Lessons from Munib Islam

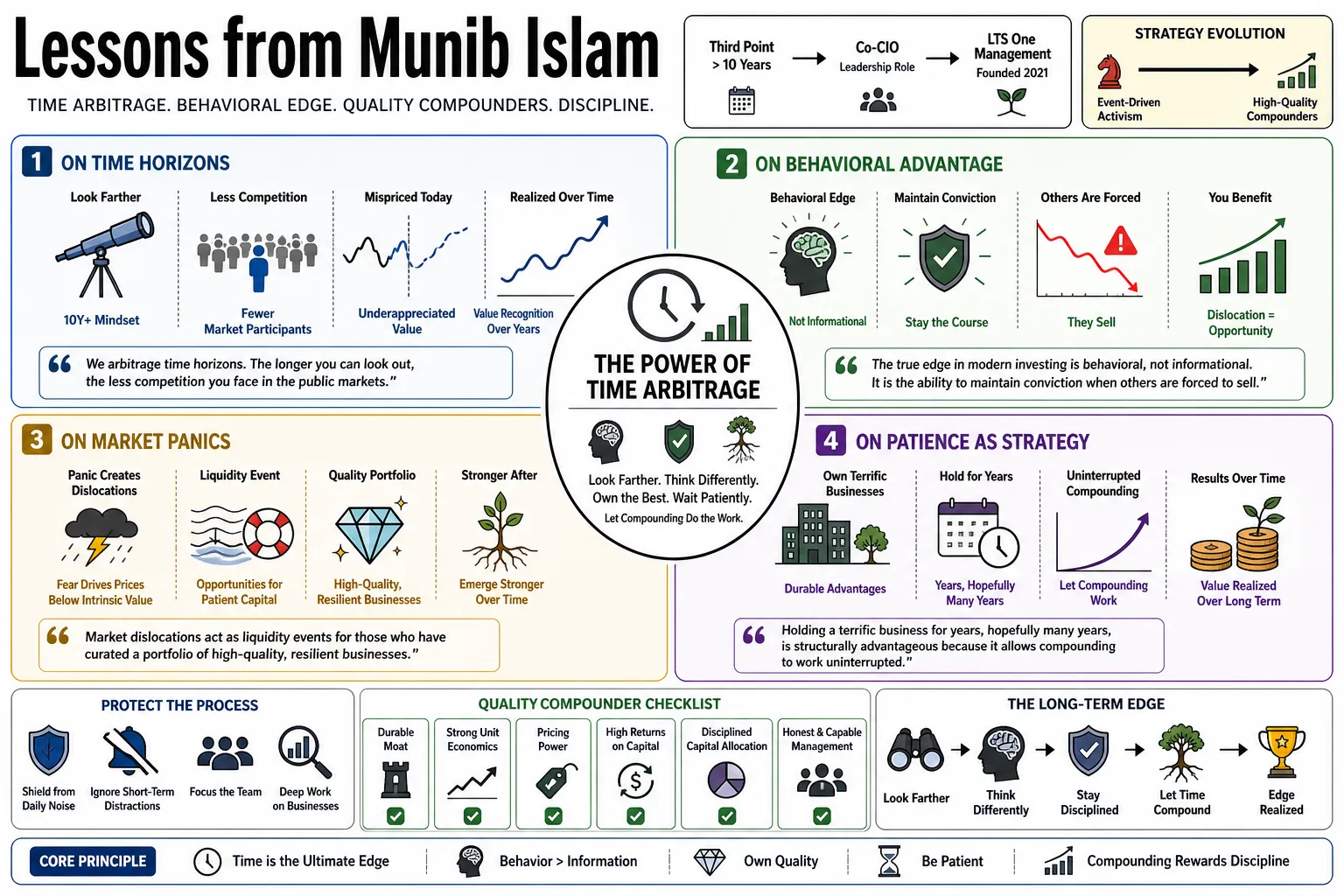

Munib Islam spent more than a decade at Third Point, rising to co-CIO before leaving to found LTS One Management in 2021. Over his career, his strategy has shifted away from event-driven activism and toward buying high-quality compounders for the long term. This collection covers his approach to time arbitrage, assessing business quality, and the discipline required to simply sit on great stocks.

