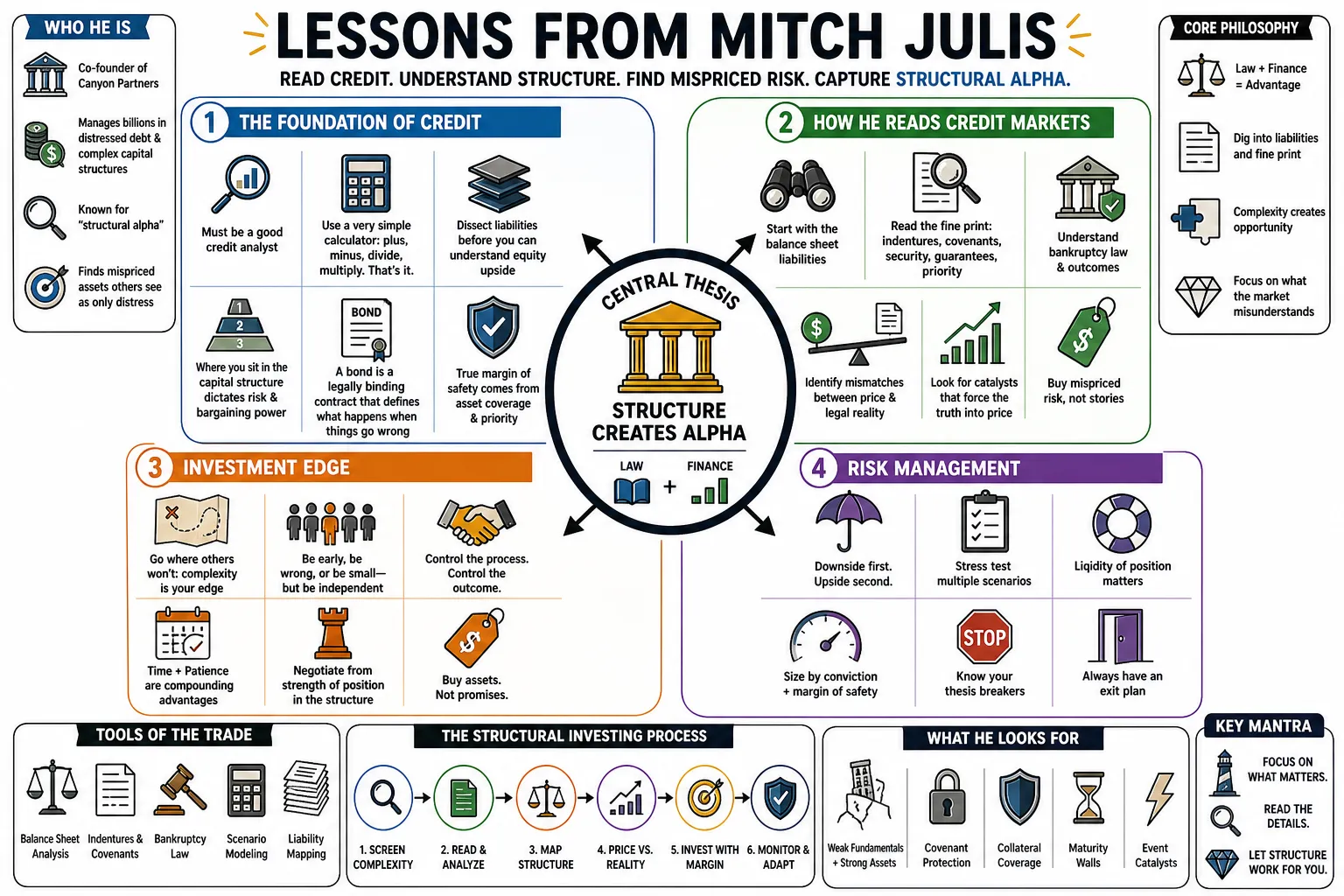

Lessons from Mitch Julis

Mitchell Julis co-founded Canyon Partners, a firm managing billions in distressed debt and complex capital structures. He built his reputation on "structural alpha," finding mispriced assets by digging into balance sheet liabilities and the fine print of bankruptcy law. This profile covers his methods for reading credit markets, mixing law and finance to spot arbitrage opportunities where others see only distress.

