Lessons from Paul Black

Paul Black, co-CEO and portfolio manager at WCM Investment Management, helped grow the firm from a small operation into a major global equity player. He argues that a company's culture dictates the trajectory of its competitive moat, and that this trajectory matters far more than the moat's absolute size. This profile outlines his framework for analyzing businesses and identifying sustainable growth.

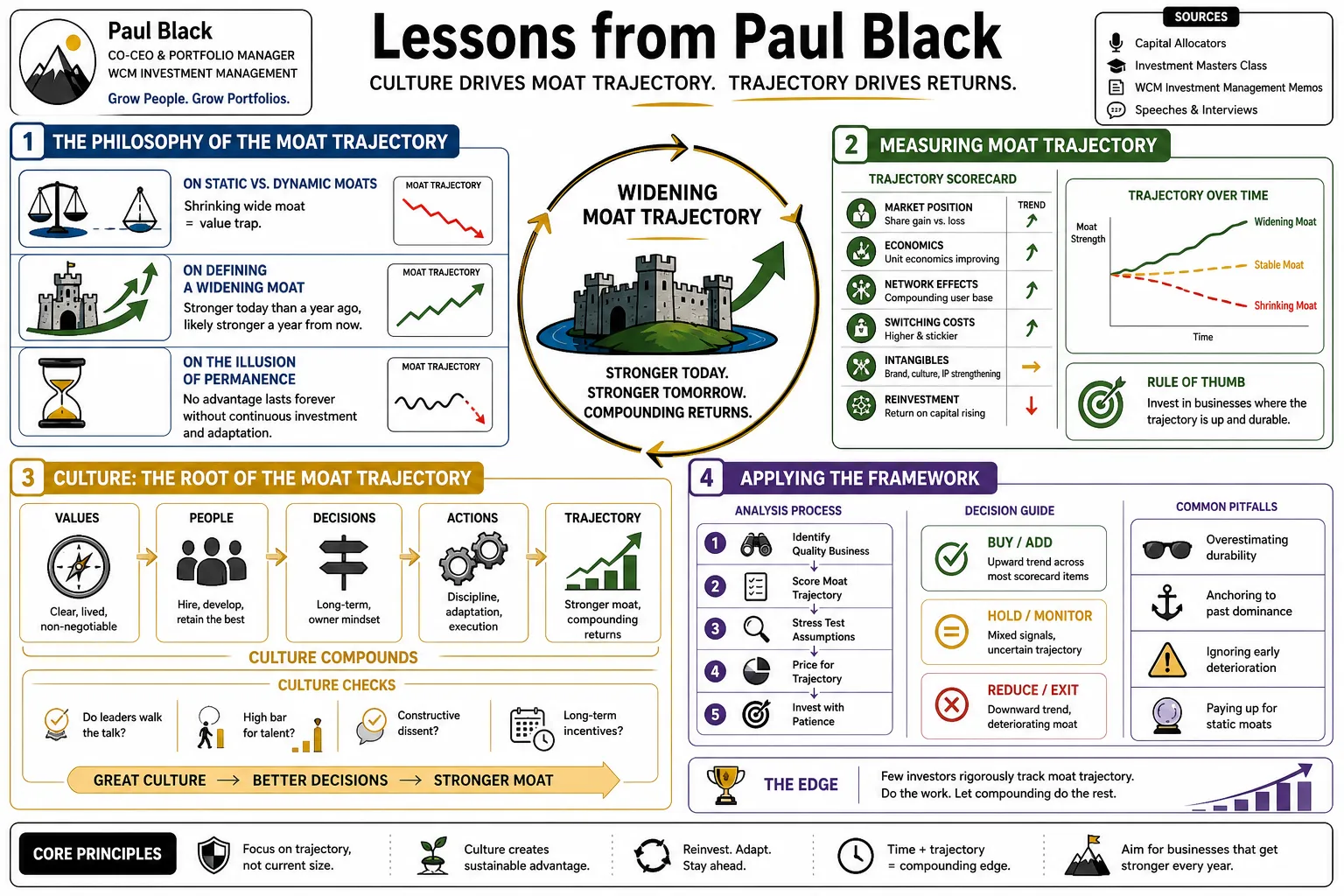

Part 1: The Philosophy of the Moat Trajectory

- On static vs. dynamic moats: "Most investors focus on the current size of a competitive advantage, but we found that a shrinking wide moat is a value trap. It is the trajectory of the moat that dictates future returns." — Source: Capital Allocators

