Lessons from Neil Dutta

As Head of Economic Research at Renaissance Macro Research, Neil Dutta built his reputation by predicting US economic resilience in 2022 when consensus expected a recession, and later calling the early softening in labor and housing markets. This profile collects his views on consumer spending, monetary policy, and the practical link between macroeconomic data and the markets.

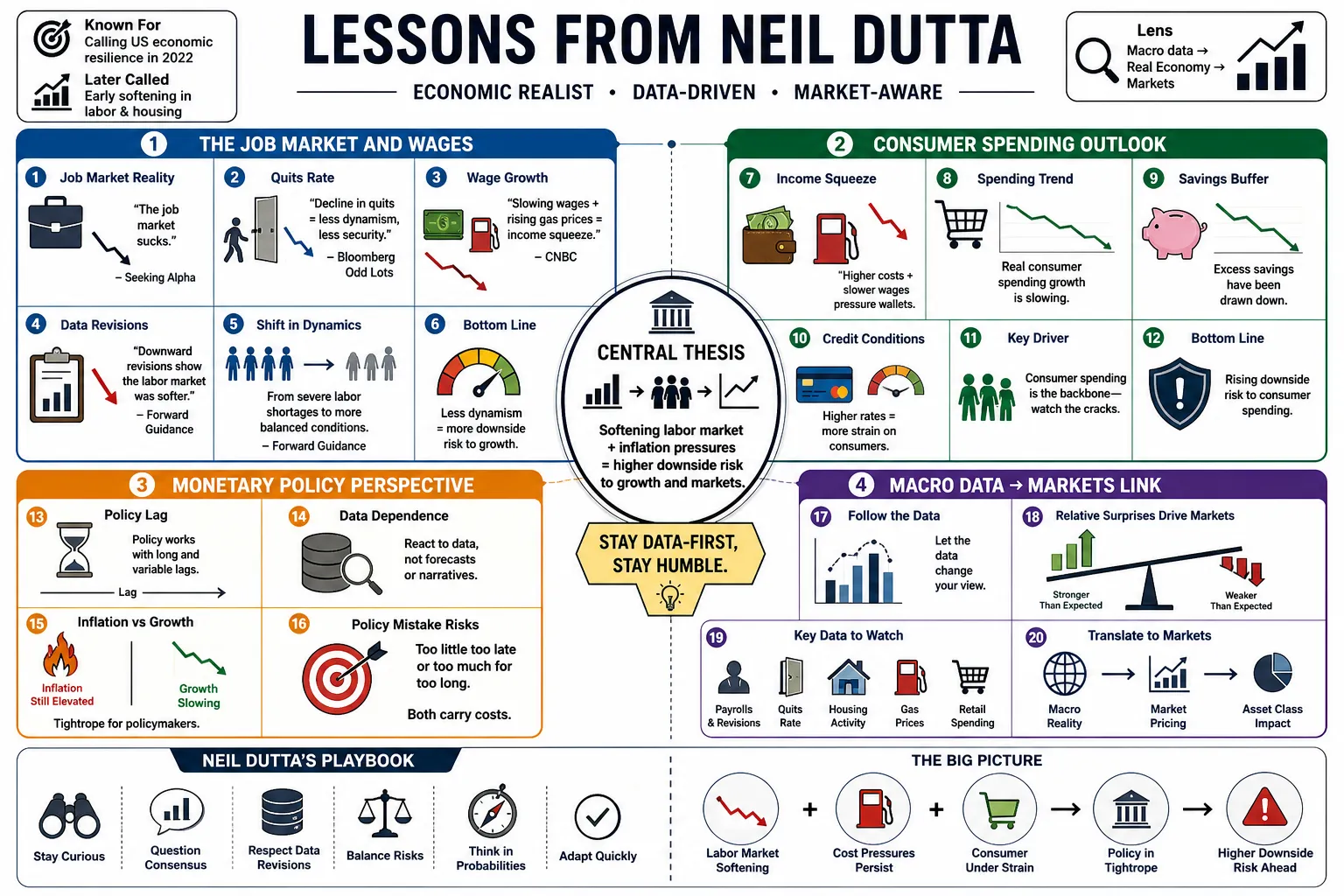

Part 1: The Job Market and Wages

- On weak labor markets: "The job market sucks." — Source: Seeking Alpha

- On the quits rate: "The decline in workers quitting their jobs is a clear indicator that the labor market is losing its dynamism and workers are feeling less secure." — Source: Bloomberg Odd Lots