Part 1: The Foundation of Credit

- On the necessity of credit analysis: "To be a good value investor, you must be a good credit analyst." — Source: [Policy Punchline]

- On the simplicity of math: "I use a very simple calculator: plus, minus, divide, multiply. That's it." — Source: [Value Investing Congress]

- On capital structure: "You cannot understand a company's equity upside without first dissecting the exact terms of its liabilities." — Source: [Value Investing with Legends]

- On balance sheet priority: "Where you sit in the capital structure dictates both your risk and your bargaining power during a restructuring." — Source: [Canyon Partners Insights]

- On evaluating debt: "A bond is a legally binding contract that defines what happens when things go wrong." — Source: [Milken Institute Global Conference]

- On margin of safety: "True margin of safety in distressed investing comes from asset coverage, not earnings projections." — Source: [Private Capital Podcast]

- On the illusion of safety: "High ratings from credit agencies often mask underlying structural weaknesses in collateralized obligations." — Source: [Capital Allocators]

- On credit cycles: "Credit markets operate on a cycle of amnesia, where investors repeatedly forget the consequences of excess borrowing." — Source: [Institutional Investor]

- On fundamental analysis: "The most important work happens away from the screen, reading the covenants and understanding the legal obligations." — Source: [Value Investing with Legends]

- On distressed entry points: "The best time to buy debt is when forced sellers are liquidating for compliance reasons, rather than fundamental deterioration." — Source: [Milken Institute Global Conference]

Part 2: Navigating Complexity and Distress

- On structural alpha: "Alpha can be found in the structure of the investment itself, by identifying mispriced complexities that others refuse to analyze." — Source: [Private Capital Podcast]

- On market inefficiencies: "The most profitable opportunities exist in the spaces between traditional asset classes, where standard models fail to apply." — Source: [Canyon Partners Insights]

- On the value of lawyers in finance: "Legal knowledge is an analytical edge when evaluating distressed debt, because bankruptcy is a legal process." — Source: [Policy Punchline]

- On restructuring: "A bankruptcy filing is not the end of a company; it is often a mechanism to clear liabilities and uncover the actual value of the operating business." — Source: [Value Investing Congress]

- On information arbitrage: "In complex situations, the investor who reads the 500-page indenture has a distinct advantage over the one who relies on the summary." — Source: [Value Investing with Legends]

- On special situations: "Event-driven investing requires predicting human behavior and legal outcomes, not just cash flows." — Source: [Capital Allocators]

- On the nature of distress: "Distress usually stems from a mismatched capital structure rather than a fundamentally flawed business model." — Source: [Milken Institute Global Conference]

- On identifying catalysts: "A cheap bond is only a good investment if there is a clear legal or financial mechanism that will force value realization." — Source: [Institutional Investor]

- On market panic: "When generalists flee a complex sector, specialists can acquire assets at a discount to liquidation value." — Source: [Private Capital Podcast]

- On evaluating management in distress: "During a restructuring, you have to assess whether management is aligned with the equity holders or the new creditors." — Source: [Value Investing Congress]

Part 3: Law, Accounting, and Finance

- On accounting as accountability: "Accounting is the civic language of accountability; you cannot invest responsibly without speaking it fluently." — Source: [Policy Punchline]

- On financial reporting: "GAAP earnings often obscure the actual cash generation capability of a business undergoing restructuring." — Source: [Value Investing with Legends]

- On the intersection of disciplines: "The most successful distressed investors operate at the exact point where law, accounting, and finance overlap." — Source: [Private Capital Podcast]

- On reading footnotes: "The real risks are rarely on the income statement; they are buried in the footnotes detailing off-balance-sheet liabilities." — Source: [Institutional Investor]

