Lessons from Meron Colbeci

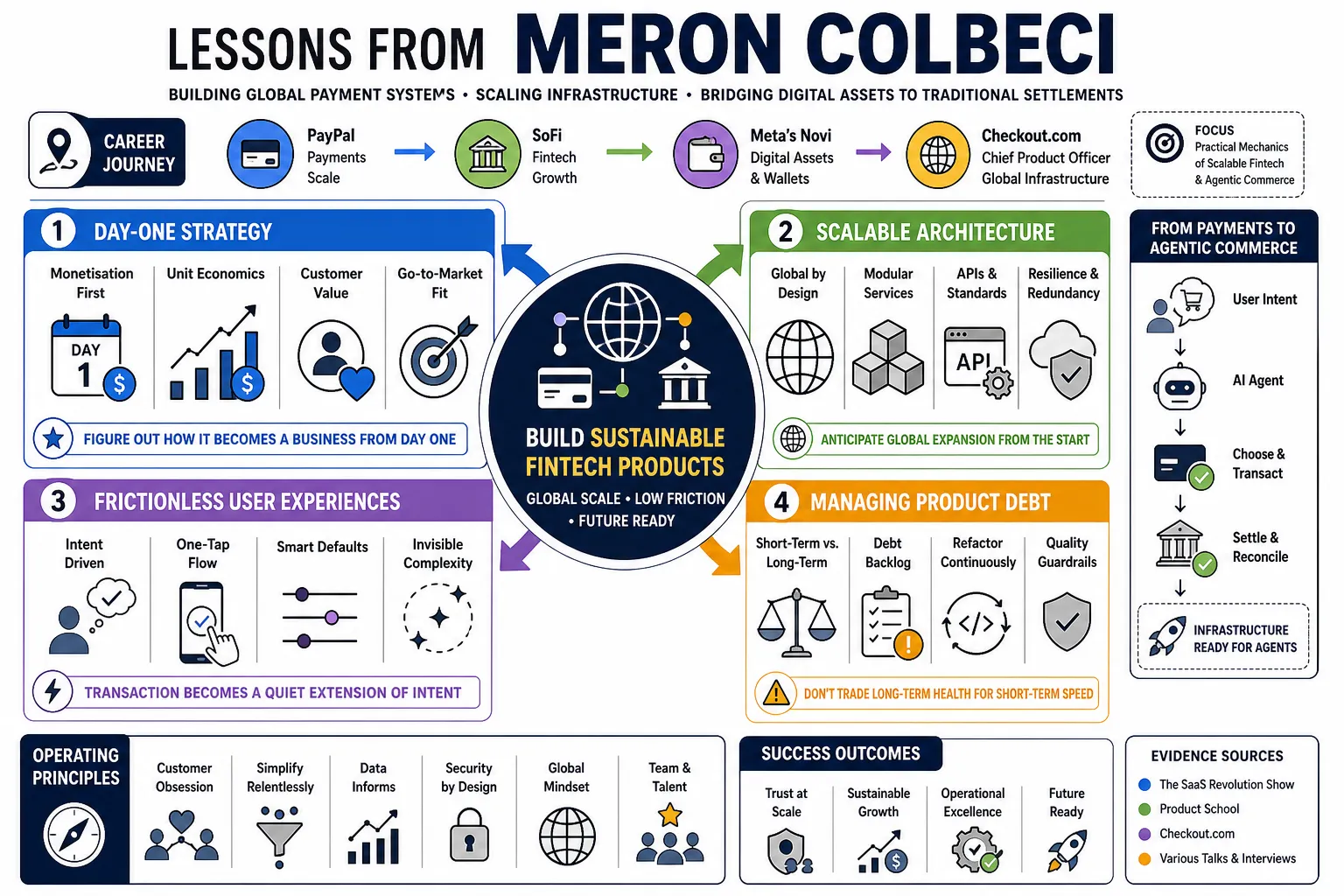

Meron Colbeci has spent his career running consumer and enterprise payment systems across PayPal, SoFi, Meta's Novi, and now as Checkout.com's Chief Product Officer. He focuses on the practical mechanics of scaling global financial infrastructure and moving digital assets into traditional settlements. This profile breaks down his technical and operational methods for building sustainable fintech products and prepping them for agentic commerce.