- On defining a widening moat: "A widening moat means the company's competitive position is stronger today than it was a year ago, and will likely be stronger a year from now." — Source: Investment Masters Class

- On the illusion of permanence: "No competitive advantage lasts forever without continuous investment and adaptation. Assuming a moat is permanent is the easiest way to lose money." — Source: WCM Investment Management Memos

- On measuring trajectory: "You measure trajectory by looking at incremental changes in market share, customer retention, and pricing power over rolling periods, rather than absolute historical margins." — Source: First Trust Podcast

- On the danger of legacy businesses: "Companies that rest on historical success often stop innovating. They look cheap on a screener, but their economic foundation is quietly eroding." — Source: Value Investor Insight

- On compounding advantage: "When a company finds a way to widen its moat, it often creates a flywheel effect. The stronger they get, the easier it becomes to take share from weaker rivals." — Source: Capital Allocators

- On spotting shrinking moats: "Shrinking moats often mask themselves with aggressive share buybacks or cost cutting. These actions prop up earnings per share while the underlying business deteriorates." — Source: Invest Like the Best

- On the importance of direction: "I would rather own a business with a narrow but widening moat than a business with a massive but shrinking moat." — Source: Investment Masters Class

- On competitive fade: "The natural law of capitalism is mean reversion. To defy the fade, a company must have a mechanism to constantly reinforce its barriers to entry." — Source: First Trust Podcast

- On long-term predictability: "A widening moat is the only reliable indicator we have found that a company can sustain high returns on invested capital over a decade or more." — Source: WCM Investment Management Memos

Part 2: Culture as a Competitive Advantage

- On culture and moats: "Culture is the DNA of the moat. If the moat is the output, the corporate culture is the essential input that produces it." — Source: Capital Allocators

- On defining culture: "Culture is simply the collective behavior of the people inside an organization when nobody is watching. It dictates how they respond to stress and opportunity." — Source: What Got You There

- On assessing culture: "You cannot read about a company's culture in a regulatory filing. You have to speak with former employees, competitors, and suppliers to understand what is actually rewarded internally." — Source: Value Investor Insight

- On alignment: "A great culture is one that perfectly aligns with the company's specific competitive advantage. A cost leader needs a frugal culture; an innovator needs a culture of psychological safety." — Source: First Trust Podcast

- On cultural decay: "When a business starts losing its competitive edge, the root cause is almost always a breakdown in the culture that occurred years prior." — Source: Investment Masters Class

- On culture as a shield: "A strong culture acts as an immune system. It rejects bad hires, bad ideas, and bad behavior before they can compromise the core business." — Source: Capital Allocators

- On replicating success: "Competitors can copy your product, your pricing, and your marketing strategy. They cannot easily copy the ingrained behaviors and trust within your workforce." — Source: WCM Investment Management Memos

- On leadership transitions: "The ultimate test of a culture is whether it survives the departure of a charismatic founder. If the culture relies entirely on one person, it is a vulnerability." — Source: Invest Like the Best

- On toxic environments: "High turnover, internal politics, and a focus on short-term metrics are leading indicators that a company's competitive advantage is about to shrink." — Source: Value Investor Insight

- On the ROI of culture: "Investing in culture shows up in tangible financial outcomes like lower customer acquisition costs, higher employee retention, and better capital allocation." — Source: What Got You There

Part 3: Leadership, Ego, and Empowerment

- On ego in leadership: "Ego is the enemy of compounding. Leaders who need to be the smartest person in the room inevitably stifle the growth of the people around them." — Source: Capital Allocators

- On empowerment: "The best CEOs view their job as building an environment where great decisions can be made at the lowest possible level, rather than making all the decisions themselves." — Source: What Got You There

- On honest feedback: "Real kindness in a professional setting includes giving honest and direct feedback. Allowing someone to underperform without telling them is a failure of leadership." — Source: First Trust Podcast

- On setting the tone: "The leader sets the emotional atmosphere of the organization. If the leader is defensive and reactive, the entire company will adopt a defensive posture." — Source: Invest Like the Best

- On hiring better than yourself: "A true mark of a healthy organization is when senior leaders are actively recruiting people who are more talented than they are without feeling threatened." — Source: Investment Masters Class