- On creditor rights: "Your recovery in a default is determined entirely by the legal remedies available to your specific tranche of debt." — Source: [Milken Institute Global Conference]

- On academic foundations: "Studying public policy and law provides a framework for understanding how regulatory environments shape market outcomes." — Source: [Princeton University News]

- On corporate governance: "Weak covenants are a form of hidden debt that management can use at the expense of bondholders." — Source: [Value Investing Congress]

- On forensic analysis: "You have to look at the numbers like a forensic accountant, searching for what management is trying to hide." — Source: [Capital Allocators]

- On legal precedence: "Understanding how judges have ruled in past bankruptcies is required for pricing the risk of a current distressed asset." — Source: [Policy Punchline]

Part 4: Lessons from Drexel and Wachtell

- On learning at Drexel: "The environment at Drexel Burnham Lambert taught the importance of exhaustive research and understanding every layer of a company's financing." — Source: [Private Capital Podcast]

- On Michael Milken's influence: "Working under Milken demonstrated that high-yield debt, when properly underwritten, could offer equity-like returns with senior protections." — Source: [Value Investing with Legends]

- On the origins of the high-yield market: "The early days of high-yield required building custom financial structures to fund companies that traditional banks ignored." — Source: [Milken Institute Global Conference]

- On transitioning from law to finance: "Moving from Wachtell Lipton to Drexel allowed for the application of legal structuring skills directly to investment decisions." — Source: [Policy Punchline]

- On surviving market collapses: "The fall of Drexel showed that relying too heavily on a single funding mechanism carries existential risk." — Source: [Institutional Investor]

- On evaluating credit quality: "The 1980s proved that cash flow sustainability matters far more than historical credit ratings." — Source: [Value Investing Congress]

- On building a network: "The relationships formed during the Drexel era became the foundation for sourcing complex deals decades later." — Source: [Capital Allocators]

- On market perception: "Assets that are universally despised by the establishment often hold the greatest mathematical value." — Source: [Private Capital Podcast]

- On continuous learning: "The early career transitions from policy to law to finance were driven by a need to understand how capital actually moves through the economy." — Source: [Princeton University News]

Part 5: Building and Scaling Canyon Partners

- On founding principles: "Canyon was built on the premise that a multi-strategy approach allows capital to flow to wherever the mispricing is most severe." — Source: [Canyon Partners Insights]

- On partnership: "A successful firm requires partners who challenge your assumptions and bring complementary analytical skills." — Source: [Value Investing with Legends]

- On institutional growth: "Scaling an asset manager requires transitioning from a collection of smart trades to a repeatable process." — Source: [Capital Allocators]

- On avoiding silos: "Investment professionals must communicate across asset classes, because distress in the bond market usually previews problems in the equity market." — Source: [Institutional Investor]

- On client alignment: "Long-term success is only possible when the liquidity terms of the fund match the duration of the underlying investments." — Source: [Private Capital Podcast]

- On maintaining discipline: "As assets under management grow, the hardest task is passing on mediocre deals and waiting for genuine structural alpha." — Source: [Milken Institute Global Conference]

- On real estate integration: "Real estate debt often requires the same forensic credit analysis as corporate distress." — Source: [Canyon Partners Insights]

- On talent acquisition: "The best analysts are often those with non-traditional backgrounds who can read legal documents as well as spreadsheets." — Source: [Policy Punchline]

- On adapting to markets: "A firm must be willing to pivot from distressed debt to healthy corporate credit depending on where the cycle dictates value." — Source: [Value Investing Congress]

- On legacy: "Building a lasting firm means creating a culture that prioritizes intellectual debate over hierarchy." — Source: [Capital Allocators]

Part 6: Risk Management and Market Cycles

- On defining risk: "Risk is not volatility; risk is the permanent impairment of capital due to a misunderstanding of the legal structure." — Source: [Value Investing with Legends]

- On macroeconomic factors: "Macro trends are important, but they should serve as context for bottom-up credit analysis, not the primary driver of the investment." — Source: [Policy Punchline]

