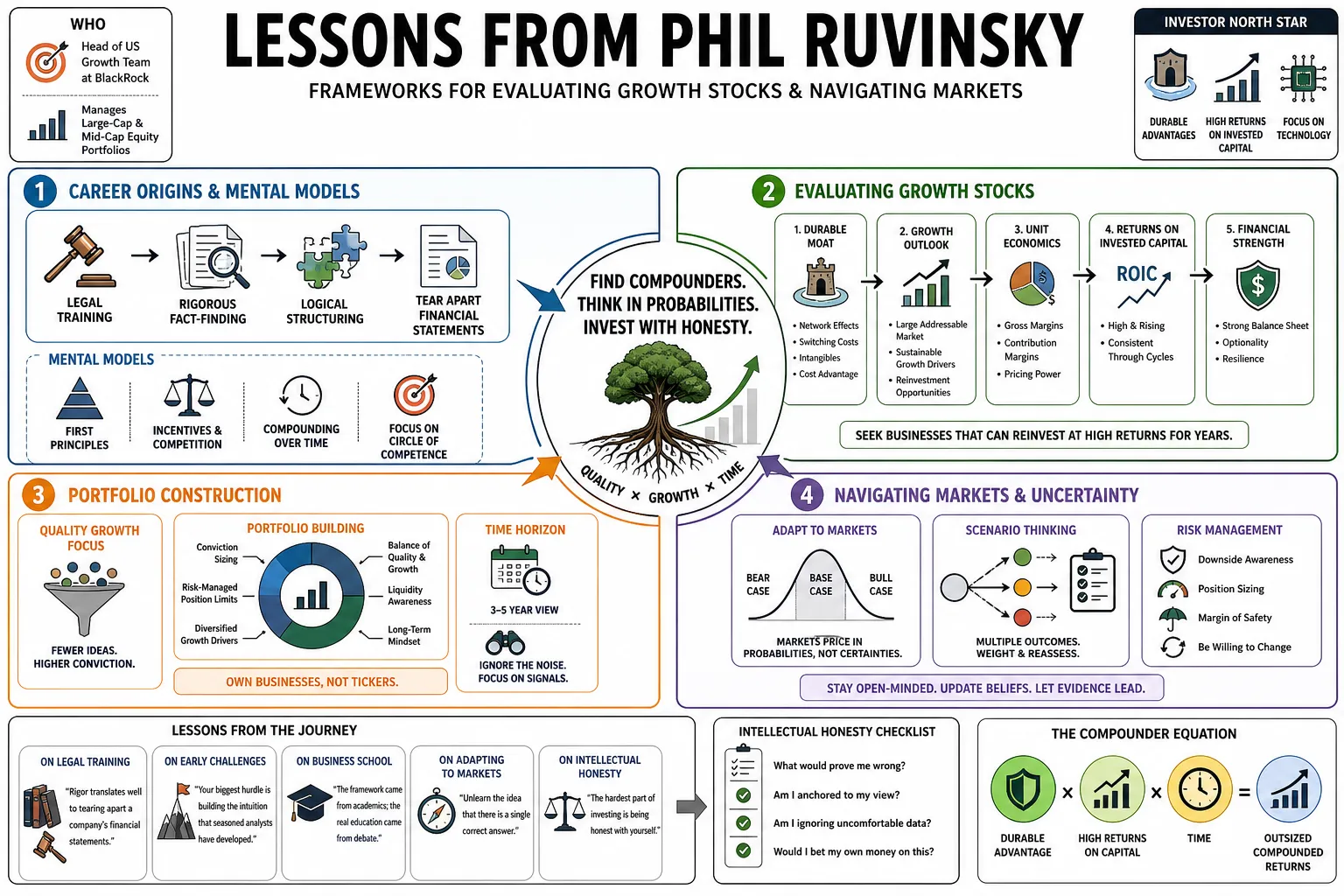

Phil Ruvinsky is the Head of the US Growth Team at BlackRock, where he manages large-cap and mid-cap equity portfolios. He built his career by identifying companies with durable competitive advantages and high returns on invested capital, especially within the technology sector. This profile breaks down his framework for evaluating growth stocks, constructing portfolios, and navigating market shifts.