- On wage growth: "Slowing wage growth combined with rising gasoline prices is creating an income squeeze that increases the downside risk to consumer spending." — Source: CNBC

- On employment data revisions: "Downward revisions to payroll data often reveal that the labor market was much softer in real-time than the initial headline numbers suggested." — Source: Forward Guidance

- On the shift in labor dynamics: "We have moved from an environment of severe labor shortages to one where employers have regained the upper hand." — Source: Renaissance Macro Research

- On hiring versus firing: "Even if companies aren't executing mass layoffs, a freeze in new hiring is enough to slowly push the unemployment rate higher." — Source: Bloomberg Surveillance

- On the labor market's lag: "The labor market is often the last domino to fall; by the time unemployment spikes, the economic damage has already been done elsewhere." — Source: Masters in Business

- On initial jobless claims: "Initial claims remain one of the best, most timely indicators of turning points in the economic cycle." — Source: Fox Business

- On wage inflation: "Wage growth is a lagging indicator of inflation, not a leading one, meaning the Fed shouldn't wait for wages to crash before cutting rates." — Source: Bloomberg Odd Lots

- On prolonged weakness: "The softening of the labor market doesn't happen overnight; it is death by a thousand cuts, and it's already started." — Source: The Indian Sun

Part 2: Inflation and Prices

- On the nature of inflation: "Inflation that remains above the 2% target for several years forces the Fed to adopt a more hawkish tone to establish credibility." — Source: Morningstar

- On supply shocks: "You have to separate supply-shock volatility from true demand-driven inflation to understand the underlying trend." — Source: Renaissance Macro Research

- On inflation targets: "The last mile of getting inflation back down to exactly 2% is often the hardest and most economically painful." — Source: Bloomberg Surveillance

- On service sector inflation: "Sticky services inflation is the primary reason the Federal Reserve has had to maintain higher rates for longer." — Source: CNBC

- On core versus headline CPI: "While headline inflation grabs the news, core CPI is what policymakers actually trade and make decisions on." — Source: Forward Guidance

- On the impact of tariffs: "You can't spell liberation without obliteration. The economic damage from trade tensions and tariffs is already in motion." — Source: The Indian Sun

- On pricing power: "Companies that enjoyed massive pricing power during the pandemic are finding that consumers are finally pushing back." — Source: Masters in Business

- On deflationary forces: "Goods deflation has been a massive tailwind for the headline inflation numbers, masking some of the stickiness in services." — Source: Bloomberg Odd Lots

- On energy prices: "Spikes in energy and gasoline prices act as a direct tax on the consumer, complicating the inflation picture while simultaneously slowing growth." — Source: Fox Business

Part 3: Federal Reserve and Monetary Policy

- On Fed reaction functions: "The stock market has probably predicted four of the last five Fed pivots." — Source: Masters in Business

- On a looming policy error: "They should be teeing up a cut for June. They won't. But they should." — Source: Bloomberg Odd Lots

- On the Fed's predicament: "The Fed faces a difficult predicament when conflicting economic signals—such as slowing wage growth but volatile labor data—make policy paths unclear." — Source: Seeking Alpha

- On rate hike probabilities: "The White House has effectively given the Fed a green light to hike interest rates if necessary to establish credibility." — Source: Investing.com

- On waiting too long: "The primary risk for the Federal Reserve is waiting too long to adjust policy as unemployment begins to rise." — Source: Bloomberg Odd Lots

- On monetary lags: "Monetary policy operates with long and variable lags, meaning the economy is still digesting the impact of previous tightening." — Source: Renaissance Macro Research

- On Fed credibility: "Central bankers will often prioritize their inflation-fighting credibility over short-term economic pain." — Source: Morningstar