- On liquidity: "The price of an asset is often dictated more by the liquidity needs of the current holder than by the asset's intrinsic value." — Source: [Private Capital Podcast]

- On downside protection: "Every investment thesis must start by identifying the worst-case scenario and ensuring the legal documents provide a floor on losses." — Source: [Milken Institute Global Conference]

- On leverage: "Debt is a tool that amplifies returns, but it also reduces the margin of error to zero if cash flows stumble." — Source: [Institutional Investor]

- On market timing: "You cannot time the exact bottom of a credit cycle, but you can buy assets cheaply enough that the timing becomes irrelevant." — Source: [Value Investing Congress]

- On portfolio construction: "Concentration is necessary for outperformance, but it must be balanced by uncorrelated idiosyncratic situations." — Source: [Capital Allocators]

- On stress testing: "Models must be tested against extreme scenarios, because financial crises happen with much greater frequency than standard distributions predict." — Source: [Canyon Partners Insights]

- On patience: "The hardest part of value investing is holding cash when the market is expensive and peers are chasing yield." — Source: [Value Investing with Legends]

Part 7: Structural Alpha and Mispricing

- On real estate value: "The physical asset is only half the equation; the financing structure dictates who actually captures the value of the property." — Source: [Private Capital Podcast]

- On build-to-core strategies: "Funding new development can generate structural alpha if you accurately underwrite the supply and demand imbalances in specific local markets." — Source: [Canyon Partners Insights]

- On distressed property: "Buying the debt on a distressed building is often a safer and cheaper way to acquire the equity." — Source: [Milken Institute Global Conference]

- On municipal finance: "Evaluating municipal debt requires understanding local politics and pension obligations just as much as tax revenue." — Source: [Policy Punchline]

- On litigation finance: "Treating legal claims as an investable asset class requires a deep understanding of judicial precedent and settlement probabilities." — Source: [Institutional Investor]

- On corporate spin-offs: "Spinoffs frequently create forced selling by index funds, generating artificial price dislocation for value investors to exploit." — Source: [Value Investing Congress]

- On post-reorganization equity: "Companies emerging from bankruptcy often trade at a discount because their new shareholder base consists of former creditors eager to sell." — Source: [Value Investing with Legends]

- On regulatory changes: "Shifts in banking regulations constantly create new pockets of illiquidity where non-bank lenders can step in and dictate terms." — Source: [Capital Allocators]

- On asset complexity: "The harder an asset is to explain to a traditional investment committee, the higher the likelihood it is mispriced." — Source: [Private Capital Podcast]

Part 8: Philosophy, Teaching, and Values

- On intellectual humility: "The market will quickly punish arrogance; you must constantly reassess your thesis as new facts emerge." — Source: [Value Investing with Legends]

- On the role of education: "Establishing programs in public policy and finance ensures that future leaders understand the practical implications of economic theory." — Source: [Princeton University News]

- On Jewish values in business: "Ethical behavior and a commitment to debate and textual analysis are principles that translate directly from Jewish tradition to financial analysis." — Source: [Stars of David Podcast]

- On mentorship: "Having great teachers and partners is the single most important factor in developing a durable investment philosophy." — Source: [Policy Punchline]

- On curiosity: "The best investors maintain a relentless curiosity about how systems work, from macroeconomic policy down to municipal zoning laws." — Source: [Capital Allocators]

- On long-term thinking: "True wealth creation comes from compounding capital over decades, which requires ignoring the daily noise of the financial press." — Source: [Milken Institute Global Conference]

- On philanthropy: "Financial success should be used to support institutions that promote rigorous academic inquiry and civic responsibility." — Source: [Princeton University News]

- On critical thinking: "Do not accept the consensus view; always read the primary source documents and do the math yourself." — Source: [Value Investing Congress]

- On the nature of markets: "Markets are systems of human behavior; understanding history and psychology is just as important as understanding finance." — Source: [Private Capital Podcast]