they are usually hidden in sectors facing temporary distress or neglect. — Source: [First Eagle Investments]

- On market panics: When fear dominates the market and liquidity dries up, contrarian investors must be prepared to act as liquidity providers. — Source: [The Investor's Podcast]

- On career risk: Portfolio managers often fail to act as contrarians because buying unpopular assets carries significant career risk if the timing is slightly off. — Source: [Richer, Wiser, Happier Podcast]

- On herd mentality: The instinct to follow the crowd is deeply ingrained in human psychology, which is why structural contrarianism remains an enduring edge. — Source: [WealthTrack]

Part 5: The Strategic Role of Gold and Scarcity

- On the nature of gold: "The paradox of gold is that its utility as a monetary reserve is its uselessness as a commodity... it is a natural resource perpetuity." — Source: [ABC Bullion]

- On scarcity value: "The reason we own gold is it's the embodiment of scarcity value." — Source: [Hearts and Minds Investments]

- On portfolio ballast: Gold serves as a strategic ballast in a portfolio, offering protection when fiat currencies are debased or traditional financial assets suffer a systemic shock. — Source: [First Eagle Insights]

- On outlasting regimes: Gold has proven its ability to preserve purchasing power by outlasting corporate fads, economic cycles, and even sovereign regimes. — Source: [ABC Bullion]

- On non-correlated assets: Holding an asset that does not rely on the performance of the broader economy or the solvency of a counterparty is vital for absolute resilience. — Source: [WealthTrack]

- On monetary expansion: In an era of sustained sovereign debt and central bank balance sheet expansion, gold acts as a hedge against the inevitable debasement of paper money. — Source: [The Investor's Podcast]

- On cash: Holding cash is a defensive posture that provides the optionality to capitalize on future market dislocations, even if it yields nothing in the short term. — Source: [First Eagle Investments]

- On hard assets: When inflation takes hold, investors should seek out hard assets and businesses that require little ongoing capital expenditure to maintain their real value. — Source: [Richer, Wiser, Happier Podcast]

- On shadow currencies: Gold effectively functions as a shadow currency that cannot be printed at will by politicians facing fiscal deficits. — Source: [WealthTrack]

Part 6: Identifying Durable Business Quality

- On business moats: A lasting business possesses a moat built on scarce, intangible assets—such as a dominant brand or network effect—that competitors cannot easily replicate. — Source: [First Eagle Insights]

- On capital allocation: The long-term success of a business relies heavily on management's ability to rationally allocate capital, repurchasing shares when cheap and avoiding overpriced acquisitions. — Source: [Graham & Doddsville]

- On pricing power: The ultimate test of a high-quality franchise is its ability to raise prices to offset inflation without losing market share. — Source: [First Eagle Investments]

- On market share: Companies that dominate small, localized niches often face less competition and enjoy higher returns on capital than those fighting in massive, commoditized global markets. — Source: [The Investor's Podcast]

- On structural advantages: We seek out businesses where the economics are driven by structural supply constraints rather than highly cyclical demand factors. — Source: [Richer, Wiser, Happier Podcast]

- On management alignment: Investing alongside founder-led teams or management with significant insider ownership ensures that their incentives are aligned with long-term shareholders. — Source: [WealthTrack]

- On balance sheet strength: A strong balance sheet provides a company with the staying power to survive economic winters and aggressively invest when weaker competitors retreat. — Source: [First Eagle Insights]

- On capital intensity: Businesses that require massive, continuous capital expenditures simply to stand still are highly vulnerable to inflation and technological disruption. — Source: [Graham & Doddsville]

- On adaptability: The best companies do not rely on a static environment; they possess the cultural adaptability to evolve their business models as the world changes. — Source: [The Investor's Podcast]

Part 7: Navigating Macro Risks and Sovereign Debt

- On structural debt: The massive accumulation of global sovereign debt limits the flexibility of central banks and creates a fragile foundation for future economic growth. — Source: [First Eagle Insights]

- On complacency: Markets have a dangerous tendency to become complacent, pricing in ideal conditions and ignoring the historical reality of deep economic cycles. — Source: [WealthTrack]

- On inflation: Inflation is a stealth tax that slowly confiscates wealth; portfolios must be designed to withstand its corrosive effects over decades. — Source: [The Investor's Podcast]

- On financial repression: Governments heavily burdened by debt are structurally incentivized to maintain negative real interest rates, quietly inflating away their obligations at the expense of savers. — Source: [Richer, Wiser, Happier Podcast]

- On geopolitical risk: Globalization was a deflationary force for decades, but rising geopolitical tensions threaten to reverse this trend, leading to localized supply chains and higher structural costs. — Source: [First Eagle Investments]

- On fiat vulnerabilities: The implicit trust in fiat currency systems is tested when fiscal deficits run persistently high, necessitating the ownership of assets outside the traditional financial system. — Source: [First Eagle Insights]

- On ignoring the macro: While we are bottom-up investors, ignoring massive macroeconomic imbalances like sovereign debt is naive, as these forces eventually shape the micro environment. — Source: [WealthTrack]

- On interest rates: The long era of declining interest rates artificially inflated asset prices across the board; investors must prepare for an environment where this tailwind is removed. — Source: [The Investor's Podcast]

- On sovereign solvency: The assumption that developed nations will always honor their debts in real terms is a historical anomaly that prudent investors should view with skepticism. — Source: [First Eagle Investments]

- On market fragility: The combination of high leverage, passive investing flows, and algorithmic trading has created a market structure prone to sudden, violent dislocations. — Source: [Richer, Wiser, Happier Podcast]

Part 8: The Limits of Forecasting

- On macro forecasting: "We have two classes of forecasters: Those who don't know—and those who don't know they don't know." — Source: [Studylib]

- On predictability: The global economy is a complex, non-linear system, making precise point forecasts fundamentally impossible and dangerously misleading. — Source: [First Eagle Insights]

- On humility: Intellectual humility is a prerequisite for survival; recognizing the limits of your own foresight prevents the hubris that leads to catastrophic bets. — Source: [Richer, Wiser, Happier Podcast]

- On preparedness vs. prediction: Rather than trying to predict exactly when a storm will hit, investors should focus on building a sturdy ship capable of surviving any weather. — Source: [First Eagle Investments]

- On probabilistic thinking: Investing is not about absolute certainty; it is about weighing probabilities and ensuring that the consequences of being wrong are manageable. — Source: [WealthTrack]

- On false precision: Complex financial models often provide a false sense of precision, masking the underlying uncertainty of the assumptions built into them. — Source: [The Investor's Podcast]

- On expert consensus: The consensus view of economic experts is frequently wrong at major turning points because they extrapolate current conditions in a linear fashion. — Source: [Graham & Doddsville]

- On unknown unknowns: True risk does not stem from the events we can anticipate and measure, but from the unpredictable shocks that no one has factored into prices. — Source: [First Eagle Insights]

- On avoiding ruin: The goal of investing is not to be perfectly right about the future, but to avoid being so wrong that it removes you from the game permanently. — Source: [Richer, Wiser, Happier Podcast]