Part 1: Product Development & Design

- On Day-One Strategy: "I don't think that it's 'important' - it's absolutely critical to figure out the full monetisation strategy or 'how does this become a business' from the very first day." — Source: The SaaS Revolution Show

- On Scalable Architecture: "Building scalable financial products requires a foundational architecture that anticipates global expansion rather than treating it as an afterthought." — Source: Product School

- On Frictionless User Experiences: "The best financial technology reduces friction to the point where the transaction becomes a quiet extension of the user's intent." — Source: Checkout.com

- On Managing Product Debt: "Prioritizing immediate feature releases must be balanced with addressing underlying technical and product debt to sustain long-term velocity." — Source: The SaaS Revolution Show

- On Cross-Platform Consistency: Checkout.com's Money20/20 roundup says embedded finance only works when providers create a smooth experience that respects the merchant's brand while accounting for local market conditions. That supports the safer lesson that global consistency comes from a common platform that can flex around region-specific requirements. — Reference: Checkout.com Money20/20 roundup on smooth embedded-finance experiences

- On Consumer-Grade Enterprise Tools: "Enterprise fintech platforms must adopt the intuitive design principles traditionally reserved for consumer-facing applications." — Source: Product School

- On Iterative Prototyping: "Rapid iteration cycles in product development allow teams to validate complex financial features with users before committing heavy engineering resources." — Source: The Org

- On Data-Informed Design: "Product design decisions in fintech should be heavily influenced by transactional data patterns to optimize conversion rates." — Source: Checkout.com

- On Adapting to Scale: "The product management frameworks that work for early-stage fintechs often break down when transitioning to global payment volumes." — Source: Money20/20

- On End-to-End Ownership: "A successful product function oversees the entire lifecycle, from the initial user interface design down to the core operational processes." — Source: Product School

Part 2: Monetization & Business Strategy

- On Revenue Mechanics: "Understanding the unit economics of a transaction is a prerequisite before designing any user-facing payment feature." — Source: The SaaS Revolution Show

- On Strategic Market Entry: "Expanding into new markets, such as the U.S., requires a calculated approach that aligns product capabilities with regional merchant demands." — Source: The Stack

- On Partnership Economics: "Strategic integrations with platforms like Fireblocks demonstrate how collaborative tech ecosystems can drive mutual business growth." — Source: NYSE Floor Talk

- On Value Extraction: "Monetization shouldn't be bolted onto a product; it must naturally derive from the clear value provided to the end user." — Source: The SaaS Revolution Show

- On Pricing Transparency: "Clear and transparent pricing models are essential for building long-term trust with enterprise merchants." — Source: Checkout.com

- On Balancing Growth and Margins: "Rapid market expansion in fintech must be carefully weighed against the margin implications of processing low-value, high-volume transactions." — Source: Money20/20

- On Feature Packaging: "Bundling financial services effectively requires a deep understanding of merchant workflows and pain points." — Source: The SaaS Revolution Show

- On Competitive Differentiation: "In a crowded payments market, differentiation comes from specialized capabilities rather than just a race to the bottom on price." — Source: The Stack

- On Capital Efficiency: "Modern product leadership requires evaluating the capital efficiency of new initiatives just as rigorously as their technical feasibility." — Source: SaaStr Podcast

- On Long-Term Business Sustainability: "Building a market-leading product means aligning near-term user adoption with long-term revenue viability." — Source: The SaaS Revolution Show

Part 3: Scaling Global Fintech

- On Globalizing Products: Jas Shah's Fintech: Under the Hood episode description says Colbeci explains how a fintech globalises its product. That supports the narrower lesson that scaling payments internationally means handling local payment methods, compliance, and market-specific operating choices rather than forcing a single template everywhere. — Reference: Fintech: Under the Hood episode description on globalising fintech products

- On Infrastructure Resilience: "Global payment systems require infrastructure capable of handling high-throughput volume without degradation in authorization rates." — Source: Checkout.com

- On Localizing the Checkout Experience: "A standardized checkout process fails in a global context; localization is required for varying consumer payment preferences." — Source: Connecting the Dots in Fintech

- On Managing Latency: "Reducing transaction latency across international borders is a significant technical hurdle in scaling payment networks." — Source: Checkout.com

- On Regulatory Agility: Checkout.com's Money20/20 roundup says businesses incorporating embedded finance must think about a regulatory landscape that is inherently local. That supports the lesson that global payments products need architecture and operating practices that can adjust quickly as regional rules differ or change. — Reference: Checkout.com Money20/20 roundup on local regulatory landscapes

- On Scaling Talent: "As fintech companies expand across borders, maintaining a cohesive product culture across distributed teams becomes a primary leadership challenge." — Source: The Org