- On humility: "Humility allows a leader to change their mind when presented with new facts. Arrogance forces a leader to defend a bad decision to save face." — Source: WCM Investment Management Memos

- On decentralized authority: "When you push decision-making down to the people closest to the customer, you increase the speed of the organization and widen the moat." — Source: Capital Allocators

- On managing growth: "As a firm scales, the founder must transition from being a doer to being an architect of systems and culture. Many fail to make this leap." — Source: What Got You There

- On succession planning: "Great leaders start thinking about their successor the day they take the job. They view their tenure as a temporary stewardship of the culture." — Source: First Trust Podcast

Part 4: Learning from Failure and Post-Mortems

- On the necessity of failure: "If you are not experiencing failure, you are not taking enough risk. The goal is not to avoid failure, but to survive it and extract the lesson." — Source: Capital Allocators

- On investment post-mortems: "We instituted rigorous post-mortems for our biggest mistakes. We dissect what went wrong, not to assign blame, but to update our mental models." — Source: Investment Masters Class

- On intellectual honesty: "It is incredibly painful to admit you were wrong about a thesis you defended publicly. But intellectual honesty is the only way to improve your hit rate over time." — Source: Value Investor Insight

- On pattern recognition: "Analyzing your losers is how you build pattern recognition. You start to see the early warning signs of cultural decay or moat erosion much faster." — Source: Invest Like the Best

- On avoiding the blame game: "A culture that punishes honest mistakes will soon find that employees hide bad news. You must reward the prompt reporting of failure." — Source: What Got You There

- On doubling down: "The worst mistakes usually happen when ego gets involved and you double down on a losing position to prove the market wrong. You have to know when to cut." — Source: Capital Allocators

- On continuous improvement: "Every failure should result in a tangible change to your process. If a mistake does not change how you work, it was a wasted opportunity." — Source: WCM Investment Management Memos

- On behavioral biases: "Post-mortems often reveal that the error was not in the spreadsheet, but in our own behavioral biases like falling in love with management or ignoring disconfirming evidence." — Source: First Trust Podcast

- On organizational resilience: "A firm's longevity is directly tied to its ability to absorb a heavy blow, figure out why it happened, and rebuild stronger." — Source: Investment Masters Class

Part 5: Identifying Sustainable Growth

- On organic vs. acquired growth: "We heavily prefer businesses that can grow organically. Serial acquirers often destroy value and dilute their culture in the pursuit of revenue growth." — Source: Value Investor Insight

- On total addressable market: "A large market is meaningless if the company cannot defend its share. We look for companies that dominate a specific niche and then expand outward into adjacencies." — Source: Capital Allocators

- On pricing power: "The clearest evidence of a widening moat is the ability to raise prices without losing customers. If a company sweats every time it raises prices, the moat is thin." — Source: First Trust Podcast

- On customer pain points: "Sustainable growth comes from systematically removing friction for the customer. The companies that do this best capture the most value." — Source: Invest Like the Best

- On capital light business models: "Businesses that can grow without requiring massive continuous capital expenditures have a structural advantage. They generate free cash flow that can be reinvested into widening the moat." — Source: WCM Investment Management Memos

- On tailwinds: "You want to invest in businesses that are riding structural multi-decade tailwinds. It is much easier to swim with the current than against it." — Source: Investment Masters Class

- On global scalability: "We look for business models and cultures that translate across borders. A localized advantage is good, but a globally scalable advantage creates massive compounders." — Source: Capital Allocators

- On switching costs: "Growth is far more sustainable when a product becomes so deeply embedded in a customer's workflow that ripping it out introduces unacceptable business risk." — Source: Value Investor Insight

- On network effects: "A network effect is one of the most powerful moat-widening dynamics. Every new user adds value to the existing user base, making the service harder to displace." — Source: Invest Like the Best

- On reinvestment runways: "Growth slows when a company runs out of profitable places to deploy capital. We hunt for management teams that have identified long runways for internal reinvestment." — Source: What Got You There

Part 6: Building a High-Performance Organization

- On alignment of incentives: "Show me the incentive structure, and I will show you the company's future. If you reward short-term earnings, you will get short-term behavior at the expense of the long term." — Source: First Trust Podcast

- On hiring for adaptability: "We prioritize adaptability and curiosity over raw intellect. The market changes too fast to rely on people who are rigid in their thinking." — Source: Capital Allocators

- On the value of debate: "A high-performance team requires cognitive diversity and the psychological safety to argue fiercely about ideas without making it personal." — Source: What Got You There