Part 1: Career Origins and Mental Models

- On Legal Training: "The rigorous fact-finding and logical structuring required in law translate surprisingly well to tearing apart a company's financial statements." — Source: [Value Investing with Legends]

- On Early Challenges: "When you transition from a completely different discipline, your biggest hurdle is building the intuition that seasoned analysts have developed over a decade." — Source: [Value Investing with Legends]

- On Business School: "The academic environment provided the formal framework, but the real education came from debating valuation models with peers who saw the world differently." — Source: [Value Investing with Legends]

- On Adapting to Markets: "You have to unlearn the idea that there is a single correct answer. Markets price in probabilities, not certainties." — Source: [Columbia Business School]

- On Intellectual Honesty: "The hardest part of the job is admitting when your initial thesis was wrong and the market was right." — Source: [Columbia Business School]

- On Building Conviction: "Conviction does not come from a spreadsheet. It comes from understanding the underlying unit economics better than the marginal seller." — Source: [BlackRock Author Profile]

- On Continuous Learning: "The half-life of knowledge in technology investing is incredibly short. If you stop reading, you fall behind in months." — Source: [BlackRock Author Profile]

- On Seeking Disconfirming Evidence: "I spend more time trying to figure out why a company might fail than why it might succeed." — Source: [Value Investing with Legends]

- On Patience: "Sometimes the best action to take in a volatile market is to sit on your hands and trust the work you did when things were calm." — Source: [Value Investing with Legends]

Part 2: Fundamental Investment Philosophy

- On Growth Equity: "True growth investing is not about paying any price for revenue expansion; it is about finding businesses where cash flows will compound predictably over long durations." — Source: [BlackRock Active Equities]

- On Quality: "A high-quality business generates excess cash and has intelligent places to deploy it without damaging its core returns." — Source: [Value Investing with Legends]

- On Return on Invested Capital: "ROIC is the single most important metric. A company that cannot generate a return above its cost of capital is simply destroying value as it grows." — Source: [Some ROIC Mentions]

- On Valuation: "Valuation is a sanity check, not a starting point. We look at the business quality first and ask what price makes sense second." — Source: [BlackRock Active Equities]

- On Margin Expansion: "Investors often model linear margin expansion, but in reality, margins expand in step-functions as a company scales past its fixed cost base." — Source: [Value Investing with Legends]

- On Free Cash Flow: "Earnings can be manipulated by accounting assumptions, but free cash flow tells you the actual economic reality of the enterprise." — Source: [BlackRock Active Equities]

- On Long-Term Thinking: "The market is obsessed with the next quarter's earnings. We look for companies optimizing for the next five years of market share." — Source: [Value Investing with Legends]

- On Intangible Assets: "Traditional accounting does a poor job of capturing the value of a loyal customer base or a proprietary data set." — Source: [Value Investing with Legends]

- On Risk Management: "Risk is not volatility. Risk is the permanent impairment of capital because you misunderstood the business model." — Source: [BlackRock Active Equities]

- On The Role of Analysts: "An analyst's job is to figure out what a company is worth; a portfolio manager's job is to figure out how much of it to own." — Source: [Value Investing with Legends]

Part 3: Identifying Sustainable Competitive Advantages

- On Network Effects: "The strongest moat in modern business is a two-sided network where every new user makes the product better for existing users." — Source: [Value Investing with Legends]

- On Switching Costs: "You want to invest in software that becomes so deeply embedded in a customer's daily operations that removing it would disrupt their business." — Source: [BlackRock US Growth Strategy]

- On Scale Economies: "Scale only matters if it translates into a lower cost per unit that can be passed on to customers or dropped to the bottom line." — Source: [Value Investing with Legends]

- On Brand Equity: "A brand is only a moat if it allows a company to charge a premium price without losing market share." — Source: [BlackRock US Growth Strategy]

- On Durability: "We are constantly asking ourselves what this business will look like in ten years and what forces could potentially dislodge it." — Source: [Value Investing with Legends]

- On Disruption: "Incumbents rarely die from a single blow; they die from a thousand cuts delivered by faster, more focused upstarts." — Source: [Value Investing with Legends]

- On Pricing Power: "The ultimate test of a competitive advantage is whether a company can raise prices without having a meeting about it." — Source: [Value Investing with Legends]