Part 1: The Power of Time Arbitrage

- On Time Horizons: "We arbitrage time horizons. The longer you can look out, the less competition you face in the public markets." — Source: [Masters Invest]

- On Behavioral Advantage: "The true edge in modern investing is behavioral, not informational. It is the ability to maintain conviction when others are forced to sell." — Source: [Value Investing with Legends]

- On Market Panics: "Market dislocations act as liquidity events for those who have curated a portfolio of high-quality, resilient businesses." — Source: [Masters Invest]

- On Patience as Strategy: "Holding a terrific business for years, hopefully many years, is structurally advantageous because it allows compounding to work uninterrupted." — Source: [Masters Invest]

- On the Daily Noise: "We must actively protect our analysts from the daily noise and market distractions to foster the environment required for deep, substantive research." — Source: [Masters Invest]

- On Institutional Constraints: "Many institutional investors are trapped by quarterly performance metrics, leaving multi-year structural advantages mispriced." — Source: [Value Investing with Legends]

- On Delayed Gratification: "The capacity for delayed gratification is arguably the most important variable in realizing extraordinary investment returns." — Source: [LTS One Management Overview]

- On Compounding Over Time: "Time is the enemy of the poor business and the friend of the great one. We simply aim to align ourselves with the latter." — Source: [Masters Invest]

- On Strategic Inactivity: "Once a great asset is acquired at a reasonable price, the most difficult and profitable action is often doing nothing at all." — Source: [Value Investing with Legends]

- On Horizon Arbitrage in Europe: "European markets frequently offer exceptional businesses trading at discounts to U.S. peers because local investors are structurally less patient." — Source: [Masters Invest]

Part 2: Defining and Measuring Business Quality

- On Moats: "A sustainable competitive advantage is not a static trait; it is a dynamic barrier that management must widen every single day." — Source: [Value Investing with Legends]

- On Profitability Machines: "We look for profitability machines, meaning companies that can sustainably generate high returns on invested capital over decades." — Source: [Masters Invest]

- On Establishing Quality First: "Business quality must always be established and stress-tested before we even begin to discuss valuation." — Source: [Masters Invest]

- On Unit Economics: "True business quality is revealed at the unit economic level. If the micro does not work, the macro story is irrelevant." — Source: [Value Investing with Legends]

- On Pricing Power: "The truest test of a moat is the unexercised capacity to raise prices without permanently impairing unit volume." — Source: [LTS One Management Overview]

- On Organic Growth: "We prioritize businesses capable of driving organic growth through internal reinvestment rather than relying on financial engineering or serial acquisitions." — Source: [Masters Invest]

- On Competitive Dynamics: "Understanding who the customer is, why they stay, and how much pain they would endure before switching is fundamental to assessing quality." — Source: [Value Investing with Legends]

- On Capital Intensity: "The best businesses in the world require very little incremental capital to grow their cash flows." — Source: [LTS One Management Overview]

- On Industry Structure: "An average company in a structurally sound, consolidated industry often outperforms a great company in a highly fragmented, rational industry." — Source: [Third Point Transition Announcement]

- On Durability: "We must assess whether a company’s competitive advantage can remain sustainable for the foreseeable future, beyond the current management team." — Source: [Masters Invest]

Part 3: The Importance of Corporate Culture and Trust

- On Trust as an Asset: "Trust is a highly durable economic asset. It lowers transaction costs internally and builds unshakeable customer loyalty externally." — Source: [Masters Invest]

- On Human Cooperation: "Great companies harness the dynamics of human cooperation and foster a family-like commitment among their employees." — Source: [Masters Invest]

- On Cultural Due Diligence: "Assessing culture is as critical as assessing the balance sheet. A toxic culture is an unrecorded liability." — Source: [Value Investing with Legends]

- On Decentralization: "Empowering operational leaders and pushing decision-making down to the lowest logical level is a hallmark of scalable cultures." — Source: [Value Investing with Legends]

- On Ownership Mentality: "When employees view themselves as owners rather than renters, the entire trajectory of the enterprise shifts." — Source: [LTS One Management Overview]