- On removing toxicity: "You can have a brilliant analyst, but if they are toxic to the culture, they are a net negative to the firm's overall performance. You have to let them go." — Source: Investment Masters Class

- On fostering ownership: "When employees feel like owners, they stop optimizing for their own bonuses and start optimizing for the health of the enterprise." — Source: WCM Investment Management Memos

- On shared language: "Great organizations develop an internal vocabulary. It creates a shorthand for complex concepts and reinforces the culture with every conversation." — Source: Invest Like the Best

- On continuous learning: "The best firms treat learning as a core competency. They are always reading, always benchmarking against competitors, and always trying to break their own models." — Source: Capital Allocators

- On structural simplicity: "Complexity is the enemy of execution. Keep the organizational chart flat so that information travels from the front lines to the decision makers without distortion." — Source: Value Investor Insight

- On celebrating small wins: "Momentum is a real force in organizations. By celebrating small improvements in the moat or the culture, you build the confidence needed to tackle massive challenges." — Source: First Trust Podcast

Part 7: Investment Strategy and Risk Management

- On defining risk: "Risk is not volatility. Volatility is just the price you pay for liquidity. Real risk is the permanent impairment of capital caused by buying a structurally flawed business." — Source: Capital Allocators

- On portfolio concentration: "If you truly understand the trajectory of a company's moat, you should be willing to concentrate your capital. Diversification often serves as a hedge against ignorance." — Source: Value Investor Insight

- On ignoring macro noise: "Macroeconomic predictions are notoriously unreliable. We prefer to spend our time analyzing the micro-economics of individual businesses, which we can actually understand." — Source: Investment Masters Class

- On valuation: "Valuation is a secondary metric for us. A cheap company with a shrinking moat is a bad investment, while an expensive company with a widening moat often grows into its valuation over time." — Source: Invest Like the Best

- On patience: "The hardest part of investing is doing nothing. Once you own a great business with a widening moat, the most profitable action is usually to just sit on your hands." — Source: WCM Investment Management Memos

- On selling discipline: "We sell when the culture breaks down, when the moat begins to shrink, or when we find an inherently superior business. We do not sell just because the stock went up." — Source: First Trust Podcast

- On avoiding turnaround stories: "Turnarounds seldom turn. It takes a monumental effort to reverse a shrinking moat, and as outside investors, we prefer to bet on established winners." — Source: Capital Allocators

- On information edge: "The edge today is not in getting information faster; it is in interpreting public information through a better framework like analyzing the cultural alignment of a firm." — Source: What Got You There

- On position sizing: "Position sizing should be dictated by your conviction in the moat's trajectory and the quality of the culture, rather than by the historical volatility of the stock." — Source: Value Investor Insight

Part 8: Long-Term Thinking and Compounding

- On the eighth wonder of the world: "Compounding only works if you do not interrupt it unnecessarily. The taxes and friction of constant trading destroy the math of long-term wealth creation." — Source: Investment Masters Class

- On time horizons: "Most of Wall Street is trying to guess what will happen in the next quarter. We are trying to determine what a business will look like in a decade. That time arbitrage is our biggest advantage." — Source: Capital Allocators

- On surviving drawdowns: "To hold a stock for ten years, you have to be willing to look foolish for two or three of those years. If you cannot stomach a drawdown, you cannot compound." — Source: Invest Like the Best

- On the nature of great companies: "Great companies are rarely built overnight. They are the result of thousands of small, correct decisions made by an aligned culture over many years." — Source: WCM Investment Management Memos

- On filtering out noise: "To think long-term, you must actively curate your information diet. Stop reading the daily market commentary and start reading books on history, psychology, and systems." — Source: What Got You There

- On legacy: "As a firm, our goal is to build an institution that outlives its founders and consistently delivers for our clients, rather than merely generating short-term alpha." — Source: First Trust Podcast

- On alignment with clients: "You cannot invest for the long term if your client base has a short-term horizon. You must attract investors who understand and embrace your philosophy." — Source: Capital Allocators

- On constant evolution: "Even our investment process must have a widening moat. We are constantly tweaking our frameworks and learning from our history to ensure we do not become obsolete." — Source: Value Investor Insight

- On the ultimate goal: "At the end of the day, investing is about finding exceptional people building exceptional things, and providing them the capital to keep going." — Source: Investment Masters Class