- On the neutral rate: "The debate over where the neutral rate of interest actually sits is the most important argument in macroeconomics right now." — Source: Forward Guidance

- On restrictive policy: "Just because the economy hasn't broken yet doesn't mean policy isn't restrictive; it just means the buffers were larger than expected." — Source: Bloomberg Surveillance

- On quantitative tightening: "QT operates quietly in the background, but it steadily drains liquidity and tightens financial conditions over time." — Source: CNBC

Part 4: The Consumer and Real Income

- On the consumer illusion: "Dollars might be getting spent, but not much stuff is being bought." — Source: Renaissance Macro Research

- On consumer reliance: "If you're banking on the consumer to simply hold everything up, you might be late to catch a more material slowdown in the economy." — Source: Fox Business

- On the income squeeze: "The combination of sticky inflation and cooling wages creates a real income squeeze that inevitably limits household spending." — Source: Bloomberg Odd Lots

- On the K-shaped recovery: Dutta warns that consumer spending can look healthy in aggregate while labor softness, flat real disposable income, and slowing wage growth create a weaker path for many households. — Reference: Business Insider interview on labor softness, income growth, and consumer-spending risk

- On excess savings: "The buffers of excess savings accumulated during the pandemic have largely been depleted for the bottom half of the income distribution." — Source: Seeking Alpha

- On credit card debt: "Rising credit card balances and increasing delinquency rates are clear signs of stress among lower-income consumers." — Source: CNBC

- On consumer confidence: "Consumer sentiment often tracks gasoline prices and headline inflation more closely than the actual unemployment rate." — Source: Forward Guidance

- On spending habits: "Even if external shocks resolve, it does not mean consumers will immediately increase their discretionary spending." — Source: Renaissance Macro Research

- On retail sales: "Headline retail sales can look robust purely due to inflation, masking a decline in the actual volume of goods purchased." — Source: Masters in Business

- On household balance sheets: "While aggregate household net worth looks at record highs on paper, that wealth is not evenly distributed or easily accessible for daily spending." — Source: Bloomberg Surveillance

Part 5: Housing and Real Estate

- On the housing recession: "The housing sector is functionally in a recession, struggling to get things moving despite builder incentives." — Source: Seeking Alpha

- On housing and the broader economy: "Without activity in new home sales, the pipeline for future construction dries up, which subsequently reduces the household spending tied to housing." — Source: John Burns Research and Consulting

- On affordability: In the JBREC housing discussion, Dutta points to rising inventories where builders operate, falling home prices, and choppy mortgage-rate conditions as the core housing pressure points. — Reference: JBREC housing-market interview with Neil Dutta

- On mortgage rates: "The housing market is entirely captive to the path of mortgage rates, which are dictated by the Fed's fight against inflation." — Source: Morningstar

- On builder sentiment: "Homebuilder confidence often leads actual construction data, providing an early warning sign for the residential real estate sector." — Source: CNBC

- On the lock-in effect: "Existing homeowners are locked into low mortgage rates, restricting supply and creating a dysfunctional existing home sales market." — Source: Bloomberg Odd Lots

- On housing as a leading indicator: "Housing is traditionally the most interest-rate sensitive sector and is usually the first to enter and exit an economic cycle." — Source: Fox Business

- On rent inflation: "Market asking rents have cooled significantly, but it takes a long time for this to filter into the official inflation data." — Source: Renaissance Macro Research

- On real estate feedback loops: Dutta treats housing as economically important even though residential investment is only a modest share of GDP, because rising inventories, weaker home prices, and softer construction employment can feed into broader slowdown risk. — Reference: JBREC transcript on residential investment, housing inventories, and broader economic risk

Part 6: Markets vs. The Economy

- On the market-economy relationship: "The stock market is not the economy, but it's not NOT the economy." — Source: The Transcript

- On market timing: "The stock market has probably predicted four of the last five Fed pivots, rather than actual economic recessions." — Source: Masters in Business

- On safe havens: "If there's a recession, Treasuries will be bid. That's still the play." — Source: The Indian Sun