- On Transparency: "Cultures that punish honest mistakes breed fear and stagnation. Cultures that study mistakes breed innovation." — Source: [Masters Invest]

- On Founder Influence: "The cultural imprint of a visionary founder can compound value for decades after they have stepped back from daily operations." — Source: [Value Investing with Legends]

- On Customer Obsession: "The strongest cultures are not competitor-obsessed; they are intensely, almost irrationally, customer-obsessed." — Source: [Masters Invest]

- On Cultural Entropy: "Culture requires constant maintenance. Without intentional reinforcement, institutional standards naturally degrade over time." — Source: [Third Point Transition Announcement]

- On Intangible Moats: "The hardest competitive advantages for rivals to replicate are the intangible ones: shared beliefs, aligned incentives, and mutual trust." — Source: [Masters Invest]

Part 4: Capital Allocation and Reinvestment

- On the Value of Reinvestment: "A high return on invested capital is only half the equation. The ability to reinvest large sums of capital at those rates is what creates compounding machines." — Source: [Value Investing with Legends]

- On Capital Scarcity: "Managers who operate with a mentality of capital scarcity tend to make vastly superior allocation decisions." — Source: [Masters Invest]

- On Dividends vs. Growth: "If a company has a clear runway to reinvest capital at 20% returns, paying a dividend is a destruction of shareholder value." — Source: [LTS One Management Overview]

- On Share Repurchases: "Buybacks are mathematically brilliant when the stock is undervalued and criminally wasteful when it is overvalued." — Source: [Value Investing with Legends]

- On M&A Strategy: "Most acquisitions destroy value. The rare exceptions are led by operators who approach M&A with the discipline of a value investor." — Source: [Masters Invest]

- On the Denominator Effect: "Growth in earnings means little if the share count is expanding at the same rate. We focus on per-share value creation." — Source: [Third Point Transition Announcement]

- On Option Value: "The best capital allocators keep their balance sheets pristine to take advantage of the option value of distress in their industry." — Source: [Value Investing with Legends]

- On Base Rates: "When evaluating a company's transition into a new market, we heavily weight the base rates of similar historical pivots." — Source: [Masters Invest]

- On R&D Spend: "True R&D is a capital expenditure disguised as an operating expense. We look for companies that invest heavily in their own obsolescence." — Source: [Masters Invest]

Part 5: Management Evaluation and Incentives

- On Skin in the Game: "We insist on competent management with substantial skin-in-the-game. Incentives drive all human behavior." — Source: [Masters Invest]

- On Agency Costs: "The public market is riddled with agency costs. Our job is to find the rare management teams that treat outside capital as their own." — Source: [Value Investing with Legends]

- On Compensation Structures: "If a CEO's bonus is tied to absolute revenue growth rather than per-share metrics, you are virtually guaranteeing value destruction." — Source: [LTS One Management Overview]

- On Leadership Temperament: "We evaluate the temperament of a CEO during a crisis. The best leaders exhibit calm rationality when others panic." — Source: [Masters Invest]

- On Founder-Led Businesses: "There is an empirical advantage to investing alongside founders who view their company as their life's work, rather than a career stepping stone." — Source: [Value Investing with Legends]

- On Board Independence: "A truly independent board is the shareholder's first line of defense. Weak boards enable entrenched management." — Source: [Third Point Transition Announcement]

- On Succession Planning: "The final test of a great CEO is their ability to select and groom a successor who can maintain or improve the institutional standards." — Source: [Masters Invest]

- On Candor: "Read the shareholder letters. Managers who speak candidly about their failures are far more trustworthy than those who only highlight their successes." — Source: [Value Investing with Legends]

- On Capital Allocation Track Records: "A CEO's track record of capital allocation is the most objective metric of their strategic competence." — Source: [Masters Invest]

Part 6: Continuous Learning and Multi-Disciplinary Thinking

- On Borrowing Wisdom: "My investment framework is deeply rooted in curiosity and a commitment to learning from legendary operators like Bezos, Sinegal, and Singleton." — Source: [Masters Invest]