- On Cross-Border Settlements: "Improving the speed and reliability of cross-border settlements is a central focus for modern global payment platforms." — Source: Checkout.com

- On Market Nuances: "Understanding the subtle behavioral differences in how consumers interact with digital money in different countries is critical for adoption." — Source: Connecting the Dots in Fintech

- On Infrastructure as a Service: "Providing core payment capabilities as modular services allows merchants to scale their own operations more effectively internationally." — Source: The Stack

- On Managing Operational Complexity: "As the product portfolio grows globally, simplifying internal operations is necessary to maintain development speed." — Source: Product School

Part 4: Agentic Commerce & AI

- On Autonomous Agents: "Agentic commerce is reshaping the checkout moment, and Google's Agent Payments Protocol (AP2) is an important step forward." — Source: NoCash

- On Open Protocols: "At Checkout.com, we're proud to support open protocols that strengthen trust and give merchants the flexibility to meet their customers where they are, however they want to shop." — Source: NoCash

- On Machine-to-Machine Payments: "The rise of agentic commerce introduces a future where AI agents complete transactions on behalf of consumers." — Source: The Stack

- On Evolving Authentication: The same Checkout.com roundup says agentic commerce raises a basic identity question because the shopper is no longer necessarily the cardholder. That supports a safer lesson that authentication has to evolve when software agents begin initiating purchases on a user's behalf. — Reference: Checkout.com Money20/20 roundup on identity in agentic commerce

- On AI in Transaction Routing: "Leveraging AI for intelligent transaction routing can significantly optimize authorization rates and reduce processing costs." — Source: Checkout.com

- On Trust in Agentic Systems: "Establishing a framework of trust is the most critical dependency for the widespread adoption of AI-executed commerce." — Source: NoCash

- On Predictive Purchasing: "The intersection of payments and AI enables systems that anticipate consumer needs and automate the purchasing cycle." — Source: The Stack

- On Adaptive Fraud Models: Checkout.com's Money20/20 roundup links digital identity, deepfake risk, and agentic commerce to the need for stronger trust and verification technology. That supports the narrower lesson that fraud controls must adapt to agent-driven transaction behavior instead of assuming every purchase follows a traditional human checkout pattern. — Reference: Checkout.com Money20/20 roundup on trust, fraud, and verification

- On The New Checkout Interface: "Agentic commerce will eventually make traditional graphical checkout interfaces obsolete for routine purchases." — Source: Connecting the Dots in Fintech

Part 5: Payments Infrastructure as an Invisible Force

- On Invisible Payments: In the Fintech: Under the Hood introduction, Shah describes payment service providers as the invisible force that lets people buy safely online and in person, and says Checkout.com has embraced that framing. That supports the lesson that great payments infrastructure removes friction while staying dependable in the background. — Reference: Fintech: Under the Hood introduction on payments as an invisible force

- On Background Reliability: "Consumers should never have to think about the infrastructure processing their payments; its reliability must be an absolute given." — Source: Connecting the Dots in Fintech

- On Merchant Abstraction: "Effective payment platforms abstract away the complexities of acquiring banks, card networks, and alternative payment methods for the merchant." — Source: Checkout.com

- On The Infrastructure Layer: "Operating at the foundational infrastructure layer can shape millions of daily digital interactions." — Source: Money20/20

- On Minimizing Drop-offs: "Every visible step in a payment flow is a potential point of cart abandonment; the less visible the payment, the higher the conversion." — Source: Checkout.com

- On Embedded Finance: Checkout.com's Money20/20 roundup says integrating financial services directly into business platforms is transforming digital commerce, opening new revenue streams, boosting conversion, and deepening customer insight. That supports the lesson that embedded finance makes payments feel more like a built-in product capability than a separate flow. — Reference: Checkout.com Money20/20 roundup on the B2B embedded-finance opportunity

- On Tokenization: "The use of tokenization is a core mechanism for ensuring security while keeping the payment process invisible to returning users." — Source: Checkout.com

- On System Uptime: "When operating as an invisible infrastructure provider, system uptime and processing speed are the ultimate metrics of product quality." — Source: Product School

- On Integration: "Providing developer-friendly APIs helps merchants to embed payments invisibly into their proprietary applications." — Source: The Stack

Part 6: Stablecoins & Digital Assets

- On 24/7 Settlements: "The primary utility of stablecoin settlements for merchants lies in their ability to facilitate continuous, 24/7 access to funds." — Source: Payment Expert

- On Fiat and Crypto Convergence: "The future of payments involves a blended ecosystem where fiat currencies and digital assets operate interoperably." — Source: Checkout.com