- On Distribution: "Having the best product is useless if you don't own the channel to deliver it to the end consumer efficiently." — Source: [Value Investing with Legends]

- On Competitive Strategy: "Strategy is about choosing what not to do. Companies that try to be everything to everyone usually end up with no moat at all." — Source: [Columbia Business School]

Part 4: Analyzing the Technology Sector

- On Software as a Service: "The SaaS model is beautiful because it smooths out revenue recognition, but you have to watch customer acquisition costs very closely." — Source: [Value Investing with Legends]

- On Semiconductors: "Semiconductors have moved from highly cyclical commodities to the foundational infrastructure of the digital economy." — Source: [BlackRock US Growth Strategy]

- On Cloud Computing: "The migration to the cloud is a multi-decade transition, and we are still in the middle innings of workload migration." — Source: [Value Investing with Legends]

- On Cybersecurity: "Security is no longer a discretionary IT expense; it is a board-level mandate that commands a growing share of enterprise budgets." — Source: [BlackRock Active Equities]

- On Consumer Tech: "In consumer technology, user engagement metrics are often more predictive of future cash flows than current quarterly revenue." — Source: [Value Investing with Legends]

- On Platform Companies: "The most valuable technology companies are platforms that enable other businesses to build upon them." — Source: [Value Investing with Legends]

- On Hardware Margins: "Hardware businesses are notoriously difficult because the replacement cycles are unpredictable and the margin degradation is constant." — Source: [Value Investing with Legends]

- On Telecom: "The telecom sector requires massive upfront capital expenditures, making it a game of scale and regulatory navigation." — Source: [BlackRock Active Equities]

- On Tech Valuations: "High multiples in tech can be justified if the terminal market size is massive and the unit economics improve with scale." — Source: [Value Investing with Legends]

- On R&D Spending: "We view R&D not as an expense, but as a reinvestment into the company's future moat." — Source: [Some ROIC Mentions]

Part 5: The Impact of Artificial Intelligence

- On Generative AI: "Generative AI is a platform shift on par with mobile or the internet, forcing us to re-evaluate the competitive positioning of every company we follow." — Source: [Value Investing with Legends]

- On AI Infrastructure: "The early winners in AI are the companies selling the picks and shovels: the silicon and the data center architecture required to run these models." — Source: [Value Investing with Legends]

- On Data Assets: "In an AI-driven world, proprietary data is the new oil. The models are commoditizing, but unique data sets cannot be easily replicated." — Source: [Value Investing with Legends]

- On Productivity: "AI will drive massive productivity gains across the economy, but the value will accrue unevenly between software vendors and their enterprise customers." — Source: [Value Investing with Legends]

- On Coding and Engineering: "AI coding assistants are changing the economics of software development, lowering the barrier to entry for new applications." — Source: [BlackRock US Growth Strategy]

- On Disruption Risk: "Companies relying on basic information retrieval or low-level cognitive tasks face an immediate threat from AI." — Source: [Value Investing with Legends]

- On The Investment Process: "We are actively integrating AI tools to parse transcripts and analyze data sets, but human judgment remains the final filter." — Source: [Value Investing with Legends]

- On Capital Intensity: "Training foundational models is incredibly capital intensive, limiting the field to a few massive hyperscalers with deep pockets." — Source: [Value Investing with Legends]

- On Hype Cycles: "We have to separate the structural AI winners from the companies simply adding keywords to their earnings scripts to boost their multiples." — Source: [Value Investing with Legends]

Part 6: Nuances of Portfolio Construction

- On Portfolio Concentration: "We prefer to own fewer companies that we understand deeply rather than spreading capital thinly across a hundred mediocre ideas." — Source: [Value Investing with Legends]

- On Sizing Positions: "Position size should reflect both the asymmetry of the potential return and your level of conviction in the thesis." — Source: [BlackRock Active Equities]

- On Trimming Winners: "It is painful to sell a stock that is doing well, but you have to enforce discipline when the valuation disconnects from the underlying fundamentals." — Source: [Value Investing with Legends]

- On Adding to Losers: "A declining stock price is not a reason to buy more; you must re-underwrite the thesis to ensure the intrinsic value hasn't also declined." — Source: [Value Investing with Legends]