- On Mental Models: "No single model is sufficient for understanding complex realities. You must build a latticework of mental models across disciplines." — Source: [Masters Invest]

- On Reading Broadly: "The answers to the most difficult investment questions are rarely found in finance textbooks. They are found in history, psychology, and biology." — Source: [Value Investing with Legends]

- On Evolving Frameworks: "An investor who hasn't changed their mind on a core belief in five years is likely suffering from intellectual stagnation." — Source: [LTS One Management Overview]

- On the Role of Mentorship: "The transition from an event-driven mindset to a compounding mindset is a journey best navigated with the guidance of experienced mentors." — Source: [Third Point Transition Announcement]

- On Studying Failure: "We spend as much time studying the catastrophic failures of once-great businesses as we do studying the successes." — Source: [Masters Invest]

- On Intellectual Honesty: "The hardest person to fool is yourself. Intellectual honesty requires a systematic process for tracking your own mistakes." — Source: [Value Investing with Legends]

- On Curiosity as a Filter: "When interviewing analysts, extreme, unquenchable curiosity is the single most predictive trait of future success." — Source: [Masters Invest]

- On the Synthesis of Ideas: "Alpha is often generated at the intersection of two seemingly unrelated fields of study." — Source: [Masters Invest]

Part 7: Risk Management and Market Psychology

- On Redefining Risk: "Risk is not volatility. Risk is the permanent impairment of capital, often resulting from overpaying for deteriorating businesses." — Source: [Value Investing with Legends]

- On Margin of Safety: "A margin of safety allows you to be wrong about the macro environment and still survive the investment." — Source: [LTS One Management Overview]

- On Uncommon Sense: "In periods of market euphoria, common sense becomes incredibly uncommon. That is when discipline is most vital." — Source: [Masters Invest]

- On Quantitative Illusions: "Relying exclusively on quantitative data at the expense of rational, qualitative thinking is a recipe for disaster." — Source: [Masters Invest]

- On Market Consensus: "You cannot generate superior returns by agreeing with the consensus. You must be divergent and you must be right." — Source: [Value Investing with Legends]

- On Luck Versus Skill: "In the investment business, it is dangerously easy to confuse a bull market with personal genius." — Source: [Masters Invest]

- On Position Sizing: "Conviction should dictate position size. If you are not willing to make it a meaningful part of the portfolio, you likely haven't done enough work." — Source: [Third Point Transition Announcement]

- On Emotional Control: "The mechanics of valuation are simple; the psychology of investing is agonizingly difficult." — Source: [Value Investing with Legends]

- On Narrative Bias: "Investors are hardwired to love a good story. We must constantly verify that the math supports the narrative." — Source: [Masters Invest]

Part 8: Navigating Public versus Private Markets

- On the Private Market Mindset: "We approach public equities with the exact same rigorous, long-term ownership mentality as a private equity sponsor." — Source: [Value Investing with Legends]

- On Activism's Evolution: "Activism has its place, but true compounding happens through constructive private engagement rather than public combat." — Source: [LTS One Management Overview]

- On Liquidity as a Tool: "Public market liquidity is a tool to be used opportunistically, not a mandate to trade frantically." — Source: [Value Investing with Legends]

- On Board Dynamics: "Sitting on a corporate board teaches you the stark difference between reading a proxy statement and driving actual operational change." — Source: [Masters Invest]

- On Sourcing Ideas: "The best public market investments often mirror the characteristics of the most highly sought-after private market buyouts." — Source: [Third Point Transition Announcement]

- On Constructive Engagement: "Management teams are far more receptive to advice when it comes from a discreet partner rather than a hostile agitator." — Source: [Value Investing with Legends]

- On Information Asymmetry: "In public markets, the edge has shifted from acquiring unique information to possessing a unique interpretation of ubiquitous information." — Source: [Masters Invest]

- On Alignment with Founders: "Partnering with families like the founders of 3G Capital allows us to deploy capital with structural patience that most funds lack." — Source: [LTS One Management Overview]

- On the Ultimate Goal: "Whether public or private, the objective remains the same: identify exceptional operators, allocate capital rationally, and get out of their way." — Source: [Value Investing with Legends]