- On Treasury Management: "Digital assets offer enterprise merchants new, more efficient mechanisms for corporate treasury management and cross-border liquidity." — Source: NYSE Floor Talk

- On Practical Crypto Utility: "Moving beyond speculation, the focus in digital assets must be on building practical utility for everyday commercial transactions." — Source: Money20/20

- On Secure Digital Asset Infrastructure: "Partnerships with specialized custody providers like Fireblocks are essential for securely managing enterprise digital asset operations." — Source: NYSE Floor Talk

- On On-Chain Transparency: "Leveraging blockchain technology provides an unprecedented level of auditability and transparency for complex financial flows." — Source: Checkout.com

- On Consumer Crypto Adoption: Checkout.com's stablecoin announcement says digital-money payments are especially useful in markets where access to cards is uneven, local currencies are volatile, or shoppers already hold digital dollars. That supports a safer lesson that consumer crypto adoption grows when the product solves everyday payment access problems rather than staying speculative. — Reference: Checkout.com stablecoin launch on practical consumer use cases

- On Regulatory Clarity for Digital Assets: "Designing crypto-based payment products requires operating within a framework that anticipates future regulatory oversight." — Source: Payment Expert

- On Stablecoins as a Medium of Exchange: "Stablecoins solve the volatility issue inherent in early cryptocurrencies, making them viable for standard merchant pricing and settlement." — Source: NYSE Floor Talk

Part 7: Product & Marketing Alignment

- On The New Power Partnership: "The alignment between product and marketing functions is rapidly becoming the most critical partnership within the modern C-suite." — Source: SaaStr Podcast

- On Unified Messaging: "A product's technical capabilities and its market positioning must be developed concurrently, not sequentially." — Source: SaaStr Podcast

- On Shared Metrics: "Product and marketing teams must be evaluated on shared business outcomes, such as merchant acquisition and retention, to ensure tight alignment." — Source: The Org

- On Go-To-Market Strategy: "A successful go-to-market motion requires the product team to deeply understand the marketing narratives that resonate with enterprise buyers." — Source: SaaStr Podcast

- On Feedback Loops: "Marketing provides the qualitative market signals that help product teams prioritize features that will actually drive commercial growth." — Source: SaaStr Podcast

- On Positioning Technical Features: "Translating complex payment infrastructure updates into clear, benefit-driven marketing messages is a joint responsibility." — Source: Checkout.com

- On Collaborative Roadmapping: "The product roadmap should be a collaborative document that reflects both technical feasibility and marketing timing." — Source: Product School

- On Launch Execution: "Product launches fail when marketing is brought in at the end; they succeed when marketing is involved from the product discovery phase." — Source: SaaStr Podcast

- On Understanding the Customer Voice: "Both product managers and marketers must spend significant time directly engaging with merchants to maintain a unified understanding of the customer voice." — Source: The SaaS Revolution Show

Part 8: Customer-Centricity & The Digital Economy

- On Evaluating Technology: "Having worked with Checkout.com before, I had a good sense of how great the technology was and how capable the team was." — Source: Checkout.com

- On Democratizing Access: "I was inspired by the focus on building customer-first technologies that will help democratize access to the digital economy." — Source: Checkout.com

- On Merchant-Centric Design: "Every product decision should map back to a specific operational pain point experienced by the merchant." — Source: Product School

- On Financial Inclusion: The same Checkout.com stablecoin announcement says giving consumers another way to pay online can help merchants capture demand in places where traditional card access is limited. That supports the lesson that scalable payments infrastructure can widen participation in the digital economy when it expands practical payment access. — Reference: Checkout.com stablecoin launch on expanding payment access

- On Designing for Trust: "In digital financial services, user interface design is fundamentally an exercise in establishing and maintaining user trust." — Source: Checkout.com

- On Solving Core Problems: "The most successful fintech products don't just optimize existing processes; they solve fundamental problems regarding money movement and access." — Source: The SaaS Revolution Show

- On The End-User Experience: "While selling to merchants, the ultimate test of a payment product is the frictionless experience it provides to the merchant's end consumer." — Source: Connecting the Dots in Fintech

- On Adapting to Merchant Growth: "A payment platform must be capable of seamlessly scaling alongside a merchant as they grow from a startup to a global enterprise." — Source: The Stack

- On The Purpose of Fintech: "The true measure of success in financial technology is transaction volume and the degree to which it expands participation in the global digital economy." — Source: Checkout.com