- On Cash Drag: "Holding too much cash in a growth portfolio can severely hinder long-term compounding, so we stay fully invested when we find quality." — Source: [BlackRock US Growth Strategy]

- On Sector Limits: "We don't manage strictly to benchmark sector weights; if the best opportunities are concentrated in software, that is where we will deploy capital." — Source: [Value Investing with Legends]

- On Idea Generation: "The best ideas rarely come from Wall Street research; they come from reading industry journals, talking to competitors, and tracking supply chains." — Source: [Value Investing with Legends]

- On Avoiding Value Traps: "A low multiple usually means the market believes the cash flows are structurally impaired. It is our job to figure out if the market is right." — Source: [BlackRock Active Equities]

- On Portfolio Balance: "You want a mix of steady compounders and higher-velocity names where the market is mispricing a near-term inflection." — Source: [Value Investing with Legends]

- On The Macro Environment: "We monitor the macro environment, but we don't build portfolios based on interest rate forecasts; we build them based on company fundamentals." — Source: [Value Investing with Legends]

Part 7: Navigating Market Trends and Indexing

- On Indexing: "The rise of passive investing has created inefficiencies. When rules-based buyers purchase without regard to price, it leaves opportunities for fundamental stock pickers." — Source: [Value Investing with Legends]

- On Market Concentration: "The current concentration in the top names reflects the reality that these mega-caps have achieved unprecedented scale and profitability." — Source: [Value Investing with Legends]

- On Active Management: "Active management proves its worth during market dislocations when correlations break down and individual business quality dictates outcomes." — Source: [BlackRock Active Equities]

- On Liquidity: "Liquidity is an illusion until you actually need it. We heavily favor companies with deep daily trading volumes." — Source: [Value Investing with Legends]

- On Retail Participation: "Retail flows can cause short-term distortions, but over a five-year horizon, cash flow generation is what dictates the stock price." — Source: [Value Investing with Legends]

- On Price Discovery: "As passive vehicles grow, price discovery relies on a shrinking pool of active managers, which paradoxically makes deep fundamental research more valuable." — Source: [Value Investing with Legends]

- On Volatility: "Volatility is not a risk to be avoided; it is the mechanism that allows us to acquire great assets at a discount." — Source: [Columbia Business School]

- On Regulatory Shifts: "Antitrust scrutiny in the tech sector is a reality, but many of these companies have such ingrained utility that regulatory fines act merely as a speed bump." — Source: [Value Investing with Legends]

- On Growth vs. Value: "The debate between growth and value is largely semantic. All investing is value investing if you are paying less than the present value of future cash flows." — Source: [Value Investing with Legends]

Part 8: Corporate Governance and Capital Allocation

- On Management Evaluation: "You cannot model culture in a spreadsheet, but a poor culture will eventually destroy the best business model." — Source: [Value Investing with Legends]

- On Capital Allocation: "A CEO's most important job is capital allocation. Retaining earnings only makes sense if they can reinvest at high rates of return." — Source: [Some ROIC Mentions]

- On Share Repurchases: "Buybacks are brilliant when the stock is undervalued, but value-destructive when management buys back shares at cyclical peaks just to offset dilution." — Source: [Value Investing with Legends]

- On Dividends: "For mature tech companies, initiating a dividend imposes discipline on management and signals that hyper-growth is transitioning to steady cash flow." — Source: [BlackRock Active Equities]

- On M&A Strategy: "Most large acquisitions fail to create value. We prefer companies that pursue smaller bolt-on acquisitions that integrate easily into their existing platform." — Source: [Value Investing with Legends]

- On Executive Compensation: "Incentives drive outcomes. We scrutinize proxy statements to ensure management is paid on metrics like ROIC rather than pure revenue growth." — Source: [Value Investing with Legends]

- On Founder-Led Companies: "Founders often have a longer time horizon than hired executives, which aligns well with our investment philosophy." — Source: [Value Investing with Legends]

- On Board Independence: "A strong, independent board is necessary to push back against a charismatic CEO who wants to pursue a pet project at the expense of shareholders." — Source: [BlackRock Active Equities]

- On Stock-Based Compensation: "Stock-based compensation is a real expense. Ignoring it inflates cash flow numbers and misrepresents the true economic profitability of the business." — Source: [Value Investing with Legends]