- On taking the other side of consensus: "The most profitable trades often come from taking the other side of a deeply entrenched macroeconomic consensus." — Source: Forward Guidance

- On the role of a market economist: "The job is taking esoteric economic research and moving it from the far five-yard line into the end zone for investors." — Source: Masters in Business

- On market narratives: "Investors must be wary of economic narratives that sound too good to be true and focus instead on the raw data." — Source: Fox Business

- On equity risk premiums: "When bond yields rise significantly, they naturally compress the equity risk premium, forcing a re-evaluation of stock valuations." — Source: Bloomberg Surveillance

- On credit spreads: "Corporate credit spreads are often a better real-time indicator of economic distress than the equity market." — Source: CNBC

- On market complacency: "Markets can remain irrational and complacent about macroeconomic risks for far longer than fundamental data justifies." — Source: Renaissance Macro Research

Part 7: AI and Business Investment

- On AI versus the consumer: "Over the last six months, capital expenditures on AI added more to the growth of the US economy than all consumer spending combined." — Source: Renaissance Macro Research

- On the narrowness of capex: "While AI investment is booming, traditional business investment outside of the tech sector has been quite sluggish." — Source: John Burns Research and Consulting

- On AI masking weakness: Dutta separates the AI capex boom from the rest of the economy: he has argued that AI-related information-processing equipment and software added more to GDP growth in early 2025 than consumer spending, while other business investment looked sluggish. — Reference: Sherwood coverage of Dutta's AI-capex contribution to GDP growth

- On the sustainability of the AI boom: "The key question for the macro outlook is whether the AI investment cycle can sustain the broader economy indefinitely." — Source: Bloomberg Odd Lots

- On productivity gains: "If AI truly delivers on its promise, we should eventually see it reflected in higher aggregate productivity numbers, not just tech earnings." — Source: Forward Guidance

- On corporate margins: "The ability of companies to maintain profit margins in a slowing economy depends heavily on their capacity to deploy technology to reduce labor costs." — Source: Fox Business

- On tech as a defensive sector: "In the modern economy, large technology companies with massive cash piles increasingly act as defensive assets during periods of macro uncertainty." — Source: Masters in Business

- On capital misallocation: "Periods of massive technological hype always carry the risk of capital misallocation, which eventually weighs on growth." — Source: CNBC

- On equipment and software: "When analyzing capex, looking specifically at information processing equipment and software tells the real story of corporate priorities." — Source: Renaissance Macro Research

Part 8: Forecasting and Macro Philosophy

- On changing your mind: Dutta's 2025 recession call is framed as a change in the same checklist he used earlier: no excess savings, visibly softer labor markets, housing stocks rolling over, and business confidence already bruised. — Reference: The Indian Sun summary of Dutta's changed recession view

- On recession predictions: The Forward Guidance episode description says Dutta explains why he avoided recession calls in prior years but was calling for one in 2025, with the labor market weakening and tariffs, wages, and oil shaping the outlook. — Reference: Blockworks Forward Guidance episode page on Dutta's 2025 recession call

- On incremental correctness: "Success in macro forecasting is about incremental correctness and adjusting probabilities, not making singular heroic calls." — Source: Tamma Capital

- On data dependence: "True data dependence means being willing to abandon your prior thesis when the incoming numbers invalidate it." — Source: Bloomberg Surveillance

- On the shape of downturns: "Not every recession is a spectacular financial crash; some are just long, shallow, and driven by an erosion of confidence and spending." — Source: The Indian Sun

- On contrarianism: "Being a contrarian isn't about just being different; it's about seeing where the consensus has extrapolated the data too far." — Source: Forward Guidance

- On leading indicators: "You have to look at the second derivative of the data—the rate of change—to catch turning points before they become obvious." — Source: Bloomberg Odd Lots

- On base effects: "Understanding year-over-year base effects is crucial; sometimes the data looks good simply because the previous year was so terrible." — Source: Renaissance Macro Research

- On the limits of macro: "Macroeconomics can tell you the direction of the tide, but it can't always tell you which specific boats will float or sink." — Source: Masters in Business